Real reviews from international investors who closed with HomeAbroad

★★★★★

“Quick response, reliable & trustworthy. HomeAbroad helped me find the perfect agent & purchase my investment property in Katy, TX. Would definitely recommend!”

RM

Rashmi Mayekar

Non-US Resident Investor • Property

★★★★★

“HomeAbroad was a game-changer! They helped me get mortgage financing and find an agent who understood my needs. I couldn’t be happier with their assistance.”

SP

Steve Papadakis

Newcomer on H1-B Visa

★★★★★

“Awesome experience in working with them. Very patient in understanding my needs as an investor and helped me with the correct loan product for me. I will recommend them and use them again.”

JB

John Bolla

Investor from New York, NY

★★★★★

“Jonet from HomeAbroad answered all my questions regarding specifics for work visa holders to purchase our first investment property in Tampa. Was patient and kind and also connect me with a real estate agent.”

Ok

Okissa

Purchased Investment Property in Tampa.

🛂

Valid Passport

Current passport from your home country

💰

Proof of Funds

Bank statements showing down payment + 6 months reserves

Florida is the top destination for foreign real estate investors in the US, accounting for 21% of all foreign buyer purchases. Markets like Miami, Orlando, Tampa, and Jacksonville continue to attract investors, supported by strong rental demand, population growth, and steady occupancy across both long-term and short-term rentals.

For international real estate investors, the challenge is rarely finding a property. It is getting financing that does not depend on US tax returns, US income, or US credit report.

HomeAbroad’s DSCR loan solves that problem by qualifying you primarily on the property’s rental income, not your personal income. We originate DSCR loans for foreign nationals and underwrite them with a Florida-specific lens, including rent caps, property tax mechanics, HOA dues, and insurance realities that directly affect DSCR.

DSCR Loan Florida Snapshot

No US Credit History

US Income and Credit History Not Required

Minimum Down Payment

25%

Maximum Loan Amount

$10M

Fast Track Closing

27 Days

DSCR Loan Florida Program Terms

Feature

HomeAbroad DSCR Loan

DSCR Ratio

Best terms typically apply at DSCR ≥ 1.0. If DSCR is below 1.0, the loan may still be eligible with a higher down payment. Our No-Ratio DSCR option (DSCR 0 to 1) can support foreign national investors buying properties with clear income upside, even when the property’s rent does not fully cover the monthly payment.

US Credit Score

Not required for foreign nationals

Loan Amount

$100K – $10M

Down Payment

25%

LTV

Up to 75% (Purchase) Up to 75% (Rate and Term Refi) Up to 70% (Cash-Out Refi)

Cash Reserves

6 months

Where We Lend DSCR Loans in Florida

HomeAbroad offers DSCR loans across Florida, providing tailored support for global investors in top-performing cities, including Miami, Tampa, Orlando, and more. Here are a few cities where we lend DSCR Loans in Florida.

Miami

Tampa

Jacksonville

Tallahassee

Orlando

Fort Lauderdale

St. Petersburg

Hialeah

West Palm Beach

Gainesville

Lakeland

Hollywood

Pompano Beach

Deltona

Sarasota

Florida Investment Properties On Sale

Build wealth with HomeAbroad DSCR loans across Florida’s top markets.

Our streamlined digital process gets you from application to funding faster than traditional lenders.

1

Get Pre-Qualified

Submit a quick online application. No credit pull required for initial quote.

⏱ 5 minutes

2

Submit Documents

Upload property details, lease agreements, and basic ID verification.

⏱ Same day

3

Property Appraisal

We order an appraisal and a rent schedule to confirm DSCR qualification.

⏱ 5–7 days

4

Close & Fund

Sign closing documents and receive your funds. Remote closing available.

⏱ 27 days total

Why Investors Choose HomeAbroad

DSCR Loan Experts

We focus on DSCR investor loans. Expect clear cash flow math, rent documentation, and underwriting that reflects how rental properties are evaluated.

Foreign National Mortgage Experts

No US credit? No problem. At HomeAbroad, our expert loan officers can still qualify you for a DSCR loan. We do not rely on US income or tax returns to underwrite your loan.

AI-Powered Property Search Platform

Our investment property search helps you shortlist rentals that fit DSCR qualification. Screen for rent strength, yield, and investor criteria before you write the offer.

End-to-End Support

We keep the process moving, from LLC formation to bank accounts, insurance to property management. Everything is handled by us so you can focus on growing your portfolio.

