Editorial Integrity

Making informed real estate decisions starts with having the right knowledge. At HomeAbroad, we offer US mortgage products for foreign nationals & investors and have a network of 500+ expert HomeAbroad real estate agents to provide the expertise you need. Our content is written by licensed mortgage experts and seasoned real estate agents who share insights from their experience, helping thousands like you. Our strict editorial process ensures you receive reliable and accurate information.

DSCR Loan Pros and Cons: Quick Overview:

Biggest Pro: Qualify based on property's rental income, not personal income

Biggest Con: Slightly Higher interest rates and down payment than conventional loans

Best For: Foreign nationals, self-employed investors, portfolio scaling

Not Ideal For: Primary residence buyers

Minimum Down Payment: 25%

Credit History Required: No US credit history required at HomeAbroad

DSCR loans have become one of the most popular financing options for real estate investors, particularly those who don’t fit the traditional lending mold. But like any loan product, they come with both advantages and limitations that are worth understanding before you apply.

The biggest appeal is straightforward: DSCR loans qualify the property, not the borrower. This means no personal income verification, no employment history, and at HomeAbroad, no US credit history required. For foreign nationals, this removes the barriers that make conventional financing difficult or impossible.

Whether you are evaluating your first US investment property or looking to scale an existing portfolio, this guide breaks down the key pros and cons of DSCR loans, who they work best for, and how to decide if this is the right financing path for your goals.

Table of Contents

What Is a DSCR Loan and How Does It Work?

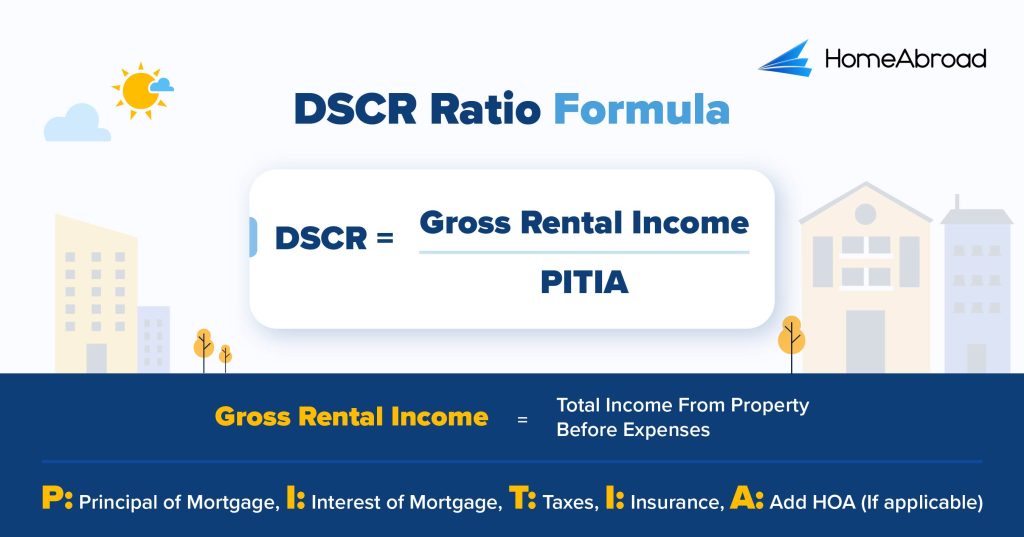

A DSCR loan (Debt Service Coverage Ratio loan) is a type of investment property financing that qualifies borrowers based on the rental income of the property rather than their personal income. Instead of reviewing tax returns, pay stubs, or employment history, lenders evaluate whether the property generates enough income to cover its loan payments.

The qualification is built around one core formula:

A DSCR of 1.0 means the property’s income exactly covers its expenses. Anything above 1.0 means the property generates more income than it costs to finance. At HomeAbroad, a DSCR of 1.0 or higher qualifies for standard terms, and we also offer financing for properties below 1.0 through our No-Ratio DSCR program.

What we consistently see is that investors who understand this formula before evaluating properties make significantly better purchase decisions. The distinction here is simple: DSCR loans shift the qualification from the borrower to the property.

