Editorial Integrity

Making informed real estate decisions starts with having the right knowledge. At HomeAbroad, we offer US mortgage products for foreign nationals & investors and have a network of 500+ expert HomeAbroad real estate agents to provide the expertise you need. Our content is written by licensed mortgage experts and seasoned real estate agents who share insights from their experience, helping thousands like you. Our strict editorial process ensures you receive reliable and accurate information.

Quick Answer:

Yes, foreign nationals can use a DSCR loan for multifamily property purchases in the United States. Instead of qualifying based on personal income, employment history, or US credit, qualification is based primarily on the property’s combined rental income and its ability to support the mortgage payment.

Duplexes, triplexes, and fourplexes are financed as residential properties, which keeps the process simpler than commercial multifamily financing. Foreign national investors qualify with a 25% down payment in most cases.

Because rental income comes from multiple units, multifamily properties often generate stronger cash flow than comparable single-family rentals. This guide explains how a DSCR loan for multifamily property investments works, qualification requirements, down payments, and how foreign nationals can finance duplexes, triplexes, and fourplexes from abroad.

Table of Contents

What Counts as a 2–4 Unit Multifamily Property for a DSCR Loan?

A multifamily property is a residential building that contains more than one housing unit. However, not all multifamily properties are financed the same way.

For DSCR lending, the most important distinction is whether the property contains 2–4 units or 5 or more units. Duplexes, triplexes, and fourplexes are treated as residential real estate, while properties with five or more units fall into the commercial category.

The distinction determines whether a property is eligible for residential DSCR financing or commercial multifamily financing, making it one of the first considerations when evaluating a multifamily investment.

Duplex, Triplex, and Fourplex: The Residential 2–4 Unit Category

A 2–4 unit multifamily property consists of multiple residential units located on the same property.

Common examples include:

- Duplex: 2 residential units

- Triplex: 3 residential units

- Fourplex: 4 residential units

Although these properties generate income from multiple tenants, they are still considered residential real estate. This allows foreign national investors to use residential DSCR financing rather than navigating the additional complexity associated with commercial loans.

Duplexes, triplexes, and fourplexes can generate rental income from multiple units under a single loan, which often produces stronger cash flow than a comparable single-family rental.

Why Properties With 5+ Units Fall Into Commercial Financing

Properties with five or more units are evaluated differently because underwriting places greater emphasis on the property’s operating performance, income history, occupancy, and commercial-investment characteristics. As a result, financing often follows commercial multifamily guidelines rather than the residential underwriting standards commonly used for duplexes, triplexes, and fourplexes.

Commercial multifamily financing involves different underwriting standards, documentation requirements, loan structures, and approval processes. Rather than focusing primarily on a residential investment property’s rental income, the analysis becomes more similar to commercial real estate financing.

For many foreign national investors, duplexes, triplexes, and fourplexes offer a practical middle ground. They provide the income potential of a multifamily investment while remaining eligible for residential DSCR financing programs.

Why 2–4 Unit Properties Work Well for Foreign National Investors

Single-family rentals are often the starting point for foreign national investors. However, duplexes, triplexes, and fourplexes can offer an advantage that becomes important when financing is based on rental income: multiple units create multiple income streams.

For investors using a DSCR loan, higher rental income helps support the mortgage payment while generating positive cash flow. Instead of relying on a single tenant, a multifamily property collects rent from two, three, or four units under one loan.

At HomeAbroad, we’ve helped more than 500 investors from over 40 countries purchase and finance US investment properties. One reason duplexes, triplexes, and fourplexes remain popular investment properties is the balance they offer between income potential and financing simplicity. These properties can generate income from multiple units while still qualifying for residential financing programs.

One Loan, Multiple Rent Checks: How Multi-Unit Income Can Strengthen Your DSCR

A DSCR loan focuses on a property’s ability to generate enough rental income to cover its debt obligations. Because multifamily properties receive rent from multiple units, they have a larger rental-income base than a comparable single-family rental.

