Real reviews from international investors who closed with HomeAbroad

★★★★★

“Quick response, reliable & trustworthy. HomeAbroad helped me find the perfect agent & purchase my investment property in Katy, TX. Would definitely recommend!”

RM

Rashmi Mayekar

Non-US Resident Investor • Property

★★★★★

“HomeAbroad was a game-changer! They helped me get mortgage financing and find an agent who understood my needs. I couldn’t be happier with their assistance.”

SP

Steve Papadakis

Newcomer on H1-B Visa

★★★★★

“Awesome experience in working with them. Very patient in understanding my needs as an investor and helped me with the correct loan product for me. I will recommend them and use them again.”

JB

John Bolla

Investor from New York, NY

★★★★★

“Jonet from HomeAbroad answered all my questions regarding specifics for work visa holders to purchase our first investment property in Tampa. Was patient and kind and also connect me with a real estate agent.”

Ok

Okissa

Purchased Investment Property in Tampa.

🛂

Valid Passport

Current passport from your home country

💰

Proof of Funds

Bank statements showing down payment + 6 months reserves

Louisiana continues to attract income-focused real estate investors because rental returns remain compelling relative to entry prices. According to our internal market analysis, rental yields in Louisiana average around 8.7%, placing it among the stronger cash-flow markets in the US.

For foreign nationals, Louisiana’s appeal goes beyond yield alone. Lower price points reduce capital concentration risk, and many rental markets are supported by stable tenant bases tied to healthcare, education, energy, and port-related employment.

At HomeAbroad, we structure DSCR loans in Louisiana tailored for international real estate investors, allowing them to act on those opportunities without waiting to establish US income or residency. By qualifying primarily on the property’s rental performance, we help foreign nationals move forward when the numbers work, not when traditional documentation finally lines up.

DSCR Loan Louisiana Snapshot

No US Credit History

US Income and Credit History Not Required

Minimum Down Payment

25%

Maximum Loan Amount

$10M

Fast Track Closing

27 Days

DSCR LoanLouisianaProgram Terms

Feature

HomeAbroad DSCR Loan

DSCR Ratio

Best terms typically apply at DSCR ≥ 1.0. If DSCR is below 1.0, the loan may still be eligible with a higher down payment. Our No-Ratio DSCR option (DSCR 0 to 1) can support foreign national investors buying properties with clear income upside, even when the property’s rent does not fully cover the monthly payment.

US Credit Score

Not required for foreign nationals

Loan Amount

$100K – $10M

Down Payment

25%

LTV

Up to 75% (Purchase) Up to 75% (Rate and Term Refi) Up to 70% (Cash-Out Refi)

Cash Reserves

6 months

Where We Lend DSCR Loans in Louisiana

HomeAbroad offers DSCR loans across Louisiana, providing tailored support for global investors in top-performing cities, including New Orleans, Baton Rouge, Lafayette, and more. Here are a few cities where we lend DSCR Loans in Louisiana.

Shreveport

New Orleans

Baton Rouge

Lafayette

Lake Charles

Elmwood

Bossier City

Houma

Alexandria

Kenner

Monroe

Morgan City

Pineville/li>

Marrero

Gretna

Louisiana Investment Properties On Sale

Build wealth with HomeAbroad DSCR loans across Louisiana’s top markets.

Our streamlined digital process gets you from application to funding faster than traditional lenders.

1

Get Pre-Qualified

Submit a quick online application. No credit pull required for initial quote.

⏱ 5 minutes

2

Submit Documents

Upload property details, lease agreements, and basic ID verification.

⏱ Same day

3

Property Appraisal

We order an appraisal and a rent schedule to confirm DSCR qualification.

⏱ 5–7 days

4

Close & Fund

Sign closing documents and receive your funds. Remote closing available.

⏱ 27 days total

Why Investors Choose HomeAbroad

DSCR Loan Experts

We focus on DSCR investor loans. Expect clear cash flow math, rent documentation, and underwriting that reflects how rental properties are evaluated.

Foreign National Mortgage Experts

No US credit? No problem. At HomeAbroad, our expert loan officers can still qualify you for a DSCR loan. We do not rely on US income or tax returns to underwrite your loan.

AI-Powered Property Search Platform

Our investment property search helps you shortlist rentals that fit DSCR qualification. Screen for rent strength, yield, and investor criteria before you write the offer.

End-to-End Support

We keep the process moving, from LLC formation to bank accounts, insurance to property management. Everything is handled by us so you can focus on growing your portfolio.

