![DSCR Loan Down Payment Requirements [2026]](https://homeabroadinc.com/wp-content/uploads/2023/01/DSCRDownPayment-500x325.jpg)

Editorial Integrity

Making informed real estate decisions starts with having the right knowledge. At HomeAbroad, we offer US mortgage products for foreign nationals & investors and have a network of 500+ expert HomeAbroad real estate agents to provide the expertise you need. Our content is written by licensed mortgage experts and seasoned real estate agents who share insights from their experience, helping thousands like you. Our strict editorial process ensures you receive reliable and accurate information.

Key Takeaways:

1. A higher down payment typically leads to lower interest rates, reduced monthly payments, and more favorable DSCR loan terms for investment properties.

2. Down payment requirements are influenced by factors such as the property’s DSCR ratio, overall cash flow strength, and property type rather than personal income.

3. With HomeAbroad's DSCR loan, Foreign national investors can qualify without a US credit history, though a higher down payment is often required to strengthen the deal profile.

4. HomeAbroad offers DSCR loans for foreign national investors, with down payment options starting at a minimum of 25%, structured to secure competitive financing terms.

At HomeAbroad, our DSCR loans for foreign national investors start with a minimum down payment of 25%. Based on our experience working with international buyers, this level helps balance risk, improve loan terms, and support sustainable rental cash flow.

We’ve helped over 500 foreign nationals close DSCR loans without a US credit history. For international investors, down payment size influences not just approval, but also interest rates, monthly payments, and how comfortably the property clears DSCR requirements.

What we see most often is that a higher down payment improves loan terms by lowering leverage, reducing monthly debt obligations, and creating more margin in the property’s cash flow. As a result, many investors choose to put more than the minimum down to secure better pricing and stronger long-term performance.

Whether your goal is to strengthen cash flow or qualify for more favorable loan terms, understanding how DSCR loan down payments work is essential to maximizing returns on US investment properties.

This guide breaks down HomeAbroad’s DSCR loan down payment requirements and explains how factors like DSCR ratio and property type influence what you need to bring to the table.

Table of Contents

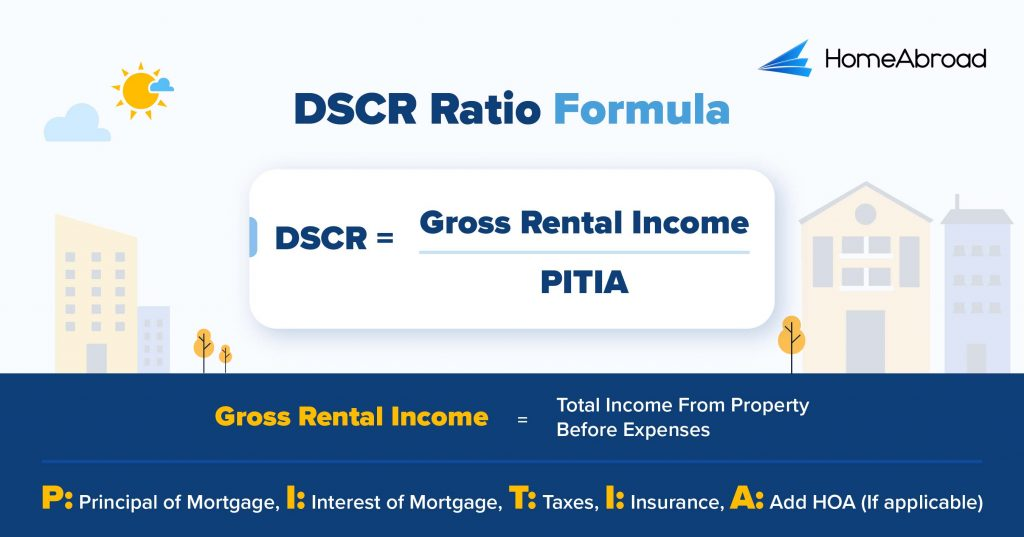

What is a DSCR Loan and How to Calculate it?