For example, if one unit becomes vacant in a fourplex, the property continues generating income from the remaining units. While vacancies still affect cash flow, income is not dependent on a single tenant.

This diversification is one reason duplexes, triplexes, and fourplexes are commonly used as long-term rental investments. Multiple units can help create more consistent income while improving overall portfolio resilience.

Steven Glick

Director of Mortgage Sales · HomeAbroad

The clients who choose duplexes, triplexes, and fourplexes are often looking for a balance between cash flow and simplicity. They like having multiple income-producing units under one property while still using residential financing rather than moving into commercial lending.

How a DSCR Loan Removes the No-US-Credit, No-US-Income Barrier

One of the biggest challenges foreign nationals face when investing in US real estate is qualifying for financing without a US credit history, US employment income, or domestic tax returns.

A DSCR loan approaches qualification differently. Rather than focusing primarily on personal income and employment documentation, qualification is based largely on the property’s rental-income potential.

How DSCR Is Calculated Across 2–4 Units

A DSCR loan measures whether a property’s rental income is sufficient to cover its housing expenses. For a duplex, triplex, or fourplex, the calculation uses the combined rental income from all units rather than looking at each unit separately.

This is one reason many investors prefer multifamily properties. Multiple income-producing units create a larger rental-income base, helping support the property’s debt obligations.

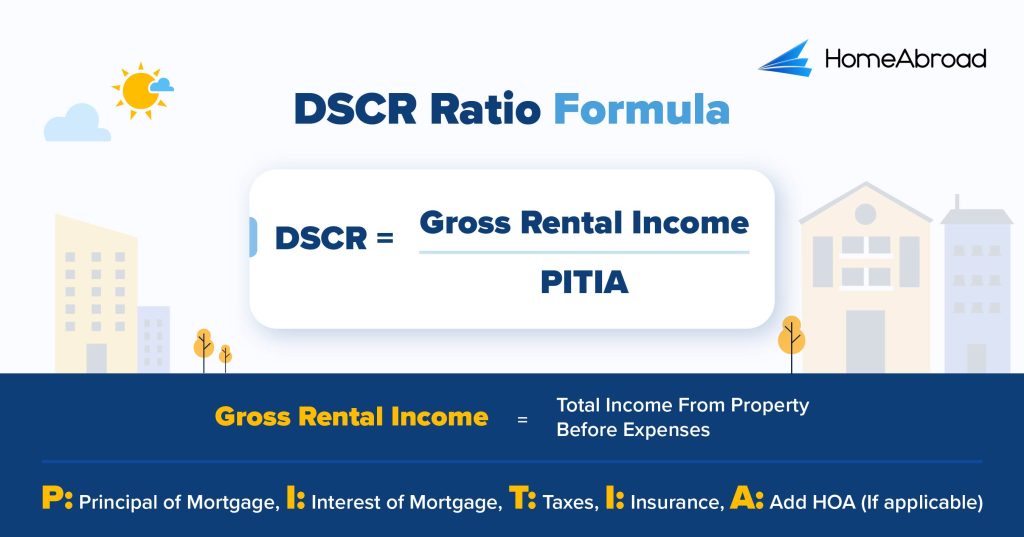

The Formula: Combined Gross Rent ÷ PITIA

DSCR stands for Debt Service Coverage Ratio. The ratio compares a property’s monthly rental income against its monthly housing expenses.

DSCR Formula:

Where:

- Rental Income = Combined monthly rent from all units

- PITIA = Principal, Interest, Taxes, Insurance, and Association Dues (if applicable)

A DSCR of 1.0 means the property’s rental income exactly covers its monthly housing expenses.

At HomeAbroad, a DSCR of 1.0 or higher generally provides the strongest path to qualification. However, some properties may still qualify through our No-Ratio DSCR program, which is designed for investments with a DSCR below 1.0.

