Editorial Integrity

Making informed real estate decisions starts with having the right knowledge. At HomeAbroad, we offer US mortgage products for foreign nationals & investors and have a network of 500+ expert HomeAbroad real estate agents to provide the expertise you need. Our content is written by licensed mortgage experts and seasoned real estate agents who share insights from their experience, helping thousands like you. Our strict editorial process ensures you receive reliable and accurate information.

Key Takeaways

1. Non-resident aliens can finance US property purchases through foreign national and DSCR mortgage programs even without US income, a Social Security number, or a US credit history.

2. HomeAbroad’s DSCR loans qualify the property based on rental income rather than the borrower’s personal income, making them one of the most efficient financing options for overseas investors.

3. Foreign national full-documentation loans typically require larger down payments, international credit verification, foreign income documentation, and 6–12 months of reserves compared to standard US mortgages.

4. FIRPTA withholding, Section 871(d) tax elections, and US estate-tax exposure are critical considerations for non-resident alien buyers and should be planned before closing, not after purchase.

5. Non-resident alien buyers can complete the entire mortgage process remotely through HomeAbroad, including pre-qualification, underwriting, and closing, without traveling to the United States.

Table of Contents

Most mortgage guides explain how visa holders living in the United States can finance a property. This guide is for a very different buyer: someone living outside the US who wants to purchase American real estate and needs financing to do it remotely.

For non-resident aliens, the mortgage process operates under a completely different set of rules. Conventional Fannie Mae and Freddie Mac financing is generally unavailable, US credit history may not exist, overseas wire transfers require additional documentation, and lenders evaluate foreign income and reserves through specialized underwriting programs built specifically for international buyers.

Based on HomeAbroad’s experience helping 500+ foreign national and visa-holder borrowers from 40+ countries finance US real estate, one of the most common questions we hear is: “Can I even get a mortgage without a US address?” The answer is yes, but through a financing path that most traditional lenders do not offer.

This guide explains how non resident alien mortgages actually work, including the loan options available, qualification requirements, DSCR financing, remote-closing procedures, tax exposure under FIRPTA and Section 871(d), and the ownership structures foreign buyers should understand before purchasing property in the United States.

Who Is a Non Resident Alien? (And Why the Definition Matters for Your Mortgage)

The IRS Definition vs. the Lender Definition

From a US tax perspective, a non-resident alien (NRA) is generally a foreign national who has not passed either the Green Card Test or the Substantial Presence Test established by the IRS. In simple terms, the person does not hold permanent US residency and does not spend enough time physically present in the United States to be treated as a US tax resident.

Mortgage underwriting, however, does not always follow the IRS definition exactly.

Many lenders apply their own overlays based on where the borrower lives, earns income, holds assets, and plans to purchase property. Some portfolio and non-QM lenders focus less on formal IRS residency classification and more on practical underwriting questions:

- Does the borrower live outside the US?

- Is the income earned abroad?

- Is there US credit history?

- Can reserves and source of funds be verified internationally?

The distinction here is that non-permanent residents living in the US can often access Fannie Mae-backed conventional financing. Non-resident aliens generally cannot. Buyers living abroad are usually locked out of the agency mortgage market entirely and instead qualify through specialized foreign national loan structures.

NRA vs. Non-Permanent Resident Alien: Not the Same Thing

This is one of the most commonly misunderstood parts of the foreign national mortgage market.

A non-permanent resident alien typically lives inside the United States on a valid visa such as an H-1B, L-1, or E-2 visa. These borrowers may have US employment, US tax returns, Social Security numbers, and domestic credit history.

A non-resident alien is different. The borrower lives outside the United States entirely and is purchasing US real estate remotely as an overseas investor, second-home buyer, or cross-border property owner.

Even though both borrower categories are foreign nationals, the mortgage paths are completely different because the underwriting risk profile is different.

