Editorial Integrity

Making informed real estate decisions starts with having the right knowledge. At HomeAbroad, we offer US mortgage products for foreign nationals & investors and have a network of 500+ expert HomeAbroad real estate agents to provide the expertise you need. Our content is written by licensed mortgage experts and seasoned real estate agents who share insights from their experience, helping thousands like you. Our strict editorial process ensures you receive reliable and accurate information.

Key Takeaways 1. Foreign national investors can use DSCR cash-out refinance loans to access equity from US rental properties without US income verification, W-2s, or traditional US credit history. 2. HomeAbroad’s DSCR refinance programs qualify primarily based on the property’s rental income relative to PITIA, with most programs allowing up to 75% LTV for qualified borrowers. 3. All-cash foreign buyers may qualify for delayed-financing refinance structures, allowing them to recover invested capital without waiting through long conventional seasoning periods. 4. The final cash-out amount depends on both appraisal value and DSCR performance. Higher refinance payments can reduce DSCR and lower the amount of accessible equity. 5. Cash-out refinance proceeds are generally not taxable income and do not trigger FIRPTA withholding, allowing foreign investors to access liquidity while keeping the property and rental-income stream intact.

Table of Contents

Foreign national investors who purchased US rental property a few years ago are often sitting on significant untapped equity through appreciation, principal paydown, or both. What many do not realize is that they may be able to access that equity through a DSCR cash-out refinance without needing US income verification, a US credit score, or traditional employment documentation.

For international investors, a cash out refinance is not just a way to lower a rate or restructure debt. It is a capital-recycling strategy. Instead of selling a performing rental property, foreign nationals can refinance the asset, pull equity out tax-efficiently, and use the proceeds to fund another acquisition, renovate an existing property, or expand into a new US market.

At HomeAbroad, we structure DSCR cash out refinance loans specifically for foreign national and non-resident alien investors purchasing and holding US rental property from abroad. This article explains how the process works, including qualification mechanics, DSCR requirements, LTV limits, delayed financing for all-cash buyers, what the cash can be used for, and the refinance process from application through closing.

Based on HomeAbroad’s experience helping 500+ foreign national and visa-holder borrowers finance US real estate, one pattern stands out clearly: investors who understand how to recycle equity early tend to scale their portfolios much faster than investors who leave capital trapped inside appreciated properties.

What a Cash Out Refinance Actually Does for a Foreign National Investor

A cash-out refinance allows a foreign national investor to replace an existing mortgage with a new, larger loan and receive the difference in cash at closing.

If the property is already owned free-and-clear, the refinance works as a first mortgage placed against the property’s equity.

The amount available depends on:

- Current property value

- Existing loan balance

- Maximum loan-to-value (LTV) allowed

- DSCR qualification

- Reserve requirements

For example, if a rental property is worth $500,000 and qualifies for a 75% LTV refinance, the maximum new loan amount would generally be $375,000. If the existing mortgage balance is $200,000, the remaining equity after payoff and closing costs may be received as cash.

It is important to distinguish between a rate-and-term refinance and a cash-out refinance.

A rate-and-term refinance restructures the existing mortgage to reduce the interest rate, change the loan term, or improve monthly cash flow without materially increasing the loan balance.

A cash-out refinance does the opposite. The loan balance increases because equity is being extracted from the property.

One of the most overlooked strategies for foreign national investors is delayed financing after an all-cash purchase.

Under HomeAbroad’s DSCR cash-out refinance programs, foreign nationals who purchased a property entirely with cash may be able to refinance shortly after closing and recover a significant portion of their original capital without waiting through long seasoning periods common in conventional lending.

What most guides do not cover is that all-cash buyers can often refinance into a DSCR loan as soon as the appraisal, title work, and ownership documentation are complete. In many cases, there is no requirement to wait 6–12 months before accessing equity the way conventional agency programs typically require.

For international investors, this creates a powerful capital-recycling strategy: acquire quickly with cash, stabilize the property, then refinance to recover capital for the next acquisition.

Why DSCR Is the Right Qualification Path for Non-Resident Investors

For most non-resident alien investors, conventional mortgage qualification simply does not fit the reality of how international buyers earn income and hold assets.

