Editorial Integrity

Making informed real estate decisions starts with having the right knowledge. At HomeAbroad, we offer US mortgage products for foreign nationals & investors and have a network of 500+ expert HomeAbroad real estate agents to provide the expertise you need. Our content is written by licensed mortgage experts and seasoned real estate agents who share insights from their experience, helping thousands like you. Our strict editorial process ensures you receive reliable and accurate information.

Quick Answer

If you’re buying a rent-ready investment property that you plan to hold for long-term rental income, a DSCR loan is typically the better choice. If you’re buying a distressed property that needs renovation before it can be rented or sold, a hard money loan is generally the better fit.

A DSCR loan provides long-term financing based on the property’s rental income, making it well suited for stabilized investment properties. A hard money loan is a short-term financing solution built for investors who need to acquire, renovate, and reposition a property before their planned exit.

The right loan depends on your investment strategy, the property’s condition, your expected holding period, and how quickly you need to close. Many experienced foreign national investors use both financing options at different stages of building a US real estate portfolio, with each loan serving a different purpose.

Table of Contents

Choose a DSCR loan for rent-ready properties you plan to hold as long-term rental investments.

Choose a hard money loan for distressed properties that require renovations before they can be rented or sold.

DSCR loans focus on long-term rental ownership, while hard money loans support short-term value-add projects.

The right financing depends on your investment strategy, property condition, timeline, and long-term goals, not just the interest rate.

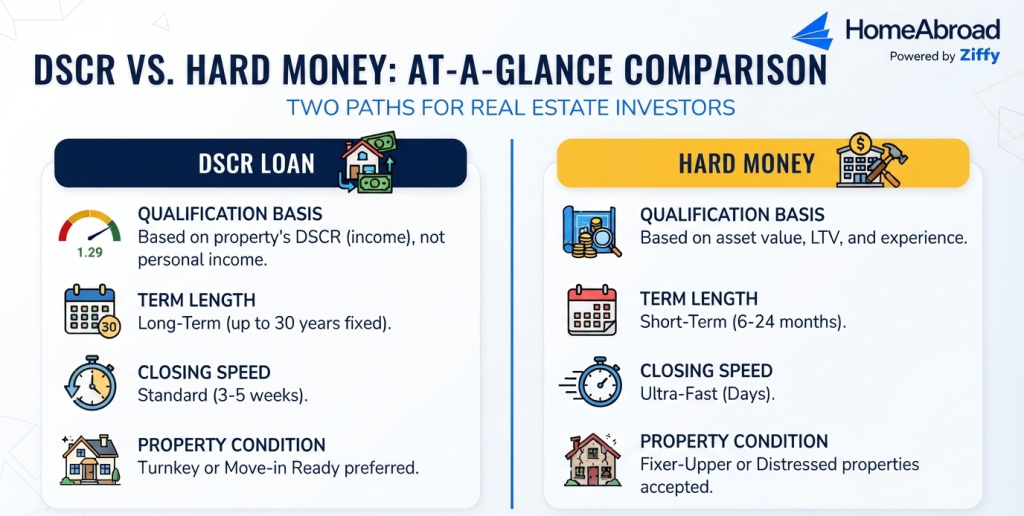

DSCR Loan vs Hard Money Loan: Side-by-Side Comparison

Feature | DSCR Loan | Hard Money Loan |

|---|---|---|

Qualification Basis | Property’s rental income (DSCR) | Property value, after-repair value (ARV), and asset strength |

US Credit Required | No US credit history required for HomeAbroad’s DSCR Loan | Not always required; varies by lender and loan program |

Typical Interest Rate | Approximately 7.00%–7.25% | Typically 9%–13%+ |

Loan Term | Up to 30 years | Typically 6–24 months |

Down Payment | Minimum 25% down for most foreign national borrowers | Varies by project, borrower, and property condition |

Closing Timeline | Typically within 30 days | Often 7–14 days |

Property Condition | Best suited for rent-ready, income-producing properties | Designed for distressed properties requiring renovation |

Prepayment Penalty | May apply depending on the loan program | Generally uncommon due to the short loan term, but varies by lender |

Best Exit Strategy | Long-term rental ownership and cash flow | Renovate and sell, or refinance into long-term financing |

Best For | Buy-and-hold investors purchasing stabilized rental properties | Fix-and-flip, BRRRR, and value-add investment strategies |

HomeAbroad’s foreign national DSCR loan rates are approximately 7.00% to 7.25% as of July 2026. Your final interest rate depends on factors such as the property’s DSCR, loan amount, loan-to-value (LTV), credit profile, and overall loan scenario.