Worked Example: A Fourplex Property

One of our foreign national investors purchased a fourplex using DSCR financing. The property generated rental income from four leased units, each with slightly different rents based on unit size and lease terms.

Monthly Rental Income

- Unit 1: $1,150

- Unit 2: $1,050

- Unit 3: $1,100

- Unit 4: $1,200

Combined Monthly Rent: $4,500

The property’s monthly PITIA (principal, interest, taxes, insurance, and association dues, where applicable) was approximately $3,600.

DSCR Calculation

$4,500 ÷ $3,600 = 1.25 DSCR

A DSCR of 1.25 means the property’s rental income exceeded its monthly housing expenses by 25%. Because qualification is based on the property’s income-producing ability, the combined rent from all four units helped support the loan.

What I tell clients at this step is to focus on the property’s total income picture. For a duplex, triplex, or fourplex, qualification is based on the combined rent from all units compared with the property’s housing expenses, not on any individual unit by itself.

The advantage of multifamily properties becomes easier to see when comparing how rental income scales across different property types.

Property Type | Monthly Rent | Monthly PITIA | DSCR |

|---|---|---|---|

Single-Family Rental |

| $2,400 | 1.13 |

Duplex | $4,000 | $3,000 | 1.33 |

Fourplex | $4,500 | $3,600 | 1.25 |

The comparison highlights how rental income can scale across multiple units while housing expenses remain tied to a single property. As the number of income-producing units increases, rental income may grow faster than housing expenses, helping strengthen a property’s DSCR and overall cash-flow profile.

DSCR Loan Requirements for Foreign Nationals Buying Multifamily Properties

Foreign national investors are often surprised to learn that financing a US duplex, triplex, or fourplex does not require the same documentation typically associated with conventional mortgages.

Our DSCR loan program is designed specifically for investment properties. Qualification focuses primarily on the property’s rental-income potential and the investor’s ability to complete the transaction, rather than US employment history, tax returns, or a domestic credit profile.

Features | Requirements |

|---|---|

DSCR Ratio | >= 1 for best terms, <1 eligible with a higher down payment. We provide DSCR Loans for foreign nationals with a DSCR ratio as low as 0.75, meaning you are eligible even if your rental covers just 75% of the mortgage. |

Credit Score | No US Credit History Required |

Down Payment | 25% |

LTV Ratio | Purchase: Up to 75% |

Cash Reserves | 6 Months |

Property Use | Investment properties (residential and commercial) |

Loan Amount | >=$100K – $10M |

Down Payment and LTV

For foreign national investors, HomeAbroad typically offers financing up to 75% LTV, which means a 25% down payment is generally required.

In addition to the down payment, investors should plan for closing costs and required reserves. Maintaining adequate liquidity after closing is an important part of building a sustainable investment portfolio.

Qualifying Without US Credit and Where an ITIN Fits

One of the most common misconceptions among international investors is that they need a US credit score before purchasing rental property in the United States.

US credit history is not required for HomeAbroad’s DSCR loan program. Investors can qualify without a US credit score, US employment income, or US tax returns because qualification is based primarily on the property’s rental-income potential.

An Individual Taxpayer Identification Number (ITIN) may be useful for certain banking or tax-related activities, but it is not required for every transaction.

Source of Funds, AML, and International Wire Transfers

Foreign national investors must be able to document the source of their down-payment funds, reserves, and closing funds.

This typically involves providing bank statements, investment-account records, business documentation, property-sale proceeds, or other records that establish a clear source of funds. Documentation is reviewed as part of anti-money laundering (AML) and compliance requirements.

One of the most common delays we see involves funds moving through multiple accounts without a clear paper trail. The strongest applications are usually the ones where documentation is organized before the property goes under contract.

International wire transfers should also be planned in advance to allow sufficient time for compliance reviews and funds to clear before closing.

