Editorial Integrity

Making informed real estate decisions starts with having the right knowledge. At HomeAbroad, we offer US mortgage products for foreign nationals & investors and have a network of 500+ expert HomeAbroad real estate agents to provide the expertise you need. Our content is written by licensed mortgage experts and seasoned real estate agents who share insights from their experience, helping thousands like you. Our strict editorial process ensures you receive reliable and accurate information.

Depreciation recapture is a separate tax calculation that applies when you sell a US rental property you’ve depreciated, and it applies to foreign nationals the same way it applies to US taxpayers.

The portion of your gain tied to straight-line depreciation is generally capped at a 25% federal rate. This is different from, and in addition to, ordinary capital gains tax.

FIRPTA (Foreign Investment in Real Property Tax Act) withholding at closing is a deposit against your total tax bill, not the bill itself. Recapture and capital gains tax are calculated separately on your nonresident tax return.

Nonresident aliens are generally not subject to the 3.8% Net Investment Income Tax that often applies to this type of gain for US taxpayers.

Cost segregation and bonus depreciation can shrink your tax bill during ownership, but the components they accelerate often come back at higher rates when you sell.

Table of Contents

What Depreciation Recapture Actually Means

If you’ve depreciated a US rental property, the IRS expects some of that benefit back when you sell. That’s depreciation recapture: the portion of your sale gain that’s tied to depreciation you claimed, or were entitled to claim, during ownership.

For most foreign national investors, this shows up as what the IRS calls unrecaptured Section 1250 gain. It’s taxed at a maximum federal rate of 25%, separately from the rest of your gain, which is generally taxed at standard long-term capital gains rates of 0%, 15%, or 20%.

This rule applies to foreign nationals exactly as it applies to US citizens. Your citizenship, visa status, or country of residence doesn’t change the recapture calculation itself. What changes is how the rest of your US tax picture interacts with it, particularly FIRPTA (Foreign Investment in Real Property Tax Act) withholding and the Net Investment Income Tax, both covered below.

Who This Affects

This applies to any foreign national, nonresident alien, or foreign-owned entity that has depreciated a US rental property, regardless of whether you made the Section 871(d) election to be taxed on net rental income.

Here’s the detail that catches investors off guard: the IRS calculates recapture based on depreciation that was “allowed or allowable,” not just depreciation you actually claimed on a return. If you were eligible to depreciate the property and didn’t, the IRS still treats you as if you had when you sell. Skipping the deduction during ownership doesn’t avoid recapture. It just means you paid more tax along the way for no benefit.

If you’re still deciding whether the 871(d) election makes sense for your rental income, it’s worth understanding upfront that the depreciation deductions it unlocks come with this future recapture obligation attached. Our guide to rental property depreciation for foreign nationals covers how depreciation works during ownership; this article picks up where that one leaves off, at the point of sale.

How Section 1250 Recapture Works

Section 1245 Vs. Section 1250: Why The Distinction Matters

The tax code splits depreciable property into two categories that are taxed very differently when recaptured.

Section 1245 covers personal property, things like appliances, furniture, and certain equipment. When these are sold, all depreciation taken on them is recaptured as ordinary income, up to your top marginal rate.

Section 1250 covers real property, meaning the building itself and its structural components. Residential rental buildings placed in service after 1986 are required to use straight-line depreciation, so there’s typically no depreciation recapture at ordinary rates under Section 1250 in the traditional sense. Instead, the gain tied to that straight-line depreciation becomes what the IRS calls unrecaptured Section 1250 gain, and it gets a lower cap.

Section 1245 Property | Unrecaptured Section 1250 Gain | |

|---|---|---|

What it covers | Personal property, equipment, appliances, and certain reclassified building components | The building itself, depreciated straight-line |

Maximum federal rate | Ordinary income rates, up to 37% | 25% |

Where it commonly shows up | Cost segregation studies, accelerated depreciation | Standard 27.5-year residential or 39-year commercial depreciation |

Unrecaptured Section 1250 Gain: The 25% Cap

Here’s the mechanic in plain terms. When you sell, your total gain is the difference between your sale price and your adjusted basis. Depreciation lowers your basis every year you claim it, which means it raises your taxable gain when you sell.