A DSCR (Debt Service Coverage Ratio) loan is a type of mortgage designed for real estate investors looking to purchase rental properties. Unlike conventional loans, DSCR loans allow investors to qualify based on the property’s income rather than their personal income.

The core metric for a DSCR loan is the DSCR ratio, which measures whether a property’s rental income is sufficient to cover its mortgage obligations. It’s a key factor we use to assess loan eligibility.

Here is the DSCR formula:

PITIA stands for Principal, Interest, Taxes, Insurance, and HOA dues (if applicable). It represents your total monthly debt obligation, not just the mortgage payment.

Steven Glick,

Director of Mortgage Sales, HomeAbroad | NMLS# 1231769

Recently, we worked with a Mexico-based investor purchasing a single-family rental property in Princeton, Texas, who wanted to qualify for a mortgage without relying on US income or credit history.

We structured the deal using a DSCR loan with a 25% down payment on a $240,000 property, where the qualification was based entirely on the property’s rental income. The income profile supported a DSCR above 1.0, meaning the property generated enough to cover its loan obligations, resulting in stable cash flow and a smooth approval process.

The loan was approved and closed within 28 days, allowing the investor to move forward without traditional income verification and continue building their portfolio.

If you’re exploring similar opportunities, you can learn more about how DSCR loans work in Texas and what to expect when investing in this market.

HomeAbroad’s DSCR loans qualify you based on a property’s rental income relative to mortgage payments. A standard DSCR loan requires the monthly gross rent to be equal to or greater than the mortgage payment (PITIA), which means a DSCR of 1.0 or higher is the ideal scenario for securing the best loan terms.

However, not all properties will meet this threshold, so we also offer our No-Ratio DSCR Program for properties with a DSCR between 0 and 1. This option allows investors to still qualify for financing, but it comes with a slightly larger down payment (a 5% hit to LTV) and higher interest rates. This program focuses less on rental income and more on other factors, giving investors with firm long-term plans the opportunity to secure financing.

At HomeAbroad, we offer tailored DSCR loans to help international real estate investors grow their portfolios with competitive loan terms. Learn more about the DSCR loan and application process in our DSCR Loan Guide.

DSCR Loan Down Payment Requirements Explained

At HomeAbroad, we typically require a 25% down payment for foreign investors. This ensures that international real estate investors have access to competitive loan options tailored to their individual financial profiles and investment goals.

The reason this matters is that down payment size directly affects leverage, pricing, and refinancing flexibility over the life of the loan. With DSCR loans, equity isn’t just about qualifying. It influences how resilient the deal is under real-world conditions.

When we evaluate DSCR loans, several key factors are directly shaped by the size of the down payment.

1. Loan-to-Value (LTV):

Our loan officers at HomeAbroad evaluate risk through the loan-to-value (LTV) ratio, which compares the loan amount to the property’s purchase price or appraised value. A larger down payment lowers the LTV, reducing risk and helping you secure better loan terms, including lower interest rates.

2. Rate-Term Refinance:

For those seeking to lower monthly payments or secure a more favourable interest rate, we offer rate-term refinance options, enabling you to refinance your DSCR loan without increasing your loan balance. In this scenario, maintaining a favourable LTV ratio is key, often based on your initial down payment and current property equity.

3. Cash-Out Refinance:

Our cash-out refinance option lets you tap into your property’s equity, allowing you to refinance for a larger amount than the current loan balance.

To be clear, we generally require a higher down payment or greater equity to ensure a strong LTV ratio and maintain competitive loan terms in these scenarios.

At HomeAbroad, we tailor our loan products and down payment requirements to support foreign national investors, ensuring you have the flexibility and financing options to maximize your investment returns.

Total Cash Required: Down Payment + Closing Costs

The down payment is only part of the total capital required for a DSCR loan. Many investors focus on the upfront percentage but overlook additional costs involved in closing the deal.