Holding Title: LLC vs Personal Name

HomeAbroad can finance eligible multifamily investment properties purchased in either an investor’s personal name or through an LLC.

Many foreign national investors choose LLC ownership as part of a broader investment strategy, while others purchase directly in their own name. The appropriate structure depends on each investor’s circumstances and should be discussed with qualified legal and tax advisors.

Property Requirements: Non-Owner-Occupied and the 1007 Rent Schedule

HomeAbroad’s DSCR loans are intended for non-owner-occupied investment properties.

As part of the financing process, the property must be appraised and support the rental-income assumptions used for qualification. For many residential investment properties, the appraisal package includes a Form 1007 rent schedule, which helps establish market rental value.

Reserve Requirements and Other Qualification Factors

HomeAbroad generally requires six months of PITIA reserves after closing. Property condition, documentation quality, source-of-funds verification, and overall transaction strength also play a role in the approval process.

A property may produce attractive rental income and still fall short because of reserve requirements, documentation issues, or property-specific concerns. Reviewing these factors early can help investors avoid surprises later in the financing process.

How to Finance a Duplex, Triplex, or Fourplex From Abroad

Financing a duplex, triplex, or fourplex from abroad follows a structured process that can be completed remotely. HomeAbroad works with foreign national investors throughout the process, from pre-qualification to closing, allowing transactions to be completed without establishing a US employment history or relocating to the United States.

Step 1: Get Pre-Qualified

The process begins with a review of your investment goals, available funds, ownership structure, and target property type. This initial review helps determine purchasing power and identify the most appropriate financing options before you begin making offers.

Get pre-qualified for a 2–4 unit DSCR loan today!

Step 2: Analyze the Property and Rental Income

Once a property is identified, the next step is evaluating its rental-income potential. Because DSCR qualification is based primarily on the property’s income-producing ability, projected rents, market conditions, and cash-flow expectations all play an important role.

Many investors use HomeAbroad’s AI-native investment property search platform to compare opportunities, evaluate projected rental income, and identify properties that align with their investment objectives before moving forward.

Step 3: Complete the Application and Submit Documentation

After selecting a property, investors submit the mortgage application along with supporting documentation.

This typically includes identification documents, proof of available funds, source-of-funds documentation, and records needed to support the transaction. Investors purchasing through an LLC may also provide entity-related documentation during this stage.

Step 4: Appraisal and Rent Analysis

An appraisal is ordered to evaluate the property’s value and rental-income potential. For many multifamily properties, the appraisal package includes a rent schedule that helps establish market rents and supports the DSCR analysis.

This step confirms that the property’s income profile aligns with the financing request.

Step 5: Close Remotely

Many foreign national investors complete the closing process without traveling to the United States.

HomeAbroad can finance eligible properties purchased in an investor’s personal name or through an LLC, and we support remote closings for eligible transactions, allowing many investors to complete the purchase process from their home country. Once closing is complete, the property becomes part of the investor’s US rental portfolio and begins generating income according to its lease structure.

Common Mistakes and Edge Cases With Multi-Unit DSCR Loans

Most financing issues arise when investors assume every income-producing property is financed the same way. In practice, differences in unit count, reserve requirements, and property type can affect how a multifamily property is evaluated. Some of the most common issues arise when investors assume that every income-producing property is financed the same way.

Assuming a 5+ Unit Property Works Like a Fourplex

One of the most common misconceptions is that a five-unit apartment building can be financed exactly like a duplex, triplex, or fourplex.

In reality, the financing process changes significantly once a property contains five or more residential units. While a fourplex is typically eligible for residential DSCR financing, a five-unit property generally falls into the commercial multifamily category and follows a different underwriting process.

Steven Glick

Director of Mortgage Sales · HomeAbroad

One misconception we regularly clear up is that adding one more unit doesn’t change the financing. In practice, the difference between four units and five units can completely change the type of loan available and the documentation required.