Louisiana is a market where that approach makes practical sense. Investors here are often focused on rental stability, yield, and manageable entry prices instead of appreciation-driven strategies. That dynamic allows international buyers to participate without reshaping their finances to fit US-centric borrower standards.

What we see often is foreign nationals delaying solid opportunities because they assume financing depends on personal income profiles or long US credit histories. HomeAbroad’s DSCR loans remove that friction by keeping the decision anchored to the property itself, which aligns naturally with how income-focused rental deals are evaluated across Louisiana.

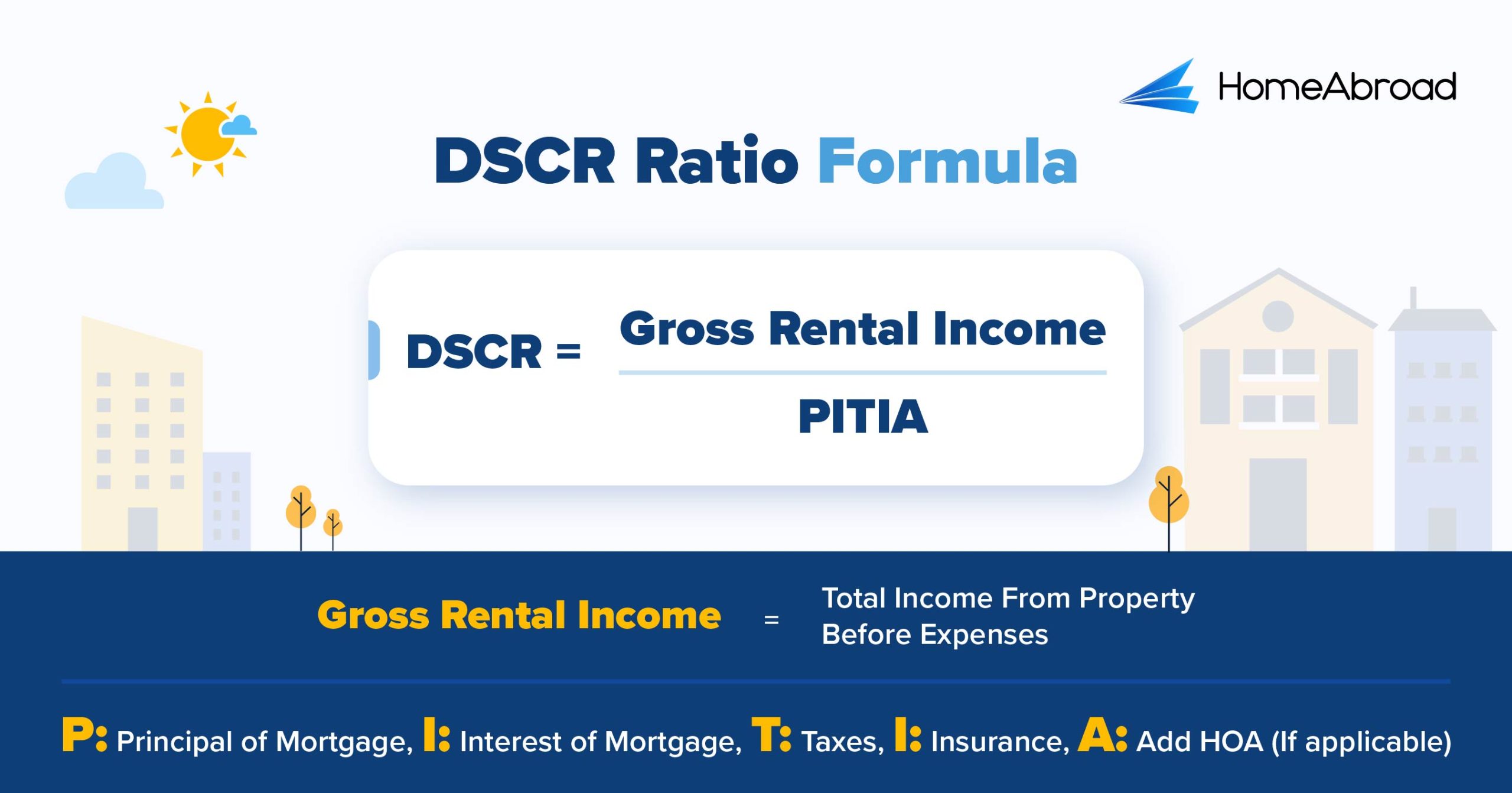

How DSCR is Calculated?

