Editorial Integrity

Making informed real estate decisions starts with having the right knowledge. At HomeAbroad, we offer US mortgage products for foreign nationals & investors and have a network of 500+ expert HomeAbroad real estate agents to provide the expertise you need. Our content is written by licensed mortgage experts and seasoned real estate agents who share insights from their experience, helping thousands like you. Our strict editorial process ensures you receive reliable and accurate information.

Turnkey real estate investing means buying a US rental property that is already renovated, already tenanted, and already under property management. There is no industry-standard definition of the term, so what you actually receive varies by provider.

DSCR (Debt Service Coverage Ratio) financing suits the turnkey model because qualification runs on the property’s rental income rather than your US credit history or personal income.

The provider’s tenant comes with a lease, and that lease becomes an underwriting input. Your qualifying rent may not match the brochure.

A provider’s pro forma is a sales projection. Underwriting does not run on it, and your purchase decision should not either.

Foreign investors can complete a turnkey purchase without traveling to the US, though the tax treatment at both ends of the hold period needs planning well before closing.

Table of Contents

What Turnkey Real Estate Investing Actually Means

What Is a Turnkey Property?

Turnkey has no standard definition. Neither state real estate commissions nor the National Association of REALTORS (NAR) define what qualifies as a turnkey property. Instead, the term is used by sellers and providers, so what is included can vary significantly from one property to another.

One turnkey property may include a new roof, updated HVAC and electrical systems, a screened tenant on a 12-month lease, and professional property management already in place. Another may simply have fresh paint, new flooring, and a tenant who moved in last week. Both can be marketed as turnkey, but they may offer very different levels of renovation, cash flow stability, and long-term value.

Before evaluating any turnkey property, ask one simple question: What exactly is included, in writing?

The Three Things a Turnkey Package Usually Bundles

Completed renovation: The provider bought a property that needed work, did the work, and is selling the finished result. You are not managing contractors or approving change orders.

A placed tenant: Someone is living in the property under a signed lease and paying rent. A residential lease generally transfers with the property in most US states, meaning you take on the existing tenant, rent, and remaining lease term. Landlord-tenant rules are set at the state level, however, and the specifics vary. Confirm how leases are treated in the state where you’re buying.

Property management: A local company handles rent collection, maintenance calls, inspections, and tenant communication. Property management fees commonly range from 8% to 12% of collected rent, although the exact percentage depends on the market, property type, and services included. Many turnkey providers manage the properties they sell through an in-house division, which is worth understanding before you sign anything.

Turnkey vs BRRRR vs Fix and Flip

None of these three is the correct answer for every investor. They solve different problems, and the right one depends on how much of the work you can realistically supervise from where you live.

Why Turnkey Appeals to Foreign Investors, and Where the Fit Breaks

Turnkey real estate is often marketed as passive real estate investing, and for foreign nationals buying from abroad, the operational appeal is real. If you live in Dubai, Mumbai, London, or Toronto, you cannot walk a renovation site, compare contractor bids, or meet prospective tenants. Every hands-on investment strategy assumes a local presence you simply do not have.

Turnkey removes that challenge by completing much of the work before you take ownership. The property is typically renovated, leased, and ready to generate rental income, often with professional property management already in place. For many foreign nationals, that makes turnkey one of the simplest ways to buy a first US investment property.

The trade-off is convenience. Turnkey properties save you the time and effort of finding, renovating, and leasing a property, but that convenience is reflected in the purchase price. Providers typically buy below market value, renovate the property, prepare it for tenants, and then sell it at a price that covers their acquisition costs, renovation expenses, holding costs, and profit.

That doesn’t make turnkey a bad investment. It simply means you’re paying for a completed, income-producing property rather than creating the value yourself. As a result, turnkey properties rarely come with significant built-in equity on day one.

It also means many of the assumptions behind your projected returns were made before you entered the transaction. The renovation scope, the tenant, the agreed rent, and sometimes even the property manager may already be in place. Understanding those assumptions, rather than accepting them at face value, is one of the most important parts of evaluating a turnkey investment.