What we see often is that international real estate investors delay purchases because they assume financing requires permanent residency or a long US financial history. DSCR loans remove that assumption by allowing investors to move forward based on the property’s income potential, making Florida rental investments accessible earlier in the investment cycle.

DSCR Loans give foreign nationals more flexibility to enter the Florida real estate market. Instead of waiting to establish local employment or residency, investors can evaluate opportunities based on rental performance and move when the numbers make sense.

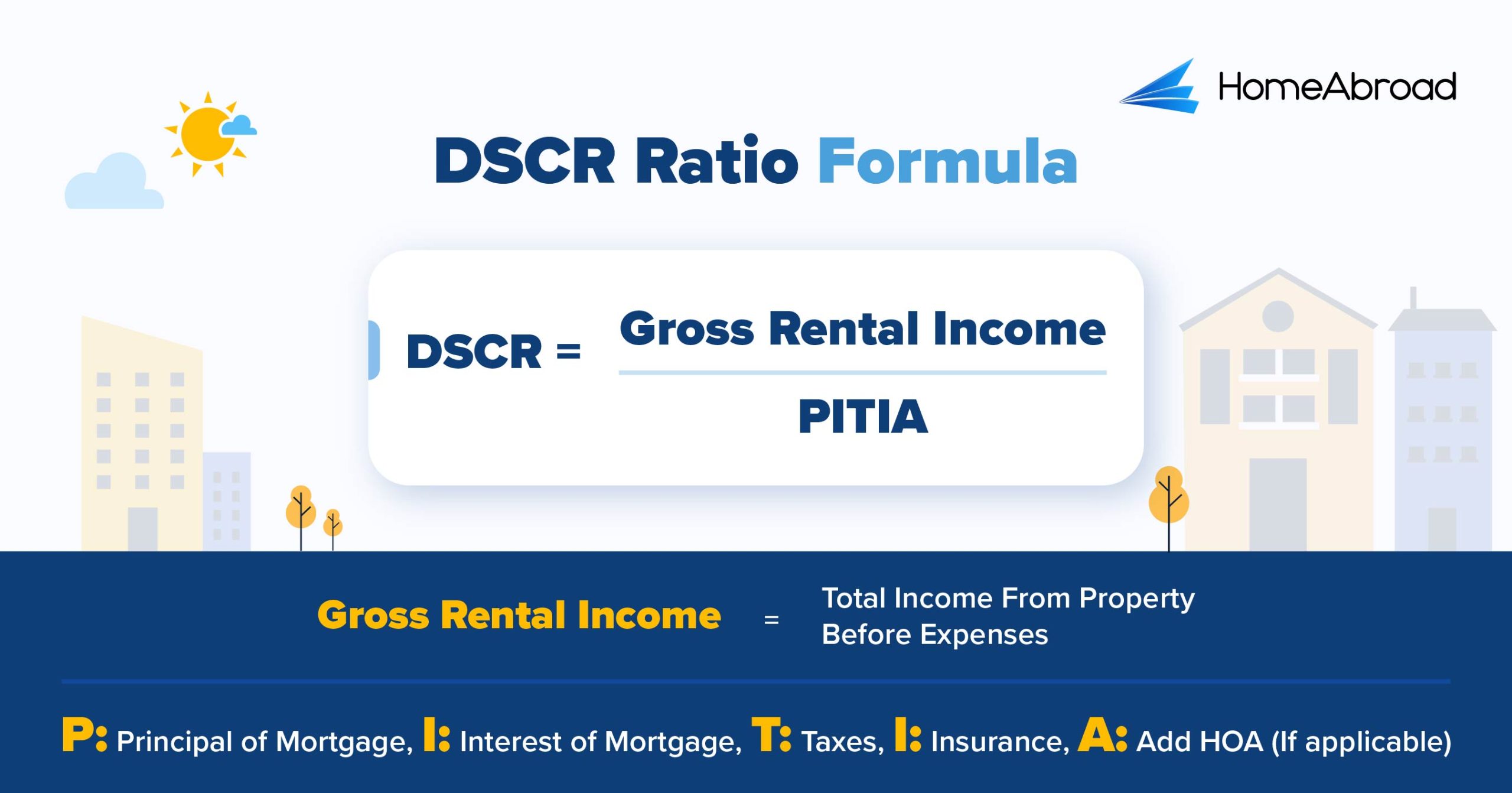

How DSCR is Calculated?

