Editorial Integrity

Making informed real estate decisions starts with having the right knowledge. At HomeAbroad, we offer US mortgage products for foreign nationals & investors and have a network of 500+ expert HomeAbroad real estate agents to provide the expertise you need. Our content is written by licensed mortgage experts and seasoned real estate agents who share insights from their experience, helping thousands like you. Our strict editorial process ensures you receive reliable and accurate information.

Key Takeaways

1. The BRRRR refinance is the stage where your deal either works or falls short, since this is when you attempt to recover your capital and move to the next investment.

2. DSCR loans qualify based on the property’s income, which means lease stability, rent collection, and documentation matter more than your personal income or credit profile.

3. At HomeAbroad a DSCR of 1.0 or higher is typically required for refinance, and stronger ratios generally lead to better terms and smoother approvals.

4. Most BRRRR refinances are completed within 3 to 6 months, but the actual timeline depends on how quickly the property is renovated, rented, and fully stabilized.

5. Full capital recovery is not always the outcome, as the final loan amount depends on the appraised value and LTV limits, not just your total investment.

If you’ve completed a BRRRR deal and reached the refinance stage, this is where the outcome is decided. The BRRRR refinance DSCR loan is not just another step in the process, it is the point where you either recover your capital or get stuck holding more cash in the deal than expected.

Based on the BRRRR refinances we’ve structured for foreign national investors, the most common mistake is treating the refinance as something to figure out after rehab. In practice, the refinance needs to be planned before the deal even closes.

This is where most deals run into problems. The property may be renovated and rented, but the loan used at the start does not align with DSCR refinance requirements. That mismatch shows up during underwriting through documentation gaps, rent history issues, or lower-than-expected appraisals.

In this guide, we break down exactly how to refinance a BRRRR property into a DSCR loan, what lenders actually look for, and how to structure your deal so the refinance works as expected.

Table of Contents

What Is a BRRRR Refinance?

In the BRRRR method, the refinance stage is where you replace your short-term acquisition and rehab loan with a long-term loan based on the property’s updated value and rental income. This is the point where you recover part or all of the capital you put into the deal.

In a typical BRRRR flow, the refinance happens after the property is renovated and stabilized with a tenant in place. The lender looks at the appraised value and the property’s income, not what you originally paid or spent on rehab.

What most investors don’t realize is that this step is not automatic. The refinance only works if the property meets specific criteria around rent, documentation, seasoning, and valuation. If those are not aligned, the deal holds your capital longer than expected or requires additional cash at closing.

Why DSCR Loans Are the Ideal Exit for BRRRR

DSCR loans are built around the exact outcome BRRRR is trying to achieve. Once the property is renovated and rented, the refinance is based on the income the property generates, not your personal income or tax returns.

This matters because most BRRRR investors are scaling. Using traditional loans that rely on personal income or DTI quickly becomes a bottleneck. DSCR removes that constraint by focusing on whether the property can support its own debt.

Another key shift is how refinancing works today. In 2023, Fannie Mae updated its guidelines under Announcement SEL-2023-01, increasing seasoning requirements for cash-out refinances to 12 months. For BRRRR investors, that change makes it difficult to recycle capital on the timeline the strategy depends on.

The distinction here is not just that DSCR is an alternative, it is that it aligns with how BRRRR actually operates. When the strategy depends on refinancing quickly and recycling capital, DSCR is what allows the model to function within a realistic timeline under current lending conditions.