Investors comparing multifamily opportunities should understand where that line exists before beginning their property search.

Under-Budgeting Reserves as Unit Count Increases

As properties become larger, investors often focus on purchase price and rental income while overlooking liquidity requirements. Reserve requirements become more important as property size and portfolio exposure increase. Investors who focus only on the down payment often underestimate the amount of liquidity needed to complete a transaction and operate the property comfortably after closing.

As portfolios grow or property values increase, reserve requirements can become a more meaningful part of the capital needed to complete a transaction. A property may appear affordable based on the down payment alone, but reserves, closing costs, and operating liquidity should also be factored into the investment plan.

Mixed-Use Properties and Short-Term Rental Income

Properties that combine residential and commercial uses require a separate review because financing eligibility depends on the property’s specific characteristics. Short-term-rental income is evaluated differently from traditional long-term rental income and should be discussed before making an offer.

Investors considering mixed-use buildings, vacation rentals, or unconventional property types should discuss the property’s specifics early in the financing process rather than assuming it will qualify under standard multifamily guidelines.

Identifying these issues early helps investors focus on properties that align with their financing strategy and reduces the likelihood of unexpected qualification issues later in the process.

Ready to Finance a Duplex, Triplex, or Fourplex?

For foreign national investors, duplexes, triplexes, and fourplexes can provide a practical way to generate rental income from multiple units while remaining eligible for residential DSCR financing.

HomeAbroad specializes in helping foreign nationals purchase and finance US investment properties. Our DSCR loan programs are designed for international investors and support eligible purchases through personal ownership structures or LLCs, without requiring US credit history.

Whether you’re evaluating your first duplex or comparing several multifamily investment opportunities, the next step is determining how much financing a specific property can support before you make an offer.

A pre-qualification review can help you understand available financing options, required documentation, projected cash flow, and the property’s rental-income profile before you move forward.

Get pre-qualified today to review your financing options, evaluate a property’s rental-income profile, and move forward with confidence.

FAQs

Can You Get a DSCR Loan on a Multifamily Property?

Yes. Foreign national investors can use a DSCR loan to finance eligible duplexes, triplexes, and fourplexes. Because these properties fall within the residential 1–4 unit category, they can typically be financed using residential DSCR loan programs rather than commercial multifamily financing. Qualification is based primarily on the property’s rental-income potential and ability to support the mortgage payment.

What’s a Good DSCR for a 2–4 Unit Property?

A DSCR of 1.0 or higher is generally considered a strong benchmark because it means the property’s rental income covers its monthly housing expenses. Higher ratios indicate an additional cash-flow cushion. HomeAbroad also offers No-Ratio DSCR options for certain investment properties that may not meet standard DSCR requirements.

How Much Down Payment Do Foreign Nationals Need?

At HomeAbroad, foreign national investors typically need a 25% down payment when financing a multifamily property through a DSCR loan program. Investors should also plan for closing costs and required reserves in addition to the down payment. The exact structure may vary based on the property and loan scenario.

Can I Hold a Multifamily Property in an LLC?

Yes. HomeAbroad can finance eligible multifamily investment properties held in an LLC or purchased in an investor’s personal name. Many foreign national investors use LLCs as part of a broader ownership strategy, although the appropriate structure depends on individual legal, tax, and investment objectives. Investors should consult qualified legal and tax advisors before making ownership decisions.

How Many DSCR Loans Can I Have?

There is no universal limit that applies to every investor or financing program. Many investors use DSCR loans to build portfolios over time, acquiring multiple rental properties as they expand their holdings. The ability to obtain additional financing typically depends on factors such as property performance, available reserves, liquidity, and overall portfolio strength.

![DSCR Loans Guide for Foreign Nationals: What It Is & How to Apply in [2026]](https://homeabroadinc.com/wp-content/uploads/2022/06/dscr-loan-guide-1.png)