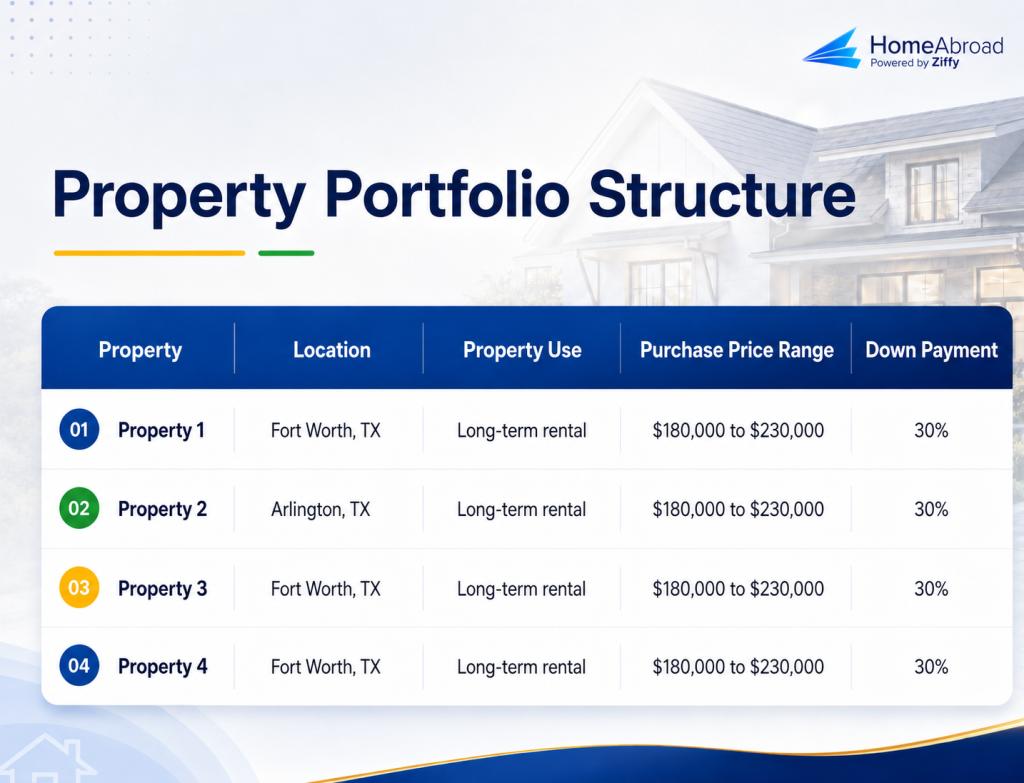

A Turkish B1/B2 visa holder purchased four rental homes in Texas through HomeAbroad over an eight-month period. Using approximately $220,000 in documented assets, the buyer made 30% down payments and kept the purchases within a $180,000 to $230,000 range.

The homes were located in Fort Worth, TX and Arlington, TX. The buyer purchased moderately priced single-family homes for long-term rental use, keeping enough capital available for each subsequent closing.

