Editorial Integrity

Making informed real estate decisions starts with having the right knowledge. At HomeAbroad, we offer US mortgage products for foreign nationals & investors and have a network of 500+ expert HomeAbroad real estate agents to provide the expertise you need. Our content is written by licensed mortgage experts and seasoned real estate agents who share insights from their experience, helping thousands like you. Our strict editorial process ensures you receive reliable and accurate information.

The Section 871(d) net election allows foreign nationals to pay tax on net US rental income instead of a flat 30% tax on gross rent.

Eligible expenses such as mortgage interest, property taxes, insurance, management fees, HOA dues, and depreciation can significantly reduce taxable rental income.

The election is made by filing Form 1040-NR with a Section 871(d) statement, while Form W-8ECI can help stop the default 30% withholding on future rental income.

Tax savings during ownership should be weighed against future considerations such as depreciation recapture, basis adjustments, and tax liability when the property is sold.

Table of Contents

Quick Answer

A Section 871(d) net election allows a foreign national to be taxed on net US rental income rather than paying a flat 30% tax on gross rental income, as permitted under IRC Section 871(d) and related IRS guidance. For many investors, this is one of the most important tax elections available because it allows eligible expenses to be deducted before tax is calculated.

HomeAbroad has helped finance US investment properties for more than 500 foreign national investors from over 40 countries. One pattern we frequently see is investors assuming the 30% gross-rent rule is their only option, even when deductible expenses significantly reduce the property’s taxable income.

Without the election, nonresident alien rental income is generally treated as FDAP income and may be subject to a 30% tax on gross rent. With the election, rental income is treated as effectively connected income (ECI), allowing the property owner to deduct eligible rental-property expenses.

The result can be a significantly lower tax bill, especially for rental properties with substantial operating expenses. The comparison later in this guide shows how the same property can produce very different tax outcomes under the default 30% rule and the Section 871(d) net election.

Why Foreign Landlords Get Hit With 30% on Gross Rent by Default

The FDAP(Fixed, Determinable, Annual, or Periodical) default: 30% tax on gross rent

Under Internal Revenue Code Section 871(a), rental income earned by a nonresident alien is generally treated as FDAP income (Fixed, Determinable, Annual, or Periodical income). Unless another election is made, this income is subject to a flat 30% federal tax on the gross amount received.

The tax is calculated before expenses are considered. Mortgage interest, property taxes, insurance, repairs, property management fees, and depreciation generally do not reduce the amount subject to tax under the default FDAP rules. In many cases, the tax is also withheld at the source by the person responsible for making the payment.

What effectively connected income (ECI) changes

A Section 871(d) net election allows rental income to be treated as effectively connected income (ECI) instead of FDAP income (Fixed, Determinable, Annual, or Periodical income). Once the election is in place, the property owner can generally deduct ordinary and necessary expenses associated with operating the rental property.

This distinction can have a major impact on the amount of tax owed. Rather than paying tax on gross rent, the investor pays tax on the property’s net profit after eligible deductions are applied.