The portion of that gain equal to your accumulated straight-line depreciation is unrecaptured Section 1250 gain, and it’s taxed at a maximum rate of 25% rather than the standard long-term capital gains brackets.

The recapture rate isn’t a flat 25% for everyone. It’s a ceiling. If your ordinary income tax rate is lower than 25%, you pay your lower rate on this portion instead. For most investors with meaningful accumulated depreciation on a property held for several years, though, 25% is the number to plan around.

What Falls Outside The 25% Cap

If you used a cost segregation study or bonus depreciation to accelerate deductions on components of the property, that changes the picture. Those components are typically reclassified as Section 1245 property, and depreciation taken on them is recaptured at ordinary income rates rather than the 25% cap. We’ll come back to this trade-off in more detail below.

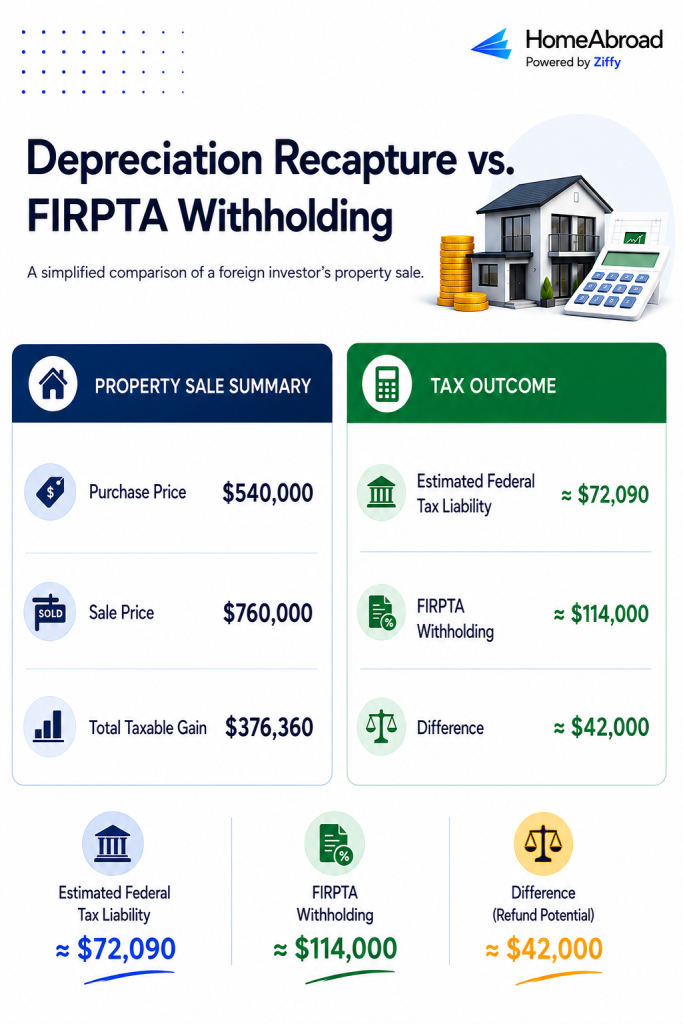

A Simplified Client Scenario

One of our foreign national clients purchased a US rental property for $540,000. After allocating $430,000 to the building and $110,000 to the land, the depreciable portion of the property generated approximately $15,636 in annual straight-line depreciation.

After owning the property for 10 years, accumulated depreciation totaled approximately $156,360, reducing the property’s adjusted basis to about $383,640.

When the investor decided to sell the property for $760,000, the total taxable gain was approximately $376,360. Of that amount, $156,360 represented accumulated depreciation and was treated as unrecaptured Section 1250 gain. At the maximum federal recapture rate of 25%, that portion of the tax was approximately $39,090.

The remaining $220,000 of gain was taxed separately under the long-term capital gains rules. At an illustrative 15% rate, the capital gains tax would be approximately $33,000.

In this scenario, the investor’s combined federal tax liability was roughly $72,090. Because the investor was a nonresident alien who hadn’t elected to file jointly with a US spouse, the 3.8% Net Investment Income Tax generally didn’t apply.

Now compare that with FIRPTA withholding. Since this was an investment property, the buyer withheld 15% of the $760,000 sale price, approximately $114,000, at closing.