In our experience, first-time DSCR borrowers often underestimate closing costs, which typically range from 2% to 4% of the loan amount. This can add a significant amount on top of your down payment, so planning your total investment upfront is critical to avoid last-minute funding gaps.

Steven Glick,

Director of Mortgage Sales, HomeAbroad | NMLS# 1231769

DSCR Loan Down Payment Comparison Table

One of the most important factors in DSCR loans is how your down payment impacts your loan terms, flexibility, and qualification.

Down Payment | LTV | Typical Rate Impact | Monthly Payment (on $400K purchase) | Minimum DSCR Needed |

|---|---|---|---|---|

25% (minimum) | 75% | Base rate | ~$2,200–$2,600 | DSCR 1.0+ required for standard terms |

30% | 70% | ~0.25–0.50% lower | ~$2,050–$2,400 | 1.0 (more flexibility) |

35% | 65% | Slight additional improvement | ~$1,900–$2,200 | 1.0 (more flexibility) |

40%+ | 60% | Minimal rate change (best for flexibility) | ~$1,750–$2,000 | No-Ratio program eligible |

Note: These figures are illustrative examples. Actual rates, monthly payments, and DSCR requirements vary based on loan terms, interest rate, property taxes, insurance, HOA dues, and overall deal structure.

Check the latest DSCR loan interest rates to stay updated on current market pricing.

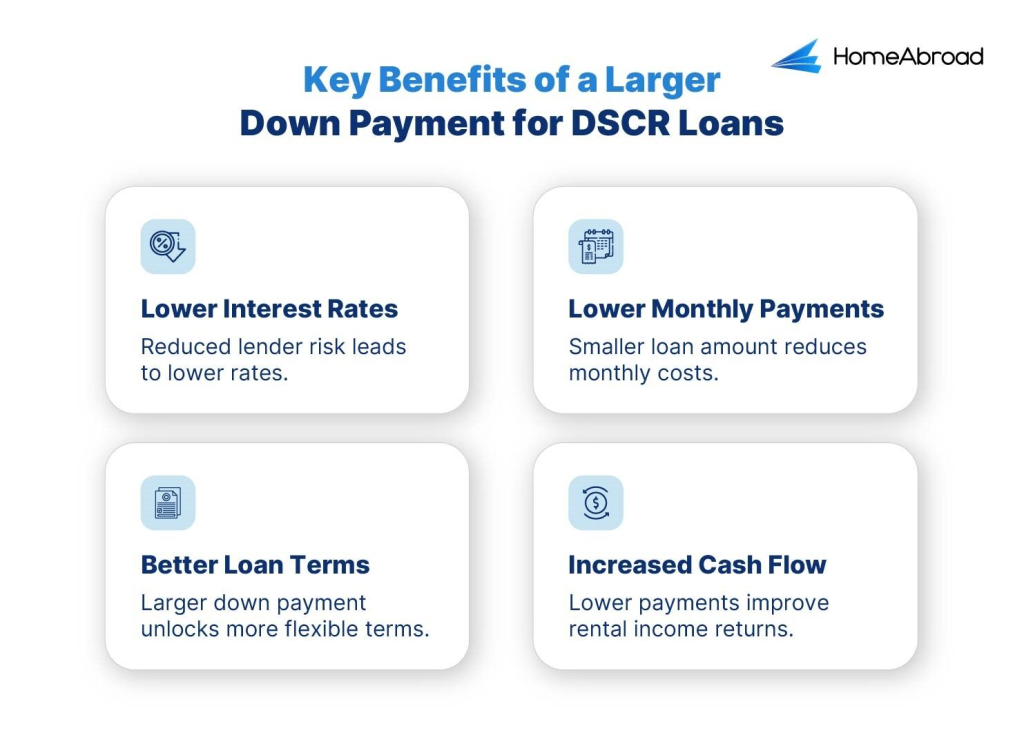

Benefits of a Larger Down Payment for DSCR Loans

For DSCR loans, down payment size does more than satisfy a requirement. It directly shapes pricing, cash flow stability, and long-term flexibility for international real estate investors.