Steven Glick

Director of Mortgage Sales · HomeAbroad

The biggest difference isn’t the property. It’s the documentation behind it. A strong turnkey file includes the renovation scope, the existing lease, the property management agreement, and information that supports the property’s rental income. When those documents are organized from the beginning, underwriting spends less time asking follow-up questions and more time moving the loan toward approval.

How Turnkey Properties Are Financed as a Foreign National

Why DSCR Financing Fits the Turnkey Model

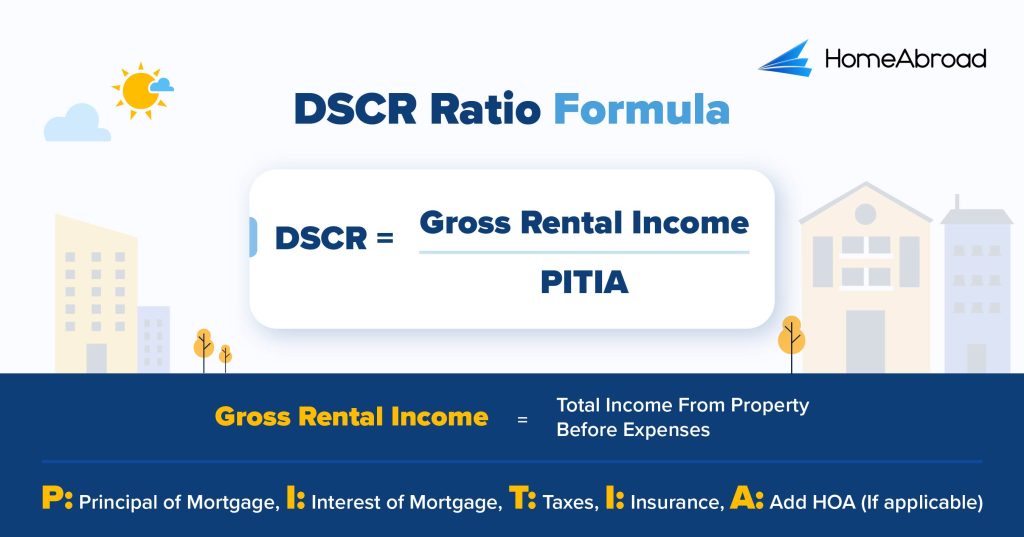

HomeAbroad’s DSCR loan qualifies you on the property’s rental income rather than your personal income, your employment history, or a US credit score. DSCR stands for Debt Service Coverage Ratio and measures whether a property’s rental income covers its monthly carrying cost.

Here is how the DSCR ratio is calculated:

This structure lines up well with turnkey for a specific reason. A turnkey property already has rent, which is the input DSCR underwriting weighs most heavily. There is no leasing period to wait through and no projection to defend, because a tenant is already paying.

One boundary worth setting before going further. Foreign national programs may not require an established US credit history, and HomeAbroad works with investors who have none. That is not the same as no credit review, no documentation, or approval regardless of the file.

You will still provide identity documents, proof of funds, reserve evidence, source-of-funds documentation showing how money moved from your home country, and full property documentation. What changes is the route to qualification, not the existence of underwriting.

In-Place Lease vs Market Rent, and Why the Difference Moves Your Loan

The provider placed the tenant. The provider set the rent. That lease is now a document in your loan file, and the number on it feeds directly into your DSCR calculation.

Separately, the appraisal on an investment property typically includes a rent schedule, which is the appraiser’s independent opinion of what the property should command in its market based on comparable rentals. Two rent figures, two sources, and they do not always agree.

Which figure your loan qualifies on is a program-level rule. Some programs use the in-place lease. Some use appraised market rent. Some use the lesser of the two, which is the version that surprises people, because it means an optimistic lease from the provider gains you nothing while a conservative appraisal can cost you.

Illustrative Example

Consider a single-family rental where the monthly PITIA is $1,850.