DSCR underwriting starts with a simple formula:

What counts as “Gross Rental Income” for DSCR Underwriting

Market rent supported by the appraisal rent schedule (commonly used for 1 to 4-unit rentals)

Executed lease rent, when acceptable to the lender and consistent with market support

What is included in PITIA

Principal

Interest

Taxes (Florida property taxes and applicable assessments)

Insurance (including wildfire-related costs where relevant)

Association dues (HOA), if applicable)

A Quick Example

Understand how DSCR Ratio is Calculated for a Florida Property:

Avg. Home Value in Tampa: $368,151

Avg. Rental Income in Tampa: $1,980

Loan Term: 30 Years

Interest Rate: 7.4%

Monthly Mortgage Payment(PITIA):$1,460

DSCR = $1,980 ÷ $1,460

DSCR = 1.3

Monthly Positive Cash Flow: $520

A DSCR of 1.3 means the property generates more income than required to cover the loan’s debt obligations, creating positive cash flow and serving as a strong indicator of financial stability for us.

However, we understand that not every property's rental income will meet this threshold, which is why we also offer our No-Ratio DSCR Program for properties with a DSCR between 0 and 1. With the No-Ratio program, you can still secure financing, although it will require a slightly larger down payment (a 5% reduction in LTV) and a higher interest rate. This option is ideal for investors with a strong long-term strategy who want to acquire properties that may not immediately generate a 1.0 cash flow ratio.

Benefits of DSCR Loans in Florida

DSCR loans offer several advantages for foreign nationals investing in Florida:

Qualification Based on Rental Income, Not Personal Income Documentation

At HomeAbroad, we do not rely on US W2s, US paystubs, or US tax returns to qualify a foreign national DSCR loan. We qualify you primarily on the property’s rental income profile and the strength of your overall file.

Faster Closing Times

DSCR loans can move quickly when the property, rent support, and documentation are straightforward. Appraisal and rent schedule timing still matters, especially in competitive Florida markets. At HomeAbroad, we can close your deal in as few as 27 days.

Scale Your Portfolio Faster

International real estate investors like DSCR lending because it creates a repeatable qualification approach across multiple properties. When you understand how rent, PITIA, and reserves will be evaluated, it becomes easier to screen deals before you write offers.

Foreign National Friendly

DSCR loan is one of the best mortgage options for foreign nationals, who often face friction with conventional underwriting. DSCR lending is commonly used to reduce that friction because the property performance drives the qualification logic.

“Most foreign nationals we work with assume financing will be the hardest part of buying in Florida. In reality, once the deal is structured around the property’s rental income, a DSCR loan becomes a scalable way to finance rental property.”

How HomeAbroad Helped an International Investor Get a DSCR Loan in Florida

HomeAbroad worked with an international investor based in Europe who was purchasing a long-term rental property in Tampa, Florida. The investor did not have US income or a US credit history and wanted financing that relied on the property’s cash flow rather than personal documentation.

Using HomeAbroad’s DSCR loan, the deal was underwritten entirely on rental income, allowing the investor to move forward without traditional financing roadblocks.

Property Details:

Location: Tampa Property Value: $420,000 Monthly Rental Income: $2,850

Loan Details:

Loan Amount: $315,000 Down Payment: 25% ($105,000) Interest Rate: 7.1% Loan Term: 30 years Monthly Mortgage (PITIA): $2,130

With a DSCR of 1.33, the property comfortably supports the loan based on rental income alone and generates $720 in monthly cash flow, showing how DSCR financing can work for foreign nationals investing in Florida without relying on US income, employment, or credit history.

Florida Rental Market Overview

Florida’s rental market remains one of the strongest in the nation, driven by population growth, a large renter base tied to mobility and tourism, and a steady pipeline of domestic and international tenants, all of which support rental absorption across the state.

As per our data, the key market statistics for 2025 are:

Median gross rent in Florida: approximately $2,304/month

Median value of housing units: around $419,000 statewide

Median selected monthly owner costs with a mortgage: $1,860

Owner-occupied housing unit rate: 67.3% (implying a substantial renter share)

The distinction here is market structure. Florida combines relatively accessible home prices with a large renter population, which supports rental participation even as ownership costs rise. That balance is a key reason Florida remains a rental-first market for many investors, including international real estate investors entering the US for the first time.