This structure makes DSCR loans particularly well suited for:

-

Foreign nationals without US credit history or income documentation

Foreign nationals without US credit history or income documentation - Self-employed investors whose tax returns don’t reflect actual income

- Investors looking to scale a portfolio without being limited by DTI

For a detailed breakdown of how DSCR is calculated and what lenders look for, see our DSCR loan requirements guide.

DSCR Loan Pros for Real Estate Investors

DSCR loans offer a distinct set of advantages for investors, particularly those who don’t qualify through conventional financing channels. In our experience, these are the benefits that matter most in practice.

1. No Income Verification Required

DSCR loans are qualified entirely on the property’s rental income. There is no requirement to submit tax returns, pay stubs, or employment history. For investors with complex income structures or those who are self-employed, this removes one of the biggest friction points in the loan process.

2. No US Credit History Required

At HomeAbroad, foreign nationals and visa holders can qualify for a DSCR loan without a US credit score or credit history. Qualification is based on the deal itself, not your financial background in the US.

3. Simpler and Faster Qualification Process

Because the focus is on the property rather than the borrower, the documentation requirements are significantly lighter than conventional loans. What we consistently see is that well-prepared DSCR applications move through underwriting faster than almost any other loan type.

4. Portfolio Scalability Without DTI Limits

Conventional loans cap how much you can borrow based on your debt-to-income ratio. DSCR loans have no such limitation. As long as each property covers its own expenses, you can continue adding properties to your portfolio without your personal income becoming a bottleneck.

5. Works for Multiple Property Types

DSCR loans cover a range of investment property types including single-family homes, 2-4 unit multifamily, condos, and short-term rentals. This flexibility allows investors to pursue different strategies under the same loan structure.

6. Accessible for Foreign Nationals

At HomeAbroad, our DSCR loans are specifically designed so foreign nationals and visa holders can qualify without a US credit history, or US tax returns. This opens a direct path to US real estate investment that most conventional programs simply don’t offer.

DSCR Loan Cons for International Real Estate Investors

DSCR loans are a strong option for many investors, but they are not without limitations. Understanding these upfront helps you plan your deal structure more effectively and avoid surprises during the process.

1. Higher Down Payment Requirement

DSCR loans typically require a minimum 25% down payment, which is higher than many conventional loan options. For investors purchasing higher-value properties, this means a significant amount of capital needs to be in place before closing.

2. Higher Interest Rates Compared to Conventional Loans

Because DSCR loans carry more flexibility in qualification, they typically come with slightly higher interest rates than conventional financing. The tradeoff is that the qualification process is significantly simpler, but the cost of borrowing is higher over the life of the loan. Check current DSCR loan interest rates to see where rates stand today.

3. Investment Properties Only

DSCR loans are exclusively for income-producing investment properties. Primary residences, vacation homes for personal use, and properties requiring major renovation do not qualify. Investors looking to purchase a home to live in will need to explore conventional financing instead.

Steven Glick,

Director of Mortgage Sales, HomeAbroad | NMLS# 1231769

DSCR Loan Pros and Cons Comparison Table

A side-by-side comparison makes it easier to evaluate whether a DSCR loan aligns with your investment strategy.

Pros | Cons |

|---|---|

Qualify based on property income, not personal income | Higher interest rates compared to conventional loans |

No US credit history required at HomeAbroad | Requires larger down payment (typically 25%) |

No DTI limits → easier to scale portfolio | Rental income based on appraisal, not projections |

Faster approval and closing (often within 30 days) | May include prepayment penalties |

Flexible loan structures for different investment strategies | |

Ideal for foreign nationals and global investors |

DSCR loans offer flexibility and scalability, with the main tradeoff being a higher upfront capital requirement and the need for careful deal structuring. For investors focused on long-term portfolio growth and a simpler qualification process, DSCR loans remain a strong fit despite the higher costs.

When a DSCR Loan Makes Sense for Investors

DSCR loans are most effective when the investment property itself is strong enough to support the financing. The better the property performs, the easier it is to qualify and scale.