What we see most often is that investors who commit more equity upfront gain meaningful advantages across the life of the loan, especially when the property income is the primary qualifying factor.

Here’s how a larger down payment works in your favor.

1. Lower Interest Rates

A larger down payment can significantly reduce the interest rate on your DSCR loan. Since the risk to HomeAbroad Loans is lower when more money is put down up front, we’re able to offer more competitive interest rates.

Here’s a real example from one of our recent deals that shows how this works:

We recently worked with a UK-based buyer purchasing a second home in Edgewater, Florida. By putting down 30% on a $292,000 property, the loan was structured at a lower risk tier, which allowed the borrower to qualify for more competitive pricing compared to minimum down payment scenarios. Even without a US credit history, the higher equity helped offset risk, resulting in smoother underwriting and a fixed rate of 7.624% with a 30-year term.

2. Lower Monthly Payments

A higher down payment also reduces your loan amount, leading to smaller monthly payments. With lower monthly debt obligations, you can maintain a more substantial cash flow from rental income, making the investment more sustainable over a 30-year term.

In our client’s case, the 30% down payment reduced the loan amount to $204,400 on a $292,000 property. This directly lowered the monthly payment obligation and made the overall deal more manageable, especially given the borrower had no US credit history. Lower leverage like this helps keep cash flow more stable over a 30-year term.

3. Better Loan Terms

At HomeAbroad, we reward larger down payments with improved loan terms. This might include more flexible repayment options, fewer prepayment penalties, or even faster loan approval. A higher down payment reduces risk, giving you leverage to negotiate terms that align with your investment goals.

The 30% down payment helped our client reduce overall lender risk, allowing the loan to be structured more efficiently despite having no US credit history. This led to a smoother underwriting process and a stable 30-year fixed loan with predictable long-term payments.

This example highlights how a higher down payment not only improves approval chances but also leads to more stable and investor-friendly loan structures.

What Factors Influence DSCR Loan Down Payment?

Down payment requirements for DSCR loans aren’t arbitrary. They’re driven by how the property performs, how income is generated, and how much risk exists in the overall structure of the deal.

At HomeAbroad, we tailor DSCR loan structures based on these variables rather than applying a one-size-fits-all rule. Below are the key factors that influence how much equity is required.

1. Debt Service Coverage Ratio (DSCR)

DSCR is one of the most direct inputs into down payment requirements. A higher DSCR indicates stronger cash flow relative to the debt, which lowers risk.

The reason this matters is that stronger cash flow gives us more flexibility on leverage. Properties with higher DSCR ratios may qualify with standard down payment requirements and more favorable terms.

However, we also offer our No-Ratio DSCR Program for properties with a DSCR between 0 and 1. This option allows investors to still qualify for financing. To be clear, it comes with a slightly larger down payment (a 5% hit to LTV) and higher interest rates to mitigate the additional risk.

2. Credit Score

At HomeAbroad, Foreign investors do not need a US credit history or employment verification, making DSCR loans more accessible to them. However, because foreign investors lack a US credit history, they are considered higher risk, resulting in a higher down payment requirement.

This ensures the loan remains stable while keeping qualification accessible to international investors.

3. Short-Term Rental Properties

Short-term rental (STR) properties are evaluated differently from long-term rentals when it comes to income qualification.

Instead of relying on a lease agreement or standard market rent, lenders typically look for 12 months of Airbnb or VRBO income history to determine qualifying income. If the property is newly acquired and has no operating history, underwriters may apply a conservative vacancy adjustment, often around 25–30%, to estimate income.

As a result, a property showing strong peak-season income may qualify at a lower effective monthly income. We’ve seen cases where properties with high gross earnings still fall below a 1.0 DSCR once seasonality and vacancy assumptions are applied.

