Editorial Integrity

Making informed real estate decisions starts with having the right knowledge. At HomeAbroad, we offer US mortgage products for foreign nationals & investors and have a network of 500+ expert HomeAbroad real estate agents to provide the expertise you need. Our content is written by licensed mortgage experts and seasoned real estate agents who share insights from their experience, helping thousands like you. Our strict editorial process ensures you receive reliable and accurate information.

Key Takeaway

1. At HomeAbroad, a DSCR of 1.0 or higher is generally required to qualify for better loan terms and smoother approval.

2. DSCR measures whether the property’s rental income covers its expenses, making it the key factor in DSCR loan qualification.

3. Even if your DSCR is below 1.0 you can still qualify through HomeAbroad’s No-Ratio DSCR Program with adjusted terms.

4. You can still qualify below 1.0 through options like No-Ratio DSCR programs, with adjusted terms.

Table of Contents

At HomeAbroad, we typically require a DSCR of 1.0 or higher for investment properties, meaning the property’s rental income should at least cover its loan obligations. This baseline ensures the deal is financially viable from a cash flow perspective and meets the minimum criteria for approval.

The DSCR (Debt Service Coverage Ratio) measures whether a property’s rental income can cover its loan payments. The higher the ratio, the stronger the deal and the easier it is to qualify.

Since DSCR loans are structured around the property’s performance rather than the borrower’s personal income, this ratio becomes a key factor in evaluating the strength of the investment. we focus on how consistently the property can generate income and whether that income is sufficient to support the loan over time.

This guide breaks down what qualifies as a good DSCR ratio, how lenders evaluate it, and how you can structure your deal to meet DSCR requirements confidently while maximizing your investment potential.

How to Calculate Your DSCR and Where Most Investors Get It Wrong

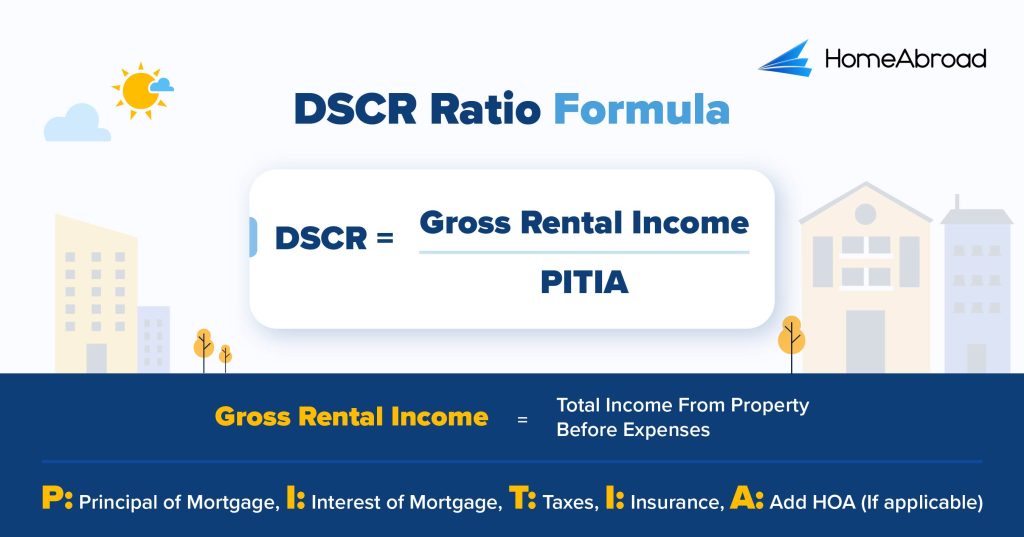

DSCR (Debt Service Coverage Ratio) is calculated by comparing a property’s rental income to its total monthly loan expenses. The DSCR formula is simple:

This example shows what a well-balanced DSCR deal looks like. With a DSCR of 1.25, the property not only covers its expenses but also provides a healthy income cushion, which strengthens loan approval and improves overall terms.

Where Most Investors Get It Wrong

1. Using Projected Instead of Appraisal-Based Rent

What most investors don’t realize is that lenders rely on appraisal-supported rental income, not optimistic estimates from platforms or assumptions. Online tools often show higher “potential rent,” but appraisers use comparable rental properties (rent comps) within a specific radius. If your assumed rent is even 10–15% higher than what the appraisal supports, your DSCR can drop below the required threshold.

2. Ignoring Full PITIA Costs

Many investors calculate DSCR using only principal and interest, ignoring other components like taxes, insurance, and HOA dues. The distinction here is that PITIA includes all housing-related costs, and even small additions like a $200 HOA or higher insurance premium can significantly reduce your DSCR ratio and impact qualification.