Borrower Type | Fannie Mae / Freddie Mac | FHA Loans | DSCR Loans | Full Documentation loan |

|---|---|---|---|---|

Permanent Resident Alien | Yes | Yes | Yes | Yes |

Non-Permanent Resident Alien | Usually yes, if visa and credit requirements are met | No (post-May 2025 HUD changes) | Yes | Yes |

Non-Resident Alien (NRA) | No | No | Yes | Yes |

What Actually Changes When You’re Buying from Abroad

Financing US property as a true non-resident alien works differently from a standard domestic mortgage in almost every major area of underwriting.

For non-resident alien buyers, the financing process works very differently from a standard US mortgage. Most borrowers living abroad cannot use Fannie Mae, Freddie Mac, FHA, or other agency-backed loan programs. Instead, HomeAbroad structures financing through foreign national mortgage programs such as DSCR loans and Full Documentation loans that are designed specifically for international buyers.

One thing that surprises many overseas investors is that a US credit history is often not required. HomeAbroad can qualify many foreign national borrowers using alternative financial documentation instead. Depending on the program, this may include International Credit Reports (ICRs), foreign bank reference letters, overseas mortgage-payment history, or reserve verification from international financial institutions.

The financial requirements are also different from what most US-based borrowers expect. Foreign national buyers usually need larger down payments, commonly around 20–25%, along with additional reserve funds that remain available after closing. The reserve requirement becomes especially important for investment-property financing and DSCR loans.

The operational side of the transaction also requires more coordination. Overseas wire transfers need a clear paper trail showing where the funds originated, particularly when money moves across multiple international accounts before closing. Remote closings may also involve Power of Attorney documentation, apostille requirements, or Remote Online Notarization, depending on the property state and transaction structure.

To be clear, non resident alien mortgages are widely available through specialized foreign national mortgage programs. But the terms, rates, down payments, and reserve requirements differ from what domestic US borrowers typically receive.

Non Resident Alien Mortgage Options: Which Loan Type Fits Your Situation

At HomeAbroad, we offer multiple mortgage solutions specifically designed for non-resident alien buyers purchasing US real estate from abroad. The right loan structure depends on how the property will be used, how income is documented, whether the borrower has US credit history, and how much flexibility is needed after closing.

1. Full Documentation Loan

HomeAbroad’s full-documentation foreign national mortgage program is designed for international buyers living outside the United States who want to qualify using personal income and assets.

These loans are commonly used for:

- Vacation homes

- Second homes

- Investment properties

- Higher-value residential purchases

Qualification is based on the borrower’s financial profile rather than only the property’s rental income.

We review:

- Foreign employment income

- Overseas business income

- Two years of foreign tax returns

- Employer letters

- Foreign bank statements

- International credit history

Instead of relying only on traditional US credit scores, qualification may also use:

- International Credit Reports (ICRs)

- Foreign mortgage-payment history

- Bank reference letters

- Verified foreign tradelines

Down payments start around 20%, depending on the borrower profile, property type, reserves, and country of residence.

What most guides do not mention is that foreign income documentation is not standardized across the industry. Some mortgage programs accept translated foreign pay stubs and bank statements, while others require notarized translations, international bank references, or additional source-of-income verification. In practice, understanding which documentation format works for which loan structure matters more than simply understanding the published guidelines.