This is why STR properties often require a higher down payment. The additional equity helps reduce the loan obligation and makes it easier for the property to meet DSCR requirements under more conservative income assumptions.

Steven Glick,

Director of Mortgage Sales, HomeAbroad | NMLS# 1231769

Use our Airbnb/STR calculator to model income scenarios with realistic vacancy assumptions.

4. Cash-Out Refinance Considerations

If you’re opting for a cash-out refinance, your down payment or existing equity becomes even more critical.

At HomeAbroad, we typically require you to have more equity in the property to maintain a favourable loan-to-value (LTV) ratio. The more equity or the larger the original down payment, the better terms you can secure on the refinance, giving you access to more cash while maintaining a healthy financial position.

5. Lender-Specific Requirements

At HomeAbroad, we understand that each investment is unique. That’s why our down payment requirements are flexible. For foreign investors, we generally require a 25% investment.

However, we assess factors such as property type, investment strategy, and financial profile to ensure we offer terms that align with your goals. Whether you’re purchasing a new property or refinancing, we work with you to tailor down payment options that best suit your needs.

Steven Glick,

Director of Mortgage Sales, HomeAbroad | NMLS# 1231769

Understanding these factors helps you plan your investment more effectively. At HomeAbroad, our goal is to structure each deal around your specific cash flow target, rather than fitting every deal into a fixed template.

Final Thoughts on DSCR Loan Down Payments

Understanding the down payment requirements for DSCR loans is essential for maximizing your investment opportunities. At HomeAbroad, we prioritise flexibility and tailor our down payment options to meet the unique needs of foreign investors.

Whether you’re aiming for better interest rates, lower monthly payments, or more favorable loan terms, your down payment plays a direct role in determining your rate tier and monthly payment. By aligning your down payment with your DSCR and investment strategy, you can structure the deal more effectively from the start.

At HomeAbroad, we go beyond just financing. As a one-stop PropTech and FinTech platform, we simplify the process of purchasing US real estate for international real estate investors by offering tailored foreign national mortgages and an AI-Native US Real Estate Investing Platform.

With access to a network of 500+ expert US real estate agents and comprehensive concierge services, from setting up LLCs to opening US bank accounts and coordinating property management, we ensure your investment journey is seamless and successful.

Ready to unlock the full potential of your real estate investments? Connect with HomeAbroad today and explore how our competitive and accessible DSCR loans can help you build lasting wealth in the US market.

Frequently Asked Questions

What is the minimum down payment required for a DSCR loan?

At HomeAbroad, foreign investors typically need a minimum 25% down payment for DSCR loans, which helps maintain a strong equity position and secure better loan terms.

Can I qualify for a DSCR loan with no US credit history?

Yes, at HomeAbroad, foreign nationals can qualify for a DSCR loan without a US credit history, as approval is based on the property’s rental income rather than personal credit.

Can I lower my interest rate with a larger down payment?

Yes, a larger down payment can help reduce your interest rate by lowering the loan-to-value (LTV) ratio and overall risk.

Are short-term rental properties eligible for DSCR loans?

Yes, HomeAbroad offers DSCR loans for short-term rental properties. However, due to income variability, these properties may require a higher down payment and more conservative income evaluation.

How much cash do I need upfront for a DSCR loan?

In addition to the down payment, investors should plan for closing costs (typically 2–4% of the loan amount), along with reserves and other transaction expenses.

Can I use funds wired from overseas for my down payment?

Yes, but the funds must be sourced and seasoned. Most lenders require at least 60 days of bank statements showing the funds in a verifiable account.

![DSCR Loans Guide for Foreign Nationals: What It Is & How to Apply in [2026]](https://homeabroadinc.com/wp-content/uploads/2022/06/dscr-loan-guide-FN.png)

![DSCR Loan Rates Today [April, 2026]](https://homeabroadinc.com/wp-content/uploads/2022/09/dscr-loan-interest-rates.png)