Even though the investor’s estimated federal tax liability was about $72,090, $114,000 was withheld, leaving a difference of nearly $42,000. That’s why understanding both depreciation recapture and FIRPTA withholding before listing a property is so important.

The amount withheld at closing and the tax ultimately owed are often very different, and planning ahead can help investors determine whether requesting a withholding certificate makes sense for their transaction.

How Recapture Interacts With FIRPTA Withholding

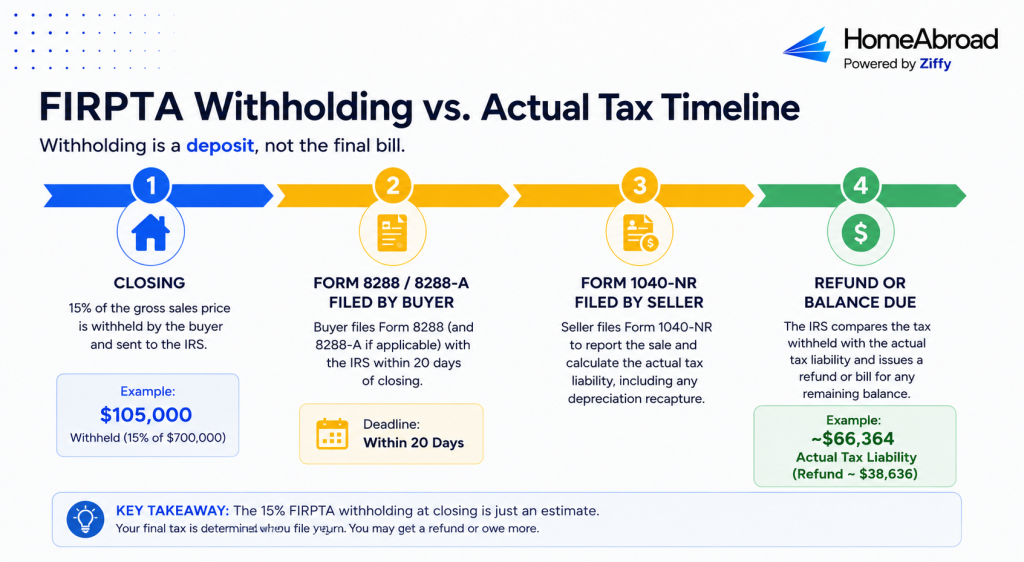

Withholding Is A Deposit, Not The Final Bill

The Foreign Investment in Real Property Tax Act requires the buyer, not the seller, to withhold a percentage of the gross sale price and send it to the IRS at closing. Depending on the sale price and how the buyer intends to use the property, that rate is generally 0%, 10%, or 15% of the amount realized.

FIRPTA withholding is calculated on the gross sale price. Your actual tax, including depreciation recapture and capital gains tax, is calculated on your net gain and reported on Form 1040-NR after the sale. As the worked example above shows, these two numbers are often very different. Many foreign sellers end up receiving a refund of some of the amount withheld once their actual return is processed.

Using Form 8288-B To Align Withholding With Actual Liability

If you expect your actual tax liability to be meaningfully lower than the default withholding amount, which is common for long-held properties with significant depreciation and a moderate gain, you can apply for a withholding certificate using Form 8288-B before closing.

This doesn’t eliminate withholding, but it can reduce the amount held back or change the timeline for when the buyer has to remit it, which matters if you’re relying on sale proceeds to fund a purchase elsewhere.

Why Tax Treaties Generally Don’t Change This

It’s a common assumption that a tax treaty between the US and an investor’s home country will reduce FIRPTA withholding. For individual nonresident alien sellers, that generally isn’t the case. FIRPTA withholding is a collection mechanism tied to the sale of US real property, and it operates independently of most income tax treaty provisions.

If you believe a specific treaty provision applies to your situation, that’s a question for a qualified US tax professional who can review the treaty language directly, not an assumption to build a sale timeline around.

The Rule That Works In A Foreign Investor’s Favor: The Net Investment Income Tax

Most US-focused guides to depreciation recapture mention a second layer of tax: the 3.8% Net Investment Income Tax, which applies to rental income and capital gains for higher-income US taxpayers. If you’re a nonresident alien, this generally doesn’t apply to you.

