Editorial Integrity

Making informed real estate decisions starts with having the right knowledge. At HomeAbroad, we offer US mortgage products for foreign nationals & investors and have a network of 500+ expert HomeAbroad real estate agents to provide the expertise you need. Our content is written by licensed mortgage experts and seasoned real estate agents who share insights from their experience, helping thousands like you. Our strict editorial process ensures you receive reliable and accurate information.

Can You Get a US Mortgage Without an SSN?(Short Answer)

Yes, you can get a US mortgage without an SSN. Foreign nationals can finance US investment property without a US credit score and without traveling to the US to close. For most investors, the most practical option is a DSCR loan, where the property’s rental income qualifies the loan instead of personal income or US-based identity.

Based on over 500 foreign national DSCR loans we’ve closed, approval does not depend on having an SSN. It depends on whether the property supports the loan and how clearly the documentation is structured.

Quick Facts:

- No SSN or ITIN required to qualify on most foreign national programs

- No US credit score required in most cases

- 25% down payment is typical

- Closing timeline ~27 days with complete documentation

Lucas Hernandez,

Mortgage Loan Originator, HomeAbroad | NMLS# 2171747

Table of Contents

How Foreign Nationals Can Get a Mortgage Without an SSN

An SSN exists to track income and taxes within the US workforce. If you don’t live or work in the US, you’re outside that system, and your mortgage doesn’t depend on it.

Foreign national mortgage programs are built for this exact scenario. These are non-QM loans designed for buyers who are not US citizens or residents and do not fit conventional underwriting. Instead of relying on an SSN, US credit score, or US-based income, the focus shifts to what can actually be verified.

At HomeAbroad, underwriting is centered around a few core factors:

- Identity verification (valid passport)

- A clear and traceable source of funds for the down payment

- Asset reserves to support the loan

- Foreign credit or banking references where available

- And depending on the loan type, either property cash flow (DSCR) or documented foreign income

The key difference is how the deal is evaluated. On DSCR loans, qualification is based on the property’s rental income, not your personal income or tax history. That removes the need for employment verification or US financial records.

These loans are not exceptions to the system. They are designed specifically for foreign investors, using asset verification and property performance instead of US-based financial history. No SSN and no US credit are not limitations, they are expected conditions in this loan category.

Property eligibility is also structured around investment use. Most foreign national loans are for rental properties, with some programs allowing second homes. Primary residence financing for non-residents is uncommon.

Closing from abroad is standard. Most foreign investors complete the entire transaction remotely using a power of attorney, without needing to travel to the US.

Steven Glick,

Director of Mortgage Sales, HomeAbroad | NMLS# 1231769

DSCR Loans: The Most Practical Option for Most Foreign Investors

What a DSCR Loan Is

A DSCR (Debt Service Coverage Ratio) loan qualifies the property, not the borrower.

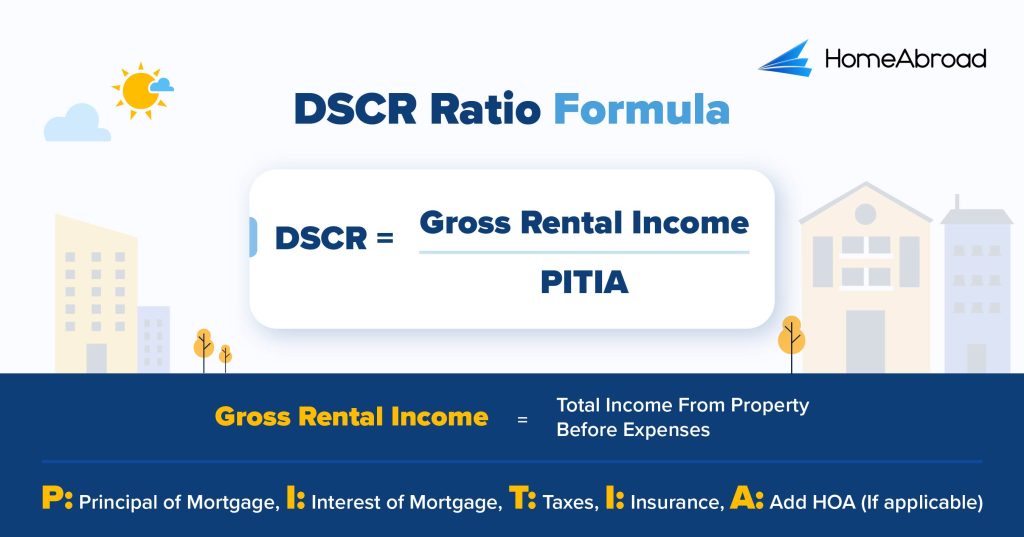

Here is the DSCR formula:

A DSCR of 1.0 means the property generates just enough income to cover the monthly mortgage payment. At HomeAbroad, we typically look for DSCR 1 or higher for stronger approvals, since it provides a buffer beyond break-even cash flow.