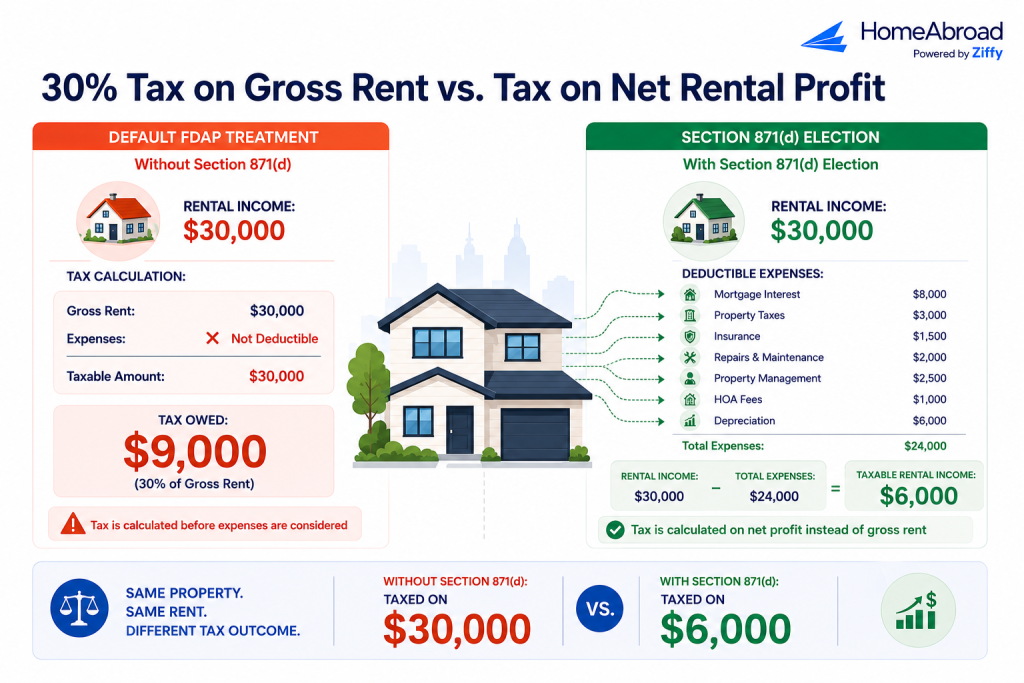

Why this matters: A rental property that generates $30,000 in annual rent and incurs $24,000 in deductible expenses would owe $9,000 in tax under the default 30% FDAP rule. Yet the property’s taxable income is only $6,000. The Section 871(d) election was created to address situations like this by allowing qualifying foreign property owners to be taxed on their net rental income instead of gross receipts.

Gross vs. Net: The Dollar Difference

The Section 871(d) net election can dramatically change how a foreign investor’s rental income is taxed. The difference is not a special tax rate or treaty benefit. The difference comes from whether tax is calculated on gross rental income or on net rental profit after eligible expenses are deducted.

In the example above, the property generates $30,000 in annual rental income and incurs $24,000 in operating expenses. Under the default FDAP rules, those expenses generally cannot be deducted when calculating tax. As a result, the investor is taxed on the full $30,000 of rental income even though the property’s taxable income is only $6,000.

With a Section 871(d) election, the same rental income is treated as effectively connected income (ECI). This allows the investor to deduct eligible rental-property expenses before tax is calculated.

Assuming the investor falls into the lowest federal income tax bracket, tax on $6,000 of taxable income could be approximately $600. By comparison, the default FDAP rules would result in a $9,000 tax liability on the same $30,000 of rental income. While actual tax liability depends on the investor’s overall tax situation, this example illustrates how the Section 871(d) election can significantly reduce the tax burden on profitable rental properties.

While actual tax liability depends on the investor’s overall tax situation, this example highlights why the Section 871(d) election can have a significant impact on after-tax cash flow and long-term investment returns.

The expenses most commonly deducted under Section 871(d) include:

- Mortgage interest

- Property taxes

- Insurance premiums

- Repairs and maintenance

- Property management fees

- HOA fees

- Depreciation

For many foreign investors, the ability to deduct these expenses is the primary reason for making the Section 871(d) election rather than remaining under the default 30% gross-rent rules.