The IRS instructions for Form 8960, which governs the Net Investment Income Tax, state directly that the tax doesn’t apply to nonresident alien individuals. The main exception is a nonresident alien who elects to be treated as a US resident in order to file a joint return with a US citizen or resident spouse.

This isn’t a reason to treat your total tax exposure as low. Depreciation recapture and capital gains tax still apply in full. But if you’ve seen a domestic investor guide stack a 25% recapture rate with an additional 3.8% NIIT charge, know that math generally doesn’t carry over to your situation as a nonresident alien seller.

Cost Segregation And Bonus Depreciation: Bigger Deductions Now, A Different Bill Later

Cost segregation studies and bonus depreciation are popular strategies for foreign investors because they accelerate deductions into the early years of ownership. Under the One Big Beautiful Bill Act, 100% bonus depreciation is now permanent for qualifying property, provided the property is both acquired and placed in service after January 19, 2025.

The IRS issued Notice 2026-11 in January 2026 to provide interim guidance on how these rules apply, including how acquisition dates and placed-in-service dates are determined for purchased and self-constructed property.

The trade-off worth planning for now, not at closing, is how those accelerated deductions get taxed when you sell. Components identified through a cost segregation study, things like flooring, certain fixtures, and specific building systems, are often reclassified as Section 1245 property. When you sell, depreciation taken on those components is generally recaptured at ordinary income rates, up to 37% federal, rather than the 25% cap that applies to straight-line building depreciation.

This doesn’t make cost segregation a bad strategy. The time value of accelerated deductions is real, and many investors come out ahead even after accounting for the higher recapture rate on those specific components.

The mistake is authorizing a cost segregation study without modeling the exit. An investor who sees only the year-one deduction and not the eventual recapture rate can be caught off guard by the final number on a return years later.

Ways Foreign Investors Manage Recapture Timing

1031 Exchanges

A 1031 exchange lets you defer capital gains tax, including depreciation recapture, by rolling proceeds into a replacement property rather than recognizing the gain immediately. The recapture liability isn’t eliminated. It carries forward into the replacement property’s basis and will need to be addressed eventually, whether through a future taxable sale or a strategy like holding until death.

One detail foreign investors sometimes miss: FIRPTA withholding still applies to the sale of the relinquished property even inside a 1031 exchange. To avoid having a large portion of your exchange proceeds tied up in withholding, you generally need to apply for a withholding certificate before the transaction closes, which requires coordination between your qualified intermediary, your tax professional, and your closing timeline.

Installment Sales

Selling on an installment basis can spread the taxable gain across the years you receive payments. Unrecaptured Section 1250 gain has its own reporting order within an installment sale: it’s generally required to be reported before the remaining capital gain in each year you receive proceeds.

In practice, this means an installment sale changes the timing of your capital gains tax more than it changes your recapture exposure, which tends to come due earlier in the payment schedule than investors expect.

Holding Until Death

Property that passes to heirs generally receives a step-up in basis to fair market value at the date of death, which eliminates the depreciation recapture and capital gains exposure that had built up during ownership. For nonresident aliens, the federal estate tax exemption for US-situs assets is generally $60,000, which is significantly lower than the exemption available to US citizens and residents.

Holding a highly appreciated property until death can trade a recapture and capital gains problem for a larger estate tax problem, depending on the value of the property and the investor’s broader estate. This is a conversation for a cross-border estate planning professional well before it becomes relevant, not a default assumption.

When a sale or refinance is part of a larger investment strategy, liquidity becomes just as important as equity. Understanding how much of your proceeds may be tied up in FIRPTA withholding or taxes helps you plan reserves, financing, and the timing of your next investment with fewer surprises.

How This Should Factor Into Your Exit And Financing Strategy

Knowing your approximate recapture and capital gains exposure before you sell changes how you plan the transaction, not just how you file afterward.

If a large share of your expected proceeds will go toward FIRPTA withholding and taxes, that affects how much cash you’ll actually have available for a down payment on a replacement property, for reserves, or for a 1031 exchange timeline. Investors who model this in advance tend to have more flexibility at closing than investors who discover the gap between gross proceeds and net proceeds for the first time when the withholding is taken out.

