Editorial Integrity

Making informed real estate decisions starts with having the right knowledge. At HomeAbroad, we offer US mortgage products for foreign nationals & investors and have a network of 500+ expert HomeAbroad real estate agents to provide the expertise you need. Our content is written by licensed mortgage experts and seasoned real estate agents who share insights from their experience, helping thousands like you. Our strict editorial process ensures you receive reliable and accurate information.

Resident Indians can use the Liberalised Remittance Scheme (LRS) to invest up to $250,000 per financial year per individual in US real estate.

Non-Resident Indians and Overseas Citizens of India can invest using offshore funds, Non-Resident External accounts, and Foreign Currency Non-Resident accounts without Liberalised Remittance Scheme limits.

HomeAbroad’s DSCR loans allow eligible investors to qualify based on a property’s rental income rather than a US credit history.

FIRPTA withholding rules can affect how proceeds are received when a US property is sold.

US estate-tax exposure begins above the $60,000 non-resident exemption, making ownership structure and tax planning important considerations.

Can Indians Buy US Property?

Yes. Resident Indians, Non-Resident Indians (NRIs), and Overseas Citizens of India (OCIs) can all legally buy US investment property. What changes is how funds are transferred to the United States.

Resident Indians typically use the Liberalised Remittance Scheme (LRS), which currently allows up to $250,000 per financial year per individual for overseas investments. NRIs and OCIs generally use offshore funds and Non-Resident External (NRE) or Foreign Currency Non-Resident (FCNR) accounts.

Financing options, property ownership rights, and US tax rules are largely the same across all three investor profiles. This guide explains how to move capital, finance a purchase, and navigate the key US tax considerations when investing in US real estate.

Table of Contents

Why Indian Investors Are Buying US Property

Indian investors continue to play a significant role in the US real estate market. According to the latest National Association of REALTORS International Transactions Report, Indian buyers purchased approximately 4,700 US residential properties valued at $2.2 billion, placing India among the top foreign buyer groups in the United States.

Beyond owning a home, Indian investors use US real estate to earn rental income, hold dollar-denominated assets, and diversify wealth outside India.

In our experience working with Indian investors, investment goals often vary based on where the buyer lives. Resident Indians frequently focus on international diversification, while NRIs often use US real estate to expand their global investment portfolios. OCI investors commonly combine long-term wealth-building goals with broader international investment strategies.

Although the opportunity is the same, the process differs in three places: how capital moves, how funds are documented, and how the transaction is reported in India. This guide separates the rules and considerations for Resident Indians, NRIs, and OCIs so you can identify the path that applies to your situation before making an investment.

Know Your Profile: Resident Indian vs NRI vs OCI

Start by identifying which category applies to you. It determines how your money reaches the United States and which funding rules apply to your investment.

For US real estate purchases, Resident Indians, Non-Resident Indians (NRIs), and Overseas Citizens of India (OCIs) can all buy and finance US investment property. The key differences relate to how funds are transferred from India and certain tax-reporting requirements.

A common point of confusion is residency status. Under FEMA, residency is determined using foreign-exchange regulations and does not always match residency under the Income Tax Act. An individual may be treated differently under the two frameworks depending on their circumstances. Because capital movement for overseas investments falls under FEMA, investors should first identify their FEMA status before planning a US property purchase.

Profile | Primary Capital Source | Annual Transfer Limit |

|

|---|---|---|---|

Resident Indian | Indian resident bank accounts through LRS | Up to $250,000 per financial year per individual | Overseas investments must comply with FEMA and LRS reporting requirements |

NRI | Offshore funds, NRE accounts, FCNR accounts | No LRS limit | Cross-border reporting and repatriation considerations may apply |

OCI | Generally treated similarly to NRIs for investment purposes | No LRS limit | Similar reporting and ownership considerations as NRIs |

The important point is that eligibility to buy US property does not change across these categories. Resident Indians, NRIs, and OCIs can purchase the same types of US investment properties, access the same financing programs, and qualify for the same HomeAbroad mortgage solutions.

Moving Your Capital to the US (FEMA, Done Right)

Resident Indians: Using the Liberalised Remittance Scheme (LRS)

Resident Indians can use the Liberalised Remittance Scheme (LRS) to invest in overseas real estate, including US investment properties. Under current RBI guidelines, an individual can remit up to $250,000 per financial year (April–March) for permitted overseas investments.

An important advantage is that the limit applies per individual. For example, a married couple could potentially remit up to $500,000 per financial year by using each person’s individual LRS allowance, subject to applicable regulations and bank requirements.