That said, DSCR below 1.0 does not automatically disqualify the deal. We offer no-ratio DSCR programs where the focus shifts to your assets, reserves, and overall deal strength instead of the income ratio alone.

The key difference is simple. Your personal income, employment, and tax history are not used to qualify the loan. The decision is based on how the property performs as an investment.

Why DSCR Is the Default Answer for Foreign Nationals

For foreign investors without an SSN, this is the most practical path.

DSCR removes the need to verify personal income, tax returns, or employment across countries. Instead of translating documents and aligning foreign financial records, underwriting focuses on the property’s performance and your available capital.

From what we’ve seen across foreign national files, this makes the process more predictable and reduces the friction that typically slows deals down.

How a DSCR Loan Is Underwritten Without an SSN

Underwriting is focused on three areas:

First, the rent figure from the appraiser’s 1007 report. This is not your projected rent or listing estimate. It is the appraiser’s market-supported rental value based on comparable properties.

Second, your source of funds. The down payment and reserves must be fully traceable, with a clear paper trail from origin to closing account.

Third, identity and asset verification. Passport, bank statements, and reserves are reviewed to confirm capacity to support the loan.

The 1007 rent comp is the most important number in the file. If it comes in lower than expected, your DSCR drops, and that directly impacts approval and terms.

Lucas Hernandez,

Mortgage Loan Originator, HomeAbroad | NMLS# 2171747

DSCR Loan Terms Foreign Nationals Typically See

While terms vary by deal, most foreign national DSCR loans follow a consistent structure.

- Loan amounts: >=$100K – $10M

- Down payment: 25%

- Rates: as of June 2026, DSCR rate ranges from 6.87% to 7.12%

- Reserves: 6 months of PITIA

- Loan structures: 30-year fixed

To be clear, foreign national mortgage rates run higher than conventional loans. That’s expected. These programs are designed for borrowers without US credit or income, and pricing reflects that risk profile. To understand how current rates looks, check the latest DSCR interest rates here.

DSCR works best when the property is rent-ready and generates stable income. If the deal depends on renovation, timing is critical, or rental income doesn’t support the loan, other financing options become more relevant.

When DSCR Isn’t the Right Fit: Other Foreign National Loan Programs

DSCR is the default for most foreign investors, but there are cases where another loan structure makes more sense.

Full-documentation foreign national loans are used when the deal doesn’t meet DSCR thresholds but the borrower can provide strong income documentation from their home country. This path relies on verified income instead of property cash flow, which means more documentation and longer underwriting, but can result in better pricing for qualified borrowers.

Bridge loans are short-term financing options used when speed is critical. They are commonly used for auction purchases, off-market deals, or situations where the investor plans to refinance later. The trade-off is higher rates and shorter terms, with a clear exit strategy required upfront.

Fix-and-flip loans are designed for renovation-based strategies where the property is not rent-ready at acquisition. These loans are structured around project cost and after-repair value rather than rental income, making them suitable for investors planning to renovate and sell rather than hold.

Eligibility Requirements for Foreign Nationals Without an SSN

Foreign national loans are structured around what can be verified. Eligibility is driven by the deal itself, not traditional borrower metrics.

What matters most:

- Down payment by product: DSCR typically 25%; full-doc 25%+; bridge 30%; fix-and-flip 25%-30%

- Reserves: usually 6–12 months of PITIA

- Source of funds: must be fully traceable and meet AML requirements

- Property eligibility: 1–4 unit residential is standard; multifamily and small commercial allowed on select programs

- Ownership structure: you can purchase as an individual or through a US LLC

The key point is that eligibility is deal-driven. The property’s cash flow, your available capital, and clean documentation determine whether the file works.

How to Decide Between Loan Products

Most foreign national investors should start with DSCR. If the property is rent-ready and the appraiser-supported rent covers the loan, this is the simplest and most reliable option. It removes income verification and keeps the process more predictable.

If the deal does not meet DSCR requirements but you can provide strong, well-documented income from your home country, full-documentation loans can offer better terms. This path introduces more documentation but may improve pricing for qualified borrowers.

Bridge and fix-and-flip loans are situational. They become relevant when the property is not rent-ready, requires renovation, or when speed is critical and the deal cannot wait for full underwriting.

The key is to match the loan to how the deal actually works. Most issues arise when investors choose based on rate or familiarity instead of structure. When the financing aligns with the property condition and exit strategy, the process becomes more predictable and easier to execute.

