Wisconsin offers a steady, practical rental landscape with property prices and rent levels that tend to stay in balance. Instead of sharp swings, demand is supported by hospitals, universities, manufacturing, and regional employers across multiple cities.

Markets like Milwaukee, Madison, and Green Bay provide investors with reasonable entry points and consistent renter demand, making it easier to evaluate deals on cash flow rather than speculation.

With HomeAbroad’s DSCR loans, investors can finance Wisconsin rental properties based on rental income, allowing deals to move forward without relying on personal income or US credit history.

DSCR Loan Wisconsin Snapshot

No US Credit History

US Income and Credit History Not Required

Minimum Down Payment

25%

Maximum Loan Amount

$10M

Fast Track Closing

27 Days

DSCR Loan Wisconsin Program Terms

Feature

HomeAbroad DSCR Loan

DSCR Ratio

Best terms typically apply at DSCR ≥ 1.0. If DSCR is below 1.0, the loan may still be eligible with a higher down payment. Our No-Ratio DSCR option (DSCR 0 to 1) can support foreign national investors buying properties with clear income upside, even when the property’s rent does not fully cover the monthly payment.

US Credit Score

Not required for foreign nationals

Loan Amount

$100K – $10M

Down Payment

25%

LTV

Up to 75% (Purchase) Up to 75% (Rate and Term Refi) Up to 70% (Cash-Out Refi)