How to Actually Make the Election

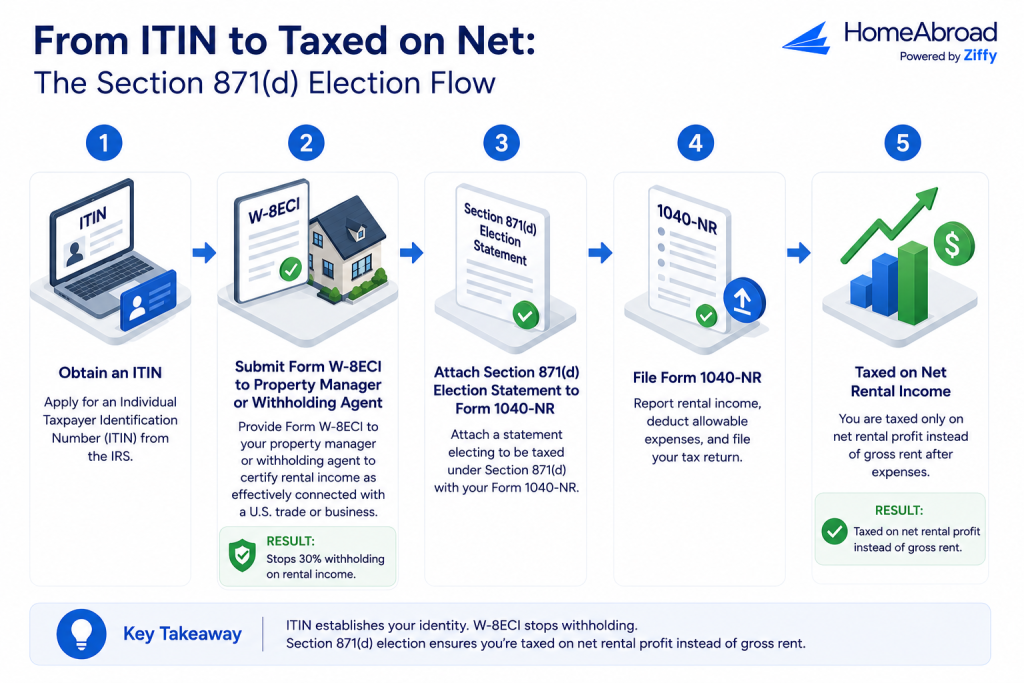

The Section 871(d) election is not made by filing a separate IRS form. Instead, foreign property owners elect net-income treatment by following a specific filing process with the IRS. This sequence is important because the election, withholding requirements, and tax-return filing obligations are all connected.

Attach the election statement to Form 1040-NR

The election is generally made by attaching a Section 871(d) election statement to Form 1040-NR, US Nonresident Alien Income Tax Return. The statement notifies the IRS that you are electing to treat rental income from US real estate as effectively connected income (ECI) rather than FDAP income.

Once the election is in place, rental income and related expenses are generally reported on Schedule E. This allows qualifying investors to deduct eligible rental-property expenses before calculating tax.

Stop withholding at the source with Form W-8ECI

Making the election and stopping withholding are two separate steps.

Many foreign property owners provide Form W-8ECI to their property manager or other withholding agent. This form certifies that the rental income is being treated as effectively connected income, allowing future rental payments to be made without the default 30% withholding that typically applies to FDAP income.

You’ll need an ITIN first

Most foreign investors need an Individual Taxpayer Identification Number (ITIN) before filing Form 1040-NR or submitting Form W-8ECI.

Obtaining an ITIN early can make the process significantly smoother. Investors who wait until tax season often find themselves trying to secure an ITIN, update withholding arrangements, and prepare tax filings at the same time.

Steven Glick

Director of Mortgage Sales · HomeAbroad

The biggest delays usually happen when investors wait until filing season to apply for an ITIN or update withholding documentation. Getting those pieces in place early can make the reporting process much easier.

Late and retroactive elections

The Section 871(d) election is not limited to the first year you own a rental property. In many cases, investors can make the election on an original return, an amended return, or retroactively with an appropriate reasonable-cause explanation.

In some situations, investors can make a late or retroactive Section 871(d) election by filing the appropriate return and providing a reasonable-cause explanation. However, refunds for prior years are generally subject to IRS filing deadlines, and deductions may be limited if required returns were not filed on time.

Because the rules surrounding late elections can be complex, foreign property owners should work with a qualified cross-border CPA or tax professional to determine the best approach for their situation.

The Trap Many Investors Overlook: Depreciation at Sale

The Section 871(d) election can reduce taxes during the years you own a rental property, but it can also affect the tax calculation when you eventually sell.

One of the most valuable deductions available under net-income treatment is depreciation. Each year, depreciation can reduce taxable rental income and improve after-tax cash flow. However, those deductions generally reduce the property’s tax basis over time.

A lower tax basis means a larger taxable gain when the property is sold. In addition to regular capital gains tax considerations, some of the depreciation claimed during ownership may be subject to depreciation recapture rules. In many cases, unrecaptured Section 1250 gain can be taxed at rates of up to 25%.

Investors often focus on the annual tax savings created by depreciation. The conversations become very different when they model the eventual sale and see how basis adjustments and recapture can affect the final tax outcome.

The IRS has launched the “Nonresident Alien Rental Income From US Real Property” compliance campaign, focusing on foreign property owners who claim rental-property deductions but fail to properly account for basis adjustments, depreciation, and gain calculations when the property is sold.