3. Overestimating Rental Potential

A pattern we’ve noticed is investors selecting properties based on best-case rental scenarios rather than consistent, market-backed income.

Short-term rental projections or seasonal income assumptions can make a deal look strong on paper, but lenders typically apply conservative estimates or adjustments, which can lower your actual DSCR during underwriting.

4. Not Structuring the Deal Early

DSCR issues often arise when investors choose a property first and consider financing later. Small adjustments like increasing the down payment, choosing a different loan term, or selecting a property with better rent-to-price ratio can improve DSCR significantly. When these decisions are made early, the approval process becomes much smoother.

Jason Saylor,

Sr. Customer Loan Specialist, HomeAbroad | NMLS# 2594493

What DSCR Ratio Do Lenders Typically Require?

At HomeAbroad, a DSCR of 1.0 or higher is generally required to qualify and secure the best loan terms, meaning the property generates enough rental income to fully cover its monthly expenses.

In our experience, most approved DSCR loans fall in the 1.1 to 1.25 range, where the property not only covers its costs but also shows a margin of safety. This is where underwriting tends to move more smoothly, as the income comfortably supports the loan.

The reason this matters is that DSCR is not just a threshold it’s a signal of deal strength. A higher DSCR reduces perceived risk, which can translate into better pricing, fewer conditions, and faster approval.

What most investors don’t realize is that the DSCR used for approval is based on appraisal-supported rental income, not optimistic projections. Even a small difference in rent assumptions can impact whether a deal meets the required ratio.

Jason Saylor,

Sr. Customer Loan Specialist, HomeAbroad | NMLS# 2594493

This is why focusing only on hitting 1.0 is not enough. Structuring your deal to achieve a strong DSCR with realistic rental data gives you a much higher chance of approval and better loan terms.

What If Your DSCR Is Below 1.0?

A DSCR below 1.0 means the property’s rental income does not fully cover its monthly expenses. While this may seem like a deal-breaker, it doesn’t automatically disqualify you.

I recently worked with a client who was looking to purchase an investment property in Orlando, Florida, but the deal came in with a DSCR of 0.87. Instead of declining the deal, we structured it under our No-Ratio DSCR program.

At HomeAbroad we understand that not every property’s rental income will meet the standard DSCR threshold, which is why we offer our No-Ratio DSCR Program for properties with a DSCR between 0 and 1.

However, this flexibility comes with adjusted terms:

-

A slightly higher down payment (typically a 5% reduction in LTV)

A slightly higher down payment (typically a 5% reduction in LTV) - Higher interest rates compared to standard DSCR loans

The reason this works is that we balance the lower DSCR by strengthening other parts of the deal, such as equity and reserves.

Jason Saylor,

Sr. Customer Loan Specialist, HomeAbroad | NMLS# 2594493

The key is understanding that DSCR is just one part of the deal. With the right structure and long-term strategy, even below-1.0 scenarios can still be strong investment opportunities.

How Your DSCR Ratio Directly Affects Your Mortgage Rate and Loan Terms

Your DSCR ratio doesn’t just determine whether you qualify it directly impacts your interest rate, loan terms, and overall deal structure. The stronger your DSCR, the lower the perceived risk, and the better the terms you can secure.

1. Interest Rates

A higher DSCR typically leads to lower interest rates because the property generates more than enough income to cover the loan.

- DSCR 1.25+ → Better pricing and lower rates

- DSCR 1.0–1.24 → Standard rates

- Below 1.0 → Higher rates due to increased risk

The reason this matters is that even a small rate difference can significantly impact your monthly cash flow and long-term returns. Check the latest DSCR loan interest rates here.

2. Down Payment and LTV

DSCR also influences how much you need to put down.

- Strong DSCR → Standard 75% LTV (25% down)

- Lower DSCR → Reduced LTV (higher down payment required)

This is how lenders balance risk when income coverage is tighter.

3. Loan Approval Conditions

Stronger DSCR ratios usually result in:

- Fewer conditions during underwriting

- Faster approval timelines

- Less scrutiny on supporting documents

A weaker DSCR may require additional documentation or stricter structuring.

4. Flexibility in Loan Structuring

With a higher DSCR, you have more flexibility to:

- Choose better loan terms

- Negotiate pricing

- Structure the deal more efficiently

Lower DSCR scenarios limit these options and often require trade-offs.

Jason Saylor,

Sr. Customer Loan Specialist, HomeAbroad | NMLS# 2594493

Your DSCR ratio ultimately defines how strong your deal looks to a lender. Improving it even slightly can lead to better rates, lower capital requirements, and a smoother path to closing.

