Editorial Integrity

Making informed real estate decisions starts with having the right knowledge. At HomeAbroad, we offer US mortgage products for foreign nationals & investors and have a network of 500+ expert HomeAbroad real estate agents to provide the expertise you need. Our content is written by licensed mortgage experts and seasoned real estate agents who share insights from their experience, helping thousands like you. Our strict editorial process ensures you receive reliable and accurate information.

Key Takeaways:

1. HomeAbroad offers DSCR loans specifically for foreign nationals investing in US real estate, with no US credit history or income documentation required.

2. A DSCR of 1.0 or higher is typically required for the best terms, showing the property covers its expenses.

3. HomeAbroad’s DSCR loans require a minimum 25% down payment and 6 months of cash reserves.

4. DSCR loans make it easier for foreign nationals to invest in US real estate and scale their portfolio without being limited by DTI requirements.

Table of Contents

DSCR loan requirements for investment property in 2026 typically include a minimum DSCR ratio (usually 1.0 or higher), a down payment, and sufficient cash reserves. These requirements are designed to ensure the property generates enough income to cover its loan payments.

At HomeAbroad, our DSCR loans are structured around the property’s cash flow rather than your personal income, making them accessible for foreign nationals who may not have a US credit history or traditional income documentation.

Based on the DSCR loans we’ve structured for foreign nationals, DSCR loan approvals often come down to how well the deal is structured. Rental income, expense assumptions, and reserve positioning tend to matter more than simply meeting minimum thresholds on paper.

This guide breaks down each requirement in detail, covering eligibility criteria, property requirements, DSCR calculation, and how to qualify for a DSCR loan for investment property in 2026.

DSCR Loan Requirements for Investment Property in 2026

Our DSCR loan requirements are designed specifically for foreign nationals investing in US real estate.

Here’s a clear breakdown of what we look for:

Feature | Requirement |

|---|---|

DSCR Ratio | ≥ 1.0 for best terms. Eligible down to 0.75 with a higher down payment |

Credit Score | Not required for foreign nationals |

Down Payment | 25% |

LTV | Purchase: Up to 75% |

Cash Reserves | 6 Months |

Loan Amount | >=$100K – $10M |

These requirements are structured to make DSCR loans accessible to foreign investors, even without US income or credit history. The flexibility in DSCR ratio and loan structure allows you to qualify based on the strength of the property rather than traditional financial documentation.

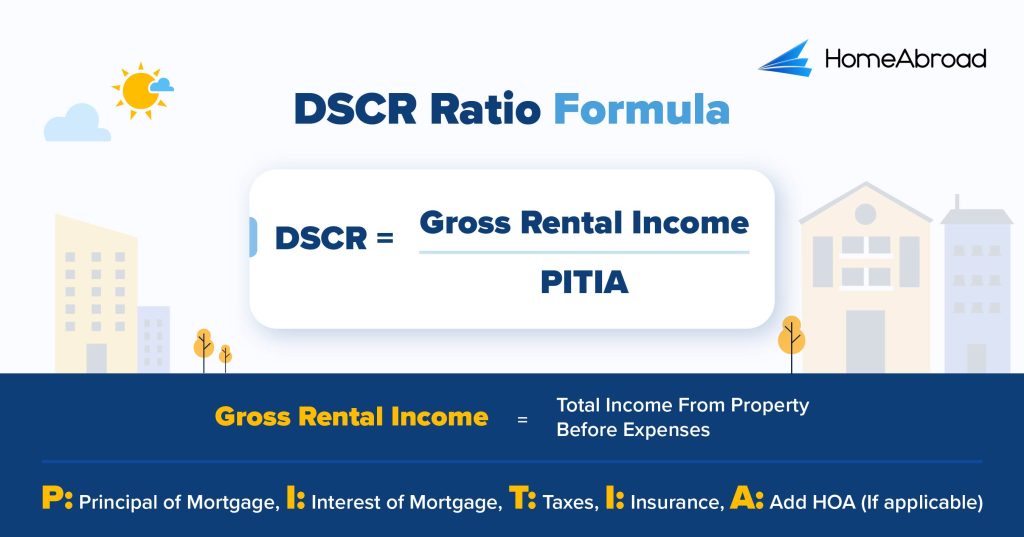

How DSCR Is Calculated for Loan Qualification

DSCR (Debt Service Coverage Ratio) measures whether a property’s income is enough to cover its loan payments. It’s the core metric we used to qualify for a DSCR loan.

The formula is simple:

This means the property generates 23% more income than required to cover its expenses, which strengthens the loan application.