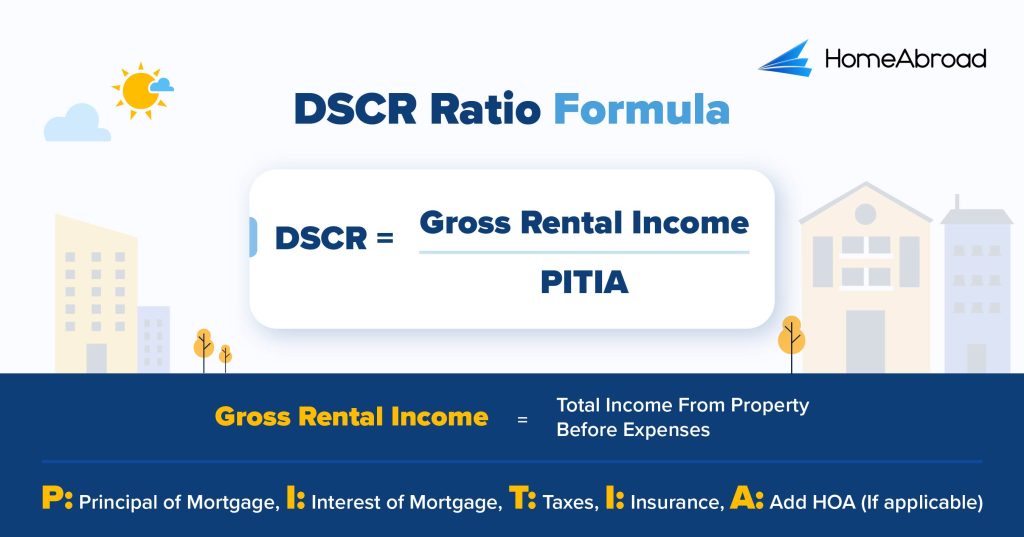

2. DSCR Loan (Debt Service Coverage Ratio)

For many non-resident alien investors, HomeAbroad’s DSCR loan program is the most efficient financing option available.

Instead of qualifying the borrower’s personal income, DSCR underwriting qualifies the property itself based on rental cash flow.

The DSCR formula is:

In practical terms, the property’s rental income is compared against its monthly PITIA obligations:

- Principal

- Interest

- Taxes

- Insurance

- Association dues

We require the property to achieve a DSCR ratio of 1 or higher. For properties with DSCR 0-1, we offer a No ratio DSCR loan.

The biggest advantage for buyers living abroad is simplicity. HomeAbroad’s DSCR programs generally do not require:

- US employment history

- Foreign income verification

- Social Security numbers

- Traditional US credit history

Instead, the focus shifts almost entirely to:

- Rental-income potential

- Down payment

- Reserve funds

- Property appraisal and rent analysis

HomeAbroad’s DSCR programs require:

- 25% down payment

- 6 months of reserves

- Passport identification or ITIN

- Investment-property use only

DSCR financing is commonly used for:

- Single-family rentals

- 2–4 unit properties

- Long-term rentals

- Short-term rental investments

The limitation is that DSCR loans are not intended for primary residences or personal-use vacation homes.

3. Asset-Depletion / Asset-Based Loan

Asset-based financing is designed for borrowers with substantial liquid assets but inconsistent or difficult-to-document income.

Instead of reviewing employment income, these programs calculate a synthetic monthly income using:

- Offshore cash reserves

- Investment portfolios

- Liquid financial assets

This structure is commonly used by:

- Retired international buyers

- High-net-worth individuals

- Investors with large offshore portfolios

- Buyers with irregular income streams

For asset-based qualification, lenders focus heavily on liquidity and documentation quality. Assets usually must be verifiable through official statements, seasoned for a minimum period before application, transferable between international and US banking systems, and held at recognized financial institutions with clear ownership records.

4. Bank Statement Loan

Bank statement loans are primarily designed for self-employed foreign nationals operating businesses outside the United States.

Instead of relying entirely on tax returns, underwriting reviews:

- 12–24 months of personal bank statements

- Business bank statements

- Deposit history

- Cash-flow consistency

Average monthly deposits are then used to estimate qualifying income.

This structure is especially useful for international business owners whose tax returns may understate actual cash flow because of:

- Business deductions

- International accounting structures

- Foreign tax treatment differences

Depending on the country and documentation type, certified translations or notarization may also be required.