Cash Reserves

6 months

Table of Contents

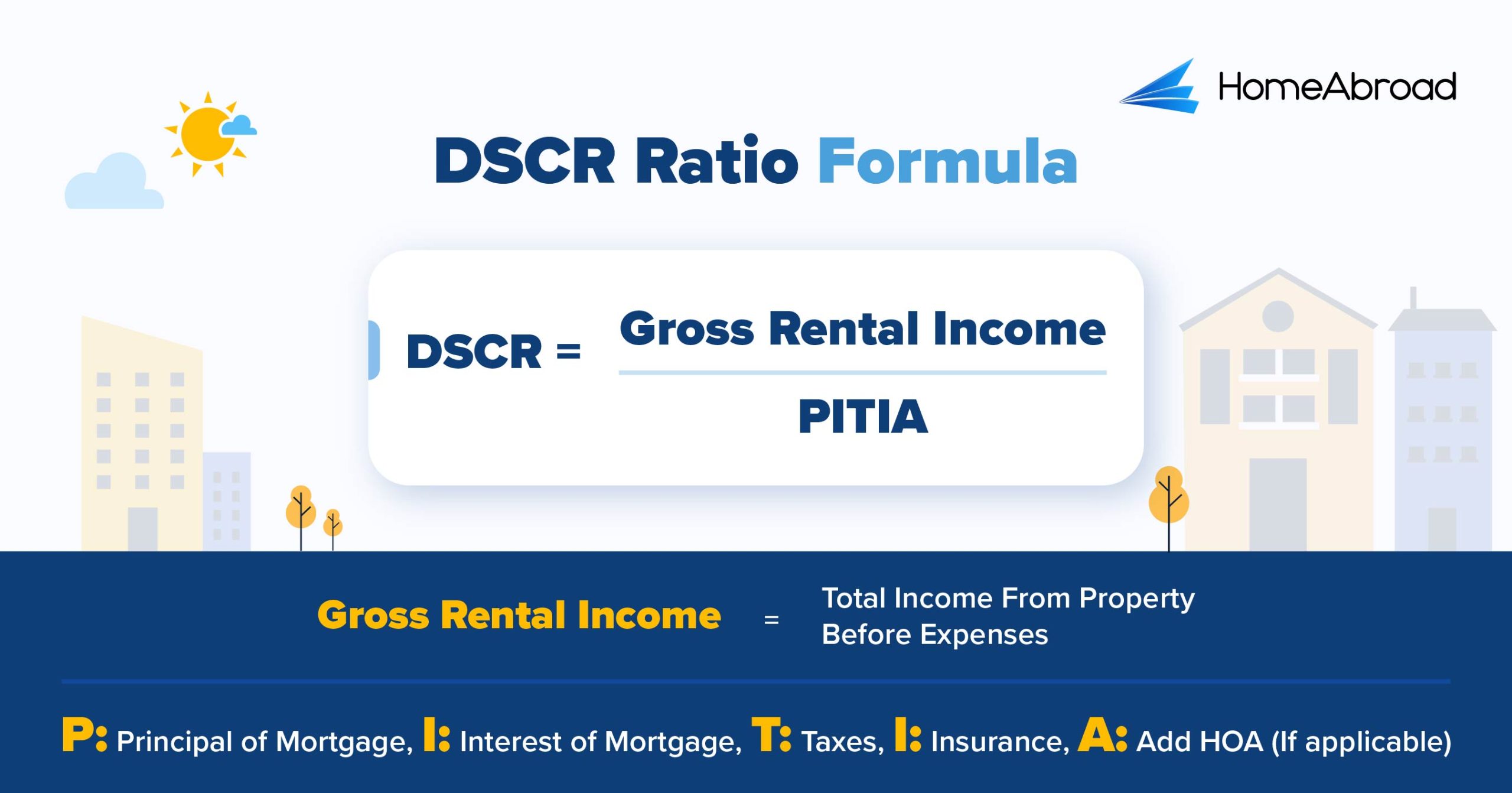

How DSCR is Calculated?

DSCR underwriting starts with a simple formula:

What counts as “Gross Rental Income” for DSCR Underwriting

Market rent supported by the appraisal rent schedule (commonly used for 1 to 4-unit rentals)

Executed lease rent, when acceptable to the lender and consistent with market support

What is included in PITIA

Principal

Interest

Taxes (Wisconsin property taxes and applicable assessments)

Insurance (including wildfire-related costs where relevant)

Association dues (HOA), if applicable)

Example

Calculating the DSCR Ratio for a Wisconsin Property:

Avg. Home Price: $195,542

Down payment: 25%

Loan Term: 30 Years

Interest Rate: 7.2%

Monthly Mortgage Payment(PITIA): $1,316

Avg. Rental Income: $1,500

DSCR = $1,500÷ $1,316

DSCR = 1.14

Monthly Positive Cash Flow: $184

A DSCR of 1.14 shows that the property’s rental income covers its full monthly costs with room to spare, resulting in about $184 in positive monthly cash flow. This level of coverage is typically sufficient for DSCR qualification and helps keep the investment stable even if expenses shift slightly over time.

Use our DSCR Ratio Calculator to see how your property’s rent and expenses stack up.

However, not all properties will meet this threshold, so we also offer our No-Ratio DSCR Program for properties with a DSCR between 0 and 1. This option allows investors to still qualify for financing, but it comes with a slightly larger down payment (a 5% hit to LTV) and higher interest rates. This program focuses less on rental income and more on other factors, giving investors with strong long-term plans the opportunity to secure financing.

🛂

Valid Passport

Current passport from your home country

💰

Proof of Funds

Bank statements showing down payment + 6 months reserves

Benefits of DSCR Loans in Wisconsin

DSCR loans offer several advantages for foreign nationals investing in Wisconsin:

Qualification Based on Rental Income, Not Personal Income Documentation

At HomeAbroad, we do not rely on US W2s, US paystubs, or US tax returns to qualify a foreign national DSCR loan. We qualify you primarily on the property’s rental income profile and the strength of your overall file.

Faster Closing Times

DSCR loans can move quickly when the property, rent support, and documentation are straightforward. Appraisal and rent schedule timing still matters, especially in competitive Wisconsin markets. At HomeAbroad, we can close your deal in as less as 27 days.

Scale Your Portfolio Faster

International real estate investors like DSCR lending because it creates a repeatable qualification approach across multiple properties. When you understand how rent, PITIA, and reserves will be evaluated, it becomes easier to screen deals before you write offers.

Foreign National Friendly

DSCR loan is one of the best mortgage options for foreign nationals, who often face friction with conventional underwriting. DSCR lending is commonly used to reduce that friction because the property performance drives the qualification logic.

Case Study: How John Secured a HomeAbraod DSCR Loan while Generating Positive Cash Flow

John, a South Africa–based investor, wanted to acquire a rental property in Green Bay but was unable to move forward with traditional US lenders. He worked with HomeAbroad to structure a DSCR loan that qualified the deal based on the property’s rental income rather than personal income or credit history.

The rental cash flow supported the full monthly payment and generated positive cash flow, allowing the loan to close smoothly. By focusing on the asset’s performance, John was able to add a Wisconsin rental to his portfolio using a financing structure built to scale.