Steven Glick

Director of Mortgage Sales · HomeAbroad

One conversation I encourage investors to have before listing a property is how much cash they’ll actually have available after FIRPTA withholding and taxes. That number often looks very different from the sale price, and understanding it early makes it easier to decide whether selling, refinancing, or delaying the transaction is the better financial move.

This is also where financing strategy and tax strategy meet. Some investors decide that refinancing to pull out equity makes more sense than selling outright, particularly when a sale would trigger a large combined tax bill relative to the investor’s plans for the proceeds.

HomeAbroad’s DSCR (Debt Service Coverage Ratio) loan program allows foreign national investors to qualify using a property’s rental income rather than personal income documentation, which can support a cash-out refinance as an alternative to a taxable sale.

For investors who do move forward with a sale and plan to complete a 1031 exchange, timing is often the hardest part, especially when a portion of the proceeds is tied up in FIRPTA withholding while a withholding certificate is pending. HomeAbroad’s bridge financing can help close on a replacement property within the exchange window without waiting on withholding to clear first.

I’ve worked with investors who had identified their replacement property but couldn’t access all of their sale proceeds because FIRPTA withholding was still pending. In situations like that, bridge financing can provide the liquidity needed to stay on schedule for the 1031 exchange while the tax process continues separately.

State-Level Considerations

State tax treatment of depreciation recapture and capital gains varies, and not every state follows federal rules the same way. Some states have no personal income tax and don’t tax this gain separately at all, while others tax it as ordinary state income with no special recapture rate.

Because this varies by state and can change, confirm the current treatment for the state where your property is located with a tax professional rather than assuming your home country’s tax treaty or a federal rule applies at the state level too.

Questions To Bring To A Qualified US Tax Professional

- What portion of my gain will be unrecaptured Section 1250 gain, and what portion, if any, is ordinary Section 1245 recapture from a prior cost segregation study or bonus depreciation?

- Based on my adjusted basis and expected sale price, does my default FIRPTA withholding amount look significantly higher than my actual expected liability, and does it make sense to file Form 8288-B before closing?

- If I’m planning a 1031 exchange, what’s the realistic timeline for getting a withholding certificate approved relative to my 45-day identification and 180-day closing deadlines?

- Does my home country have an estate tax treaty with the US, and how does that interact with the nonresident alien estate tax exemption if I hold this property long-term?

- If I’ve made the Section 871(d) election, how does that affect my basis and my recapture calculation compared to not having made it?

How HomeAbroad Supports Foreign Investors Through The Exit

HomeAbroad works with foreign national and international investors at every stage of US real estate ownership, not just at purchase. When a sale, refinance, or 1031 exchange is on the horizon, HomeAbroad’s DSCR loan and Full Documentation Loan programs give investors financing options built around how foreign national income and assets actually work, and bridge financing is available for investors who need to move quickly on a replacement property.

None of this replaces a conversation with a qualified US tax professional about your specific recapture exposure. It does mean that once you understand what a sale will cost you, HomeAbroad can help you plan the financing side of what comes next.

Explore HomeAbroad’s DSCR loan program or Full Documentation Loan to see how financing can fit into your exit strategy.

Frequently Asked Questions

Does depreciation recapture apply if I never actually claimed depreciation on my returns?

Generally, yes. The IRS calculates recapture based on depreciation that was allowed or allowable, meaning depreciation you were eligible to claim, whether or not you actually claimed it. Not claiming depreciation during ownership doesn’t avoid recapture at sale.

Is depreciation recapture tax the same as FIRPTA withholding?

No. FIRPTA withholding is a percentage of your gross sale price withheld by the buyer at closing as a deposit toward your eventual tax bill. Depreciation recapture is part of the actual tax calculation, done separately on your net gain when you file Form 1040-NR.

Do US tax treaties reduce depreciation recapture tax for foreign sellers?

Tax treaties can affect certain types of US-source income, but they generally don’t reduce FIRPTA withholding for individual nonresident alien sellers, and they don’t eliminate the recapture tax itself. Treaty questions specific to your country should be reviewed directly with a qualified US tax professional.

Are foreign nationals subject to the 3.8% Net Investment Income Tax on depreciation recapture gains?

Generally, no. Nonresident aliens are typically exempt from the Net Investment Income Tax, with a narrow exception for those who elect to be treated as a US resident to file jointly with a US citizen or resident spouse.