Example of a Good DSCR Ratio (Real Scenario)

A real example helps clarify what a strong DSCR ratio looks like in practice.

One of our clients from South Africa purchased a rental property in Ohio through HomeAbroad using a DSCR loan structured around the property’s income rather than personal financials . The goal was to secure a property that could generate immediate cash flow while qualifying without US income or credit history.

- Monthly rental income: $2,656

- Monthly PITIA (mortgage): $914

- DSCR: 2.90

With a DSCR of 2.9, the property generated nearly three times the income required to cover its monthly expenses. This is considered an exceptionally strong DSCR and significantly reduces lender risk.

As a result, the deal moved smoothly through underwriting and closed within about a month, while also delivering strong positive cash flow for the investor.

while a DSCR of above 1.2 is considered strong, this example shows how higher DSCR deals can unlock better terms, faster approvals, and more stable long-term performance.

Explore the full case study to understand how this DSCR loan was structured and how the investor secured cash flow.

How to Improve Your DSCR Ratio

Improving your DSCR ratio comes down to one simple principle: increase rental income or reduce expenses. Even small changes can significantly impact whether your deal qualifies and the terms you receive.

1. Increase Rental Income

Higher rental income directly improves your DSCR. This can be done by:

- Choosing properties in strong rental markets

- Optimizing rent based on market comparables

- Adding value through minor upgrades or better positioning

The reason this matters is that DSCR is heavily influenced by appraisal-based rent, so realistic and well-supported rental estimates are critical.

2. Reduce Monthly Expenses (PITIA)

Lowering your total monthly payment improves your DSCR ratio.

You can do this by:

- Increasing your down payment to reduce loan amount

- Securing better loan terms (interest rate, structure)

- Choosing properties with lower taxes, insurance, or HOA dues

3. Choose the Right Property Type

Properties with stable, predictable income such as long-term rentals tend to produce stronger DSCR ratios compared to short-term or highly variable income properties.

4. Improve Deal Structure Early

A pattern we’ve noticed is that deals structured correctly from the start perform much better during underwriting. Adjusting rent assumptions, loan terms, or property selection early can prevent DSCR issues later.

5. Avoid Overestimating Rental Income

One of the most common mistakes is relying on projected or inflated rent figures. Lenders use appraisal-supported rental income, which may differ from online estimates.

Jason Saylor,

Sr. Customer Loan Specialist, HomeAbroad | NMLS# 2594493

Conclusion

A good DSCR ratio is not just about meeting a minimum requirement, it’s about how strong and stable your investment really is. While a DSCR of 1.0 or higher is typically required to qualify, stronger ratios give you better terms, smoother approvals, and more flexibility in structuring your deal.

Understanding DSCR starts with recognizing that it reflects the property’s ability to support itself. When rental income is realistic, expenses are accurately calculated, and the deal is structured correctly, qualifying becomes much more straightforward.

At HomeAbroad, we structure DSCR loans specifically for foreign nationals, allowing you to qualify based on property income without relying on US income or credit history.

Get pre-qualified today and understand how your investment property performs based on DSCR requirements.

DSCR Ratio Questions Investors Ask Most

What is DSCR?

DSCR (Debt Service Coverage Ratio) measures whether a property’s rental income is enough to cover its monthly loan payments. It is calculated by dividing rental income by PITIA (principal, interest, taxes, insurance, and HOA).

What is considered a good DSCR ratio for an investment property?

At HomeAbroad, a DSCR of 1.0 or higher is generally required to qualify, while 1.2+ is considered strong and can help secure better loan terms.

Does a higher DSCR mean a lower rate?

Yes, a higher DSCR ratio typically leads to better interest rates, smoother approval, and fewer conditions, as it shows stronger cash flow.

Can foreign nationals qualify for a DSCR loan?

Yes, at HomeAbroad, foreign nationals and visa holders can qualify for DSCR loans based on the property’s rental income, without needing US income or credit history.

Can I qualify for a DSCR loan without meeting the minimum DSCR ratio?

Yes, at HomeAbroad, you can still qualify through our No-Ratio DSCR Program for properties with a DSCR below 1.0, with adjusted terms such as a higher down payment and higher interest rates.

Does property type affect DSCR?

Yes, property type can directly impact DSCR. Properties with stable, predictable rental income such as long-term rentals typically achieve stronger DSCR ratios, while short-term or variable-income properties may result in lower or more volatile DSCR depending on income consistency.

![DSCR Loan Down Payment Requirements [2026]](https://homeabroadinc.com/wp-content/uploads/2023/01/DSCRDownPayment-scaled.jpg)