Traditional US mortgage underwriting is built around:

- US W-2 employment

- US tax returns

- Social Security numbers

- Domestic credit scores

Most foreign national investors living abroad do not have those documents available, even when they have substantial income, strong liquidity, and significant real estate experience.

That is why DSCR financing has become one of the most effective mortgage structures for non-resident investors purchasing or refinancing US rental property.

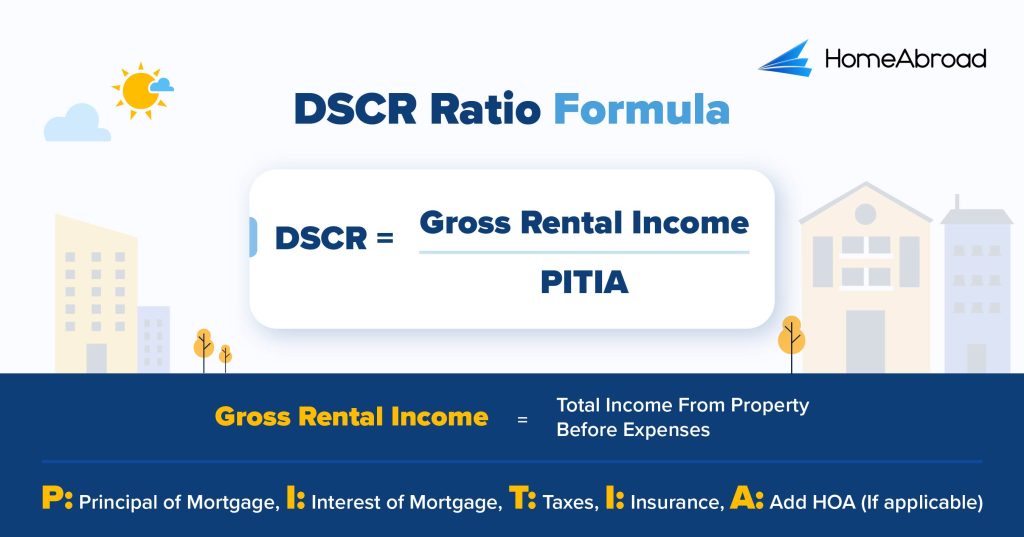

Instead of qualifying the borrower personally, HomeAbroad’s DSCR loans qualify the property based on rental cash flow.

The formula is:

PITIA includes:

- Principal

- Interest

- Property taxes

- Insurance

- HOA or association dues

That last category is where many first-time DSCR borrowers get surprised. Investors often calculate DSCR using only the mortgage payment and forget that HOA dues directly affect the ratio.

At HomeAbroad, most DSCR refinance programs require a minimum DSCR of approximately 1.0 or higher for qualification.

The distinction here matters. A DSCR of exactly 1.0 means the property is operating at break-even, the rental income covers the monthly obligations, and nothing more. The loan may still qualify, but stronger DSCR ratios, such as 1.25 or above, generally unlock better pricing, stronger leverage options, and more favorable loan structures.

The calculation of DSCR itself is also based on market rent analysis from the appraisal rather than online rent estimates or the borrower’s projected numbers.

That is an important limitation to understand upfront. If the appraisal-supported rent does not support the required DSCR threshold, the refinance may not qualify under this structure even if the borrower personally has high income or reserves.

HomeAbroad’s Cash-Out Refinance Terms for Foreign Nationals

HomeAbroad’s DSCR cash-out refinance programs are structured specifically for foreign national and non-resident alien investors holding US rental property. Qualification is based primarily on property cash flow and equity position rather than US employment history or traditional credit underwriting.

The exact loan structure depends on DSCR strength, property type, reserves, and leverage requested, but the core parameters are straightforward.

Loan-to-Value (LTV)

HomeAbroad allows up to 75% LTV on DSCR cash-out refinance loans for qualified foreign national borrowers.

Where a borrower lands within that range depends primarily on:

- DSCR ratio

- Property type

- Reserve strength

- Short-term rental exposure

- Credit profile if available

Properties with stronger cash flow and lower risk profiles generally qualify for more aggressive leverage and better pricing.

Minimum DSCR Requirement

HomeAbroad’s minimum DSCR requirement is generally 1.0 or higher.

A DSCR above 1.25 is typically preferred because it creates stronger refinance flexibility and more favorable pricing options.

