Editorial Integrity

Making informed real estate decisions starts with having the right knowledge. At HomeAbroad, we offer US mortgage products for foreign nationals & investors and have a network of 500+ expert HomeAbroad real estate agents to provide the expertise you need. Our content is written by licensed mortgage experts and seasoned real estate agents who share insights from their experience, helping thousands like you. Our strict editorial process ensures you receive reliable and accurate information.

Quick Answer: A foreign national who owns US rental property can claim depreciation as a tax deduction, just like a US investor. Depreciation allows you to deduct a portion of the building's value each year, reducing taxable rental income. Residential rental property is typically depreciated over 27.5 years, while commercial property is depreciated over 39 years. Investors can also accelerate deductions through cost segregation and 100% bonus depreciation, which the 2025 One Big Beautiful Bill Act (OBBB) made permanent for qualifying assets acquired and placed in service after January 19, 2025. Depreciation only provides a tax benefit after making a Section 871(d) election, which allows rental income to be taxed on a net basis rather than gross rent. Even then, passive-loss rules can limit how quickly some investors benefit from accelerated deductions.

Foreign nationals can claim depreciation on US rental property, spreading the building’s value over 27.5 years for residential property or 39 years for commercial property.

Depreciation only provides a tax benefit after making the Section 871(d) election, which allows rental income to be taxed on a net basis instead of gross rent.

Cost segregation and 100% bonus depreciation can accelerate deductions, but the benefit may be limited if you don’t have enough US income to use the losses.

Depreciation can reduce taxes during ownership, but it also lowers your property’s tax basis, which may affect taxes when you sell.

Table of Contents

Rental property depreciation can reduce taxable rental income without requiring additional out-of-pocket spending, making it one of the most commonly used tax deductions available to real estate investors.

For residential rental property, the building’s value is typically depreciated over 27.5 years, while commercial property is depreciated over 39 years. Investors may also accelerate deductions through strategies such as cost segregation and bonus depreciation.

However, depreciation only provides a meaningful tax benefit when rental income is taxed on a net basis. Foreign investors who have not made a Section 871(d) election are generally taxed on gross rental income, which limits the value of deductions such as depreciation.

The bigger question isn’t whether depreciation exists. It’s how much of the deduction you can actually use, when accelerated depreciation makes sense, and what trade-offs appear when the property is eventually sold.

How Depreciation Works on a US Rental Property and Why Foreign Nationals Can Use It

Foreign nationals who own US rental property can generally claim depreciation using the same IRS rules that apply to US investors. In simple terms, depreciation allows you to deduct a portion of a property’s building value each year to account for wear and tear over time, even though you haven’t actually spent that money during the year.

The first step is determining the property’s depreciable basis. When you purchase a rental property, the purchase price must typically be divided between the land and the building. Only the building portion is eligible for depreciation.

For example, if a rental property is purchased for $500,000 and $100,000 is allocated to the land, the remaining $400,000 building value becomes the basis used for depreciation calculations.

Residential rental property is depreciated over 27.5 years, while commercial property is depreciated over 39 years, as outlined in IRS Publication 527 and IRC Section 168. The IRS requires these deductions to be spread across the applicable recovery period rather than claimed all at once.

Many foreign investors assume they cannot claim depreciation because they are not US citizens or permanent residents. In reality, depreciation is based on the property’s location and use, not the owner’s citizenship. If the property is a qualifying US rental property and the investor is reporting rental income on a net basis, depreciation is generally available regardless of where the owner lives.

At HomeAbroad, we’ve helped investors from more than 40 countries purchase and finance US investment properties. While financing structures, documentation requirements, and tax situations vary from one investor to another, depreciation is often an important factor when evaluating a property’s long-term after-tax performance and overall return on investment.

The US-Situs Advantage Most Foreign Investors Miss

One of the most common misconceptions about rental property depreciation is that foreign investors are subject to less favorable depreciation rules than US investors. In many cases, that confusion comes from articles discussing a completely different situation.

Consider these two scenarios:

- A Canadian investor owns a rental property in Florida.

- A US citizen owns a rental property in Portugal.

The first property is located in the United States, while the second is located outside the United States. Even though the first owner is a foreign national, the Florida property generally follows the standard US depreciation rules available to domestic investors. The Portugal property follows a different set of rules because the property itself is located outside the United States.

This distinction is important because many online articles discussing slower depreciation schedules and restrictions on bonus depreciation are addressing foreign-located property, not US rental property owned by foreign nationals.

For foreign investors purchasing US real estate, the property’s location is what matters. A qualifying US rental property generally follows the same depreciation framework available to domestic investors.