Loan Type | NRA Eligible | Income Required | US Credit Required | Minimum Down Payment | Best For |

|---|---|---|---|---|---|

Full-Documentation Loan | Yes | Yes | No | 20% | Vacation homes, second homes, investment properties |

DSCR Loan | Yes | No | No | 25% | Rental-property investors |

Asset-Based Loan | Yes | Asset qualification only | No | 25–35% | HNWIs, retirees, asset-rich buyers |

Bank Statement Loan | Yes | Bank deposits | No | 25–35% | Self-employed foreign nationals |

What HomeAbroad Requires from Non-Resident Alien Borrowers

At HomeAbroad, non-resident alien mortgage qualification is primarily documentation-driven. Because the borrower lives outside the United States, we spend more time verifying identity, source of funds, international creditworthiness, and cross-border money movement than would typically be required for a standard domestic mortgage.

The exact requirements vary depending on the loan structure, but most foreign national mortgage programs review the same core documentation categories.

Identity and Immigration Documents

Every non-resident alien borrower must provide valid identification and proof of legal international status.

HomeAbroad commonly requires:

- A valid foreign passport

- Visa documentation if applicable, including B1/B2 visas, investor visas, or visa-waiver confirmation

- Entry documentation for borrowers traveling into the United States during the transaction process

A Social Security number is not usually required for HomeAbroad’s foreign national or DSCR mortgage programs. Many borrowers qualify using an Individual Taxpayer Identification Number (ITIN), while DSCR structures rely entirely on passport identification.

The distinction here is important because the underwriting focus is not immigration sponsorship or US employment authorization. HomeAbroad primarily verifies identity, international financial standing, and the borrower’s ability to complete the transaction legally and financially from abroad.

Credit and Financial History

Because many overseas buyers do not have traditional US credit history, HomeAbroad uses alternative credit-verification methods for foreign national mortgage qualification.

The most common option is an International Credit Report (ICR) sourced from the borrower’s home-country credit bureau.

If an ICR is unavailable, HomeAbroad may request:

- Two foreign tradeline reference letters

- Overseas mortgage-payment history

- Verified bank references

- 12-month account payment histories from financial institutions

These reference documents generally confirm:

- Account ownership

- Payment history

- Outstanding balances

- Account type

- Length of relationship with the institution

If the borrower already has a US credit history, we may review it, but most foreign national mortgage programs do not require it.

One major advantage of our DSCR loan programs is that we do not require personal income verification, employment verification, or traditional US credit qualification. Instead, underwriting focuses primarily on the property’s rental income, reserve strength, down payment, and overall cash-flow performance.

Income and Employment Documentation

Documentation requirements depend heavily on the mortgage structure.

For HomeAbroad’s full-documentation foreign national mortgage programs, we commonly request:

- Foreign employment contracts

- Overseas pay stubs

- Two years of foreign tax returns

- Employer letters on company letterhead

- Foreign bank statements showing income deposits

Self-employed borrowers may also need:

- Business registration documents

- Profit-and-loss statements

- 12–24 months of business bank statements

HomeAbroad’s DSCR loans are structured differently because qualification is based primarily on the property’s rental income rather than the borrower’s personal income.

Assets and Down Payment Documentation

HomeAbroad also verifies where the down payment funds and reserves originate.

Most programs require:

- Three to six months of bank statements

- Seasoned liquid funds

- Source-of-funds documentation for large transfers

- Post-closing reserve verification

Wire-transfer documentation becomes especially important for overseas buyers. HomeAbroad may request:

- Source-of-funds letters

- Bank confirmations

- Currency conversion records

- Exchange-rate documentation

- Transfer histories between international accounts

A pattern we’ve noticed across foreign national mortgage files is that the wire-documentation stage is where transactions slow down most often. The funds usually exist, but the paper trail is incomplete. Buyers living abroad should start documenting their source of funds 60–90 days before applying rather than trying to reconstruct transfers during underwriting.