The distinction matters because leverage alone does not determine the final cash-out amount. A property may appraise high enough for 75% LTV but still fail DSCR qualification if rental income does not sufficiently support the new payment.

Property Types Eligible

HomeAbroad’s foreign national DSCR refinance programs commonly allow:

- Single-family rentals (SFRs)

- 2–4 unit residential properties

- Townhomes

- Warrantable condos

- Short-term rental properties with documented rental history or market-rent support

Condo-heavy markets may face additional restrictions if the building is considered non-warrantable.

Loan Amounts and Borrower Eligibility

HomeAbroad offers DSCR cash-out refinance structures across a wide loan-size range depending on the property and borrower profile.

Eligible borrowers may include:

- Foreign nationals residing outside the United States

- Non-permanent resident visa holders

- Borrowers without US credit history

- International investors using passport-based qualification

ITINs are often not required when DSCR is the primary qualifying structure.

LLC Borrowing and Ownership Structure

Foreign national investors may also take title and financing through a US LLC in many DSCR structures.

This is often preferred because it can provide:

- Liability separation

- Cleaner property management operations

- Better portfolio structuring flexibility

- Potential estate-planning advantages when coordinated properly with tax counsel

Seasoning and Delayed Financing

Most DSCR cash-out refinance programs require a seasoning period, commonly between 3–6 months of ownership before equity can be extracted.

However, HomeAbroad’s delayed-financing structures allow many all-cash foreign national buyers to refinance much sooner without waiting through traditional seasoning timelines.

Prepayment Penalties

Most DSCR refinance loans include prepayment penalties, typically structured over 3–5 years.

This is an important tradeoff to understand upfront. DSCR loans prioritize flexibility around income documentation and international qualification, but that flexibility usually comes with yield-protection provisions for the lender.

What Foreign Investors Actually Do With the Cash

For most non-resident alien investors, a DSCR cash-out refinance is not about extracting equity for personal spending. It is usually a portfolio-growth strategy.

Based on HomeAbroad’s experience working with foreign national investors across multiple US markets, the borrowers using cash-out refinance most effectively are typically using the proceeds to recycle capital into additional income-producing assets rather than leaving equity trapped inside appreciated property.

Fund the Next Acquisition

The most common use case HomeAbroad sees is portfolio expansion.

A foreign investor purchases a US rental property, allows appreciation and principal paydown to build equity, then uses a DSCR cash-out refinance to extract capital for the down payment on the next acquisition.

Instead of selling the original property and triggering taxes, transaction costs, and potential FIRPTA withholding later, the investor keeps the asset and uses the equity to scale.

A pattern we’ve noticed with foreign investors building US portfolios is that the first successful cash-out refinance often becomes the inflection point where growth stops being linear. Once equity from existing rentals begins funding new acquisitions, portfolio expansion accelerates significantly faster.

Renovate to Increase DSCR

Some investors use refinance proceeds to improve the property itself.

Common examples include:

- Interior renovations

- Short-term rental upgrades

- Additional bedrooms or functional improvements

- Deferred maintenance correction

The goal is usually to increase rental income, which may improve the property’s DSCR over time and strengthen future refinance or acquisition opportunities.

This strategy is especially common in markets where appreciation has already occurred but rents still have room to grow through repositioning.

Recapitalize After an All-Cash Purchase

Foreign national investors frequently purchase US properties with cash because all-cash offers are often more competitive, especially in fast-moving markets.

HomeAbroad’s delayed-financing DSCR structures allow many investors to refinance shortly after closing and recover a large portion of that capital instead of leaving it tied up indefinitely inside the property.

That recovered liquidity can then be redirected into:

- Another acquisition

- Reserve strengthening

- Renovation capital

- Market diversification

Rebalance Across Multiple Markets

Some international investors also use cash-out refinance strategically across different US markets.

For example, investors holding appreciated properties in markets such as Miami or Austin may extract equity from those assets and redeploy the capital into higher-cash-flow markets where DSCR performance is stronger and acquisition pricing is lower.

This allows the portfolio to shift from appreciation-heavy positioning toward stronger income generation without liquidating core assets.

Tax and FIRPTA Implications Foreign Nationals Must Understand Before Refinancing

One of the biggest misconceptions foreign investors have about cash-out refinance is that the refinance proceeds are taxable income but they are not.