Jason Saylor,

Sr. Customer Loan Specialist, HomeAbroad | NMLS# 2594493

How DSCR Refinance Works in BRRRR

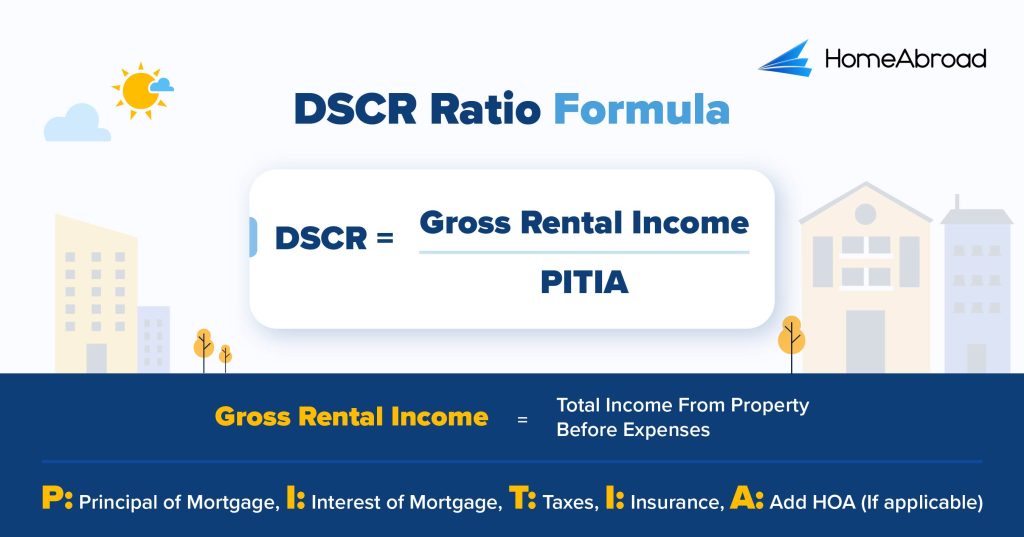

DSCR refinance is based on a simple formula:

PITIA includes your full monthly housing cost, not just the loan payment. That means property taxes, insurance, and any HOA dues are all factored into the calculation, which is where many investors see their numbers shift.

If the rent fully covers the payment, the DSCR is 1.0. Stronger deals typically fall in the 1.1 to 1.25 range, where the property generates more income than required to service the debt.

In our underwriting, we do not rely on projected numbers. We use the lower of actual lease income or appraiser-supported market rent. We also look at how stable that income is, whether rent has been collected, and whether the property is fully ready for long-term tenancy.

This is where it gets specific. A property can look profitable on paper, but if the rent is not documented correctly or the appraisal comes in lower than expected, the DSCR drops and the refinance terms change.

Jason Saylor,

Sr. Customer Loan Specialist, HomeAbroad | NMLS# 2594493

Step-by-Step: How to Refinance a BRRRR Property Into a DSCR Loan

Refinancing a BRRRR property into a DSCR loan is not a single step. It is a sequence, and the outcome depends on how well each stage is prepared before you apply.

Step 0: Model DSCR Before You Buy

Before you close on the purchase, run the DSCR based on expected rent and realistic expenses. This is where deals are either validated or rejected. If the numbers do not work here, they will not work at refinance.

Step 1: Complete Rehab to a Refinance-Ready Standard

Finishing the rehab is not just about construction. The property needs to be in a condition that supports both rental demand and appraisal value. Incomplete or cosmetic-only work can limit valuation at refinance.

Step 2: Stabilize the Property with a Lease and Rent Collection

A signed lease is not enough. The property should be rented and rent should be collected. This is what supports both DSCR calculation and underwriting confidence.

Jason Saylor,

Sr. Customer Loan Specialist, HomeAbroad | NMLS# 2594493

Step 3: Confirm DSCR Before Applying

Once the property is rented, recheck the DSCR using actual lease numbers. This confirms whether the deal still meets the requirement before you enter underwriting.

Step 4: Prepare Documentation

This is where many refinances slow down. Required documents typically include:

-

Lease agreement

Lease agreement - Proof of rent collection

- Rehab invoices and cost breakdown

- Insurance documents

- Bank statements for reserves

- LLC documents (if applicable)

- Passport and ID (for foreign nationals)

To be clear, documentation requirements vary by program, but missing or inconsistent documents are one of the most common causes of delays.

