Editorial Integrity

Making informed real estate decisions starts with having the right knowledge. At HomeAbroad, we offer US mortgage products for foreign nationals & investors and have a network of 500+ expert HomeAbroad real estate agents to provide the expertise you need. Our content is written by licensed mortgage experts and seasoned real estate agents who share insights from their experience, helping thousands like you. Our strict editorial process ensures you receive reliable and accurate information.

Key Takeaways 1. HomeAbroad’s foreign national DSCR loans allow international investors to qualify based primarily on property cash flow rather than US income, tax returns, or domestic credit history. 2. Long-term rentals are usually the cleanest fit for DSCR underwriting because signed leases and Form 1007 market-rent analysis create stable, verifiable income for qualification. 3. The most common reasons foreign national DSCR files slow down are source-of-funds gaps, weak rental comparables, late LLC formation, and incomplete cross-border documentation. 4. Most foreign national long-term rental DSCR loans close in roughly 25–35 days when reserves, translations, lease documentation, and wire trails are prepared early in the process.

Table of Contents

Long-term rentals are the most common US real estate strategy for foreign nationals, and DSCR loans are the financing structure most investors use to buy them. The reason is simple: DSCR underwriting focuses on whether the property can support its own debt payments, not whether the borrower has US income, a Social Security Number, or an established US credit profile.

At HomeAbroad, we’ve structured 500+ DSCR loans for investors from 40+ countries. In practice, long-term rentals tend to produce the cleanest underwriting path because lease income and market rent are easier to verify than short-term rental projections or transitional property strategies.

This guide walks through how DSCR loans work for foreign nationals buying long-term rental properties and where international investors most commonly run into delays.

Why DSCR Loans Work for Foreign Nationals Buying Long-Term Rentals

The biggest challenge foreign investors face with traditional US mortgages is that conventional underwriting is built around domestic financial history. Without a US Social Security Number, US tax returns, or established US credit, many banks do not have a framework for evaluating the borrower.

HomeAbroad’s DSCR loans solve that problem by shifting the focus from the borrower’s personal income to the property’s rental income.

The distinction here is that DSCR underwriting asks a different question: does the property generate enough income to cover its debt payments? Instead of qualifying based on employment or tax returns, the loan is primarily qualified using rental income relative to monthly housing expenses.

That shift removes one of the biggest barriers foreign nationals face with conventional financing.

Long-term rentals fit this structure especially well because the income is stable and easier to verify. A signed 12-month lease provides documented in-place rent, while the appraiser’s Form 1007 establishes market rent using comparable rental properties in the area. Even when the property is vacant, the file still has a measurable income framework through the appraisal process.

What most investors realize quickly is that a long-term rental file with a signed lease usually moves through underwriting faster than a short-term rental file built around projected occupancy or seasonal income assumptions.

With HomeAbroad’s DSCR program, US credit, US tax returns, and US residency are not required. Properties can also be purchased through a US LLC, which is how many international investors choose to structure ownership.

Long-term rental DSCR structures also align well with long-term hold strategies commonly used by foreign investors. Investors should still understand FIRPTA rules before planning a future sale, since foreign owners of US real estate can face withholding requirements when exiting an investment property.

If you want a broader breakdown of program structures, see our guides on How DSCR Loans Work and Foreign National Mortgage Options.

Why Long-Term Rentals Fit DSCR Underwriting Better Than Other Strategies

Not every real estate strategy fits DSCR underwriting equally well. For foreign nationals, long-term rentals usually create the cleanest and most predictable approval path because the income is easier to document and verify.

Compared to short-term rentals like Airbnb or VRBO properties, long-term rentals have a simpler income structure. Short-term rental underwriting often depends on AirDNA projections or 12 months of platform history, and many programs apply seasonality adjustments to account for fluctuating occupancy. A long-term rental with a signed lease gives underwriting stable monthly income from day one, which generally produces a stronger and more predictable DSCR calculation.

The same applies when comparing DSCR to BRRRR or fix-and-flip strategies. DSCR loans are designed for stabilized, rent-ready properties. If a property is still under renovation or not yet rentable, it typically falls into a bridge or fix-and-flip structure first, with the investor refinancing into a DSCR loan after stabilization.

There is also a difference between residential and commercial underwriting. Residential 1–4 unit long-term rentals use a simpler DSCR framework based on rent versus PITIA. Properties with 5 or more units move into commercial underwriting, where qualification is based more heavily on NOI and commercial financial analysis.

In our experience, foreign national investors buying stabilized 1–4 unit long-term rentals usually close faster than short-term rental or rehab-heavy deals. Strong LTR files often close in roughly 25–30 days, while STR files can stretch closer to 35–45 days because the income takes longer to validate.