A DSCR cash-out refinance is a loan secured against the property’s equity, not income generated from selling the asset. Because the investor is borrowing against equity rather than disposing of the property, the cash received through the refinance is generally not treated as a taxable event for US income-tax purposes.

That distinction matters because it is one reason many foreign national investors prefer refinancing over selling appreciated property.

FIRPTA, short for the Foreign Investment in Real Property Tax Act, becomes relevant when a foreign owner sells US real estate, not when the property is refinanced. While FIRPTA withholding does not apply to a cash-out refinance itself, foreign investors should still understand the broader tax framework surrounding US real estate ownership because the future sale of the property may eventually trigger FIRPTA withholding obligations.

The more immediate tax consideration for many non-resident investors is rental-income treatment.

By default, foreign nationals receiving US rental income may be subject to a flat withholding structure on gross rental income. However, many investors elect to treat rental income as effectively connected income under Section 871(d).

That election allows qualifying investors to deduct:

- Mortgage interest

- Property taxes

- Depreciation

- Repairs and maintenance

- Insurance

- Property management fees

This often creates a materially lower effective tax burden and can improve actual net cash flow retained from the property after refinancing.

The distinction is important because stronger retained cash flow often improves long-term DSCR performance and portfolio scalability.

Foreign investors should also understand that refinancing does not eliminate US estate-tax exposure.

Under current US estate-tax rules, non-resident aliens generally receive only a $60,000 exemption on US-sited assets, compared to the substantially larger exemption available to US citizens. Depending on how the property is owned, estate-tax exposure may still exist even when the property is held through certain LLC structures.

More advanced ownership structures, such as foreign-corporation ownership combined with US LLC vesting, may provide mitigation opportunities, but those decisions require coordination with a US international tax attorney and estate-planning professional.

HomeAbroad handles the lending and refinance structure, but we strongly recommend that foreign national investors also consult a US-based CPA and international tax advisor before refinancing US property. The mortgage structure is only one piece of the broader investment and tax strategy.

For a full breakdown of FIRPTA withholding rules and foreign-seller obligations, link this section to HomeAbroad’s dedicated FIRPTA guide or pillar article.

The HomeAbroad Cash-Out Refinance Process

HomeAbroad’s DSCR cash-out refinance process for foreign national investors is designed to work remotely and efficiently without requiring US income documentation, US tax returns, or traditional employment verification.

The process itself is heavily property-driven. The refinance is underwritten based primarily on the property’s value, rental income, DSCR performance, and the investor’s reserve strength.

Step 1 — Pre-Qualification Review

The process starts with a pre-qualification discussion focused on the property and the investor’s refinance goals.

At this stage, HomeAbroad reviews:

- Property location and type

- Current estimated value

- Existing loan balance or equity position

- Current rental income

- Target cash-out amount

- Ownership structure (personal name or LLC)

The goal is to assess whether the requested leverage is realistic based on projected LTV and DSCR before a formal application begins.

Step 2 — Documentation Package

Once the file moves forward, HomeAbroad collects the core documentation package.

This commonly includes:

- Passport or identification documents

- Lease agreements if available

- Entity documents for LLC borrowers

- Two to three months of bank statements showing reserve funds

- Insurance and mortgage statements for the existing property

Importantly, HomeAbroad’s DSCR refinance programs generally do not require:

- US tax returns

- US employment verification

- Foreign income documentation

- W-2s or pay stubs

Qualification is based primarily on the property itself rather than the borrower’s personal income profile.

Step 3 — Appraisal Order

HomeAbroad then orders the appraisal.

The appraisal determines two critical numbers:

- Market value, which sets the maximum LTV ceiling

- Market rent, which drives the DSCR calculation

The distinction matters because the appraiser’s market-rent analysis is what underwriting uses, not necessarily the investor’s current lease agreement or projected rent assumptions.

A pattern we see often is appraised market rent coming in lower than the investor’s existing lease rate, especially in markets where rents have softened recently. That difference directly affects DSCR qualification and potential cash-out proceeds.

Step 4 — DSCR Underwriting

During underwriting, HomeAbroad calculates DSCR using the appraiser’s market rent against the projected PITIA payment on the new refinance amount.