Do You Need an ITIN at All?

Short answer for the buying side: no. An ITIN is not required to qualify for a foreign national mortgage on most programs.

The distinction here is between buying and selling.

Where it becomes relevant is at exit. FIRPTA(Foreign Investment in Real Property Tax Act) applies when a foreign owner sells US real estate. It requires a withholding on the sale proceeds, typically:

- 0% in limited exemption cases

- 10% or 15% depending on the sale price and buyer’s intended use

Form 8288-B can be filed to reduce the withholding if done correctly and on time. If not, the withheld amount is settled later through a tax refund, which can take 6 months or more.

The reason this matters is timing. FIRPTA applies at sale, not purchase, but the lack of an ITIN can slow down filings and delay access to funds when you exit the investment.

In practice, many investors choose to apply for an ITIN early, even though it’s not required to buy. It keeps the structure cleaner and avoids complications later.

We recommend consulting a US tax professional before any sale. FIRPTA treatment depends on your residency status, deal structure, and exit strategy.

Common Mistakes Foreign Investors Make Without an SSN

These are recurring issues we see across foreign national files. They are not complex, but they tend to surface late in the process when timelines are tight.

1. Wiring Funds Without a Clear Source-of-Funds Chain

A pattern we see often is funds moving across multiple accounts or coming from business entities without a documented trail. Underwriting requires a clear path from origin to closing account, and gaps can pause the file. Keeping funds consolidated and documented early avoids last-minute delays.

2. Submitting Documents Without Apostille or Proper Translation

In our experience, this issue doesn’t show up early. Documents look complete at submission but get flagged during final review because they lack certified translation or apostille. Fixing this close to closing can easily add a few weeks to the timeline.

3. Locking the Deal Before Validating Rent (DSCR)

What we see often is investors relying on expected rent or listing estimates instead of the appraiser’s 1007 rent. DSCR is calculated using that market-supported number, not projections. If the rent comes in lower, it directly affects qualification and may require restructuring the deal.

4. Choosing the Lowest Rate Without Checking the Prepayment Penalty

A lower rate can look attractive upfront, but DSCR loans often include prepayment penalties. These are commonly structured as step-down schedules over several years. If your strategy involves refinancing or selling early, the penalty can offset any rate savings.

5. Locking Insurance Too Late

Insurance is a required part of closing, not something to handle at the end. Delays in securing a policy can push closing timelines or even impact your rate lock. This is more common for foreign investors unfamiliar with US insurance requirements.

6. Assuming You Need to Travel to the US to Close

A common assumption we see with first-time foreign investors is that they need to be physically present. In reality, most transactions close remotely using a power of attorney. Not setting this up early creates unnecessary coordination issues late in the process.

Get Pre-qualified: Without an SSN

Pre-qualification is where your deal becomes actionable.

At HomeAbroad, the process is built for foreign investors. We start with your target market or property range, and a basic overview of your available funds for down payment and reserves. You don’t need an SSN, ITIN, US credit score, or even a US bank account to get started.

In practice, this is enough to determine whether your deal fits a DSCR loan or another structure and to identify any gaps early, before you begin making offers.

We’ve helped investors from 40+ countries purchase US real estate through foreign national loan programs. The pattern is consistent. Files that are clear and structured at the pre-qualification stage move faster and with fewer conditions later.

Pre-qualification typically comes back within a few business days. If you’re ready to move forward, you can connect with HomeAbroad to review your deal and take the next step with a clear, structured plan.

FAQs

Can I get a US mortgage without an SSN as a foreign national?

Yes, foreign national mortgage programs are built for buyers outside the US system. At HomeAbroad, we qualify loans based on your assets and the property’s income, not your SSN or US-based identity.

Do I need a US credit score?

No. At HomeAbroad, our foreign national DSCR loan programs do not require a US credit score or any credit history. Qualification is based on the property’s rental income not your personal income or employment.

Do I need to travel to the US to close?

No. At HomeAbroad, we offer remote closing options, so you can complete the entire transaction from your home country using a power of attorney and properly notarized documents.

What’s the minimum down payment on a foreign national mortgage?

This depends on the loan type. DSCR loans typically require 25%–30%, while other programs may vary. The reason this matters is that higher down payments reduce risk and improve approval strength.

How does FIRPTA affect me when I sell?

FIRPTA requires a withholding on sale proceeds when a foreign owner sells US real estate. This typically ranges from 10% to 15% depending on the sale price and buyer’s intended use. You can file Form 8288-B to reduce the withholding if submitted correctly and on time, otherwise the amount is refunded later through the tax process.