Jason Saylor,

Sr. Customer Loan Specialist, HomeAbroad | NMLS# 2594493

Who Qualifies: Foreign National Eligibility

DSCR loans are designed for both non-resident investors living outside the US and visa holders currently residing in the country.

For this type of financing, a foreign national generally falls into one of two categories. The first is a non-resident alien (NRA), meaning the borrower does not live in the United States and does not file US taxes as a resident. The second includes visa holders such as H1B, F1, O-1, L-1, and similar categories who live in the US but are not US citizens or green-card holders.

A valid passport is required and should remain valid for at least six months beyond the expected closing date. The borrower’s country of residence must also not fall under restricted or sanctioned jurisdictions.

One of the biggest differences with DSCR underwriting is that a US Social Security Number(SSN) is not required. An ITIN can be useful later for tax reporting and ownership structure, but it is not necessary to qualify for the loan itself.

For NRA borrowers, there is no requirement to live in the United States or hold a US visa. The closing process can typically be completed remotely through a mobile notary, international signing appointment, or US consulate process, depending on the transaction structure and state requirements.

Most foreign national DSCR loans are structured through a US LLC. In that setup, the LLC becomes the borrowing entity while the investor signs as the member or guarantor. Both single-member and multi-member LLC structures are commonly used.

To be clear, borrowers from sanctioned or restricted jurisdictions cannot proceed regardless of property strength or available assets. This is typically screened early in the process to avoid delays later in the transaction.

Jason Saylor,

Sr. Customer Loan Specialist, HomeAbroad | NMLS# 2594493

Long-Term Rental Property Requirements for DSCR Loans

HomeAbroad’s DSCR loans are designed for residential investment properties that can support stable long-term rental income. The strongest files are usually straightforward residential assets with clear rental comparables and minimal operational complexity.

Eligible property types typically include single-family residences (SFRs), 2–4 unit residential properties, warrantable condominiums, townhomes, and planned unit developments (PUDs). These property types fit the standard residential DSCR underwriting framework used for long-term rentals.

Certain property types fall outside that framework. Primary residences are not eligible because DSCR loans are business-purpose investment loans. Manufactured homes, raw land, mixed-use properties, and most rural properties are also commonly excluded or restricted depending on the market. Properties with 5 or more units generally move into commercial lending structures with a different DSCR calculation model.

The property must also be rent-ready at closing. That means it needs to be habitable and capable of supporting a tenant immediately. If the property still requires renovation before it can be leased, investors typically use a bridge or fix-and-flip structure first and refinance into DSCR after stabilization.

One thing that surprises investors is how often condo approvals depend on the HOA itself rather than the unit. A property can have strong rent numbers and appraisal value but still fail because the homeowners association does not meet warrantability requirements. Investor concentration, pending litigation, reserve funding, and HOA financial health are all reviewed during underwriting, which is why HOA documents are often requested early in the process.

For occupied properties, the lease must be fully executed, current, and consistent with the rent underwriting uses in the DSCR calculation. Month-to-month arrangements or verbal leases are generally treated as vacant during review.

HomeAbroad lends in most US states, though foreign national eligibility can vary by location and program structure, so confirming eligibility before going under contract is important.

DSCR Loan Requirements for Long-Term Rentals

Feature | Requirements |

|---|---|

DSCR Ratio | >= 1 for best terms, <1 eligible with a higher down payment. We provide DSCR Loans for foreign nationals with a DSCR ratio as low as 0.75, meaning you are eligible even if your rental covers just 75% of the mortgage. |

Credit Score | No U.S. Credit History Required |

Down Payment | 25% |

LTV Ratio | Purchase: Up to 75% |

Cash Reserves | 6 Months |

Property Use | Investment properties (residential and commercial) |

Loan Amount | >=$100K – $10M |

DSCR ratio is one of the most important qualifying metrics in the review process. A DSCR of 1.0 or higher generally receives the strongest terms because the property fully covers its monthly debt obligations.

We also offer foreign national DSCR loans with ratios below 1.0, which means the property may still qualify even if the rental income does not fully cover the mortgage payment. Lower-DSCR scenarios typically require stronger equity positions and reserves.

One thing investors should review carefully is prepayment penalty structure. Many foreign national DSCR loans include a prepayment penalty period, especially on lower-rate fixed options. The exact structure varies by program, but it can affect investors planning to refinance or sell within the first few years.

The overall structure is designed around predictable rental income, stable reserves, and sustainable debt coverage rather than US employment history or personal income qualification.