DSCR underwriting starts with a simple formula:

What counts as “Gross Rental Income” for DSCR Underwriting

Market rent supported by the appraisal rent schedule (commonly used for 1 to 4-unit rentals)

Executed lease rent, when acceptable to the lender and consistent with market support

What is included in PITIA

Principal

Interest

Taxes (Louisiana property taxes and applicable assessments)

Insurance (including wildfire-related costs where relevant)

Association dues (HOA), if applicable)

A Quick Example

Understand how DSCR Ratio is Calculated for a Louisiana Property:

Avg. Home Value in Shreveport: $132,659

Avg. Rental Income in Tampa: $1,111

Loan Term: 30 Years

Interest Rate: 7.4%

Monthly Mortgage Payment(PITIA):$860

DSCR = $1,111 ÷ $860

DSCR = 1.29

Monthly Positive Cash Flow: $251

A DSCR of 1.29 means the property generates more income than required to cover the loan’s debt obligations, creating positive cash flow and serving as a strong indicator of financial stability for us.

However, we understand that not every property's rental income will meet this threshold, which is why we also offer our No-Ratio DSCR Program for properties with a DSCR between 0 and 1. With the No-Ratio program, you can still secure financing, although it will require a slightly larger down payment (a 5% reduction in LTV) and a higher interest rate. This option is ideal for investors with a strong long-term strategy who want to acquire properties that may not immediately generate a 1.0 cash flow ratio.

Benefits of DSCR Loans in Louisiana

DSCR loans offer several advantages for foreign nationals investing in Louisiana:

Qualification Based on Rental Income, Not Personal Income Documentation

At HomeAbroad, we do not rely on US W2s, US paystubs, or US tax returns to qualify a foreign national DSCR loan. We qualify you primarily on the property’s rental income profile and the strength of your overall file.

Faster Closing Times

DSCR loans can move quickly when the property, rent support, and documentation are straightforward. Appraisal and rent schedule timing still matters, especially in competitive Louisiana markets. At HomeAbroad, we can close your deal in as few as 27 days.

Scale Your Portfolio Faster

International real estate investors like DSCR lending because it creates a repeatable qualification approach across multiple properties. When you understand how rent, PITIA, and reserves will be evaluated, it becomes easier to screen deals before you write offers.

Foreign National Friendly

DSCR loan is one of the best mortgage options for foreign nationals, who often face friction with conventional underwriting. DSCR lending is commonly used to reduce that friction because the property performance drives the qualification logic.

How HomeAbroad Helped a Canadian Investor Secure a DSCR Loan to Buy a Rental Property in Louisiana

David, a Canadian national, wanted to purchase his first rental property in the US as a way to build long-term passive income. Despite having the capital to invest, he repeatedly ran into roadblocks with traditional lenders that required US income, tax returns, or an established credit history.

That changed when David connected with Steven Glick, a seasoned loan expert at HomeAbroad who specializes in DSCR loans for foreign nationals. Steven guided him through the process, from identifying a cash-flowing property in Louisiana to closing remotely with minimal paperwork.

Director of Mortgage Sales, HomeAbroad | NMLS# 1231769

“In cases like this, the biggest unlock is shifting the focus from the investor’s income to the property. Once the rental income clearly supported the costs, the rest of the process moved quickly, even with the investor based outside the US.”

With expert guidance from HomeAbroad, David successfully entered the US rental market and began building long-term wealth without traveling or submitting traditional documentation

Louisiana Rental Market Overview

Louisiana’s rental market is supported by steady tenant demand and relatively affordable home prices compared to many other states. For many households, renting remains a practical choice, which helps maintain consistent leasing activity across the state.

Based on our analysis of primary public datasets, the following Louisiana market statistics provide helpful context for 2025:

Median gross rent in Louisiana: approximately $1,500/month

Median value of housing units: around $230,421 statewide

Median selected monthly owner costs with a mortgage: $1,540

Owner-occupied housing unit rate: 68.1% (implying a substantial renter share)

In our experience, rental demand in Louisiana tends to hold even when market conditions shift. Many tenants rent out of necessity or job mobility, which helps keep occupancy stable and supports income-focused rental investments.

Top Places to Invest in Louisiana with a DSCR Loan

Louisiana continues to attract income-focused real estate investors because of its affordability and rental performance. Based on our data, Louisiana’s average home price sits around $206,193, compared to the US average of $357,277, investors can enter the market at a significantly lower cost while still targeting meaningful rental income.

Baton Rouge, Lafayette, and Shreveport see steady, long-term demand from students and professionals driven by major universities and employers. At the same time, New Orleans, Lake Charles, and Natchitoches thrive on tourism, which drives strong short-term rental demand.

Below are some Louisiana cities international investors often consider when using a DSCR loan for rental property investments:

The investment properties shown below are pulled from the HomeAbroad property-search platform and can change daily. Review each listing’s rent assumptions, cash flow, and DSCR inputs before you underwrite an offer.

