Editorial Integrity

Making informed real estate decisions starts with having the right knowledge. At HomeAbroad, we offer US mortgage products for foreign nationals & investors and have a network of 500+ expert HomeAbroad real estate agents to provide the expertise you need. Our content is written by licensed mortgage experts and seasoned real estate agents who share insights from their experience, helping thousands like you. Our strict editorial process ensures you receive reliable and accurate information.

A US tax treaty typically does not eliminate FIRPTA withholding or significantly change the US tax treatment of rental income from US real estate.

For rental properties, the Section 871(d) election is often more important than treaty status because it allows qualifying investors to be taxed on net rental income rather than gross rent.

Tax treaties can have the greatest impact on estate tax planning, particularly for investors from countries with US estate tax treaty protection.

The most effective time to evaluate ownership structure, estate tax exposure, FIRPTA planning, and financing strategy is before purchasing a property, not after closing.

Table of Contents

US tax treaties and US real estate do not always interact the way foreign investors expect. Rental income, property sales, and estate tax exposure follow specific US tax rules that often remain in place regardless of treaty status.

HomeAbroad has helped more than 500 foreign national investors from over 40 countries finance US investment properties. A recurring question from investors is whether a tax treaty changes FIRPTA withholding, rental income taxation, or estate tax exposure. In many cases, the answer depends less on the treaty itself and more on factors such as the Section 871(d) election, FIRPTA planning strategies, ownership structure, and estate tax treaty eligibility.

This guide examines how tax treaties affect foreign real estate investors at three stages of ownership: holding a property, selling a property, and passing a property to heirs. You’ll see where treaty provisions can influence the outcome, where standard US real estate tax rules still apply, and which planning decisions deserve attention before investing.

The Treaty Question Most Foreign Investors Get Backwards

A tax treaty and a real estate tax benefit are not the same thing. One question comes up repeatedly when foreign investors begin researching US property taxes: “My country has a tax treaty with the United States. What does that actually change?” The answer is often less than investors expect.

Tax treaties can provide meaningful benefits in certain situations, but ownership of US real estate follows a different set of rules than many other cross-border investments. The result is that investors frequently spend time looking for treaty exemptions while overlooking planning decisions that have a much larger effect on rental income taxation, FIRPTA withholding, and estate exposure.

Tax treaties and mortgage eligibility are separate issues. Whether an investor comes from a treaty country or a non-treaty country, the financing process is driven by the loan program, property, and borrower qualifications. The tax planning conversation should happen alongside the financing conversation, not instead of it.

NMLS #1231769

For a broader overview of US tax obligations, see our guide to US taxes for foreign real estate buyers. If you’re specifically researching FIRPTA withholding rules when selling a property, our complete FIRPTA guide covers the sale process in detail.

What a Tax Treaty Actually Does And What It Doesn’t

What treaties are designed to do

Tax treaties are designed to prevent the same income from being taxed twice and to determine which country has the primary right to tax specific types of income. They also establish rules for claiming foreign tax credits, resolving residency conflicts, and reducing withholding on certain cross-border payments such as dividends, interest, and royalties.

US real estate follows a different framework. The United States retains taxing rights over income and gains derived from real property located within its borders. As a result, treaty benefits that apply to other types of cross-border income often do not change the core US tax treatment of rental income, property sales, or estate tax exposure tied to US real estate.

Why real estate is the big exception

Most US tax treaties contain an “immovable property” or “real property” article that gives the country where the property is located the right to tax income and gains from that property. Because the real estate is located in the United States, the US generally retains taxing rights regardless of where the owner lives.