The biggest difference between these financing options is how they fit into your investment strategy. A DSCR loan is designed for investors purchasing income-producing rental properties they intend to hold over the long term. A hard money loan is a short-term financing solution built for acquiring and renovating properties that may not yet qualify for conventional or DSCR financing.

How DSCR Loans Work for Foreign National Investors

A DSCR (Debt Service Coverage Ratio) loan is designed for investors purchasing income-producing rental properties. Instead of qualifying the borrower based on personal income, employment, or tax returns, the loan is underwritten using the property’s ability to generate enough rental income to cover its monthly housing expense.

For investors without a US Social Security Number, US credit history, or US-sourced income, this financing approach provides a practical way to purchase long-term rental property in the United States. If you’re new to this financing option, see our Foreign National DSCR Loan Guide for a complete overview.

What HomeAbroad Evaluates

Unlike a conventional mortgage, a Foreign National DSCR Loan focuses primarily on the property’s financial performance rather than the borrower’s personal income.

During underwriting, HomeAbroad reviews factors such as:

- The property’s Debt Service Coverage Ratio (DSCR) based on market rental income.

- The appraiser’s Form 1007 market rent schedule for long-term rental properties.

- The property’s location, occupancy, and overall investment profile.

- The loan amount, down payment, and available cash reserves.

- The borrower’s ownership structure, including purchases made in an individual name or through a US LLC.

Because qualification is based on the property’s income potential, borrowers generally do not need to provide US employment income, W-2s, or US tax returns to qualify for a Foreign National DSCR Loan.

Steven Glick

Director of Mortgage Sales · HomeAbroad

For many foreign investors, the biggest advantage of a DSCR loan is that the property’s rental income drives the qualification. That allows investors without US employment income or an established US credit history to finance income-producing rental properties using the property’s financial performance.

Typical Terms for Foreign National Borrowers

While every loan is individually underwritten, HomeAbroad’s Foreign National DSCR Loan Program generally includes:

- Minimum 25% down payment for most foreign national borrowers.

- At least six months of post-closing cash reserves.

- DSCR of 1.0 or higher for the most competitive terms, with No-Ratio DSCR Loans available for eligible properties with a DSCR below 1.0.

- The option to purchase personally or through a US LLC, depending on the investor’s ownership and tax strategy.

- Prepayment penalty options, which can influence the interest rate and should be evaluated based on your expected holding period.

To learn more, explore our DSCR Loan Requirements Guide before selecting a loan structure.

How Hard Money Loans Work for Foreign National Investors

Hard money loans are short-term, asset-based loans designed for properties that may not qualify for long-term financing in their current condition. They are commonly used to purchase distressed, vacant, or value-add properties that require renovations before they can generate stable rental income.

For foreign national investors pursuing a fix-and-flip or BRRRR strategy, HomeAbroad’s Fix and Flip Loan provides the speed and flexibility needed to acquire, renovate, and reposition investment properties. Once the renovations are complete and the property is rented, many investors refinance into a long-term DSCR loan to reduce financing costs and improve cash flow.

Asset-Based Lending and ARV Explained

Unlike a DSCR loan, which focuses on a property’s rental income, a hard money loan is primarily based on the property’s value and investment potential.

One of the key metrics is the After-Repair Value (ARV), which estimates what the property is expected to be worth after renovations are complete. Lenders use the current property value, renovation budget, and projected ARV to determine the loan amount and financing structure.

Because these loans are intended for short-term projects, they typically have:

- Loan terms ranging from 6 to 24 months.

- Higher interest rates than long-term DSCR loans.

- Faster approvals and funding for time-sensitive acquisitions.

- Flexible financing for properties that are not yet rent-ready.

For investors purchasing distressed properties, a hard money loan is often the most practical financing solution because traditional investment property loans generally require the property to be in rentable condition.

What Foreign Investors Should Watch For

Although hard money financing offers flexibility, it also requires careful planning.

Foreign national investors should consider:

- Cross-border wire transfer timelines, which can affect how quickly the down payment and closing funds arrive.

- Construction draw schedules, especially if renovation funds are released in stages during the project.

- Personal guarantees, which may be required depending on the lender and ownership structure.

- Balloon payments, since most hard money loans must be repaid or refinanced at the end of the loan term.

Why Not a Conventional Loan?

Conventional investment property loans are built primarily for borrowers with an established US financial profile. Most lenders require a US credit history, W-2 income, tax returns, employment verification, and debt-to-income (DTI) calculations as part of the qualification process. While some foreign nationals may meet these requirements, many international investors purchasing US rental property do not.