City

Rental Type

Rental Yield

New Orleans

Short-Term

23.5%

Baton Rouge

Short-Term

14.2%

Lafayette

Short-Term

12.7%

Shreveport

Long-Term

10%

Lake Charles

Long-Term

6.7%

New Orleans: The vibrant cultural capital with a booming short-term rental market

New Orleans isn’t just about music and Mardi Gras. Known as the Big Easy, it draws millions with its rich culture, festivals, and historic neighborhoods. This strong tourism appeal supports one of the most active short-term rental markets in the state.

Median Home Price: $247,205

Average Rent: $1,756

What this means for investors: New Orleans offers high short-term rental income potential, with solid occupancy rates and strong average nightly pricing. Its tourism-driven demand and limited supply of legal short-term rentals create a favorable environment for DSCR-based financing. International real estate investors can count on consistent rental income and long-term appreciation in key neighborhoods.

Investment Properties Listed Today on Sale in New Orleans

Baton Rouge: A steady performer with strong short-term rental appeal

As the state capital and home to Louisiana State University, Baton Rouge combines government stability with a vibrant student population and medical workforce. Its mix of education, healthcare, and culture drives year-round demand for both short- and mid-term rentals.

Median Home Price: $228,376

Average Rent: $1,406

What this means for investors: Baton Rouge offers predictable occupancy and high rental turnover, especially near university and hospital districts. Short-term rentals can perform well in targeted neighborhoods, making them a smart pick for global investors using DSCR loans to qualify based on the property’s rental income rather than personal documents.

Investment Properties Listed Today on Sale in Baton Rouge

Lafayette: A cultural hub with consistent rental returns

Lafayette is known for its Cajun heritage, vibrant arts scene, and strong regional economy. With key industries like healthcare, oil and gas services, and education, the city attracts a stable tenant base seeking both short- and long-term housing.

Median Home Price: $222,435

Average Rent: $1,432

What this means for investors: Lafayette provides a healthy balance of affordability and tenant demand. Foreign investors can tap into a growing rental market, qualify easily with DSCR loans, and build equity in one of Louisiana’s most stable mid-size cities.

Investment Properties Listed Today on Sale in Lafayette

Shreveport: A quiet cash flow city with solid long-term rental performance

Shreveport may not make national headlines, but it’s gaining traction with savvy global investors looking for affordable entry points and stable rental returns. With strong demand for single-family homes and a growing healthcare and logistics sector, Shreveport supports reliable long-term tenants.

Median Home Price: $135,592

Average Rent: $1,100

What this means for investors: Low home prices combined with strong rent-to-price ratios make Shreveport a prime location for long-term rental investments. International real estate investors can easily meet DSCR requirements and achieve positive cash flow without investing large amounts of upfront capital.

Investment Properties Listed Today on Sale in Shreveport

Lake Charles: An energy-driven city rebuilding with rental upside

Lake Charles sits at the heart of southwest Louisiana’s petrochemical and LNG industry. The town is in a rebuilding phase following recent hurricanes, creating a window of opportunity for investors focused on long-term growth and strong tenant demand.

Median Home Price: $197,450

Average Rent: $1,100

What this means for investors: Lake Charles offers a solid mix of affordability and rental demand, especially for long-term leases. With its industrial backbone and limited new construction, rental properties here can generate consistent income and meet DSCR benchmarks with ease.

Investment Properties Listed Today on Sale in Lake Charles

Louisiana Specific DSCR Underwriting Factors that Investors Overlook

Louisiana’s real estate market offers affordable entry points and high rental yields, especially in cities like New Orleans, Baton Rouge, and Lafayette. However, the state’s distinct legal system, weather risks, and short-term rental laws require special attention.

Key factors to keep in mind include:

Rental use and tenant profile assumptions

In Louisiana, rental performance can vary significantly based on who the tenant base actually is. Workforce rentals, student housing, and tourism-driven rentals behave very differently in terms of stability and turnover.

What we see often is investors applying the same rent assumptions across markets without accounting for tenant profile, which can affect how reliably rental income supports DSCR over time.

Hurricane Exposure and Insurance Volatility

Louisiana faces recurring storm activity and rising flood insurance costs. Many private insurers have scaled back coverage, prompting reliance on state-run Louisiana Citizens policies. Properties in coastal or low-lying zones may require both homeowners and flood insurance. Newer homes or raised structures often get better rates.