Funds should be transferred through an authorized dealer (AD) bank using the appropriate purpose code and routed directly to the transaction’s title company or escrow account. Investors should avoid transferring funds through personal intermediary accounts unless specifically instructed by the parties involved in the transaction.

Tax Collected at Source (TCS) may apply to certain overseas remittances under current Indian tax rules. Because TCS thresholds and rates can change through annual budget updates, investors should confirm the applicable requirements at the time of the transaction.

For Resident Indians, the most common documentation requirements include proof of identity, bank records, remittance forms, and supporting documentation showing the purpose of the overseas investment.

NRIs: Offshore Funds, NRE Accounts, and FCNR Accounts

LRS applies to Resident Indians, not NRIs. This distinction is one of the most misunderstood aspects of cross-border investing.

NRIs commonly use offshore savings, NRE accounts, and FCNR accounts to fund US real estate purchases. Funds held in NRE and FCNR accounts are generally fully repatriable and are not subject to LRS limits.

NRO accounts follow different rules. Repatriation from an NRO account is generally limited to $1 million per financial year, subject to applicable documentation and compliance requirements, including Forms 15CA and 15CB where required.

From a financing perspective, lenders often prefer clear source-of-funds documentation. In our experience, NRE account statements frequently provide a straightforward audit trail when documenting down payment funds, reserves, and closing costs for a US mortgage transaction.

OCI Investors

For overseas real estate investments, OCI investors who maintain funds outside India generally follow the same funding and documentation framework used by NRIs when purchasing US real estate. OCI investors commonly use offshore funds, NRE accounts, FCNR accounts, and other permitted funding sources when purchasing US property.

The documentation process is typically similar to that used for NRI borrowers, particularly when establishing the source of funds for down payments, reserves, and closing costs.

Compliance Guardrails That Protect Your Transaction

Regardless of investor category, funds should move through authorized banking channels with a clear and documented audit trail.

Cash transactions, informal transfer arrangements, and undocumented funding sources can create significant compliance issues and delay a transaction. Documentation should clearly establish where funds originated, how they were transferred, and how they will be used in the purchase.

Jeff Larrabee

Senior Customer Loan Specialist, HomeAbroad

The biggest source-of-funds problems usually appear late in the process, not because the funds are ineligible, but because the documentation trail isn’t complete. The borrowers who close most smoothly are the ones who organize account statements, transfer records, and supporting documents before they start shopping for property.

HomeAbroad reviews source-of-funds documentation early in the financing process so potential issues can be identified before they affect underwriting or closing timelines.

Financing Without US Credit: Foreign-National Mortgages

A common misconception among Indian investors is that a US credit score is required to finance investment property in the United States. In reality, HomeAbroad’s foreign-national mortgage programs are specifically designed for international investors who may not have an established US credit history.

For rental-property investors, a DSCR loan is often the most popular option. Instead of qualifying based on personal income, tax returns, or employment history, qualification is based primarily on the property’s rental income and ability to cover its debt obligations. HomeAbroad’s DSCR loans are designed for investors purchasing income-producing real estate and can be a practical option for buyers who want a streamlined qualification process.

Investors who prefer to qualify using personal income may also consider full-documentation mortgage programs, which evaluate employment income, business income, assets, and other financial documentation.

Current foreign-national DSCR loan rates start from approximately 7.00%, although rates vary based on factors such as loan size, property type, leverage, reserves, and overall transaction strength.