For most foreign national investors, the practical choice is between a DSCR loan for stabilized rental properties and a hard money loan for distressed properties that require renovation.

The most common question we receive from foreign investors is whether not having US credit means they can’t finance a property. In many cases, it simply means they need a loan program that’s built for international investors instead of a conventional mortgage.

If you’re comparing DSCR and conventional financing, see our DSCR Loan vs Conventional Loan Guide for a detailed breakdown of qualification requirements, costs, and the situations where each loan type makes the most sense

Which Financing Strategy Fits Your Investment Goal?

The right financing depends on your investment objective, the property’s condition, and your planned exit strategy. The scenarios below illustrate when a DSCR loan, a hard money loan, or a combination of both is typically the better fit.

Buying a Turnkey Rental to Hold Long Term → Choose a DSCR Loan

If you’re purchasing a rent-ready property with stable rental income and plan to hold it as a long-term investment, a DSCR loan is typically the better choice. It offers long-term financing, predictable monthly payments, and qualification based on the property’s rental income rather than your personal income.

Steven Glick

Director of Mortgage Sales · HomeAbroad

When a property is already producing reliable rental income, most investors benefit from locking in long-term financing instead of paying for short-term capital they no longer need.

Buying a Distressed Property to Flip → Choose a Hard Money Loan

Properties that require significant renovations before they can be rented or sold are generally better suited for hard money financing. These loans provide faster funding and are designed for short-term renovation projects where speed is often more important than long-term financing costs.

HomeAbroad’s Fix and Flip Loan is a financing solution designed for international real estate investors purchasing distressed properties to renovate and either sell or refinance them. If your goal is to renovate and sell the property within months, this loan is usually the more practical financing solution.

BRRRR Strategy (Buy, Renovate, Rent, Refinance) → Use Both

Many experienced foreign investors use both financing options as part of the same investment strategy.

Start with a hard money loan to acquire and renovate the property. Once the renovations are complete and the property is leased, refinance into a Foreign National DSCR Loan to secure long-term financing with lower monthly payments.

This approach allows investors to complete the renovation quickly while transitioning into financing that’s designed for long-term rental ownership. If you’re considering this approach, read our BRRRR Strategy Guide to understand each stage of the investment process and how financing fits into the strategy.

Property Rents Below Break-Even (DSCR Below 1.0) → Consider a No-Ratio DSCR Loan

A property doesn’t automatically become ineligible because its projected DSCR is below 1.0.

HomeAbroad offers No-Ratio DSCR Loans for eligible foreign national investors purchasing properties that don’t fully cover the monthly housing expense through rental income. These programs typically require a higher down payment, making them a potential option for investors purchasing appreciation-focused properties or assets undergoing rental stabilization.

Need to Close in Under Two Weeks → Hard Money or a Bridge Loan

Some investment opportunities require a fast closing timeline that traditional long-term financing may not accommodate.

If you’re competing for a discounted property, purchasing from an auction, or working with a seller who requires a quick close, a hard money loan or bridge loan can provide the speed needed to secure the property. Once the property is stabilized, many investors refinance into a long-term DSCR loan.

One of our international clients needed to close quickly on a value-add property that wouldn’t qualify for long-term financing in its current condition. We structured short-term financing so the purchase could move forward, and after the renovations were complete and the property was leased, the investor refinanced into a DSCR loan for long-term ownership. Planning the exit strategy before closing made the transition much smoother.

Preparing for a Successful DSCR Refinance

Many foreign national investors refinance into a Foreign National DSCR Loan after completing a value-add project. The transition is often smoother when the refinance is planned before the renovation is finished rather than after the property is ready for long-term financing.

Before applying, review any seasoning requirements, existing prepayment penalties, and your expected rental income. Understanding these factors early can help you determine the right time to refinance and avoid unnecessary financing costs. If your current loan includes a prepayment penalty, compare the savings from refinancing with the cost of paying off the existing loan before making a decision.

Investors who prepare for a refinance from the beginning usually experience a smoother underwriting process. Keep renovation invoices, lease agreements, proof of completed work, and entity documents organized so they’re available when the property is ready for long-term financing.

Example Refinance Timeline

Stage | Typical Milestone |

|---|---|

Property Purchased | Acquired using short-term financing from another lender |

Renovation Completed | Property is ready for tenants |

Property Stabilized | Lease signed and rental income established |

DSCR Refinance | HomeAbroad evaluates the property’s rental income for long-term financing |

A well-planned refinance can reduce financing costs, provide a longer repayment term, and create more predictable monthly cash flow for long-term rental ownership.