How the Non-Resident Alien Mortgage Process Works, From Abroad

At HomeAbroad, the non resident alien mortgage process is designed to work fully remotely for buyers living outside the United States. From pre-qualification to closing, most of the transaction can be completed without the buyer traveling to the US.

The process itself is different from a standard domestic mortgage because international documentation, overseas funds movement, and remote closing coordination all require additional verification upfront.

Step 1: Choose the Right Mortgage Structure

The first step is identifying which financing structure fits the buyer’s situation and property strategy.

At HomeAbroad, non-resident alien buyers commonly qualify through:

- Foreign national full-documentation loans

- DSCR loans

- Asset-based mortgage programs

- Bank statement loans for self-employed foreign nationals

The correct structure depends on:

- Whether the property is a second home or investment property

- Whether the borrower wants income-based or DSCR qualification

- How income and assets are documented internationally

- Down payment and reserve availability

For buyers living abroad, selecting the right loan structure early matters because documentation standards vary significantly between programs.

Step 2: Pre-Qualification

The pre-qualification process is handled remotely and does not require the buyer to be physically present in the United States.

At this stage, HomeAbroad reviews:

- Passport documentation

- Basic income or asset documentation

- Estimated down payment funds

- Reserve availability

- Rental-income projections for DSCR loans

The goal is to establish a realistic purchase budget before property shopping begins.

For international buyers, pre-qualification also helps strengthen offers with sellers and real estate agents who may be unfamiliar with non-resident alien financing.

Step 3: Property Selection and Offer

Once pre-qualified, buyers can begin searching for properties that align with both their investment goals and financing eligibility.

Property type affects financing more than many overseas buyers expect. For example:

- Condos may require additional approval review

- Short-term rentals may require DSCR-specific underwriting

- Multifamily properties use different reserve and appraisal calculations

Many HomeAbroad clients also work with agents holding the CIPS (Certified International Property Specialist) designation because they specialize in cross-border real estate transactions.

Step 4: Appraisal and Underwriting

After the property goes under contract, HomeAbroad coordinates the appraisal and underwriting process.

For DSCR loans, the appraisal also includes a market-rent analysis. That rental estimate, rather than only an existing lease agreement, is what determines the property’s DSCR calculation and final loan eligibility.

Underwriting also reviews:

- Source of funds

- Reserve documentation

- International credit references

- Identity verification

- Overseas wire-transfer history

Step 5: Remote Closing

Non-resident alien buyers can usually close on US property without traveling to the United States.

HomeAbroad commonly helps coordinate:

- Power of Attorney (POA) structures, where a designated individual signs on behalf of the buyer

- Remote Online Notarization (RON), available in many US states

- Foreign notarization with apostille authentication when required by the title company or closing attorney

Tax Implications of Buying US Property as a Non-Resident Alien

For non-resident alien buyers, financing is only one part of the transaction. US tax exposure begins the moment the property is purchased, and many of the most important decisions happen before closing rather than after.

This is where many generic mortgage guides fall short. The financing structure, ownership setup, rental strategy, and long-term exit plan all affect how a non-resident alien is taxed in the United States.

FIRPTA Withholding: The Three-Tier Structure

FIRPTA, short for the Foreign Investment in Real Property Tax Act, applies when a non-resident alien sells US real estate. It does not apply when the property is purchased.

Under current FIRPTA rules, withholding is generally structured at three levels:

- 0% if the buyer purchases the property as a primary residence and the sale price is $300,000 or less

- 10% for certain owner-occupied purchases between $300,000 and $1 million

- 15% for most other transactions, including investment properties and properties above $1 million

The withholding is handled by the buyer or settlement agent and is taken directly from the seller’s proceeds at closing.

What most guides do not explain is that FIRPTA affects the exit strategy, not the acquisition itself. Every non-resident alien purchasing US real estate today is effectively creating a future FIRPTA event when the property is eventually sold.

The important distinction is that FIRPTA withholding is not always the final tax liability. Non-resident alien sellers can apply for a FIRPTA withholding certificate if the actual tax owed is expected to be lower than the withholding amount.