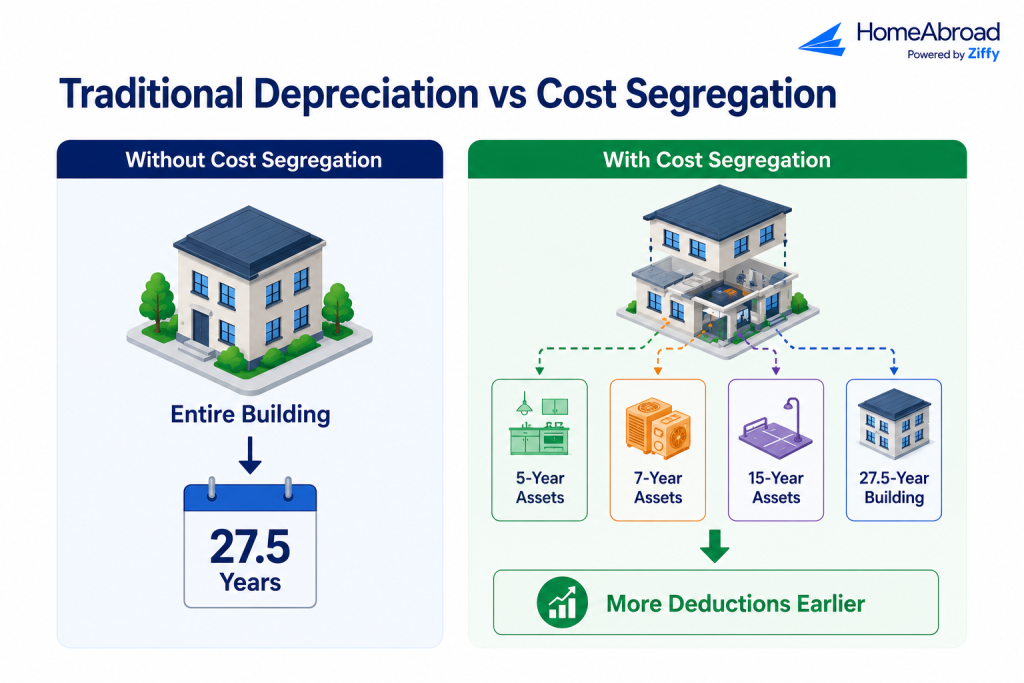

What Is Cost Segregation, and Is It Worth It for Your Rental?

A cost segregation study is a tax strategy that allows certain parts of a rental property to be depreciated faster than the building itself. Instead of depreciating the entire property over 27.5 years for residential real estate or 39 years for commercial real estate, a cost segregation study identifies components that may qualify for shorter depreciation periods.

These components are typically reclassified into 5-year, 7-year, or 15-year asset categories. Examples may include carpeting, appliances, lighting, cabinetry, parking areas, landscaping, and certain site improvements. Because these assets have shorter recovery periods, investors can claim larger depreciation deductions during the early years of ownership rather than spreading those deductions over several decades.

The primary advantage of cost segregation is timing. The total depreciation available over the life of the property does not necessarily change, but a larger portion of the deduction is moved into the first few years. For investors with sufficient taxable income, that can improve cash flow and reduce current tax liability.

The cost of a professional cost segregation study varies based on the property’s size, complexity, and location. Investors should obtain quotes from qualified cost segregation providers before proceeding.

Steven Glick

Director of Mortgage Sales · HomeAbroad

Investors who plan to hold a property for several years often ask about cost segregation when evaluating overall returns. The conversation usually comes up on larger investment properties where improving early cash flow can have a meaningful impact on long-term portfolio growth.

Cost segregation is not always the right choice for every property. It often makes the most sense for higher-value single-family rentals, multifamily properties, short-term rentals, and commercial real estate where the accelerated deductions can be significant. Smaller properties with limited depreciation potential may not generate enough additional tax savings to justify the cost of a study.

Cost segregation is often most valuable when the potential tax savings significantly exceed the cost of the study. Before moving forward, foreign investors should work with qualified tax professionals to estimate the likely benefit based on the property’s characteristics and their expected use of the resulting deductions.

Bonus Depreciation in 2026 After the OBBB

Bonus depreciation allows investors to deduct the full cost of qualifying assets in the year they are placed in service rather than depreciating them over several years. The One Big Beautiful Bill Act (OBBB), signed in July 2025, made 100% bonus depreciation permanent for qualifying property that is both acquired and placed in service after January 19, 2025.

Property acquired on or before that date but placed in service later generally does not qualify for the full 100% deduction and instead follows the applicable transition rules. The IRS addressed these provisions in IRS Notice 2026-11. Investors should consult a qualified tax professional to confirm eligibility and effective dates.

For rental property owners, bonus depreciation becomes particularly valuable when combined with a cost segregation study. Cost segregation identifies building components that can be classified into shorter recovery periods, such as 5-year, 7-year, or 15-year assets. Many of those assets may qualify for bonus depreciation.