As of August 2026, HomeAbroad’s foreign national DSCR rates for long-term rental properties are currently ranging between 6.87% and 7.12% for well-qualified scenarios, depending on factors such as DSCR ratio, LTV, reserve strength, property type, and overall file structure. For the latest pricing updates and current rate scenarios, check our DSCR loan rates page. One downside to consider is that foreign national DSCR pricing is usually higher than conventional owner-occupied financing. The tradeoff is flexibility: qualification is based on property cash flow and reserves rather than US income, tax returns, or domestic credit history.

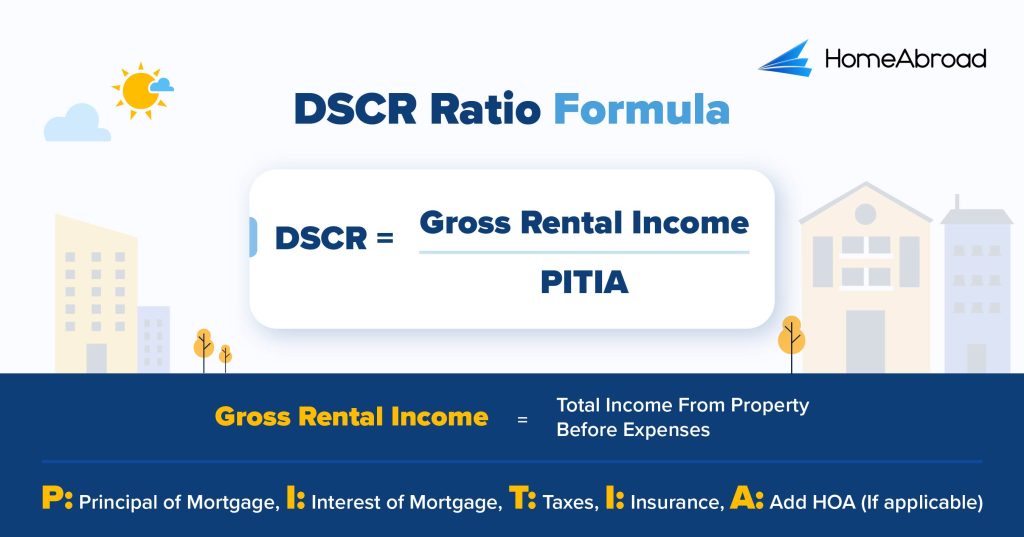

Rental Income Expectations: How DSCR Is Calculated for Long-Term Rentals

The DSCR Formula

DSCR loans for long-term rentals are qualified using the property’s rental income relative to its monthly housing expenses.

A DSCR of 1.0 means the property generates enough rental income to fully cover its monthly debt obligations. A ratio of 1.25 means the property produces a 25% cash-flow cushion above the monthly payment.

For foreign national long-term rental purchases, HomeAbroad’s minimum DSCR requirement is generally 1.0 for standard terms. Below that threshold, no-ratio options may still be available with adjusted pricing and tighter LTV requirements. These structures are commonly used by investors focused more on long-term appreciation or strategic market positioning than immediate monthly cash flow.

Qualifying Rent: The “Lower Of” Rule

For tenant-occupied long-term rentals, underwriting reviews the executed lease agreement to determine in-place rent.

For vacant properties, the appraiser completes Form 1007, also known as the Single-Family Comparable Rent Schedule, using nearby rental comparables to estimate market rent.

When both an executed lease and Form 1007 market rent are available, underwriting generally uses the lower of the two figures for qualification purposes.

For example:

- Lease rent: $2,500

- Form 1007 market rent: $2,000

- Qualifying rent used: $2,000

Or:

- Lease rent: $2,000

- Form 1007 market rent: $2,500

- Qualifying rent used: $2,000

What most guides don’t mention is that a strong lease usually cannot override a weak Form 1007. If the appraiser’s market-rent estimate comes in lower than expected, the DSCR calculation adjusts downward even if the tenant is currently paying more.

PITIA: What’s Included

PITIA includes:

- Principal

- Interest

- Property taxes

- Landlord insurance

- HOA dues, when applicable

Property taxes are often calculated using post-purchase reassessment estimates rather than the seller’s current tax bill.

Items such as property management fees, vacancy reserves, repairs, and utilities are generally not included in the PITIA calculation itself.

One thing that surprises investors is how heavily HOA dues can affect qualifying numbers. A $400 monthly HOA payment on a condo can materially reduce DSCR and push a marginal file below the 1.0 threshold.