Based on the applications we review, these are the scenarios where DSCR loans consistently perform well.

1. You Don’t Have US Income or Credit History

For foreign nationals, global investors, conventional financing is largely inaccessible. DSCR loans remove the requirement for US income documentation, employment history, and credit history entirely, making them the most practical path to US property financing for non-residents.

2. Your Property Generates Strong Rental Income

When a property has stable, predictable rental income and a DSCR of 1.0 or higher, it qualifies cleanly under standard terms. Long-term rentals with signed lease agreements and consistent rental history are particularly well suited for this type of financing.

3. You Are Self-Employed or Have a Complex Income Structure

Conventional loans rely heavily on tax returns and W-2 income. Self-employed investors often show lower taxable income on paper, which can make conventional qualification difficult. DSCR loans bypass personal income entirely, so your business structure or tax strategy doesn’t affect eligibility.

4. You Want to Scale Your Portfolio

Every conventional loan adds to your DTI, which eventually limits how many properties you can finance. DSCR loans are evaluated property by property, so each deal stands on its own. Investors looking to build a multi-property portfolio find this structure significantly easier to work with over time.

5. You Want a Simpler, Faster Process

With fewer documentation requirements and a qualification process focused on the deal rather than the borrower, DSCR loans are generally faster to process than conventional financing. For investors who want to move quickly on a property, this can be a meaningful advantage.

Steven Glick,

Director of Mortgage Sales, HomeAbroad | NMLS# 1231769

Who Should Consider a Conventional Loan Instead

DSCR loans are not the right fit for every investor or every situation. In some cases, a conventional loan may be the more practical and cost-effective option.

1. You Have Stable US Income and Strong Credit

If you have a reliable US-based income, a strong credit score, and full documentation readily available, a conventional loan will typically offer a smaller down payment requirement.

2. You Are Purchasing a Primary Residence

DSCR loans are exclusively for investment properties. If you are buying a home to live in, a conventional loan is the appropriate financing path. Primary residences do not qualify under DSCR programs regardless of the property’s rental potential.

3. Your Property Does Not Generate Rental Income

If the property you are purchasing is not intended to generate rental income, DSCR financing is not applicable. The entire qualification structure is built around rental income coverage, so non-income-producing properties fall outside the scope of this loan type.

The honest answer is that the right loan depends entirely on your profile and your goals. For investors who fit the conventional mold and are purchasing income-producing properties, it is worth comparing both options before deciding.

Conclusion

DSCR loans offer a different approach to real estate financing, one that prioritizes the property’s income over personal financials. For international investors, this creates a clear advantage by removing common barriers like income verification and US credit history.

At the same time, these benefits come with tradeoffs. Higher interest rates and larger down payments mean that DSCR loans require careful planning and the right deal structure.

When the property generates stable income and the deal is structured correctly, DSCR loans become one of the most effective ways to invest and scale in US real estate.

At HomeAbroad, we offer DSCR loans tailored specifically for foreign nationals and visa holders, along with an AI-native US real estate investing platform to help you identify investment-ready properties. Beyond financing, we also assist with LLC formation and US bank account setup, making the entire investment process more streamlined.

If you are planning to invest, understanding the pros and cons upfront will help you choose the right financing strategy and move forward with confidence.

Get pre-qualified today and see if a DSCR loan is the right fit for your investment goals.

Frequently Asked Questions

Are DSCR loans a good option for real estate investors?

Yes. DSCR loans are designed specifically for real estate investors, allowing you to qualify based on the property’s rental income rather than personal income or employment history.

Is a DSCR loan better than a conventional loan?

It depends on your profile and investment goals. DSCR loans are better suited for real estate investors, while conventional loans are generally a better fit for primary home buyers. For foreign nationals and portfolio investors, DSCR loans are the more practical option.

How many properties can I finance with DSCR loans?

There is no strict limit tied to personal income or DTI, making DSCR loans suitable for investors looking to scale their portfolio.

How much down payment do I need for a DSCR loan?

At HomeAbroad, DSCR loans require a minimum down payment of 25%. The exact amount may vary depending on the property type, loan size, and overall deal structure.