Property Details:

Location: Green Bay Property Value: $261,478 Monthly Rental Income: $1,900

Loan Details:

Loan Amount: $196,109 Down Payment: 25% Interest Rate: 7.4% Loan Term: 30 years Monthly Mortgage (PITIA): $1,560

Director of Mortgage Sales, HomeAbroad | NMLS# 1231769

“What made this deal work was speed and structure. For foreign nationals, the fastest path is not trying to ‘look US-based,’ it’s presenting a clean rental story. When rent, expenses, and ownership costs are organized upfront, investors can buy confidently from abroad and scale without waiting years to establish local credit”

By using a DSCR loan, John was able to execute the purchase without building a US credit profile first, allowing him to move forward on timing rather than paperwork.

Wisconsin Rental Market Overview

Wisconsin offers a more balanced rental environment by US standards, where property prices and rental income tend to align more naturally than in higher-cost coastal states. This alignment gives investors greater flexibility to structure DSCR-backed deals around sustainable rent levels rather than relying on tight margins or aggressive assumptions.

As per our data, the key market statistics for 2025 are:

Median gross rent in Wisconsin: approximately $1,332/month

Median value of housing units: around $316,876

Median selected monthly owner costs with a mortgage: $1,652

Owner-occupied housing unit rate: 67%

Where We Lend DSCR Loans in Wisconsin

At HomeAbroad, we offer DSCR loans across Wisconsin, making it easier for foreign nationals to invest in cities with strong rental markets, such as Milwaukee, Madison, Green Bay, and more.

Here are a few cities in Wisconsin where we offer DSCR Loans.

Madison

Milwaukee

Green Bay

Kenosha

Appleton

Racine

Waukesha

Lake Geneva

Wisconsin Dells

Bayfield

Minocqua

La Crosse

Eagle River

Eau Claire

Janesville

Top Places to Invest in Wisconsin with a DSCR Loan

Wisconsin may not always make the front page for real estate investment, but savvy real estate investors know it’s one of the Midwest’s most dependable and rewarding markets. With affordable home prices, strong rental demand, and a mix of urban and vacation rental opportunities, the state offers fertile ground for both long-term and short-term rental strategies.

Director of Mortgage Sales, HomeAbroad | NMLS# 1231769

“What we see is steady demand tied to employers and universities, which makes rent projections more reliable. That reliability is what allows DSCR underwriting to stay clean from application through closing.”

Here are some of the top-performing cities in Wisconsin to consider for your DSCR loan investment:

The investment properties shown below are pulled from the HomeAbroad property-search platform and can change daily. Review each listing’s rent assumptions, cash flow, and DSCR inputs before you underwrite an offer.

City

Rental Type

Rental Yield

Wisconsin Dells

Short-Term

25.1%

Lake Geneva

Short-Term

23.6%

Eagle River

Short-Term

15.6%

Milwaukee

Long-Term

7.4%

Kenosha

Long-Term

7.3%

Wisconsin Dells: Tourism-Driven Market with Reliable STR Demand

Wisconsin Dells is one of the Midwest’s most established vacation markets, supported by year-round resorts, indoor waterparks, and consistent weekend travel from Chicago and Minneapolis.

Median Home Price: $286,744

Average Rent: $1,256/month

What this means for investors: Short-term rentals here benefit from dependable occupancy across seasons, not just summer peaks. Well-positioned properties with family-oriented features tend to maintain steady bookings, which supports predictable DSCR performance rather than one-off seasonal spikes.

Investment Properties Listed Today on Sale in Wisconsin Dells

Lake Geneva: Premium Weekend Rental Market with High-Spend Demand

Lake Geneva is a well-established getaway for Chicago-area travelers, known for lakefront homes, upscale dining, and year-round leisure activity.

Median Home Price: $393,756

Average Rent: $2,300/month

What this means for investors: This is a quality-over-quantity STR market. Properties with lake access, strong design, and walkability can command higher nightly rates, supporting solid DSCR performance even with moderate occupancy.

Investment Properties Listed Today on Sale in Lake Geneva

Eagle River: Seasonal STR Market Built on Outdoor Tourism

Eagle River sits in Wisconsin’s Northwoods and attracts travelers looking for cabins, lakes, fishing, and winter recreation.