A DSCR around 1.20 generally reflects positive cash flow above the property’s monthly debt obligations, which is typically considered a healthy range for long-term rental underwriting.

Lucas Hernandez,

Mortgage Loan Originator, HomeAbroad | NMLS# 2171747

How HomeAbroad Reviews Your File

Every foreign national long-term rental file is reviewed across four core areas: identity and eligibility, property income, assets and source of funds, and the property itself.

These reviews do not happen one after another based on when documents arrive. They run in parallel, and underwriting issues conditions wherever gaps appear.

1. Identity & Eligibility

Identity review is usually the first thing touched after intake because certain issues stop the file immediately.

Passport validity, visa or NRA status, and country eligibility are reviewed early in the process before appraisal and title costs are incurred. If there is a sanctions concern, restricted jurisdiction issue, or passport validity problem near the expected closing date, the file is flagged before underwriting progresses further.

2. Property Income

Property income review is not just about calculating DSCR. The lease and Form 1007 are reviewed against each other to test whether the rent is realistically supported by the market.

If lease rent comes in materially above nearby rental comparables, underwriting usually takes a closer look at the Form 1007 support before accepting the income figure. In some cases, stronger comparable rentals can support an appraisal rebuttal. In others, the file may need a lower loan amount or a no-ratio structure to move forward.

HOA dues are also built directly into PITIA during this review stage, which is why condo deals with otherwise strong rent can still fall below the qualifying threshold.

3. Assets, Reserves & Source of Funds

This is usually the most documentation-heavy part of a foreign national DSCR file.

In our experience, this is also where files slow down most often. Foreign-held assets are acceptable, but statements must be complete, translated into English if necessary, and supported with verifiable currency conversion. Large deposits must be sourced clearly, whether they come from salary, business income, property sales, gifts, or transfers between accounts.

Crypto proceeds generally need to be liquidated and seasoned before they can be used for closing funds or reserves. Wires from accounts that were not originally disclosed in the file are one of the fastest ways to trigger additional conditions.

This won’t work if funds cannot be clearly sourced and documented across every transfer step. Cross-border wire gaps are one of the fastest ways a file gets paused.

4. Property Review

The property review process runs in parallel with appraisal and title work.

For condos, HOA financials and warrantability review are usually started early rather than after appraisal returns. Too many investment-property transactions stall late in the process because the HOA fails reserve, litigation, or investor-concentration requirements even when the unit itself looks strong on paper.

Underwriting also confirms the property is rent-ready at closing and that landlord insurance is structured correctly with HomeAbroad listed as mortgagee.

5. Conditional Approval

Files almost never move directly to clear-to-close.

Conditional approval comes first, followed by a list of remaining items needed to finalize the file. These conditions commonly include updated bank statements, source-of-funds clarifications, certified translations, or insurance corrections.

A pattern we’ve noticed is that files rarely slow down because there are too many conditions. They slow down because conditions are answered in batches several days apart. Borrowers who respond quickly and completely usually move through underwriting much faster.

Lucas Hernandez,

Mortgage Loan Originator, HomeAbroad | NMLS# 2171747

Realistic Timeline: From Application to Funding

Most foreign national long-term rental DSCR files move from application to funding in roughly 25–35 days when documents are submitted quickly and conditions are answered without delays.

During the first few days, underwriting reviews identity documents, property information, and initial asset documentation while appraisal and title work are ordered. Once the appraisal is completed, the Form 1007 rent schedule and lease review are used to finalize the DSCR calculation and confirm qualifying income.

The middle portion of the process is usually focused on source-of-funds review, reserve verification, LLC documentation, and conditional approval. This is where certified translations, wire trails, and large-deposit explanations are most commonly requested.

The final stage involves clearing remaining conditions, completing final underwriting review, and scheduling closing. For borrowers outside the US, signing is typically handled through a mobile notary, remote closing process, or US consulate appointment depending on state requirements.

Foreign investors should also understand FIRPTA rules before selling a US property in the future. FIRPTA can require tax withholding on the sale of US real estate owned by foreign persons, so tax planning should be discussed with a qualified CPA or tax advisor.

In practice, most of the additional timeline compared to domestic DSCR loans comes from cross-border source-of-funds verification and document translation rather than the property review itself.

Where Foreign National LTR Files Actually Stall

Most foreign national long-term rental DSCR files do not stall because the deal is weak. They stall because one part of the documentation chain breaks late in the process.

The most common issue is source-of-funds documentation gaps, especially when a large deposit appears without a clear paper trail or funds arrive from an account that was never disclosed upfront. Another frequent problem is Form 1007 rent coming in below the lease amount, which lowers qualifying income and changes the DSCR calculation unexpectedly.