The DSCR ratio shows how much income a property generates compared to its monthly expenses:

-

DSCR > 1.0 → Positive cash flow (property earns more than it’s expenses)

DSCR > 1.0 → Positive cash flow (property earns more than it’s expenses) - DSCR = 1.0 → Break-even (income equals expenses)

- DSCR < 1.0 → Property income does not fully cover loan expenses

A stronger DSCR ratio and lower LTV generally result in more favorable interest rates. Check out current DSCR loan rates here to see what you can expect based on your deal structure.

At HomeAbroad, a DSCR of 1.0 or higher typically qualifies for the best loan terms. For properties that fall below this threshold, we offer a No-Ratio DSCR Program that allows investors to still qualify for financing.

This program is designed for investors with strong long-term plans whose properties may not yet meet the 1.0 threshold. It requires a slightly larger down payment (a 5% hit to LTV) and carries higher interest rates compared to standard DSCR terms.

Understanding the DSCR calculation before you apply helps you evaluate properties more accurately and structure deals that qualify from the start. Use our DSCR loan calculator to run your numbers before applying.

DSCR Loan Property Requirements: What Types of Properties Qualify?

DSCR loan approval doesn’t just depend on numbers, the property itself must meet certain requirements. At HomeAbroad, we evaluate whether the property can generate stable, predictable income and meets basic eligibility standards for financing.

Eligible Property Types

DSCR loans are designed for investment properties, and most residential income-producing properties qualify, including:

- Single-family homes (SFR)

- 2–4 unit multifamily properties

- Condos and townhomes (subject to project eligibility)

- Short-term rental properties (Airbnb/STR)

Properties that generate consistent rental income are generally easier to qualify, especially under standard DSCR requirements.

Ineligible Property Types

Not all properties qualify for DSCR loans. At HomeAbroad, the following property types are typically not eligible:

- Primary residences or owner-occupied properties

- Properties requiring major renovations or not move-in ready

- Land or undeveloped properties

- Non-income-generating properties

The reason this matters is that DSCR loans are designed specifically for income-producing investment properties, so the property must be capable of generating stable rental income.

Property Condition and Appraisal Requirements

The property must be move-in ready and income-generating at the time of financing. An appraisal is required to determine the property’s market value and estimate rental income through a rent schedule or comparable market data.

An appraisal is required to:

- Determine the property’s market value

- Estimate rental income (through rent schedule or comparable data)

This rental estimate plays a key role in DSCR calculation and loan approval.

Choosing the right property is just as important as meeting financial requirements. A property with stable rental potential and clean appraisal data significantly improves your chances of DSCR loan approval.

DSCR Loan Requirements vs Conventional Loan Requirements for Investment Property

DSCR loans and conventional loans for investment properties follow very different qualification approaches. The key difference is that DSCR loans qualify the property, while conventional loans qualify the borrower.

Feature | DSCR Loan | Conventional Loan |

|---|---|---|

Qualification Basis | Property income (DSCR) | Personal income (DTI) |

Income Verification | Not required | Required (W-2, tax returns) |

Credit Requirement | no US credit required at HomeAbroad | Strong US credit required |

Down Payment | 25% | Typically 20–25% |

Scalability | No DTI limits → easier to scale portfolio | Limited by DTI and income |

When a DSCR Loan Makes More Sense

DSCR loans are ideal when:

- You don’t have US income or credit history

- Your property generates strong rental income

- You want a simpler qualification process based on the deal

- You plan to scale your portfolio without being limited by DTI

When a Conventional Loan May Work Better

Conventional loans may be a better fit if:

- You have a stable US income and strong credit

- You meet strict DTI requirements

The distinction here is that DSCR loans offer more flexibility for investors, especially foreign nationals, while conventional loans rely heavily on personal financial qualification and DTI limits.

Common Mistakes That Affect DSCR Loan Approval

DSCR loans are straightforward on paper, but in practice, small missteps can delay or even derail approval. Most issues come from how the deal is structured rather than the borrower itself.

Overestimating Rental Income

One of the most common mistakes is relying on online rent estimates or optimistic projections. DSCR loans are based on appraisal-supported rental income, which often comes in lower than what platforms like Zillow or AirDNA project.

A pattern we’ve noticed is that a $300–$450 difference in monthly rent is enough to drop a DSCR from 1.15 to below 1.0, changing the loan structure entirely. Running conservative numbers before applying avoids a late-stage surprise.

Ignoring Full PITIA Costs

Many investors calculate DSCR using only principal and interest, leaving out taxes, insurance, or HOA dues. This leads to an inflated DSCR that doesn’t match lender calculations. The distinction here is that DSCR is based on total housing expense (PITIA), not just the loan payment.