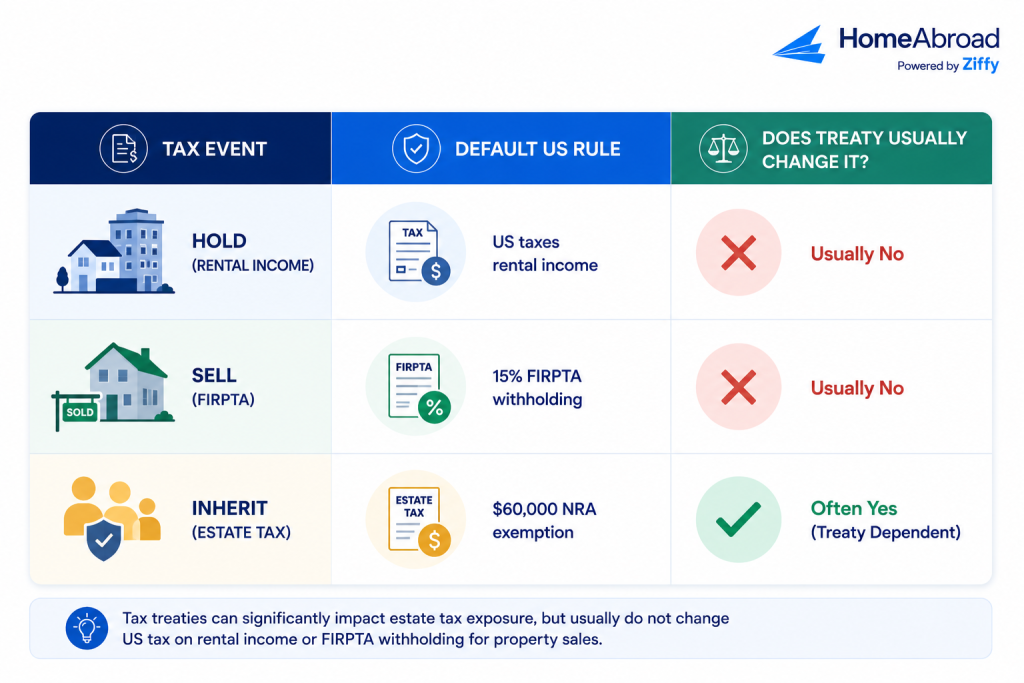

A tax treaty usually does not override the core US tax rules that apply when a foreign national earns rental income from US property, sells a US property, or passes away owning US real estate.

The three events where your home country may (or may not) matter

For foreign national investors, treaty benefits are easiest to understand by looking at three separate events: holding the property, selling the property, and passing the property to heirs.

When you earn rental income, the treaty usually does not reduce the US tax imposed on that income. When you sell the property, a treaty generally does not eliminate FIRPTA withholding for an individual investor. Estate planning is where treaty status can become much more important, because certain countries have estate tax treaties with the US that can significantly change estate tax exposure.

The role of a tax treaty can change depending on whether you’re collecting rental income, selling a property, or planning for inheritance. Looking at each stage separately makes it easier to identify where treaty provisions apply and where standard US tax rules continue to control the outcome.

Rental Income While You Hold: Treaty Vs The Section 871(d) Election

Rental income is often the first place foreign investors look for treaty benefits. The surprise for many property owners is that US real estate rental income follows rules that differ from many other cross-border income streams.

Does the treaty lower the 30%?

By default, rental income earned by a nonresident alien is generally treated as US-source Fixed, Determinable, Annual, or Periodical (FDAP) income and may be subject to a 30% tax on gross rental receipts. Because most US tax treaties preserve the United States’ right to tax income from US real estate, the treaty itself usually does not reduce this 30% treatment.

The distinction becomes important when comparing treaty benefits with the Section 871(d) election. Tax treaties often reduce withholding rates on certain types of passive income, such as dividends, interest, or royalties. Rental income from US real property is treated differently because the property is physically located in the United States.

The lever that actually helps: the Section 871(d) election

For many foreign real estate investors, the more important planning tool is the Section 871(d) election. Instead of being taxed on gross rental income, this election allows qualifying investors to treat rental activity as effectively connected income (ECI) and be taxed on net rental profit after deductible expenses.

That means expenses such as mortgage interest, property taxes, insurance, repairs, property management fees, and depreciation may reduce the taxable income generated by the property.

Jeff Larrabee

Senior Customer Loan Specialist, HomeAbroad

Many foreign investors initially focus on whether a tax treaty will reduce their rental income taxes. The conversation often shifts to the Section 871(d) election because being taxed on net rental profit instead of gross rent can have a much larger impact on the property’s after-tax performance.