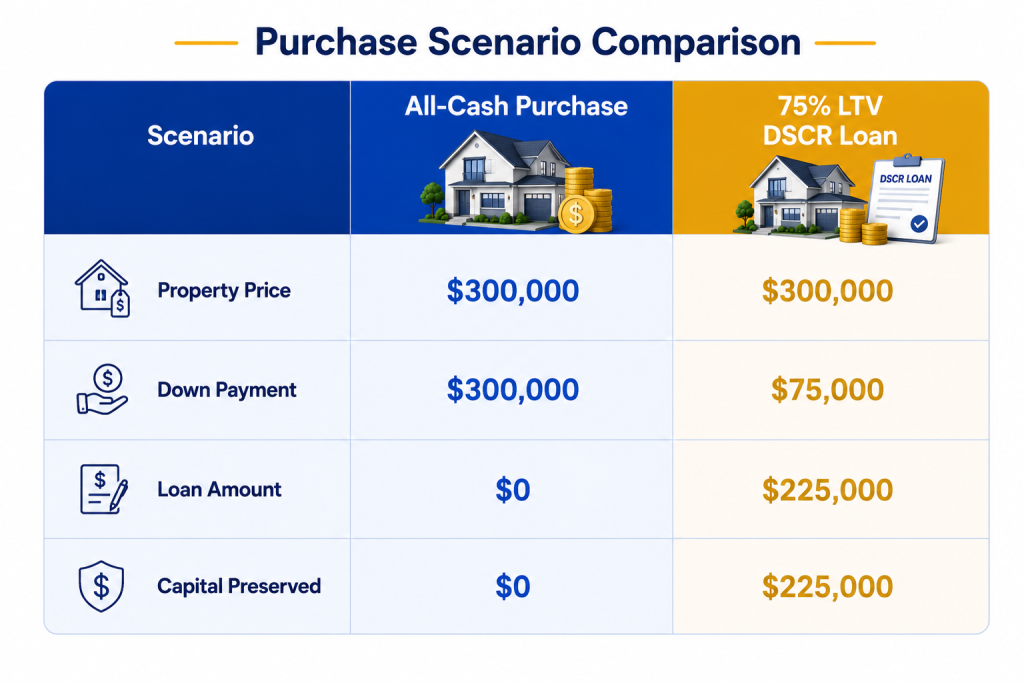

Why Financing Can Be More Efficient Than Paying All Cash

Many Indian investors have the ability to purchase US property outright. However, financing can improve capital efficiency by preserving liquidity and keeping additional capital available for future investments.

Example: $300,000 Rental Property

For a Resident Indian using LRS, preserving capital can be especially important. Rather than deploying an entire remittance allocation into a single property, financing may allow investors to maintain liquidity for reserves, future acquisitions, renovation projects, or portfolio diversification.

For Resident Indians, financing is often a capital-allocation decision as much as a mortgage decision. Investors who preserve liquidity frequently have more flexibility when evaluating future opportunities, especially when capital-transfer limits are part of the planning process.

Whether you’re a Resident Indian, NRI, or OCI investor, the right financing strategy depends on your investment goals, available capital, ownership structure, and long-term portfolio plans. HomeAbroad helps international investors evaluate DSCR loans, foreign-national mortgage programs, and financing structures designed for US investment properties.

Case Study: How an Indian Investor Bought a US Rental Property with a DSCR Loan

One HomeAbroad client, an Indian investor purchasing from India, wanted to acquire a US rental property without relying on a US credit history or tying up all of his available capital in a single investment.

The investor purchased a single-family rental property in Memphis, Tennessee, for $210,000 and used a HomeAbroad DSCR loan to finance the acquisition.

Deal Snapshot

Property | Financing |

|---|---|

Purchase Price: $210,000 | Loan Type: DSCR Loan |

Location: Memphis, TN | Loan Amount: $157,500 |

Property Type: Single-Family Rental | Down Payment: $52,500 (25%) |

Monthly Rent: $1,800 | DSCR: 1.18 |

Gross Rental Yield: 10.3% | Loan Term: 30-Year Fixed |

The property generated $1,800 in monthly rental income against a monthly PITIA payment of approximately $1,525, producing a DSCR of 1.18.

Why This Deal Matters

This transaction highlights several themes discussed throughout this guide:

- The investor qualified without a US credit history.

- The property’s rental income supported the DSCR qualification.

- Financing preserved capital that could be used for future investments instead of deploying the full purchase price upfront.

- The transaction was completed while the investor continued living in India.

Steven Glick, Director of Mortgage Sales at HomeAbroad, helped structure the financing and guide the investor through the cross-border purchase process.

Most Indian investors can buy US property. The harder part is sequencing the capital transfer, financing, and ownership structure correctly. This transaction shows how those pieces can come together in a single investment purchase.

US Tax Strategy for Indian Investors

Many guides explain how to buy US property. Far fewer explain what happens after you own it. For Indian investors, understanding the tax rules before investing can help avoid costly surprises later.

Rental Income: Why the Section 871(d) Election Matters

Rental income from US real estate is generally considered US-source income and is subject to US taxation. Most Indian investors will also need an Individual Taxpayer Identification Number (ITIN) to file US tax returns and report rental activity.

One of the most important tax elections available to foreign investors is the Section 871(d) election. Without it, rental income may be subject to a default 30% tax on gross income. By making the election, investors can generally be taxed on net rental income instead, allowing deductions for expenses such as mortgage interest, property taxes, insurance, repairs, property management fees, and depreciation.