Step 5: Apply for DSCR Refinance

Once the property is stabilized and documentation is ready, you can apply. Timing here is driven by seasoning, not just readiness. For most DSCR cash-out refinances, a minimum 6-month holding period is required from the original purchase date, not from when rehab is completed or the property is leased.

In some cases, delayed financing may allow earlier refinance for cash purchases, but standard BRRRR deals should plan around this 6-month window.

Step 6: Appraisal and Underwriting

The lender orders an appraisal based on the stabilized, post-rehab condition of the property. The loan is sized using this appraised value, not your purchase price or total investment.

If the appraisal comes in lower than expected, the loan amount is reduced, which directly impacts how much capital you can recover. This is one of the most common points where refinance expectations change during underwriting

Step 7: Close and Recover Capital

At closing, the DSCR loan replaces your short-term financing. This is where you recover part or all of your invested capital, depending on the appraisal, DSCR, and loan terms.

Jason Saylor,

Sr. Customer Loan Specialist, HomeAbroad | NMLS# 2594493

Each step builds on the previous one. If one part is misaligned, the refinance does not fail immediately, it shows up later during underwriting.

DSCR Loan Requirements for BRRRR Refinance

DSCR refinance requirements for foreign national investors are built around the property, not the borrower. The focus is on whether the deal is stabilized, documented, and generating enough income to support the refinance.

Key Requirements

- DSCR Ratio: A DSCR of 1.0 or higher is preferred for refinance. In some cases, DSCR as low as 0.75 can still qualify with a higher equity position, meaning the property covers at least 75% of the mortgage.

- Loan-to-Value (LTV): Cash-out refinances are typically capped at up to 70% of the appraised value, which directly determines how much capital can be recovered from the deal.

- Stabilized Property with Lease: The property must be fully renovated, leased, and generating rental income. Rent collection history matters, not just a signed lease.

- Cash Reserves: Around 6 months of reserves are typically required to support the loan during underwriting.

- Documentation: Lease agreement, proof of rent collection, rehab completion records, insurance documents, bank statements, and entity documents (if using an LLC) are required. For foreign nationals, passport and identity documentation are also part of the process.

To be clear, these requirements are not one-size-fits-all. If cash flow is tight or timelines stretch, short-term financing costs can impact returns. That is why having the full carry cost clearly mapped before moving forward is critical.

Rate-and-Term vs Cash-Out Refinance

At the refinance stage, you are not just qualifying for a loan, you are deciding how the deal moves forward. The choice between rate-and-term and cash-out refinance directly affects both your capital recovery and long-term cash flow.

Criteria | Rate-and-Term Refinance | Cash-Out Refinance |

|---|---|---|

Primary Goal | Lower interest rate or replace existing loan | Recover invested capital |

LTV Limits | 75% | 70% |

Cash Received | None | Yes, based on equity |

Monthly Payment | Lower (less leverage) | Higher (more leverage) |

Best Use Case | Stabilized property, focus on cash flow | BRRRR exit, recycle capital |

Impact on Strategy | Keeps more equity in the deal | Frees up capital for next deal |

The decision comes down to what you need from the deal at that stage. If your priority is to improve cash flow and hold long-term, rate-and-term may be the better fit. If your goal is to recover capital and move to the next investment, cash-out refinance is what enables that transition.

How Much Cash Can You Pull Out?

The amount of cash you can pull out in a BRRRR refinance depends on the appraised value of the property and the lender’s LTV limits. For DSCR cash-out refinances, this is typically capped at up to 70% of the appraised value.

Let’s take an example of a client we worked with recently in Florida. The property appraised at $286,500, and the refinance was structured at 70% LTV, resulting in a loan amount of $200,550. That loan first pays off the existing financing, and the remaining amount returned to the investor was approximately $124,000.