Not Planning Cash Reserves Early

Some investors focus entirely on the DSCR ratio and overlook cash reserve requirements. Even with a strong DSCR, insufficient reserves can slow down or impact approval. Reserves need to be liquid, seasoned, and in place before closing.

Choosing the Wrong Property Type

Not all investment properties qualify under DSCR programs. Properties requiring major renovation, non-warrantable condos, or properties with HOA restrictions on rentals can create eligibility issues that aren’t discovered until late in the process. Confirming property eligibility early avoids delays down the line.

Poor Documentation of Rental Income

For long-term rentals, we want to see current lease agreements. For short-term rentals, rental history or platform data may be required. Gaps in documentation or inconsistent income records can raise questions during underwriting, even when the income itself is sufficient.

Avoiding these mistakes comes down to preparation. When the income is accurately estimated, costs are fully accounted for, and documentation is in order before applying, most DSCR deals move through underwriting without significant issues.

How to Qualify for a DSCR Loan Faster

Most DSCR loan delays don’t come from the property or the borrower. They come from preparation gaps that surface during underwriting. Addressing these early keeps the process moving.

- Get Your Rental Income Estimate Right from the Start: Before applying, research comparable rental data in your target market. Your DSCR ratio is based on the appraiser’s rent schedule, not your projections. Going in with a realistic number avoids surprises once the appraisal comes back.

- Account for Full PITIA Before Running Your Numbers: Calculate your DSCR using total monthly housing expenses, including property taxes, insurance, and HOA dues, not just principal and interest. Investors who do this upfront rarely face qualification issues tied to expense miscalculation.

- Have Your Reserves Ready and Documented: Reserves need to be liquid, seasoned for at least 60 to 90 days, and clearly documented before you apply. Last-minute fund transfers or undocumented deposits slow down underwriting significantly.

- Choose the Right Property Type Early: Confirm that your target property qualifies under DSCR guidelines before going under contract. Non-warrantable condos, properties with rental restrictions, or those requiring major renovation can disqualify a deal at a late stage.

What we’ve found in practice is that borrowers who prepare their income documentation, reserve statements, and property details before typically move from application to approval significantly faster than those who gather documents reactively during underwriting.

Qualify for a DSCR Loan Today with HomeAbroad

DSCR loans have changed how real estate investors qualify for financing by shifting the focus from personal income to property performance. Instead of relying on traditional income documentation or credit history, DSCR loan requirements are built around rental income, making them a practical option for foreign nationals investing in US real estate.

Understanding these requirements is key. From DSCR ratio and rental income to reserves and property eligibility, every part of the deal needs to align for smooth approval. Approval often comes down to how well the deal is structured, not just whether it meets minimum criteria on paper.

At HomeAbroad, we specialize in DSCR loans tailored for foreign nationals. Alongside financing, we offer an AI-native US real estate investing platform designed to help you find investment-ready properties that align with your goals.

Beyond financing, we simplify the entire investment process by assisting with key steps such as US bank account setup and LLC formation, helping you move forward with clarity from start to finish.

Get pre-qualified today and see how your investment property qualifies under DSCR loan requirements.

FAQs

Can foreign nationals qualify for a DSCR loan in the US?

Yes, at HomeAbroad, foreign nationals can qualify for DSCR loans based on the property’s rental income without needing US income or credit history.

What is the minimum DSCR ratio required to qualify for a DSCR loan?

At HomeAbroad, a DSCR of 1.0 or higher is generally required to qualify and secure the best loan terms, meaning the property generates enough rental income to fully cover its monthly expenses.

How much down payment is required for a DSCR loan?

At HomeAbroad, DSCR loans typically require a minimum 25% down payment, which helps strengthen the deal and improve overall loan eligibility.

What happens if my DSCR ratio is below 1.0?

At HomeAbroad, you can still qualify through our No-Ratio DSCR Program for properties with a DSCR between 0 and 1. This option comes with a slightly higher down payment (typically a 5% reduction in LTV) and higher interest rates compared to standard DSCR loans.

How long does it take to get approved for a DSCR loan?

At HomeAbroad, we streamline the application process to ensure a smooth experience from loan application to closing. We guarantee that the closing will happen within 30 days.

![DSCR Loan Refinance: How to Qualify & Maximize Benefits [2026]](https://homeabroadinc.com/wp-content/uploads/2024/11/DSCRLoanRefinance.jpg)

![DSCR Loan Rates Today [August, 2026]](https://homeabroadinc.com/wp-content/uploads/2022/09/dscr-loan-interest-rates.png)