The provider’s lease shows monthly rent of $2,150, resulting in a DSCR of 1.16

$2,150 ÷ $1,850 = DSCR of 1.16

However, the appraiser’s Form 1007 estimates the property’s market rent at $1,925. Using that figure, the DSCR falls to 1.04.

$1,925 ÷ $1,850 = DSCR of 1.04

Both ratios are above 1.0, meaning the property’s rental income covers its monthly housing payment. Both would meet HomeAbroad’s minimum DSCR requirement, but the $225 difference in monthly rent can still affect loan pricing and other financing terms.

Know which rental income figure your financing depends on before you go under contract, not after the appraisal is complete.

Down Payment, Reserves, and Loan-to-Value

Qualifying based on rental income is only part of the process. Foreign national investors should also plan for the upfront cash required to close. HomeAbroad’s DSCR loan offers financing up to 75% loan-to-value (LTV) for purchases, so a minimum 25% down payment is generally required. Borrowers must also maintain at least six months of PITIA in post-closing reserves.

Unlike a down payment or closing costs, reserves are funds you keep after closing. They provide a financial cushion for vacancies, unexpected repairs, or temporary interruptions in rental income. Many first-time foreign investors budget for the purchase itself but overlook reserve requirements until late in the loan process, making it important to account for them from the beginning.

Before you go under contract, ask the provider for the lease, property management agreement, renovation scope, rent roll if available, and any documents supporting the property’s condition and rental income. Getting those into underwriting early helps identify questions before they become closing delays.

Four Turnkey-Specific Frictions Most Guides Skip

Everything above applies to any DSCR-financed rental. The four issues below are specific to the turnkey model, and they are the reason a turnkey file can behave differently from a property you sourced yourself.

The most common reason a turnkey purchase slows down isn’t the property itself. It’s missing or inconsistent documentation between the listing, the lease, the appraisal, and the underwriting file. When those documents tell the same story from the beginning, the path to closing is usually much smoother.

Rapid Resale and the Valuation Question

Think about the transaction history of a turnkey property. The provider bought it, often distressed and often at a low price. They renovated it over a few months before listing it for sale at a substantially higher price.That history is visible. It appears in public records and is reflected in the appraisal.

A property that changed hands recently at a much lower price, followed by a significant increase in value over a short period, naturally receives closer scrutiny from the appraiser and underwriter. The renovation may fully justify the higher price. The appraiser’s role is to determine whether the property’s condition, improvements, and comparable sales support that value.

Renovation Quality vs Appraisal Condition Rating

The renovation was scoped by the seller, to the seller’s budget, with the seller’s margin in mind. Where it becomes your concern is during the appraisal. The appraiser assigns a C1 through C6 condition rating based on the property’s overall condition, considering both cosmetic improvements and major building systems such as the roof, HVAC, electrical panels, plumbing, and foundation.

A property can look immaculate with fresh paint, new flooring, cabinets, and fixtures while still carrying a fifteen-year-old roof or aging mechanical systems. Those systems influence the appraisal regardless of how attractive the renovation appears.

The Provider’s Pro Forma Is Not an Underwriting Document

You will be sent a spreadsheet. It will show a purchase price, a rent figure, a set of expenses, and a return.

That spreadsheet is a sales document. It was built to make the property look worth buying, which is what sales documents are for. Underwriting doesn’t use it, and your decision shouldn’t either.

Common gaps: vacancy assumed at zero or near zero, maintenance held at an optimistic percentage of rent, no capital expenditure reserve for systems that will eventually need replacing, property management fees excluded or understated. Insurance costs have increased significantly in many US markets in recent years, so always obtain a current insurance quote rather than relying on older projections.

Rebuild the numbers yourself, using rent you verified from a source that is not the seller and expenses you priced independently. If the deal still works, you’ve learned something real. If it doesn’t, you’ve learned that too.