This does not mean the election is a bad idea. For many foreign investors, the tax savings generated during ownership significantly outweigh the future impact of depreciation recapture. Understanding the full lifecycle of the investment rather than evaluating the rental years in isolation.

If you’re planning to sell a US property, our FIRPTA (Foreign Investment in Real Property Tax Act) guide explains how withholding and gain calculations work for foreign owners. For estate-planning and treaty-related considerations, see our guide to US tax treaties and real estate investing.

How Net-Income Treatment Changes Your Financing Math

The Section 871(d) election is often viewed as a tax strategy, but it can also influence the economics of a real estate investment.

When rental income is taxed on gross rent, a larger portion of the property’s cash flow is lost to taxes. Net-income treatment allows eligible expenses to be deducted before tax is calculated, which can improve after-tax cash flow and increase the amount of income an investor retains from the property each year.

The impact becomes clearer when investors evaluate long-term returns, refinancing opportunities, or future property acquisitions. Investors who model their returns using after-tax cash flow often arrive at different conclusions than those who focus only on gross rental income.

Investors often focus on rental income when evaluating a property. Once taxes and operating expenses are factored into the analysis, we’ve seen the economics of a deal look very different from what the gross rent alone suggests

For foreign investors using DSCR loans or foreign national mortgage programs, understanding the relationship between rental income, operating expenses, taxes, and cash flow can lead to better investment decisions. The goal is not simply to qualify for financing but to build a property portfolio that performs well after all major expenses are considered.

Learn more about DSCR loans for foreign nationals and foreign national mortgage options to see how financing structure and tax planning can work together as part of a broader investment strategy.

The Bottom Line on the Section 871(d) Election

For many foreign investors, the Section 871(d) election is one of the most valuable tax elections available for US rental property ownership. Instead of paying a flat 30% tax on gross rental income, eligible investors can generally deduct operating expenses and pay tax on net rental profit.

The potential tax savings can be substantial, particularly for properties with significant mortgage interest, property tax, insurance, management, and depreciation deductions. At the same time, investors should understand how the election affects future tax reporting, depreciation recapture, and gain calculations when the property is eventually sold.

HomeAbroad helps foreign investors finance US investment properties through foreign national mortgage programs. If you’re planning your next investment, explore your financing options and work with experienced cross-border tax professionals to determine whether the Section 871(d) election aligns with your investment strategy.

Frequently Asked Questions

Is US Rental Income Taxable for a Foreign (Nonresident) Owner?

Yes. Rental income earned from US real estate is generally taxable in the United States, even if the property owner lives outside the country. By default, nonresident aliens are typically subject to a 30% tax on gross rental income unless they make a Section 871(d) election to be taxed on net rental profit.

Can a Foreign National Deduct Expenses on US Rental Income?

Generally, yes, if a Section 871(d) election is made. Eligible expenses may include mortgage interest, property taxes, insurance, repairs and maintenance, property management fees, HOA dues, and depreciation. Without the election, rental income is generally taxed on a gross basis, and these deductions are not available.

Is the Section 871(d) Election Irrevocable?

In most cases, yes. Once made, the election generally applies to future tax years and cannot be revoked without IRS consent. Because the decision can affect both annual tax reporting and future property sales, investors should understand the long-term implications before making the election.

What’s the Difference Between Form W-8ECI and a Section 871(d) Election Statement?

A Section 871(d) election statement is attached to Form 1040-NR to elect net-income treatment for US rental income. Form W-8ECI is provided to a property manager or withholding agent to certify that the rental income is being treated as effectively connected income, which can stop the default 30% withholding on future rental payments.

Do I Need an ITIN to Make the Election?

Most foreign property owners need an Individual Taxpayer Identification Number (ITIN) to file Form 1040-NR and submit Form W-8ECI. Obtaining an ITIN early can help avoid delays in tax reporting and withholding-related filings.

Does a Tax Treaty Reduce My Rental Income Tax?

Usually not. For most foreign investors, US tax treaties do not eliminate the ability of the United States to tax income from US real estate. The Section 871(d) election is often more important than treaty status because it allows qualifying investors to be taxed on net rental profit rather than gross rental income. For a deeper discussion, see our guide to US Tax Treaties and Real Estate Investing.