The Section 871(d) election is a tax filing position with specific reporting requirements and deadlines. Investors should work with a qualified cross-border CPA to ensure it is implemented correctly. For a detailed explanation of how the election works, see our guide to US taxes for foreign real estate buyers.

Selling: Why a Treaty Usually Won’t Cut Your FIRPTA Withholding

When a foreign national sells US real estate, the transaction may be subject to the Foreign Investment in Real Property Tax Act (FIRPTA). Under current rules, buyers are generally required to withhold 15% of the gross sale price and remit it to the IRS. For a complete explanation of how FIRPTA works, see our detailed FIRPTA guide.

The myth: “My country has a treaty, so FIRPTA won’t apply”

This is one of the most common misconceptions among foreign investors. While the United States has income tax treaties with many countries, those treaties generally do not eliminate FIRPTA withholding for individual investors selling US real property.

The reason is that gain from the sale of a US real property interest (USRPI) is treated as effectively connected income (ECI), and most treaties preserve the United States’ right to tax gains derived from US real estate. In practical terms, owning property in a treaty country does not usually exempt an individual seller from FIRPTA withholding.

What actually reduces or recovers the withholding

A more useful planning discussion centers on withholding-reduction strategies. Form 8288-B, like-kind exchanges, and entity-level elections can influence the amount withheld or recovered after a sale.

One option is filing Form 8288-B, which allows the seller to request a withholding certificate based on the actual expected tax liability rather than the default 15% of the gross sale price. Investors completing a qualifying Section 1031 like-kind exchange may also qualify for relief under specific circumstances.

Certain transactions qualify for a non-foreign affidavit, but this does not apply to a true nonresident alien seller. At the entity level, a Section 897(i) election may be available to certain foreign corporations entitled to non-discriminatory treaty treatment. This is one of the few situations where treaty provisions can become relevant, but it applies to corporate structures rather than individual investors.

The cash-flow reality investors often overlook

FIRPTA withholding is calculated on the gross sale price, not the actual profit from the transaction. A property sold for $800,000 may trigger a $120,000 withholding obligation even if the seller’s taxable gain is substantially lower.

If too much tax is withheld, the excess is generally recovered through an approved withholding certificate or by filing a US tax return, typically Form 1040-NR. The challenge is timing. Investors may wait months before receiving funds that were withheld at closing, which can affect reinvestment plans and overall liquidity.

Myth vs. Reality

Myth: “My country’s tax treaty reduces FIRPTA withholding.”

Reality: Tax treaties do not reduce FIRPTA withholding for most individual investors. Form 8288-B is the primary withholding-relief mechanism.

Important: FIRPTA applies to property sales, not refinances. Foreign investors completing a cash-out refinance are not subject to FIRPTA withholding because ownership of the property is not being transferred.

Estate Tax: The Home-Country Lever That Actually Matters

For many foreign investors, estate tax is the part of US real estate taxation that receives the least attention before purchase and the most attention after a planning problem has already been created.

Unlike US citizens and residents, who receive a federal estate tax exemption of $15 million (2026), a nonresident alien generally receives an exemption of only $60,000 for US-situs assets. Because US real estate is considered a US-situs asset, a foreign national who owns property directly can create a significant estate tax exposure that many investors never anticipate.

Estate Tax Exposure:

US Citizen/Resident Exemption (2026): $15 million

Nonresident Alien Exemption: $60,000

Where the treaty genuinely changes the math

This is one area where your home country can have a meaningful impact.

The United States has estate and gift tax treaties with a limited number of countries. Depending on the treaty, a foreign investor may qualify for a pro-rated unified credit, modified situs rules, or other provisions that reduce potential estate tax exposure. Unlike FIRPTA withholding or rental income taxation, this is a situation where treaty status can materially affect the outcome.

For investors from treaty countries, estate planning often begins with understanding what protections already exist under the treaty before deciding how to structure ownership.

No estate treaty? Plan around it

Investors from countries without estate tax treaty protection often need to think about estate planning much earlier in the process. Ownership structure, financing strategy, debt placement, insurance planning, and succession goals can all influence long-term estate tax exposure.