Without cost segregation, most residential rental property is depreciated gradually over 27.5 years. With cost segregation and bonus depreciation, qualifying components may generate substantially larger deductions during the first year of ownership.

The potential benefit can be substantial, but timing matters. Bonus depreciation accelerates deductions into the current year rather than creating new deductions. Investors should therefore evaluate whether they have sufficient taxable income to make effective use of those accelerated write-offs.

The Catch: Can You Actually Use the Deduction?

Many articles about cost segregation and bonus depreciation focus on how much depreciation can be created. What they often don’t explain is whether an investor can actually use those deductions right away.

Rental real estate is generally considered a passive activity for tax purposes. Under the passive activity loss rules, depreciation deductions and rental losses may not always offset other types of income. If a foreign national’s only US income comes from a single rental property, a large depreciation deduction created through cost segregation may not deliver an immediate tax benefit.

For example, a cost segregation provider may highlight a large first-year deduction and show how an investor could generate substantial paper losses through accelerated depreciation. While the deduction itself may be legitimate, the investor may not be able to use the entire loss in the current year if there is insufficient passive income to absorb it.

In those situations, the unused losses are typically suspended and carried forward to future tax years. They are not necessarily lost, but the tax benefit may be delayed.

This is where the economics can differ from the marketing. A foreign investor with a single US rental property and no other passive US income may generate significant depreciation deductions through cost segregation but have limited ability to use those losses immediately.

By contrast, an investor with multiple rental properties or other passive income sources may be able to apply those deductions more quickly. In both cases, the depreciation is still valuable, but the timing of the tax benefit can look very different.

As a result, an investor with a single rental property may see a much smaller near-term benefit than the headline deduction figures often highlighted in cost segregation marketing.

That doesn’t mean cost segregation or bonus depreciation are bad strategies. It simply means they should be evaluated in the context of your overall tax situation rather than in isolation.

Before paying for a cost segregation study, discuss your income profile, expected holding period, and long-term investment plans with a qualified tax professional. In many cases, the value of the strategy depends not only on how much depreciation is created, but also on when the tax benefit can actually be realized.

If you’re planning to reinvest into another property, our 1031 Exchange guide explains how certain taxes may be deferred.

What Depreciation Costs You at Sale

While depreciation can reduce taxable rental income during ownership, it also reduces your property’s tax basis. When you sell, the IRS generally requires previously claimed depreciation to be accounted for through depreciation recapture, which may be taxed as unrecaptured Section 1250 gain at rates of up to 25%.

Foreign investors should also remember that FIRPTA (Foreign Investment in Real Property Tax Act) withholding may apply to the sale of US real estate. Another commonly overlooked rule is that recapture is based on depreciation that was allowed or allowable, meaning the IRS may still require recapture even if eligible depreciation deductions were never claimed.

Because depreciation recapture and sale-side tax planning deserve a separate discussion, see our guide to Capital Gains Tax for Foreign Investors.

Next Steps for Foreign Investors

Depreciation can play an important role in the economics of a US rental property, but the right approach depends on how the property is owned, how rental income is reported, and how long the investment is expected to be held. Before making decisions about cost segregation, bonus depreciation, or sale planning, consult a qualified CPA, tax advisor, or tax attorney who understands cross-border real estate taxation.

If you’re planning your next US investment property purchase, financing should be part of the conversation as well. HomeAbroad offers mortgage solutions tailored for foreign nationals that can help investors qualify based on a property’s rental income rather than US employment history or traditional credit requirements.

Ready to invest in your next US rental property? Get pre-qualified with HomeAbroad and explore financing options designed for foreign national investors.

Frequently Asked Questions

How many years do you depreciate a US rental property?

Residential rental property is generally depreciated over 27.5 years, while commercial rental property is typically depreciated over 39 years. The deduction is spread over the property’s useful life rather than claimed all at once.

Can a foreign national claim depreciation on US rental property?

Yes. Foreign nationals who own qualifying US rental property can generally claim depreciation using the same IRS schedules available to US investors. The property’s location and use are what matter, not the owner’s citizenship or residency status.

Do I need the Section 871(d) election to benefit from depreciation?

In most cases, yes. Without a Section 871(d) election, nonresident aliens are generally taxed on gross rental income, which limits the value of deductions such as depreciation. The election allows rental income to be taxed on a net basis, making depreciation deductions useful.

Is a cost segregation study worth it for a single rental property?

It depends on the property’s value, expected holding period, and tax situation. Cost segregation often provides the greatest benefit on higher-value properties where the additional deductions can justify the cost of the study.

What happens to depreciation when I sell the property?

Depreciation reduces your property’s tax basis over time. When the property is sold, some of the tax benefit may be recaptured by the IRS, and FIRPTA withholding may also apply to foreign investors. For a detailed explanation, see our guides to Capital Gains Tax for Foreign Investors and 1031 Exchanges.