In-House Property Management and the Conflict Question

Many turnkey providers manage the properties they sell. Consider what that arrangement means structurally. The party that set the rent is the party reporting on the rent. The party that performed the renovation is the party that will quote you repairs on that renovation. The party that placed the tenant is the party that will tell you how the tenant is performing.

Plenty of integrated providers run clean operations, and there are genuine advantages to a team that knows the property from the studs out. But it is a structure you should recognize before you sign, because it removes the independent check you would otherwise have.

Two questions to ask directly. Am I required to use your management company? And if I switch to an independent management company after closing, what costs or restrictions apply?

How to Vet a Turnkey Provider from Outside the US

Everything below can be verified without leaving your country. Work through it before you make an offer, not after.

Renovation

- Itemized scope in writing, with systems listed separately from finishes

- Permits pulled for the work that required them, verified with the local building department

- Age and condition of roof, HVAC, water heater, electrical panel, and plumbing

- Any warranty on the work, in writing, and whether it transfers to you

- An independent inspection you commissioned and paid for, from an inspector with no relationship to the provider

Tenant

- The actual lease, not a summary

- Remaining term and renewal terms

- Payment history for the full tenancy

- The screening standard applied, including income multiple and background check scope

- Security deposit amount and how it transfers at closing

Numbers

- Rent verified against a source that is not the provider

- Actual expense history for the property, not projected figures

- Current property tax assessment, and whether it will reassess on sale

- An insurance quote in your name, current, for the actual property

Management

- In-house or independent

- Whether you are contractually required to use them

- Full fee schedule, including leasing fees, renewal fees, and maintenance markups

- Exit terms

- Reporting cadence and what the statement actually shows

Provider

- How long they have operated in this specific market

- Independent reviews outside their own website

- Complaint history with the state real estate commission and consumer protection agencies

- Whether they own the properties they sell or broker other people’s inventory

- References from investors who bought more than two years ago, not last quarter

At HomeAbroad, one of the most common causes of underwriting delays in turnkey purchases is incomplete or inconsistent property documentation, particularly when lease information, renovation details, or management records do not align across the loan file.

Buying a Turnkey Property Remotely

Buying a turnkey property from outside the US follows the same financing process as any other investment property purchase, but most of the process can be completed remotely.

Start with pre-approval. Knowing your loan amount before you review inventory means you’re comparing properties against real financing rather than a provider’s projection. Once your offer is accepted, underwriting begins while the appraisal is ordered through an independent appraisal management process. You do not commission the appraisal or select the appraiser, which helps ensure an independent assessment of both the property’s condition and its market rent.

At the same time, you’ll provide identity documents, proof of funds, and source-of-funds documentation showing how your purchase money moved from your home country into the transaction. For foreign national investors, documenting the movement of funds often takes longer than expected, particularly when money passes through multiple bank accounts or jurisdictions before reaching the US.

As the loan moves toward final approval, you’ll review the closing documents and coordinate signing. Remote closing and power of attorney arrangements are available in many situations, depending on your location and the closing requirements for the transaction.

If you’re signing documents outside the US, you may need notarization, apostille certification, or consular notarization, depending on your country and the documents involved. Your closing agent and lender will explain these requirements well before closing, giving you enough time to complete them without delaying the transaction.

Foreign national investors routinely complete financing and closing without traveling to the US. Availability depends on your country of residence and on the closing requirements in the state where you’re buying, so confirm both early rather than assuming they’ll resolve themselves.

Tax Realities Turnkey Marketing Leaves Out

Turnkey providers sell properties. They do not, as a rule, explain the US tax position of a nonresident owner, and the gap between a pro forma’s tax line and reality can be wide enough to change whether the investment works.

This section is general information, not tax advice. Cross-border tax positions turn on facts specific to you, and you should work with a qualified US tax professional before you buy.

Rental Income and the Section 871(d) Election

By default, a nonresident alien’s US rental income can be treated as fixed, determinable, annual, or periodical (FDAP) income and taxed on the gross amount without deductions for expenses. That means no deductions for mortgage interest, property taxes, insurance, property management fees, or other operating costs.