Estate planning decisions have the greatest flexibility before a property is acquired. Once the investment is in place and the property has appreciated, restructuring options can become more limited and costly. Because estate planning is highly fact-specific, foreign investors should work with a qualified cross-border estate attorney and tax advisor before implementing any strategy.

Steven Glick

Director of Mortgage Sales

HomeAbroad

NMLS #1231769One pattern we see is that investors from countries with estate treaty protection often focus first on investment and financing decisions, while investors from non-treaty countries are more likely to ask ownership-structure questions before they purchase. Those conversations are much easier to have before closing than after the property is already in the portfolio.

For many foreign investors, estate tax planning can ultimately have a larger financial impact than FIRPTA withholding or annual rental-income taxation. Yet it is often the last topic discussed. Understanding whether your country has treaty protection is one of the most important planning steps to take before buying US real estate.

How Six Major Buyer Countries Compare

The same US property can create very different planning considerations depending on the investor’s country of residence. The most important distinction is not whether a country has an income tax treaty with the United States, but whether estate tax treaty protection exists.

As you’ve seen throughout this guide, income tax treaties generally do not eliminate US taxation of rental income from real property or FIRPTA withholding on a sale. Estate tax treaties, however, can materially change long-term estate tax exposure for foreign investors. Always verify treaty eligibility and benefits with a qualified cross-border tax advisor before relying on a treaty position.

Country |

| Estate/Gift Tax Treaty with US? | Effect on US Rental Income Tax | Effect on FIRPTA at Sale | Home-Country Planning Note |

|---|---|---|---|---|---|

Canada | Yes | Special estate tax relief through Article XXIX-B of the US-Canada Income Tax Treaty | No treaty reduction for US real-property rent; Section 871(d) is typically the key planning tool | Standard FIRPTA withholding applies. | Estate treaty relief can be significant for larger portfolios; coordinate foreign tax credit treatment with Canadian advisors |

China | Yes | No | No treaty reduction for US real-property rental income; Section 871(d) is generally the more important planning tool | No treaty reduction for individual sellers. | No US estate tax treaty protection. Chinese investors generally remain subject to the standard $60,000 NRA estate tax exemption, making ownership structure and estate planning important before purchase. |

India | Yes | No | No treaty reduction for US rental income from real property; Section 871(d) remains the primary planning election | Standard FIRPTA withholding applies. | No estate treaty protection; investors generally remain subject to the standard $60,000 NRA estate tax threshold |

United Kingdom | Yes | Yes |

| Treaty status does not alter individual FIRPTA withholding. | Estate and gift treaty provisions can materially affect estate planning and situs analysis |

UAE | No comprehensive income tax treaty | No | No treaty relief; Section 871(d) may still allow taxation on net rental profit instead of gross receipts | No treaty-based FIRPTA relief available. | No US treaty protection for estate tax purposes; estate exposure should be evaluated before purchase |

Australia | Yes | Yes | No treaty reduction for US real-property rental income; Section 871(d) often remains the more important planning tool | Standard FIRPTA rules remain in effect. | Estate treaty provisions can provide planning benefits even though Australia does not impose a domestic estate tax |

Verification note: Treaty provisions change over time and can contain country-specific conditions, elections, and residency requirements. Estate treaty eligibility should always be verified against current IRS treaty tables and the applicable treaty text before making ownership, financing, or estate-planning decisions.

Five mistakes treaty-country investors make

Investors from treaty countries often assume the treaty itself will solve most US tax issues. In practice, the biggest mistakes usually come from misunderstanding where treaty benefits apply and where they don’t.

Mistake #1: Assuming a treaty eliminates FIRPTA withholding

Many foreign investors expect a tax treaty to reduce or eliminate FIRPTA withholding when they sell a US property. For individual investors, that is generally not the case.

Fix: Review FIRPTA planning options early, including whether a Form 8288-B withholding certificate may reduce the amount withheld at closing.