Newly signed leases can also create issues if there is limited seasoning or weak market-rent support behind the number. On condo transactions, insurance binder errors and HOA review delays are common friction points.

One issue investors consistently underestimate is LLC timing. Forming the entity after going under contract can easily add two to three weeks because title, insurance, and loan documents all need to be updated around the new ownership structure.

The honest answer is that most delays are preventable with sequencing. Form the LLC early, request certified translations before underwriting starts, and research rental comparables before agreeing to the purchase price.

Case Study: An Indian Investor Buying a US Long-Term Rental with a DSCR Loan

One of HomeAbroad’s India-based investors used a DSCR loan to purchase a single-family rental property in Memphis without relying on US credit history or personal income qualification.

Property Details

- Property Type: Single-family residence

- Purchase Price: $210,000

- Monthly Lease Rent: $1,800

- Rental Yield: 10.28%

- Down Payment: 25% ($52,500)

DSCR Loan Details

- Loan Program: HomeAbroad Foreign National DSCR Loan

- Loan Amount: $157,500

- Loan Term: 30-year fixed-rate

- Ownership Structure: US LLC

PITIA Breakdown

- Monthly Principal & Interest: $1,325

- Monthly Taxes & Insurance: $200

- HOA Dues: $0

Total PITIA came to $1,525 per month. The property had a signed long-term lease in place at $1,800 per month, and the Form 1007 market-rent analysis supported the lease amount during underwriting.

Using the qualifying rent of $1,800, the final DSCR calculation was:

- DSCR = $1,800 ÷ $1,525

- DSCR = 1.18

A DSCR of approximately 1.18 confirmed that the property generated enough rental income to comfortably cover its monthly debt obligations.

One of the biggest challenges in this transaction was coordinating India-based funds alongside US-based gift money while maintaining a clear source-of-funds trail. The issue was resolved by documenting every transfer step upfront and aligning the wire trail before final underwriting review.

This transaction is a strong example of how foreign investors can use DSCR financing to purchase cash-flowing US rental properties without US credit history or traditional income qualification.

Connect with HomeAbroad to explore your own DSCR loan options and start building your US real estate portfolio.

Get a Foreign National DSCR Loan for Long-Term Rentals

HomeAbroad has structured 500+ foreign national mortgages for investors from 40+ countries, with long-term rental DSCR loans representing one of the most common financing paths for international buyers.

If you’re planning to purchase a US rental property, getting pre-qualified early helps you understand your borrowing range, reserve requirements, DSCR eligibility, and documentation needs before you commit to a contract.

The process is fully remote and designed for foreign investors, with support for cross-border documentation, LLC structuring, source-of-funds review, and long-term rental financing in one place.

You can start by getting pre-qualified or connect directly with our DSCR loan specialist for more complex scenarios, including no-ratio files, multi-property strategies, or cross-border asset structures.

FAQs

Do foreign nationals need a US credit score for a DSCR loan?

No. HomeAbroad’s foreign national DSCR loans do not require a US credit score for qualification. The focus is primarily on the property’s rental income, down payment, reserves, and source-of-funds documentation rather than US employment or domestic credit history.

How much down payment is required for a foreign national long-term rental DSCR loan?

Most foreign national long-term rental DSCR loans require at least 25% down. Lower-leverage files with stronger DSCR ratios and reserve strength generally receive the best terms, while weaker cash-flow scenarios may require additional equity or lower LTV.

Can I close on a US rental property without coming to the United States?

Yes. Many foreign national DSCR transactions can be completed remotely. Depending on the state and closing structure, signing is typically handled through a mobile notary, remote online notarization process, or a US consulate appointment.

What DSCR ratio do I need to qualify on a long-term rental?

A DSCR of 1.0 or higher is generally the standard target for foreign national long-term rental loans. HomeAbroad also offers certain no-ratio options below 1.0 with adjusted pricing and tighter leverage requirements.

Can I use foreign bank accounts for the down payment and reserves?

Yes. Foreign-held accounts are acceptable for both down payment funds and reserves. Statements must be complete, translated into English if necessary, and supported with clear source-of-funds documentation and verifiable currency conversion.

How long does a DSCR loan typically take to close?

Foreign national DSCR loans usually take slightly longer than domestic investor loans because of cross-border source-of-funds verification, certified translations, and international documentation review. The exact timeline depends heavily on how quickly conditions and underwriting requests are completed.

![DSCR Loan Down Payment Requirements [2026]](https://homeabroadinc.com/wp-content/uploads/2023/01/DSCRDownPayment-scaled.jpg)