Median Home Price: $356,838

Average Rent: $2,750

What this means for investors: This is a seasonal STR market where peak summer and winter demand drive the majority of revenue. Investors who plan for seasonality and target outdoor-focused guests can generate strong cash flow in a market with relatively low competition.

Investment Properties Listed Today on Sale in Eagle River

Milwaukee: Year-Round Urban Rental Market with Stable Demand

Milwaukee supports consistent short-term and mid-term rental demand driven by events, business travel, and lakefront tourism.

Median Home Price: $211,990

Average Rent: $1,331/month

What this means for investors: This is a market where operational efficiency matters. Well-located properties with clean turnover and flexible stay lengths tend to maintain steady occupancy, supporting predictable DSCR performance as long as local rental rules are followed.

Investment Properties Listed Today on Sale in Milwaukee

Kenosha: Hybrid Rental Market Backed by Commuters and Lakefront Demand

Kenosha sits between Milwaukee and Chicago, benefiting from commuter rail access, lakefront appeal, and a growing downtown.

Median Home Price: $260,177

Average Rent: $1,597

What this means for investors: Kenosha works well for flexible rental strategies. Properties in walkable or waterfront areas can attract a mix of short stays and mid-length tenants, creating steady occupancy that supports DSCR qualification through consistency rather than premium pricing.

Investment Properties Listed Today on Sale in Kenosha

Wisconsin Specific DSCR Underwriting Factors that Investors Overlook

Property Taxes and Post-Purchase Reassessments

Wisconsin assesses property taxes locally, and reassessments after a sale are common. We regularly see taxes reset higher than the seller’s historical bill, especially in markets like Milwaukee and Madison. When taxes are modeled conservatively upfront, DSCR outcomes remain stable instead of tightening late in the process.

Cold-Weather Operating Reality

Heating costs, snow removal, and winter maintenance are not optional expenses here. Older housing stock can carry higher utility and repair costs, which directly affect net rental income. Investors who factor realistic winter operating costs into underwriting tend to avoid cash-flow surprises after closing.

City-Level Short-Term Rental Rules

Wisconsin leaves STR regulation to municipalities. Some cities cap permits or restrict non-owner-occupied rentals. We often advise confirming local STR eligibility before relying on projected short-term income for DSCR qualification.

Director of Mortgage Sales, HomeAbroad | NMLS# 1231769

“When clients plan for taxes, winter operating costs, and long-term tenancy from day one, the market becomes very predictable. . That consistency makes it much easier to structure DSCR loans that hold up well beyond closing.”

Strategic & Future Considerations for Foreign Nationals Investing in Wisconsin

Wisconsin is emerging as a quiet performer for foreign national investors seeking long-term rental income with DSCR loans. With relatively low property prices, solid tenant demand in mid-sized cities, and infrastructure investment along key corridors, the state offers cash-flow-friendly opportunities. However, state-specific legal and economic factors must be considered to optimize risk and returns.

Here’s what global investors must consider when evaluating future-oriented opportunities across the state.

1. Urban Revitalization and Infrastructure Investment

Downtown redevelopment in cities like Milwaukee and Madison, combined with transit, waterfront, and mixed-use projects, continues to improve livability. Investors who enter near these corridors often benefit from gradual rent growth without relying on aggressive appreciation assumptions.

2. Rising Interest in Secondary and Tertiary Markets

As prices increase in major metros nationwide, more investors are moving into smaller Wisconsin cities where entry costs remain manageable. These markets often deliver cleaner DSCR outcomes because rent-to-price alignment is easier to maintain.

3. Climate and Operating Planning Matter More Over Time

Wisconsin properties require long-term planning around winter maintenance, energy efficiency, and aging housing stock. Investors who budget for these realities upfront tend to preserve cash flow and avoid erosion of DSCR over time.

Wisconsin DSCR Loan FAQs

Can foreign nationals apply for a DSCR loan in Wisconsin without US credit history?

Yes. HomeAbroad offers DSCR loans in Wisconsin for foreign nationals, qualifying the loan based on the property’s rental income rather than US income, tax returns, or credit history.

Do I need to live in the US to buy a rental property in Wisconsin?

No. HomeAbroad supports remote purchases and closings, allowing international investors to complete the entire DSCR loan process without being physically present in the US.

Can I buy a Wisconsin investment property through an LLC?