Director of Mortgage Sales, HomeAbroad | NMLS# 1231769

“Hurricane exposure doesn’t mean a deal won’t work in Louisiana, but insurance has to be modeled realistically from the start. We’ve seen otherwise solid rentals tighten simply because coverage assumptions were too optimistic.”

Property condition and age of housing stock

Many Louisiana rental properties, especially in established neighborhoods, are older homes. Deferred maintenance, roof age, or outdated systems can affect both lender comfort and eligibility. This won’t work if a property isn’t move-in ready. DSCR loans require the asset to be rentable at closing, not a heavy-rehab project.

Parish-level taxes and assessment differences

Property taxes in Louisiana are assessed at the parish level, and millage rates can vary meaningfully between locations. Investors should review local tax assessments carefully, as variations in parish taxes can impact monthly ownership costs and long-term projections.

Strategic & Future Considerations for Foreign Nationals Investing in Louisiana

Louisiana offers international real estate investors a mix of historic charm, strong cultural tourism, and steady rental demand from both urban and industrial markets. Looking forward, infrastructure recovery, climate resilience efforts, and suburban development are shaping the next wave of real estate opportunities across the state.

Below are key considerations foreign nationals should keep in mind when investing in Louisiana real estate.

1. Unrestricted Foreign Property Ownership:

Louisiana allows full property ownership rights for foreign nationals, supporting direct investment in residential and mixed-use properties. This legal ease is especially favorable for first-time international real estate investors entering the US market.

2. Energy and Industrial Corridor Development:

Baton Rouge, Lake Charles, and Lafayette are part of the Gulf Coast’s energy belt. Continued investment in LNG, chemical, and shipping infrastructure creates consistent housing demand from rotating contractors and long-term workforce renters.

3. Major Urban and Entertainment Development

Large-scale projects like Miami Freedom Park are examples of how entertainment and mixed-use development can shape neighborhood appeal and regional demand. These kinds of projects often spur nearby residential and retail activity, attracting tenants and businesses that contribute to tighter rental markets.

4. Growing Suburban and Inland Markets

Secondary cities and surrounding suburbs, particularly those near economic corridors, are drawing interest due to affordability, local job growth, and improved flood mitigation strategies, opening up stable long-term rental prospects.

Louisiana DSCR Loan FAQs

Can foreign nationals apply for DSCR loans in the state of Louisiana?

Yes, foreign nationals can apply for DSCR loans in Louisiana through HomeAbroad, eliminating the need for a US credit score, making it a flexible financing option for global investors.

What types of properties are eligible for a DSCR loan in Louisiana?

You can finance single-family homes, duplexes, triplexes, and even short-term rental properties in high-demand cities like Baton Rouge, Lafayette, and New Orleans.

Can I apply for a DSCR loan from abroad?

Absolutely. HomeAbroad supports remote applications and closings, so you can invest in Louisiana real estate without visiting the US.

Can I refinance my Louisiana property to grow my portfolio?

Yes. If you already own a rental property in Louisiana, you can refinance to tap the equity you’ve built. Use it to purchase another property, renovate, or diversify, without personal income verification.

About the author:

Steven Glick is the Director of Mortgage Sales at HomeAbroad and has over a decade of experience in the mortgage industry. As a licensed mortgage originator (NMLS# 1231769), Steven brings deep expertise in loan processing, sales operations, and non-traditional mortgages.

* Scenario-based rate shown for illustrative purposes. Reflects current pricing available to qualified borrowers with strong credit, low loan-to-value, qualifying DSCR, and selected loan terms. Actual rates vary by borrower, property, and market conditions. Not a commitment to lend. Foreign national DSCR pricing may differ from U.S. borrower programs.

Why Choose Us

Built for Foreign Real Estate Investors

HomeAbroad is a one-stop shop for global investors, from finding properties to securing financing, setting up your LLC, opening a US bank account, and managing your portfolio.

🌍

Foreign National Mortgage Experts

No US credit history, income, or residency required. We've helped thousands of international real estate investors finance Louisiana real estate.

🤖

AI–Powered Property Search

Our investment property search platform helps you discover high-yield rentals across Louisiana using smart algorithms.

⌚

Fast Digital Process

Close in as fast as 27 days with our streamlined application, remote notarization [remote closing], and digital document signing.

🤝

500+ Expert Agents

Work with our network of experienced real estate agents who specialize in investment properties across Louisiana.

Ready to Get Started?

Get your personalized rate quote in minutes. No credit pull, no obligation.

48

States We Lend In

27 Days

Average Close Time

500+

Partner Real Estate Agents

4.9 Star

Customer Rating

Pre-qualify for a DSCR Loan as an international investor

No U.S. credit history. No personal income verification. Qualify based on property’s rental income.