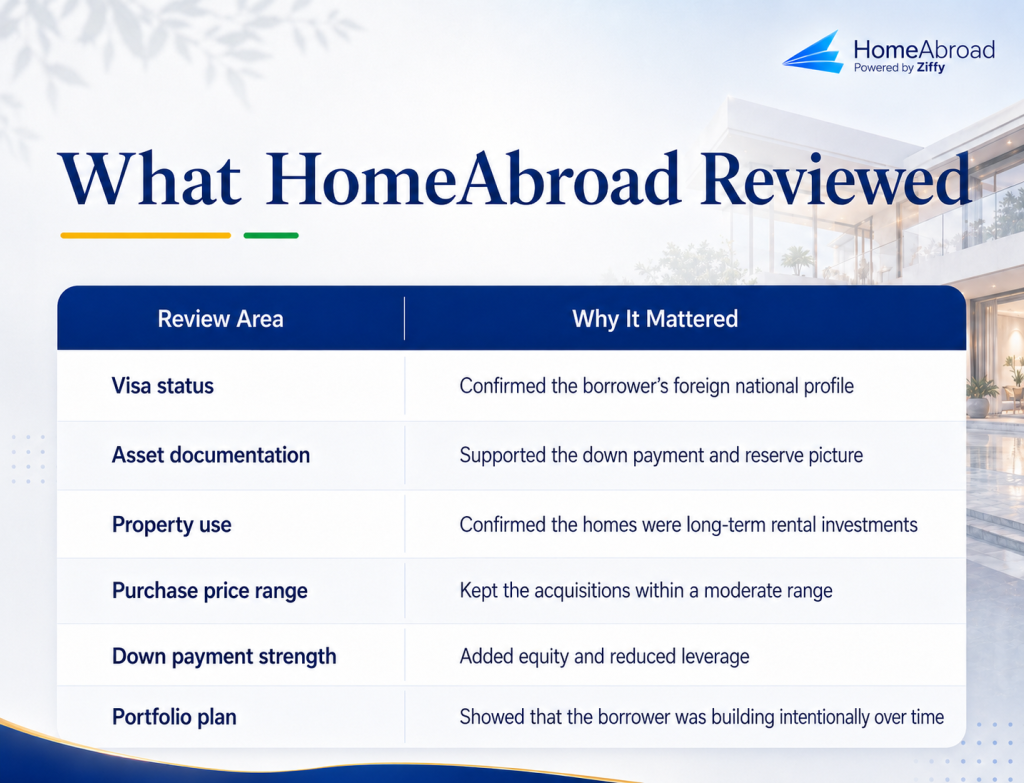

The US Department of State describes B-1/B-2 visitor visas as temporary nonimmigrant visas for foreign citizens entering the US for business, tourism, or a combination of both purposes. A B1/B2 loan package centers on visa documentation, assets, source-of-funds verification, down payment funds, reserves, and the intended use of the property.

Investment Highlights

Borrower Profile

Nationality: Turkish

Visa Type: B1/B2 visa

Financing Purpose: Portfolio growth through long-term rental purchases

Property Details

Property Use: Long-term rentals (4 properties in Texas)

Property Locations: Fort Worth, TX and Arlington, TX

Purchase Prices: $180,000 to $230,000 per property

Down Payment: 30%

Four Rental Investments for Portfolio Growth

HomeAbroad reviewed the plan as a portfolio acquisition from the first application. The initial loan package had to support the first closing while leaving enough liquidity for additional purchases.

Underwriting covered available assets, recent account activity, reserves, and the buyer’s ability to continue with later purchases after the first home closed. With purchase prices staying in a relatively narrow range, each new application opened in a context the underwriter already understood.

The 30% down payments kept equity in every property while spreading capital across four homes. For a buyer purchasing from outside the US, the loan package has to show real equity in each deal and enough liquidity after closing to support the next purchase.

Visa, Assets, and Source of Funds

HomeAbroad started with the visa and identity documents: status, passport, and source-of-funds trail. The financial picture then covered available assets, down payment funds, reserves, and intended rental use.

HomeAbroad needed to know where the funds were held, how long they had been there, and whether enough liquidity remained after closing costs. Remaining funds mattered as much as the down payment itself because the buyer was planning more than one acquisition.

After one home closed, the next submission needed updated bank statements, the new property obligation, and a current view of remaining funds. Spacing the purchases over eight months gave the buyer time to update documentation before each new application.

The borrower’s approach was not about stretching the numbers as far as possible. It was about using financing to build a portfolio in a controlled way.

Why Fort Worth and Arlington Worked for This Buyer

Fort Worth and Arlington gave the buyer access to the same broad North Texas rental region while staying within a moderate purchase range. Fort Worth had an estimated population of 1,028,117 as of July 1, 2025, according to the US Census Bureau. The broader Dallas-Fort Worth-Arlington metro reached about 8.48 million residents in 2025, according to FRED data from the Federal Reserve Bank of St. Louis.

In a metro of roughly 8.5 million residents, a long-term rental strategy has a broad tenant base to support a four-home portfolio. The properties were moderately priced rentals in a large housing market, intended for long-term holds.

Dorian Adams-Walker

Mortgage Loan Originator · HomeAbroad

By the second file, the borrower already understood what we needed to see: updated bank statements, a clean source-of-funds trail, and enough remaining liquidity after the prior closing. Later reviews moved more smoothly because the paperwork kept pace with the portfolio. The investor was building one purchase at a time, and the documentation had to stay current at each step.

Investment Properties on Sale Today

Where Similar Buyers Often Get Delayed

Documentation becomes harder when funds move across several accounts without explanation, the down payment source changes late, or too much liquidity is used on the first property.

Because the purchases were spaced over eight months, HomeAbroad could refresh the application after each closing, update the buyer’s obligations, and confirm the remaining funds before the next purchase moved forward.

Before selecting another property, buyers should have current bank statements, translated documents where needed, a clean explanation for large deposits, and enough liquidity after closing to support another purchase.

Start the Mortgage Review Before the Next Property Search

A buyer planning multiple rentals should speak with the lender before the next property search starts, especially before locking in a price range.

Before the next search, the most useful question to settle is how much capital needs to remain after this closing so the next purchase still works.

With that number in place, the search can be set around a price ceiling that leaves room for the next acquisition. Someone planning several purchases may need to stay below the maximum possible purchase price on the first home, preserve reserves, and avoid moving funds in ways that create documentation problems later.

Planning a US Rental Purchase From Abroad?

HomeAbroad helps foreign national buyers finance US real estate, including rental properties, with mortgage options designed for borrowers with limited or nontraditional US credit and income documentation.

If you are buying from outside the US, HomeAbroad can review your visa status, assets, down payment options, and property goals before you move forward with an offer.