No personal income analysis is performed under standard DSCR qualification.

Step 5 — Loan Approval and Final Terms

Once underwriting is complete, HomeAbroad issues the final loan structure, including:

- Interest rate

- Approved LTV

- Final cash-in-hand amount

- Reserve requirements

- Prepayment-penalty structure

This is also where any adjustments tied to DSCR strength or appraisal findings are finalized.

Step 6 — Closing and Funding

The refinance closing can usually be completed remotely.

HomeAbroad commonly works with:

- International wire transfers

- Remote notarization

- Power of Attorney structures when needed

For straightforward foreign national DSCR refinance files, the process timeline is often around 21–30 days from application to closing.

What Reduces Your Cash-Out Amount: Common Scenarios

One of the biggest misunderstandings foreign investors have about DSCR cash-out refinance is assuming the available equity automatically translates into cash at closing.

In reality, the final cash-out amount is constrained by both leverage limits and DSCR qualification. The property may have significant equity on paper, but the refinance still has to work within underwriting guidelines tied to appraisal value, rental income, and ownership structure.

Low Appraisal Value

The first common issue is appraisal risk.

HomeAbroad’s DSCR cash-out refinance programs generally allow up to 75% LTV, but that percentage applies to the appraised value, not the investor’s estimated value.

For example:

- Investor expects property value: $400,000

- Actual appraisal comes in at: $360,000

- 75% LTV maximum becomes: $270,000 instead of $300,000

That difference immediately reduces the maximum refinance proceeds available.

If the investor already has an existing mortgage payoff attached to the property, the actual cash received after payoff and closing costs may shrink materially.

DSCR Drops Below Qualification Threshold

The second issue is DSCR compression caused by the new refinance payment.

Here’s why that matters for the deal: DSCR is calculated against the proposed new payment, not the current one.

If the refinance significantly increases the loan balance, the new PITIA payment also rises. In some cases, the higher payment pushes the DSCR below the minimum qualifying threshold even though the property previously cash flowed comfortably.

This is where many investors miscalculate expected proceeds because they focus only on equity position and overlook how the larger payment changes the DSCR equation itself.

At HomeAbroad, a DSCR below approximately 1.0 generally will not qualify under the standard DSCR refinance structure.

Seasoning and Ownership-Structure Issues

The third category involves title and ownership complications.

Some refinance programs require a minimum seasoning period after acquisition before equity can be extracted. Others may limit eligibility if the property is currently held in:

- A foreign corporation

- A non-standard ownership structure

- An entity that does not align with DSCR program requirements

Certain programs also prefer or require vesting through a US LLC rather than direct foreign corporate ownership.

The honest answer is that the only way to know exactly how much equity can be accessed is to run the DSCR calculation against the actual appraised rent and the proposed refinance payment. HomeAbroad does this during pre-qualification so investors understand realistic leverage and cash-out expectations before the file reaches underwriting.

Foreign National Cash-Out Refinance vs. Selling the Property

For many foreign national investors, the decision eventually becomes strategic rather than operational: refinance the property and keep it, or sell the asset and redeploy the capital elsewhere.

A DSCR cash-out refinance allows the investor to access equity while continuing to own the property.

That means the investor still retains:

- The rental-income stream

- Future appreciation potential

- Existing tenants and operating history

- Long-term portfolio positioning in the market

Because the transaction is structured as debt rather than a sale, the refinance proceeds are generally not treated as taxable income.

Selling the property creates a very different outcome.

For foreign national owners, a sale may trigger FIRPTA withholding under the Foreign Investment in Real Property Tax Act. In many transactions, the buyer is required to withhold 15% of the gross sale price, not the seller’s profit, and remit it to the IRS as a tax deposit.

For example:

400,000 × 0.15 = 60,000

On a $400,000 property sale, $60,000 may be withheld at closing regardless of the seller’s actual tax liability. While some or all of that amount may eventually be recoverable through tax filing or a FIRPTA withholding certificate, the capital is still tied up during the process.

A refinance does not trigger FIRPTA withholding because ownership of the property does not change.

Selling also introduces higher transaction costs. Realtor commissions, title charges, transfer costs, and closing expenses often total around 6–8% of the sale price, while DSCR refinance closing costs are commonly closer to 2–3%.

That does not mean refinancing is always the better option.