Mistake #2: Skipping the Section 871(d) election

Some investors focus on treaty provisions and overlook the election that often has a greater impact on rental income taxation. Without a Section 871(d) election, rental income may be taxed under the default gross-income rules.

Fix: Discuss the Section 871(d) election with a qualified cross-border CPA before filing your US tax return.

Mistake #3: Discovering estate tax exposure after buying

A country may have an income tax treaty with the United States but no estate tax treaty. Many investors learn about the $60,000 nonresident alien estate tax exemption only after purchasing property.

Fix: Evaluate ownership structure and estate planning considerations before acquiring US real estate, not after.

Mistake #4: Filing Form 8288-B too late

Investors often wait until a property is under contract to begin FIRPTA planning. Unfortunately, withholding certificate requests can take time, and late filings may not prevent excess withholding at closing.

Fix: If a sale is likely, discuss Form 8288-B timing with your CPA before listing the property.

Mistake #5: Relying on advisors without cross-border experience

US real estate taxation for foreign investors involves treaty analysis, FIRPTA, estate tax exposure, and foreign tax credit coordination. A domestic-only tax advisor may not be familiar with these issues.

Fix: Work with professionals who regularly handle cross-border real estate transactions and foreign-national investors.

The investors who experience the fewest surprises are usually the ones who discuss their exit strategy before they buy. Bringing a cross-border CPA into the conversation early helps investors understand how rental income, a future sale, and estate planning fit together long before those decisions become time-sensitive.

The Bottom Line on US Tax Treaties and Real Estate Investing

Tax treaties can affect foreign real estate investors, but not always in the areas investors expect. For rental properties, the Section 871(d) election often has a greater impact than treaty status. When selling a property, FIRPTA withholding rules generally remain the same regardless of where the investor lives. Estate tax planning is where a treaty can make the biggest difference for some investors.

The common thread across all three stages is timing. Ownership structure, estate tax exposure, financing strategy, and exit planning are easier to address before purchasing a property than after the investment is already in place.

HomeAbroad helps foreign national investors finance US investment properties through DSCR loans and foreign national mortgage programs, including options for borrowers without US credit history. While your CPA or tax advisor handles the tax planning side, our team can help you evaluate financing options that align with your investment goals.

Ready to invest in US real estate? Get Pre-Qualified for a Foreign National Mortgage today.

Frequently Asked Questions

Does a US tax treaty reduce FIRPTA withholding?

Generally, no. For individual foreign investors, a US tax treaty does not typically eliminate or reduce FIRPTA withholding on the sale of US real estate. The more common way to reduce withholding is through Form 8288-B, which allows the IRS to calculate withholding based on the expected tax liability rather than the standard FIRPTA amount.

Do I pay 30% tax on my US rental income if my country has a treaty?

Possibly, but many investors elect to be taxed on net rental income instead. By default, rental income may be subject to a 30% tax on gross receipts. However, the Section 871(d) election allows qualifying foreign investors to report rental activity as effectively connected income and deduct eligible expenses before calculating tax.

Which countries have an estate tax treaty with the United States?

The United States has estate or estate-and-gift tax treaty arrangements with a limited number of countries, including the United Kingdom, Australia, Germany, France, Japan, the Netherlands, and several others. Treaty benefits vary by country, so investors should review the applicable treaty before relying on any estate tax protection.

Can a tax treaty help me avoid being taxed twice on a US property sale?

Yes. While a treaty generally does not eliminate US tax on the sale of US real estate, it may help prevent double taxation by allowing investors to claim foreign tax credits or similar relief in their home country for taxes paid to the United States. The specific treatment depends on the tax rules in your country of residence.

Does my home country’s treaty affect my mortgage eligibility?

No. Mortgage eligibility and tax treaty status are separate issues. Foreign national loan qualification is typically based on factors such as the property, loan program, available assets, and documentation requirements rather than whether your country has a tax treaty with the United States.

What matters more than treaty status when buying US real estate?

For many foreign investors, the most important planning decisions involve ownership structure, estate tax exposure, rental income elections, and FIRPTA planning. Understanding these issues before purchasing a property often has a greater financial impact than the treaty itself.