In many cases, the ability to deduct expenses and depreciation produces a significantly better outcome than being taxed on gross rental receipts. This is one of the most commonly overlooked aspects of foreign real estate investing.

Selling the Property: Understanding FIRPTA

When a foreign investor sells US real estate, the Foreign Investment in Real Property Tax Act (FIRPTA) may require withholding at closing.

A common misconception is that FIRPTA is always a flat 15% withholding tax. In reality, FIRPTA withholding rules can fall into different categories depending on the transaction and the property’s intended use, with withholding rates that may be 0%, 10%, or 15%.

Another important point is that the India-US tax treaty does not eliminate FIRPTA withholding for individual non-resident alien sellers. FIRPTA rules still apply at closing even when treaty benefits may later affect the investor’s overall tax position.

US Estate Tax: The Risk Many Investors Miss

Estate-tax planning is frequently overlooked by foreign investors focused on acquisition and financing.

For US estate-tax purposes, non-resident aliens generally receive only a $60,000 exemption, compared with a substantially higher exemption available to US citizens and residents. US-situs assets above that threshold may be exposed to estate-tax rates of up to 40%.

Ownership structure can influence estate-tax exposure, but there is no universal solution. Investors should avoid assuming that holding property through an LLC automatically eliminates estate-tax risk. Estate-tax planning should be reviewed with qualified cross-border tax and legal advisors before purchasing property.

Jeff Larrabee

Senior Customer Loan Specialist, HomeAbroad

Many investors spend months evaluating purchase prices, financing options, and rental income projections but never look closely at exit costs or estate-tax exposure. Those are often the issues that create the biggest surprises years after the purchase is complete.

India-Side Reporting and Double-Taxation Relief

Indian investors may also have reporting obligations in India. Depending on their tax status, foreign assets may need to be disclosed in Schedule FA of the Indian Income Tax Return.

The India-US Double Taxation Avoidance Agreement (DTAA) helps reduce the risk of double taxation by allowing eligible taxpayers to claim foreign-tax credits for certain taxes paid in the United States. While the treaty can help prevent the same income from being taxed twice, investors should remember that it does not eliminate FIRPTA withholding requirements.

Because cross-border tax planning depends on an investor’s residency status, ownership structure, and overall financial situation, Indian investors should consult a qualified cross-border CPA or Chartered Accountant before making investment decisions.

Entity, ITIN, and US Banking Setup

Most Indian investors focus first on finding a property and arranging financing. However, a successful US real estate investment often depends on putting the right ownership and banking structure in place before closing.

The exact setup varies by investor, but three items commonly appear in the process:

Ownership Structure: Investors may purchase property in their personal name or through an entity such as an LLC. The right structure depends on factors such as liability considerations, financing strategy, estate planning, and long-term investment goals.

ITIN (Individual Taxpayer Identification Number): Foreign investors who earn rental income from US property generally need an ITIN to file US tax returns and manage ongoing tax-reporting obligations.

US Bank Account: While not always required before purchasing property, a US bank account can simplify rent collection, property-related expenses, mortgage payments, and ongoing portfolio management.

Sequence matters more than speed. The right ownership, tax, and banking structure depends on your investment goals and long-term plans. Investors planning multiple acquisitions should also consider how ownership, banking, and financing decisions may affect future portfolio growth.

Step-by-Step: From India to a Closed US Real Estate Investment

Buying US investment property from India is often simpler than investors expect when financing, capital planning, and documentation are addressed early. Here’s what the process typically looks like when working with HomeAbroad.

1. Confirm Your Investor Profile

The first step is determining whether you are a Resident Indian, NRI, or OCI. This affects how funds move to the United States and what documentation may be required during the transaction.

2. Build Your Capital Plan

Before looking at properties, we help investors evaluate available capital, financing options, reserve requirements, ownership structure, and any FEMA-related considerations that may affect the purchase.

3. Get Pre-Qualified

HomeAbroad reviews your investment goals and helps determine whether a DSCR loan or another foreign-national mortgage program is the best fit. This stage establishes your budget, financing structure, and documentation requirements before you begin making offers.

4. Identify a Property

Through HomeAbroad’s network of investor-focused agents, investors can evaluate rental properties, compare markets, and analyze potential returns before selecting a target property.

5. Submit an Offer

Once the right property is identified, an offer is submitted and negotiations begin. After the contract is executed, the financing process moves into underwriting.