Yes. DSCR loans can be structured under a US-based LLC. HomeAbroad assists foreign nationals with LLC formation and ownership structuring to ensure the setup aligns with portfolio planning.

How long does it take to get a DSCR loan in Wisconsin?

At HomeAbroad, we streamline the application process to ensure a smooth experience from loan application to closing. We guarantee that the closing will happen within 30 days.

About the author:

Steven Glick is the Director of Mortgage Sales at HomeAbroad and has over a decade of experience in the mortgage industry. As a licensed mortgage originator (NMLS# 1231769), Steven brings deep expertise in loan processing, sales operations, and non-traditional mortgages.

* Scenario-based rate shown for illustrative purposes. Reflects current pricing available to qualified borrowers with strong credit, low loan-to-value, qualifying DSCR, and selected loan terms. Actual rates vary by borrower, property, and market conditions. Not a commitment to lend. Foreign national DSCR pricing may differ from U.S. borrower programs.

Wisconsin Investment Properties On Sale

Build wealth with HomeAbroad DSCR loans across Wisconsin ‘s top markets.

Our streamlined digital process gets you from application to funding faster than traditional lenders.

1

Get Pre-Qualified

Submit a quick online application. No credit pull required for initial quote.

⏱ 5 minutes

2

Submit Documents

Upload property details, lease agreements, and basic ID verification.

⏱ Same day

3

Property Appraisal

We order an appraisal and a rent schedule to confirm DSCR qualification.

⏱ 5–7 days

4

Close & Fund

Sign closing documents and receive your funds. Remote closing available.

⏱ 27 days total

Why Investors Choose HomeAbroad

DSCR Loan Experts

We focus on DSCR investor loans. Expect clear cash flow math, rent documentation, and underwriting that reflects how rental properties are evaluated.

Foreign National Mortgage Experts

No US credit? No problem. At HomeAbroad, our expert loan officers can still qualify you for a DSCR loan. We do not rely on US income or tax returns to underwrite your loan.

AI-Powered Property Search Platform

Our investment property search helps you shortlist rentals that fit DSCR qualification. Screen for rent strength, yield, and investor criteria before you write the offer.

End-to-End Support

We keep the process moving, from LLC formation to bank accounts, insurance to property management. Everything is handled by us so you can focus on growing your portfolio.

Why Choose Us

Built for Foreign Real Estate Investors

HomeAbroad is a one-stop shop for global investors, from finding properties to securing financing, setting up your LLC, opening a US bank account, and managing your portfolio.

🌍

Foreign National Mortgage Experts

No US credit history, income, or residency required. We've helped thousands of international real estate investors finance Wisconsin real estate.

🤖

AI–Powered Property Search

Our investment property search platform helps you discover high-yield rentals across Wisconsin using smart algorithms.

⌚

Fast Digital Process

Close in as fast as 27 days with our streamlined application, remote notarization [remote closing], and digital document signing.

🤝

500+ Expert Agents

Work with our network of experienced real estate agents who specialize in investment properties across Wisconsin.

Ready to Get Started?

Get your personalized rate quote in minutes. No credit pull, no obligation.

48

States We Lend In

27 Days

Average Close Time

500+

Partner Real Estate Agents

4.9 Star

Customer Rating

What Foreign Investors Say About Us

Real reviews from international investors who closed with HomeAbroad

★★★★★

“Quick response, reliable & trustworthy. HomeAbroad helped me find the perfect agent & purchase my investment property in Katy, TX. Would definitely recommend!”

RM

Rashmi Mayekar

Non-US Resident Investor • Property

★★★★★

“HomeAbroad was a game-changer! They helped me get mortgage financing and find an agent who understood my needs. I couldn’t be happier with their assistance.”

SP

Steve Papadakis

Newcomer on H1-B Visa

★★★★★

“Awesome experience in working with them. Very patient in understanding my needs as an investor and helped me with the correct loan product for me. I will recommend them and use them again.”

JB

John Bolla

Investor from New York, NY

★★★★★

“Jonet from HomeAbroad answered all my questions regarding specifics for work visa holders to purchase our first investment property in Tampa. Was patient and kind and also connect me with a real estate agent.”

Ok

Okissa

Purchased Investment Property in Tampa.

Pre-qualify for a DSCR Loan as an international investor

No U.S. credit history. No personal income verification. Qualify based on property’s rental income.