Real Client Success Story: Canadian Investor Closes a $1.86M Foreign National DSCR Loan in 25 Days

This completed HomeAbroad transaction shows how a foreign national investor financed a high-value US rental property using a Foreign National DSCR Loan. Instead of qualifying through conventional US income documentation, the loan was underwritten based on the property’s rental income, allowing the borrower to close nearly three weeks ahead of schedule.

Deal Snapshot

Property Details | Loan Details |

|---|---|

Location: Plantation, Florida | Loan Program: Foreign National DSCR Loan |

Property Type: Single-Family Rental | Loan Amount: $1,858,500 |

Purchase Price: $2,655,000 | Interest Rate: 6.875% |

Monthly Market Rent: $16,000 | Underwritten DSCR: 1.02 |

Ownership Structure: US LLC | Closing Time: 25 Days |

The borrower, a Canadian foreign national, purchased the property through a US LLC as a long-term rental investment. Because the property generated sufficient rental income, HomeAbroad structured the financing as a Foreign National DSCR Loan, allowing the borrower to qualify based on the property’s income instead of US employment income, W-2s, or tax returns.

With an underwritten DSCR of 1.02, the property supported the requested financing, resulting in a $1.858 million DSCR purchase loan. The transaction closed in 25 days, nearly three weeks ahead of the contractual closing deadline.

This transaction demonstrates how HomeAbroad helps foreign national investors finance income-producing rental properties through a rental-income-based underwriting approach, even when purchasing through a US LLC.

Which Loan Fits Your Investment Strategy? A Quick Decision Framework

Before choosing between a DSCR loan and a hard money loan, ask yourself these three questions:

1. How long do you plan to own the property?

- Long-term rental investment: A DSCR loan is generally the better option because it offers long-term financing based on the property’s rental income.

- Short-term renovation or flip: A hard money loan is often better suited for projects with a shorter holding period.

2. Is the property already producing rental income?

- Yes: A DSCR loan is designed for rent-ready, income-producing properties.

- No: If the property requires renovations before it can be leased, short-term financing may be the better starting point until the property is stabilized.

3. How quickly do you need to close?

- Standard closing timeline: A DSCR loan is usually the right choice for stabilized rental properties.

- Time-sensitive acquisition: A hard money loan or bridge loan may be more appropriate when speed is the priority.

If you’re purchasing a rent-ready investment property, you can also use HomeAbroad’s AI-native investment property search platform to compare listings based on projected rental income, cash flow, ROI, and financing opportunities before submitting an offer.

Ready to Finance Your Next Investment Property?

Choosing the right loan is only part of building a successful US real estate portfolio. HomeAbroad helps foreign national investors finance rental properties with mortgage solutions designed specifically for cross-border buyers.

Our team helps investors understand which financing option best fits their investment strategy, evaluate loan eligibility before making an offer, and complete the financing process from pre-qualification through closing.

In addition to financing, HomeAbroad provides an AI-native investment property search platform that helps investors identify rental properties based on projected rental income, cash flow, ROI, and market data. This allows you to evaluate both the property and the financing strategy before committing to a purchase.

Our mortgage specialists can help you identify the financing solution that best aligns with your investment goals, from financing a stabilized rental purchase to refinancing into a long-term DSCR loan after a value-add project.

Connect with a HomeAbroad loan specialist, Get pre-qualified today!

Frequently Asked Questions

Is a DSCR loan the same as a hard money loan?

No. A DSCR loan is designed for long-term financing of income-producing rental properties, while a hard money loan is a short-term financing solution commonly used for distressed properties, renovations, or fix-and-flip projects.

Can foreign nationals get hard money loans without US credit?

Some hard money lenders work with foreign national borrowers and may not require a US credit history. Qualification requirements vary by lender, loan program, and investment strategy.

Can I refinance a hard money loan into a DSCR loan?

Yes. Once a property has been renovated, leased, and meets the lender’s DSCR requirements, many foreign investors refinance into a long-term DSCR loan to reduce financing costs and improve cash flow.

Which loan costs less over the long term?

A DSCR loan generally has a lower interest rate and longer repayment term, making it more cost-effective for long-term rental ownership. Hard money loans are designed for short-term use and typically carry higher financing costs.

Which loan is better for foreign national investors?

It depends on your investment strategy. A DSCR loan is typically the better choice for purchasing and holding income-producing rental properties, while a hard money loan is better suited for acquiring and renovating distressed properties before selling or refinancing.