Section 871(d) Election: Treating Rental Income as Effectively Connected Income

By default, non-resident aliens are generally subject to a flat 30% withholding structure on gross US rental income without deductions.

The Section 871(d) election changes that treatment significantly.

When properly filed, the election allows rental income to be treated as effectively connected income (ECI), which means the property owner can deduct:

- Mortgage interest

- Property taxes

- Depreciation

- Repairs and maintenance

- Insurance

- Property management fees

This can materially reduce the effective US tax burden for rental-property investors.

For example, a property generating $40,000 in annual rent with $28,000 in deductible expenses could otherwise face withholding exposure tied to the full gross rental amount. With a properly structured Section 871(d) election, taxation may instead apply only to the remaining net income.

The election also requires filing a US non-resident tax return using Form 1040-NR, which is why HomeAbroad generally recommends working with a US CPA experienced in international tax reporting.

US Estate Tax Exposure

Non-resident aliens also face a very different estate-tax structure than US citizens.

Under current US estate-tax rules, the exemption for non-resident aliens is generally only $60,000, compared to more than $13 million for US citizens and permanent residents.

That means US real estate owned directly by a non-resident alien may create substantial estate-tax exposure.

The structure becomes more complex because LLC ownership or foreign corporate ownership does not automatically eliminate estate-tax risk. In many cases, the IRS may still look through the ownership structure to the underlying foreign owner depending on how the entity is organized.

We recommend consulting a US-based CPA and estate-planning attorney before closing on US property. The tax exposure for non-resident alien buyers is real, and ownership structures are significantly easier to plan correctly before purchase than to restructure later.

Should You Buy as an Individual or Through an LLC?

For non-resident alien buyers, the ownership structure matters almost as much as the mortgage itself.

One of the most common questions HomeAbroad receives from overseas investors is whether the property should be purchased in a personal name or through a US LLC. The answer depends on the financing structure, long-term investment goals, tax planning strategy, and how the property will eventually be managed or sold.

DSCR loans are generally more flexible around LLC ownership. Some DSCR programs allow the property to vest directly in an LLC, while others require the borrower to qualify personally before transferring ownership into the entity after closing.

Foreign national full-documentation loans are different. These loans are still primarily underwritten to the individual borrower, and LLC ownership can add additional underwriting, title, and documentation complexity.

The reason many non-resident alien investors consider LLC ownership is because it can provide:

- Liability protection

- Separation between personal and investment activity

- Cleaner operational management

- Potential probate-planning advantages

At the same time, LLC ownership does not automatically eliminate US tax exposure for foreign owners.

This is where the structure becomes more nuanced. For non-resident alien estate-tax purposes, a single-member LLC is generally considered transparent, meaning the IRS may still look through the entity to the underlying foreign individual owner. FIRPTA withholding can also still apply when US real estate held through a pass-through entity is eventually sold.

More advanced structures, such as a foreign corporation owning a US LLC, may provide additional estate-tax planning advantages, but those structures require coordination with a US international tax attorney before purchase.

The right ownership setup depends on several factors:

- Property value

- Number of planned investments

- Home-country tax treaties

- Financing structure

- Long-term exit strategy

For buyers planning to scale beyond a single property, ownership structure decisions are usually easier and less expensive to solve before closing rather than restructuring everything later.

Where Are Non-Resident Alien Buyers Purchasing in the US?

As of recent National Association of Realtors (NAR) foreign-buyer activity data, Florida, Texas, California, Arizona, and New York continue to rank among the most active states for international real estate purchases. At HomeAbroad, these same markets consistently represent a large share of the non-resident alien mortgage activity we see across foreign national and DSCR loan programs.

The reasons vary by market. Florida and Arizona attract lifestyle-driven buyers looking for vacation homes, seasonal residences, and short-term rental opportunities. Miami, Orlando, and Scottsdale remain especially popular because of international connectivity, tourism demand, and established foreign-buyer communities.