Selling may make more sense if:

- The property no longer cash flows effectively

- The investor wants to exit a specific market

- Appreciation goals have already been achieved

- The required liquidity exceeds what responsible leverage supports

The important distinction is that refinancing preserves ownership while unlocking equity, whereas selling fully exits the position and may create immediate tax and withholding consequences. For a deeper breakdown of FIRPTA withholding rules, link this section to HomeAbroad’s dedicated FIRPTA guide or pillar article.

Case Study: How an Israeli Investor Used a DSCR Cash-Out Refinance to Scale His US Portfolio

One example from HomeAbroad’s foreign national refinance experience involved an Israeli investor who used a DSCR cash-out refinance to unlock equity from a Cleveland rental property and fund the purchase of another US investment property.

Daniel, a non-resident investor living in Israel, originally purchased the property in cash for approximately $77,800 in 2020. Over time, the property appreciated significantly while continuing to generate stable rental income. By 2024, the home appraised at $140,000, creating substantial accessible equity.

Rather than selling the property and triggering transaction costs and potential FIRPTA withholding later, Daniel chose to refinance the asset through HomeAbroad’s DSCR cash-out refinance program.

The refinance structure included:

- Appraised value: $140,000

- Loan amount: $84,000

- Interest rate: 7.75% fixed

- Cash received at closing: $79,640

- Monthly PITIA payment: $938

- Monthly rental income: $1,275

- DSCR ratio: 1.36

The DSCR calculation was:

DSCR = $1,275 / $938 = 1.36

Because the property’s rental income comfortably covered the proposed refinance payment, Daniel qualified without needing traditional US income documentation or a US credit profile.

The refinance closed in 29 days, and Daniel used the $79,640 cash-out proceeds as the down payment for another investment property, allowing him to continue expanding his US real estate portfolio without injecting additional personal capital.

This case also highlights a common pattern HomeAbroad sees among foreign national investors: once a rental property accumulates enough equity and stable cash flow, a DSCR cash-out refinance often becomes the mechanism that accelerates portfolio growth from one property into multiple acquisitions.

Refinance Your US Rental Property as a Foreign National

HomeAbroad helps foreign national and non-resident investors access equity through DSCR cash-out refinance programs designed specifically for US rental properties. Our programs are structured for borrowers living abroad and generally do not require US income verification, W-2s, or traditional US credit history.

Before committing to a refinance application, speak with a HomeAbroad loan officer to review your property’s DSCR, projected LTV, appraised-rent support, and estimated cash-out potential. Running the numbers upfront helps investors understand how much equity can realistically be accessed before underwriting begins.

Connect with HomeAbroad to evaluate your property and see how much equity you may be able to unlock through a foreign national DSCR cash-out refinance

FAQs

Do foreign nationals need a US credit score to cash-out refinance?

No. HomeAbroad’s DSCR cash-out refinance programs qualify primarily based on the property’s rental income relative to the proposed PITIA payment. Traditional US credit history is generally not required for qualification.

How much equity do I need to qualify for a cash-out refinance as a foreign national?

HomeAbroad typically requires borrowers to retain at least 25% equity after refinancing, which means most DSCR cash-out refinance programs allow up to 75% LTV. The exact cash-out amount depends on the property’s appraised value, DSCR strength, reserve profile, and loan structure.

Can I cash-out refinance a property I purchased with cash?

Yes. HomeAbroad offers delayed-financing DSCR refinance structures for foreign national investors who originally purchased the property with cash. In many cases, investors can refinance shortly after acquisition without waiting through the longer seasoning periods common in conventional lending.

Can I take the loan through my US LLC?

Yes. HomeAbroad supports entity borrowing for foreign national investors through US-based LLC structures. In most cases, the foreign national owner still provides a personal guarantee on the loan even when the property is vested in the LLC.

How long does the refinance process take?

For a standard foreign national DSCR refinance file, HomeAbroad commonly closes within approximately 21–30 days. International wire transfers and reserve-documentation preparation should begin early because those are the areas that most often create avoidable delays.

Are cash-out refinance proceeds taxable for a foreign national?

No. Cash-out refinance proceeds are loan proceeds, not earned income, and are generally not treated as taxable income for US tax purposes. FIRPTA withholding applies to property sales, not refinances.