Top Places to Invest in Florida with a DSCR Loan

Florida continues to shine as one of the best states for real estate investment, and for good reason. With year-round sunshine, no state income tax, and a steady influx of new residents and tourists, it’s a natural hotspot for both long-term and short-term rental opportunities.

For foreign nationals investing in the US, Florida’s rental market offers an ideal landscape for using DSCR loans, especially when the focus is on the property’s rental income rather than the borrower’s personal income.

Here are some top cities in Florida for international real estate investors to consider for their next successful DSCR loan investment:

The investment properties shown below are pulled from the HomeAbroad property-search platform and can change daily. Review each listing’s rent assumptions, cash flow, and DSCR inputs before you underwrite an offer.

City

Rental Type

Rental Yield

Orlando

Short-Term

12.2%

Tampa

Short-Term

10.4%

Miami

Short-Term

9%

Jacksonville

Long-Term

6.7%

Fort Lauderdale

Long-Term

6.5%

Orlando: The Theme Park Capital and Growing Tech Hub

Orlando isn’t just for Mickey Mouse or theme parks. While it remains a global magnet for tourism, it’s also growing fast in tech, healthcare, and logistics. This mix makes it a powerhouse for rental income, both from vacation rentals and long-term leases.

Median Home Price: $368,928

Average Short-term Rent: $3,771/month

What this means for investors: Steady appreciation, strong tenant demand, and the perfect setup for DSCR-based qualification thanks to consistently high rental income.

Investment Properties Listed Today on Sale in Orlando

Tampa blends big-city opportunities with Gulf Coast lifestyle. Think corporate headquarters, tech startups, and one of the country’s most desirable places to live and work. The revitalized downtown and constant job growth attract both professionals and renters in droves.

Median Home Price: $368,151

Average Short-term Rent: $3,190/month

What this means for investors: High rents paired with a stable economy make it easy to meet DSCR thresholds, even for foreign nationals without US income or credit history.

Investment Properties Listed Today on Sale in Tampa

Miami: The International Gateway to Luxury and Culture

Miami is a vibrant global hub attracting foreign nationals and high-net-worth individuals. Its luxury condos and waterfront properties drive strong demand, especially in the short-term rental market.

Median Home Price: $571,026

Average Short-term Rent: $4,326/month

What this means for investors: Miami’s high rents and luxury market provide significant rental income potential, making it a strong contender for DSCR loans even in a shifting market.

Investment Properties Listed Today on Sale in Miami

Jacksonville offers affordability combined with steady growth. Its diverse economy and large land area support solid rental demand, making it attractive for investors seeking reliable cash flow.

Median Sold Price: $280,096

Average Rent: $1,569/month

What this means for investors: With lower property prices and solid rents, Jacksonville is ideal for cash-flow-driven investors looking to meet DSCR loan requirements with ease.

Investment Properties Listed Today on Sale in Jacksonville

Fort Lauderdale: Coastal Charm Meets Investment Opportunity

With its winding canals and luxury lifestyle, Fort Lauderdale is ideal for high-end short-term rentals. Its strong vacation market and upscale appeal make it a great choice for international real estate investors aiming for premium returns.

Median Home Price: $502,571

Average Rent: $2,740/month

What this means for investors: The current market favors buyers, offering more room to negotiate on price. With elevated rents, it’s a perfect fit for DSCR financing, especially for luxury or waterfront properties.

Investment Properties Listed Today on Sale in Fort Lauderdale

Florida Specific DSCR Underwriting Factors that Investors Overlook

Insurance Costs and Coverage Requirements

Florida underwriting places far more weight on property insurance than many investors expect. Wind and flood coverage can materially change monthly expenses, which directly impacts DSCR.

In our experience, deals that look strong on rent can fall below DSCR thresholds once insurance is finalized. This is why insurance needs to be reviewed early and priced accurately before underwriting begins.

Condo and HOA Structures

Florida has a high concentration of condos, especially in coastal and metro markets. HOA dues, special assessments, and rental restrictions flow directly into PITIA and can materially affect DSCR outcomes.

One thing that surprises investors is how quickly HOA costs add up and how often they’re underestimated during deal analysis. These fees are not optional in underwriting.

Short-Term Rental Rules Vary by City

Florida does not have a single, uniform short-term rental framework. Regulations are set at the city and county level, and rules can differ dramatically even within the same metro area. Some cities limit rental frequency, require local licensing, or impose additional taxes and compliance requirements.