Texas has become one of the strongest investor-focused markets for non-resident alien buyers because of population growth, business migration, and comparatively stronger rental cash-flow potential in cities like Dallas, Houston, and Austin.

California and New York remain globally recognized gateway markets, particularly for higher-net-worth international buyers seeking long-term asset preservation, education access, or part-time US residency exposure. At the same time, these markets often involve higher acquisition costs and tighter DSCR qualification because property values significantly outpace rental yields in many areas.

Market selection also affects financing eligibility directly. In DSCR lending, markets with stronger gross rental yields, such as parts of Miami, Dallas, and Phoenix, often support qualification more easily because rental income covers PITIA obligations more comfortably.

Condo-heavy markets create another layer of complexity. In cities like Miami and New York City, non-warrantable condo restrictions may limit financing options, reserve requirements, or available loan programs depending on the building structure and occupancy profile.

How HomeAbroad Supports Non-Resident Alien Mortgage Borrowers

HomeAbroad specializes in foreign national and DSCR mortgage programs built specifically for international buyers purchasing US real estate from abroad, including borrowers without US credit history or US-based income.

The process is structured to work remotely from start to finish. HomeAbroad helps coordinate:

- Remote pre-qualification

- foreign national mortgages without a US credit history

- International document preparation

- Wire-transfer documentation review

- International Credit Report (ICR) sourcing

- Foreign income translation guidance

- Remote closing coordination

We also connect buyers with CIPS-certified real estate agents experienced in cross-border transactions and international investment purchases.

Based on HomeAbroad’s experience helping 500+ foreign national and visa-holder borrowers finance US property, the biggest factor in a smooth closing is preparation. Buyers who organize source-of-funds documentation, reserve verification, and identity documents early usually move through underwriting significantly faster.

Get pre-qualified for a non-resident alien mortgage with HomeAbroad and identify the financing structure that fits your property goals, ownership strategy, and long-term investment plans before you go under contract.

Frequently Asked Questions

Can a non-resident alien get a mortgage in the United States?

Yes. Non-resident aliens can obtain US mortgage financing through foreign national mortgage programs, DSCR loans, and other non-QM loan structures designed specifically for international buyers. Conventional Fannie Mae, Freddie Mac, and FHA financing is generally not available to non-resident alien borrowers living outside the United States.

Do non-resident aliens need a Social Security number to get a US mortgage?

No. Many foreign national mortgage programs accept a valid foreign passport as the primary identification document. Some programs also accept an ITIN. DSCR loans for non-resident alien investors often require only a passport and valid international identification documentation rather than a Social Security number.

What is the minimum down payment for a non-resident alien mortgage?

Most foreign national mortgage programs require roughly 25–35% down depending on the property type, borrower profile, and reserve strength. DSCR loans for non-resident alien investors may allow lower down payments, often starting around 20–25%.

How does FIRPTA affect non-resident alien property buyers?

FIRPTA withholding applies when a non-resident alien sells US real estate, not when the property is purchased. Depending on the transaction structure, withholding may equal 0%, 10%, or 15% of the gross sale price. Understanding FIRPTA before buying matters because every future sale creates a potential withholding event.

Can a non-resident alien buy US investment property remotely without visiting the United States?

Yes. HomeAbroad regularly helps non-resident alien buyers complete US real estate purchases remotely. The transaction can usually be completed through Power of Attorney structures, Remote Online Notarization (RON), or foreign notarization with apostille authentication depending on the state and closing requirements.

Is DSCR the best loan for a non-resident alien buying investment property?

For many non-resident alien investors, yes. DSCR loans qualify primarily based on the property’s rental income rather than the borrower’s foreign income, employment history, or US credit profile. That makes DSCR financing one of the most efficient mortgage structures for overseas buyers purchasing US rental property.