Section 871(d) is an election you make with the IRS to treat that rental income as effectively connected with a US trade or business, allowing it to be taxed on a net basis after eligible deductions. It is an election, not a treaty benefit, and it does not apply automatically. A pro forma showing rent minus expenses minus tax has quietly assumed this election exists.

The Pro Forma's Missing Line Many turnkey cash flow projections assume a tax outcome that depends on your tax elections and ownership structure. Before relying on projected after-tax returns, confirm how US tax rules apply to your specific situation.

FIRPTA at Exit

The Foreign Investment in Real Property Tax Act (FIRPTA) requires withholding when a foreign person sells US real property. The rate is tiered at 0%, 10%, or 15% depending on the sale price and the buyer’s intended use of the property. It is not a flat 15%, despite how often it is described that way.

Two points that catch investors. First, withholding is not the tax. It is an advance against the tax, and the reconciliation happens when you file. Second, tax treaties generally do not reduce FIRPTA withholding for individual nonresident alien sellers, which surprises people who assume a treaty covers it.

US Estate Tax

The federal estate tax exemption for a nonresident alien is generally limited to $60,000 of US-situs assets, which is substantially lower than the exemption available to US residents. A single rental property can exceed that threshold on its own, making ownership structure an important discussion to have before purchasing US real estate.

When Turnkey Fits, and When It Does Not

Turnkey May Be a Good Fit If You… | Turnkey May Not Be a Good Fit If You |

|---|---|

Want immediate rental income from a tenant in place. | Want to buy significantly below market value. |

Prefer a more passive investment with professional property management. | Plan to renovate and create equity yourself. |

Are investing remotely and value a move-in-ready property. | Want complete control over renovations and leasing decisions. |

Value predictable financing with an established rental history. | Are comfortable managing contractors, vacancies, and lease-up yourself. |

Prefer convenience over maximizing purchase discounts. | Expect turnkey properties to deliver the lowest acquisition price. |

Here is the honest version. Turnkey buys you operations. It does not buy you a discount. If your investment thesis requires buying below market, this model will not deliver it, and no amount of provider vetting changes that.

For a remote investor whose real constraint is presence rather than price, that trade is often worth making. The right choice depends on your investment strategy and how involved you want to be after closing.

Scaling beyond a single rental property changes the financing conversation. Equity requirements, reserves, and source-of-funds documentation become more important with each acquisition. Learn how foreign nationals build a US rental portfolio.

Ready to Finance a Turnkey Property?

Get pre-approved before you start reviewing inventory. Knowing your actual loan amount lets you evaluate properties against real financing rather than a provider’s projection, and it puts you in a stronger position when you make an offer.

HomeAbroad works with foreign national investors financing US rental property without an established US credit history, qualifying on the property’s rental income through DSCR programs built for international buyers.

Frequently Asked Questions

Are turnkey properties a good investment for foreign nationals?

They can be, particularly for a first US purchase made from outside the country, because the model solves the presence problem that blocks most other strategies. The trade is that you pay retail and inherit numbers the seller assembled. Turnkey works best for investors who verify those numbers independently and hold long term.

Can I get a DSCR loan on a tenant-occupied turnkey property?

An existing tenant is generally compatible with DSCR financing, and in-place rent is often helpful rather than a complication. What matters is which rent figure the program qualifies on and whether the lease documentation is complete. Confirm both before you go under contract.

Do I need to visit the US to buy a turnkey rental?

Not usually. Pre-approval, document submission, underwriting, and signing can typically be handled remotely, though the closing mechanics depend on the state and the transaction. Commission your own inspection regardless, since not being present makes independent verification more important rather than less.

What is the difference between turnkey and move-in ready?

Move-in ready describes physical condition. Turnkey usually implies condition plus a tenant plus management, though since neither term is standardized, treat both as starting points for questions rather than as answers.

Can I replace the turnkey provider’s property manager?

Sometimes. Some providers require their in-house management as a condition of sale, others allow you to choose. Ask before you sign, and ask what leaving costs.