“A lot of investors assume short-term rental rules are uniform across Florida. In reality, STR rules are set locally, and we’ve seen deals run into issues when city restrictions aren’t checked early. If STR income is part of your DSCR strategy, local compliance has to be confirmed before you rely on those numbers.”

Strategic & Future Considerations for Foreign Nationals Investing in Florida

Florida’s real estate markets continue to evolve as population growth, infrastructure investment, and economic diversification shape where and how rental properties perform. Long-term investors should factor in broader trends that can influence demand, accessibility, and neighborhood fundamentals.

Below are key considerations international real estate investors should keep in mind when investing in Florida real estate:

1. Infrastructure Expansion Enhances Connectivity

Florida is advancing major transportation and connectivity projects that improve access across key metros. Projects under the Moving Florida Forward initiative are already easing congestion on routes like I-4 and expanding freight and commuter capacity at major interchanges, which supports both residential and commercial growth.

Future infrastructure improvements can strengthen secondary markets and make more areas livable and investable, which may expand where DSCR-qualified properties make sense.

2. Population Growth Drives Broad Tenant Demand

Florida continues to see significant domestic and international migration, which sustains rental demand across long-term and short-term markets. Even as affordability shifts and inventory adjusts, ongoing in-migration supports occupancy and cash flow fundamentals in cities from Miami to Jacksonville.

3. Major Urban and Entertainment Development

Large-scale projects like Miami Freedom Park are examples of how entertainment and mixed-use development can shape neighborhood appeal and regional demand. These kinds of projects often spur nearby residential and retail activity, attracting tenants and businesses that contribute to tighter rental markets.

4. Transit and Regional Growth Initiatives

Planned transit and mixed mobility projects, such as light rail expansions in Broward County, signal long-term efforts to improve public transportation and connectivity between major economic hubs, like airports, ports, and downtown cores. These improvements can support workforce access to jobs and expand the appeal of rental properties near transit corridors.

Florida DSCR Loan FAQs

Can foreign nationals apply for DSCR loans in the state of Florida?

Yes, foreign nationals can apply for DSCR loans in Florida through HomeAbroad, eliminating the need for a US credit score, making it a flexible financing option for global investors.

Can I buy an investment property in Florida while living in another country?

Yes. Foreign nationals can purchase Florida investment property without being physically present in the US. HomeAbroad supports remote DSCR loan closings, allowing the entire process to be completed while you’re abroad.

What are the interest rates for DSCR loans in Florida?

DSCR loan interest rates vary based on market conditions, borrower profiles, and property type, but are typically higher than conventional loan rates. However, HomeAbroad offers competitive rates that enable investors to leverage property cash flow to achieve better returns.

How long does it take to get a DSCR loan in Florida?

At HomeAbroad, we streamline the application process to ensure a smooth experience from loan application to closing. We guarantee that the closing will happen within 30 days.

About the author:

Steven Glick is the Director of Mortgage Sales at HomeAbroad and has over a decade of experience in the mortgage industry. As a licensed mortgage originator (NMLS# 1231769), Steven brings deep expertise in loan processing, sales operations, and non-traditional mortgages.

* Scenario-based rate shown for illustrative purposes. Reflects current pricing available to qualified borrowers with strong credit, low loan-to-value, qualifying DSCR, and selected loan terms. Actual rates vary by borrower, property, and market conditions. Not a commitment to lend. Foreign national DSCR pricing may differ from U.S. borrower programs.

Why Choose Us

Built for Foreign Real Estate Investors

HomeAbroad is a one-stop shop for global investors, from finding properties to securing financing, setting up your LLC, opening a US bank account, and managing your portfolio.

🌍

Foreign National Mortgage Experts

No US credit history, income, or residency required. We've helped thousands of international real estate investors finance Florida real estate.

🤖

AI–Powered Property Search

Our investment property search platform helps you discover high-yield rentals across Florida using smart algorithms.

⌚

Fast Digital Process

Close in as fast as 27 days with our streamlined application, remote notarization [remote closing], and digital document signing.

🤝

500+ Expert Agents

Work with our network of experienced real estate agents who specialize in investment properties across Florida.

Ready to Get Started?

Get your personalized rate quote in minutes. No credit pull, no obligation.

48

States We Lend In

27 Days

Average Close Time

500+

Partner Real Estate Agents

4.9 Star

Customer Rating

Pre-qualify for a DSCR Loan as an international investor

No U.S. credit history. No personal income verification. Qualify based on property’s rental income.