What matters here is not just the loan amount, but how it compares to your total investment. This is where a more useful metric comes in: capital recovery rate, which is the amount of capital recovered divided by the total amount invested.

For this deal, the investor had approximately $200,000 invested and recovered about $124,000, resulting in a capital recovery rate of around 62%. This gives a clearer picture than LTV alone.

What most investors don’t realize is that full capital recovery is not always the outcome. In many cases, recovering 60–80% of your capital while holding a cash-flowing property is still a strong result.

This is where it gets nuanced. Small changes in appraisal value or rent can shift the numbers. A lower appraisal reduces your loan amount, and lower rent can impact DSCR, which may further limit how much you can pull out.

How Long Does a BRRRR Refinance Take?

A BRRRR refinance timeline has two parts, and they are often confused.

1. Deal Timeline (Purchase to Refinance-Ready)

Most BRRRR deals take 3 to 6 months to reach refinance-ready status. This includes completing the rehab, leasing the property, and stabilizing rent. The timeline depends on how quickly the property moves through these stages.

2. Refinance Timeline (Application to Closing)

Once the property is ready and you apply, DSCR refinances typically close in 20 to 30 days when documentation is complete at submission.

Based on the refinances we’ve processed, deals that are prepared before applying tend to move smoothly, especially when documentation is submitted at application rather than collected during underwriting. Deals that enter underwriting early without that preparation often face delays that extend the overall timeline.

The key factor across both timelines is readiness. A property that is renovated, leased, and generating consistent rent, with complete documentation in place, moves through refinance far more efficiently than one that is still being stabilized.

Real Example: DSCR Refinance for a Foreign National Investor

Based on a recent DSCR refinance we structured, a Canadian investor refinanced a single-family rental in Mississippi using a property-based loan structure instead of relying on US credit or personal income.

Deal Snapshot:

- Purchase Price: $420,000

- Loan Amount: $263,000

- Interest Rate: 6.625% (fixed)

- Loan Term: 30 years

- Closing Time: 26 days

What made this refinance work was not just the property itself, but how the deal was aligned before application. The property was stabilized, income-supported, and documented correctly, which allowed the refinance to move smoothly through underwriting.

This is where the difference shows up. The refinance did not depend on the borrower’s US income or credit history. It was approved based on the property’s ability to support the loan.

If you want to see the full breakdown of this deal check out the complete case study here: A Canadian Investor Refinance Case study.

Common Reasons BRRRR Refinances Get Denied or Delayed

Not every BRRRR deal makes it through refinance. Most issues don’t show up at purchase, they show up when the lender evaluates the property against actual income, documentation, and value.

- DSCR below requirement: If the rental income does not sufficiently cover the monthly payment, the deal may not qualify or may require a lower loan amount.

- Property not fully stabilized: A property without a tenant or without consistent rent collection is difficult to refinance. A signed lease alone is usually not enough.

- Appraisal comes in below expectations: If the appraised value is lower than your projected ARV, the loan amount is reduced, which limits how much capital you can recover.

- Incomplete or inconsistent documentation: Missing lease details, unclear rent records, or incomplete rehab documentation can slow down or stop underwriting.

- Insufficient reserves: If reserve requirements are not met, lenders may pause or decline the refinance until additional liquidity is shown.

- Timing and seasoning issues: Most DSCR cash-out refinances require a minimum 6-month seasoning period from the original purchase date. Applying before that window, or before the property is fully stabilized, can delay or block the refinance.

Jason Saylor,

Sr. Customer Loan Specialist, HomeAbroad | NMLS# 2594493

These issues usually appear during underwriting. By the time they show up, fixing them often requires more time, more capital, or both.

Rates and Costs for DSCR Refinance

DSCR refinance rates are influenced by the deal, not just the market. Loan-to-value, DSCR ratio, property type, and reserve strength all affect pricing.

