Editorial Integrity

Making informed real estate decisions starts with having the right knowledge. At HomeAbroad, we offer US mortgage products for foreign nationals & investors and have a network of 500+ expert HomeAbroad real estate agents to provide the expertise you need. Our content is written by licensed mortgage experts and seasoned real estate agents who share insights from their experience, helping thousands like you. Our strict editorial process ensures you receive reliable and accurate information.

Nigerian investors showed strong interest in US real estate, especially for rental income and dollar-denominated assets.

Many attendees assumed they would need to buy in cash. The webinar showed how financing can create another path.

DSCR loans stood out because the property’s rental income can help drive the loan review.

Cash-out refinance introduced a portfolio-building strategy, where equity from one US property may help support the next acquisition.

We joined REIGPlus on June 3 for a webinar built around a question many Nigerian investors face before buying US real estate: should they move enough capital to buy in cash, or can financing help them enter the market with a better plan?

The session, “Stop Paying All Cash: How Nigerian Investors Are Financing US Real Estate Deals,” brought Nigerian investors, real estate professionals, and US financing experts into one conversation. The conversation moved to the question investors came to answer: how can a Nigerian buyer purchase US real estate without assuming an all-cash purchase is the only route?

Interest in the US market is already strong. Nigerian investors are looking at the US for rental income and dollar-denominated assets. The larger need is a clearer buying path from abroad, especially when financing and ownership setup feel unfamiliar.

Table of Contents

HomeAbroad’s Foreign National Mortgage Expertise at the REIGPlus Webinar

HomeAbroad helps international buyers finance US real estate when a standard conventional loan does not fit. That was especially relevant for the Nigerian investors on the REIGPlus webinar, many of whom came in assuming they would need to buy in cash or qualify like a US borrower.

Steven walked the Nigerian investors through how that works in practice. An investor does not always need US credit history or US residency to secure financing. The loan structure depends on the borrower’s profile, the property, the documents available, and whether the rental income can support the debt.

That is where HomeAbroad’s expertise comes in. Most large banks are built around domestic borrowers, and they have strict requirements. On the other hand, HomeAbroad works with foreign national investors who may have income and assets outside the US, but still want a clear mortgage path for a US rental property.

We also walked through the advantage of 30-year mortgage structures in the US. A longer amortization period can reduce the required monthly payment, which affects whether a rental property can support the debt.

The Financing Questions Investors Asked

Attendees asked about down payments, rental income, and Atlanta real estate. They wanted to understand what it would take to move from interest to purchase.

Financing preserves capital that an all-cash purchase locks away. If an investor uses most of their available funds to buy one property outright, there may be less room for reserves or the next acquisition. With the right mortgage structure, a buyer can put part of the capital toward the purchase and keep liquidity available after closing.

DSCR loans drew close attention because they fit the way many attendees were thinking about US real estate: as an income-producing investment.

A DSCR loan, or debt service coverage ratio loan, is designed for rental property investors. The lender reviews whether the property’s rent can support the monthly property expense, including the mortgage payment, property taxes, homeowners insurance, and any applicable homeowners association dues.

Nigerian investors without US pay stubs or US credit history often benefit from this structure. With DSCR financing, the property’s income becomes central to the loan review.

The Q&A

One attendee asked about a buyer who was retiring and worried her income-to-loan ratio would prevent her from being approved. We explained that, for the loan structure being discussed, her employment status would not drive the review. The focus would be the rental income of the property and whether the property could support its expenses.

A concern that could have stopped the buyer at the starting line became a loan-structure question instead.

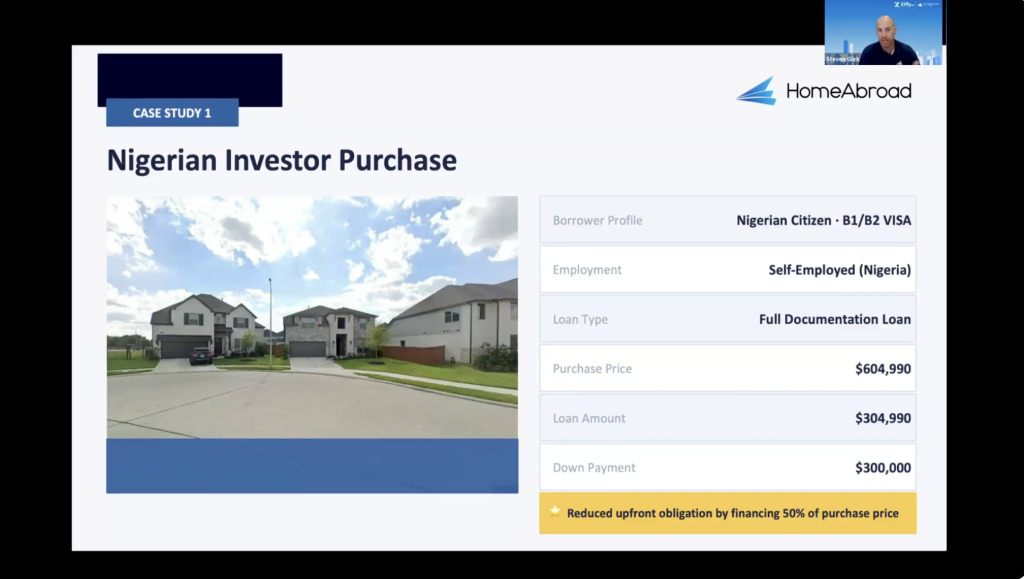

You can read the full case study here: Nigerian B1/B2 Visa Holder Secures a Texas Home

Another attendee asked whether a property would already have paying tenants at closing. The answer depends on the investment plan. Some buyers want a tenant-occupied property from day one. Others may prefer a vacant home they can renovate or prepare for a short-term rental strategy.

A separate question from an attendee in Lagos focused on buying US assets for children who are US citizens and studying in the US. The conversation moved into ownership planning and how families think about US real estate as a long-term asset. For some Nigerian investors, the goal is rental income today and a property their children can eventually use or inherit.

From First Purchase to Portfolio Planning

Nigerian investors want specific answers before they act. They want to know what the upfront cash requirement looks like, whether rental income can drive the loan review, and how a first US property can become a stepping stone to the next.

Cash-out refinance came up as a practical planning tool. As a property gains equity and the loan balance is paid down, an investor may be able to refinance and use part of that equity toward another purchase. The first property can then help fund the next one.

REIGPlus also addressed the support investors need around the transaction. Their team discussed property sourcing, entity setup, and post-closing management. For investors buying from Nigeria, the operating plan matters as much as the closing. The property still needs tenants, repairs, and day-to-day oversight.

Financing options are available for Nigerian investors, and certain rental-property loan programs may not require personal income verification or US credit history. Before committing all available cash to one US property, reviewing the financing options is worth doing first.

Ready to Explore US Real Estate Financing?

We help foreign national investors review mortgage options for US real estate purchases, including DSCR loans, full documentation loans, bridge loans, and fix-and-flip loans.

If you are planning to invest in US real estate from Nigeria, start with the financing conversation. The right loan structure can change the amount of capital you need upfront and how quickly you can move from one property to a larger investment plan.

![DSCR Loans Guide for Foreign Nationals: What It Is & How to Apply in [2026]](https://homeabroadinc.com/wp-content/uploads/2022/06/dscr-loan-guide-1.png)

![Can Foreigners Buy Property in the USA? [2026]](https://homeabroadinc.com/wp-content/uploads/2021/07/CanForeignersBuyinUS.jpg)