6. Underwriting, Appraisal, and Rental Analysis

During underwriting, the property is reviewed, documentation is verified, and an appraisal is ordered. For DSCR loans, the appraiser’s rent analysis often becomes one of the most important parts of the file because it helps establish the property’s income profile for qualification purposes.

7. Close Remotely

After final approval, closing documents are prepared, funds are transferred, and ownership is recorded. Many HomeAbroad clients complete the entire financing and closing process remotely while continuing to live and work in India.

Common Mistakes Indian Investors Make

Even experienced investors can run into avoidable issues when buying US real estate across borders. These are some of the most common mistakes we see during the financing process.

1. Assuming LRS Applies to NRIs

LRS is designed for Resident Indians. NRIs and OCIs generally use offshore funds, NRE accounts, or FCNR accounts and are not subject to LRS remittance limits. Confusing the two can lead to unnecessary planning mistakes before a transaction even begins.

2. Using the Wrong Remittance Process

Funds should move through authorized banking channels with the correct purpose code and a clear documentation trail. Cash transactions, informal transfer arrangements, and incomplete records can create compliance issues and delay closing.

3. Ignoring FIRPTA Until It’s Time to Sell

Many investors focus heavily on acquisition costs and financing but give little thought to exit planning. FIRPTA withholding applies when foreign owners sell US real estate, and understanding the rules before purchasing can prevent surprises years later.

4. Overlooking US Estate-Tax Exposure

US estate-tax planning rarely receives the same attention as financing or property selection. However, non-resident investors generally receive only a $60,000 estate-tax exemption on US-situs assets, making ownership structure and long-term planning important considerations.

5. Using Zillow Rent Instead of Appraiser Rent

A property may appear to generate strong rental income based on listing estimates or online rent projections. For DSCR financing, however, qualification is typically based on the rent determined through the appraisal process. We regularly see investors overestimate a property’s financing potential because they rely on market estimates rather than the appraiser’s rent analysis.

Ready to Invest in US Real Estate?

The right investment structure depends on more than the property itself. Capital-transfer rules, financing options, ownership structure, tax planning, and long-term portfolio goals all play a role in the outcome of a US real estate investment.

Whether you’re a Resident Indian using LRS, an NRI investing through offshore funds, or an OCI building a global property portfolio, HomeAbroad helps investors navigate financing, capital planning, and cross-border real estate transactions.

Get pre-qualified today or request a personalized rate quote to explore your financing options and evaluate your next US investment opportunity.

Frequently Asked Questions

Can a Resident Indian buy US property under LRS?

Yes. Resident Indians can use the Liberalised Remittance Scheme (LRS) to invest in US real estate. Under current RBI rules, eligible individuals can remit up to $250,000 per financial year for permitted overseas investments, including property purchases.

Do NRIs have an LRS limit when buying US property?

No. LRS applies to Resident Indians, not NRIs. NRIs typically invest using offshore funds, NRE accounts, FCNR accounts, and other permitted funding sources that are not subject to LRS remittance limits.

Can OCI cardholders invest in US real estate?

Yes. OCI investors can legally purchase, own, finance, and sell US investment property. For FEMA purposes, OCI investors are generally treated similarly to NRIs when funding overseas investments.

Do I need a US credit score to qualify for a mortgage?

Not necessarily. HomeAbroad offers foreign-national mortgage programs that allow eligible investors to qualify without an established US credit history. DSCR loans, for example, primarily evaluate the property’s rental income rather than a borrower’s US credit profile.

How much money can I repatriate after selling a US property?

The answer depends on your investor profile and where the funds are held. NRIs using NRO account funds are generally subject to a $1 million repatriation limit per financial year, while NRE and FCNR funds follow different rules. Investors should review current RBI regulations and tax requirements before repatriating proceeds.

Is rental income taxed in both the United States and India?

US rental income is generally taxable in the United States. Indian tax residents may also have reporting obligations in India. The India-US Double Taxation Avoidance Agreement (DTAA) can help prevent double taxation by allowing eligible taxpayers to claim foreign-tax credits.

Does the India-US tax treaty eliminate FIRPTA withholding?

No. The India-US tax treaty does not eliminate FIRPTA withholding requirements for individual non-resident alien sellers. FIRPTA rules still apply when US real estate is sold, although treaty provisions may affect an investor’s overall tax position after filing the appropriate tax returns.

![Can Foreigners Buy Property in the USA? [2026]](https://homeabroadinc.com/wp-content/uploads/2021/07/CanForeignersBuyinUS.jpg)