As of June, 2026, DSCR refinance rates for foreign national investors on stabilized rental properties typically range between 7.125% and 7.625%, depending on leverage and overall deal profile.

Beyond the rate, there are several costs to account for:

- Origination Fee: Typically ranges from 1% to 2% of the loan amount.

- Appraisal Cost: Varies by property type and location, usually a few hundred to over a thousand dollars.

- Title and Closing Costs: Includes title insurance, legal, and recording fees.

- Prepaid Items: Taxes, insurance, and initial escrow funding may be required at closing.

What most investors focus on is the DSCR interest rate, but the total cost of the refinance matters more. Fees, reserves, and prepaid items all impact how much capital you actually receive at closing.

The underlying mechanics here are that pricing is not fixed. DSCR, leverage, and documentation directly affect how lenders assess risk, which influences rate and terms. Higher DSCR and lower LTV reduce risk exposure, while stronger reserves and clean documentation improve how the loan is positioned in secondary markets. That is why stronger deals typically receive better pricing, while tighter deals tend to price higher.

How to Prepare Your Property for a DSCR Refinance

Getting approved faster is not about speeding up the lender, it is about entering underwriting with a property that already meets the requirements. Most delays come from deals that are not fully ready when they are submitted.

1. Stabilize rent before applying: Ensure the property is leased and rent has been collected. A signed lease without payment history can slow down approval.

2. Align lease structure with lender expectations: Lease terms, rent amount, and tenant details should be clear and consistent. This is what supports DSCR during underwriting.

3. Complete documentation upfront: Have lease agreements, rent proof, rehab records, insurance, and bank statements ready before applying. Missing documents are one of the most common causes of delays.

4. Do not apply during lease-up: Entering underwriting before rent has been collected, even if a lease is signed, typically adds 2 to 4 weeks to the timeline as the lender waits for payment confirmation.

5. Keep reserves ready: Ensure required reserves are available and clearly documented. This is a standard part of DSCR approval.

What most investors don’t realize is that approval speed is less about the lender and more about preparation. Deals that enter underwriting fully aligned tend to move smoothly, while partially prepared deals take longer to close.

Ready to Refinance Your BRRRR Into a DSCR Loan?

Refinancing a BRRRR property is where the deal either delivers on its strategy or falls short. The difference usually comes down to how well the refinance was planned before the deal started.

At HomeAbroad, we help foreign national investors structure BRRRR refinances end to end, from aligning the initial loan with the exit strategy to securing DSCR financing based on property income. We also assist with LLC formation and US bank account setup so the entire structure is in place before you reach the refinance stage.

For US-based investors, our sister platform Ziffy.ai provides similar support tailored to domestic borrowers.

Start your BRRRR refinance with a structure that supports the deal from start to end with HomeAbroad today.

Frequently Asked Questions

How soon can I refinance a BRRRR property into a DSCR loan?

Most BRRRR refinances happen within 3 to 6 months, depending on how quickly the property is renovated, rented, and stabilized. The key factor is not time alone but whether the property meets refinance requirements.

What DSCR ratio is required to qualify?

A DSCR of 1.0 or higher is typically required, meaning the property generates enough income to cover its monthly debt. In some cases, lower DSCR may still qualify with a higher down payment.

Do I need a tenant before applying for a DSCR refinance?

Yes, the property generally needs to be leased and generating rental income. A signed lease without rent collection history may not be sufficient for underwriting.

What happens if my appraisal comes in lower than expected?

A lower appraisal reduces the loan amount, which means you may not recover all your capital. You may need to leave more cash in the deal or adjust your refinance strategy.

Can I refinance a BRRRR property under an LLC?

Yes, DSCR loans commonly support LLC ownership, which is how many foreign national investors structure their investments.

Can foreign nationals use DSCR loans for BRRRR refinance?

Yes, DSCR loans are widely used by foreign national investors since qualification is based on the property’s income rather than US credit or personal income.