Editorial Integrity

Making informed real estate decisions starts with having the right knowledge. At HomeAbroad, we offer US mortgage products for foreign nationals & investors and have a network of 500+ expert HomeAbroad real estate agents to provide the expertise you need. Our content is written by licensed mortgage experts and seasoned real estate agents who share insights from their experience, helping thousands like you. Our strict editorial process ensures you receive reliable and accurate information.

Start with financing before analyzing any property. Confirm your DSCR requirements, down payment, cash reserves, and ownership structure first.

Look beyond purchase price and rental income. Evaluate NOI, cap rate, cash flow, cash-on-cash return, and DSCR together before making an offer

Account for foreign investor costs. Include currency conversion, remote property management, FIRPTA (Foreign Investment in Real Property Tax Act), and tax planning in your analysis.

Use verified data, not assumptions. Base your calculations on market rents, realistic expenses, and financing terms rather than seller projections.

Table of Contents

Real estate deal analysis is the process of testing a property’s numbers against your financing terms and your investment goals before you make an offer.

For a foreign national investor, that process has three added variables most guides never mention: financing that runs through DSCR underwriting instead of a US income statement, currency movement between your home country and US dollars, and a tax event at exit that most cash flow spreadsheets ignore entirely.

This framework walks through all six, in the order they actually matter for a foreign investor, using one property carried through every step so you can see how the numbers connect. The deals that performed well shared one trait: the investor ran the numbers before falling in love with the property, not after.

Why Deal Analysis Works Differently for a Foreign National Investor

Every rental property analysis, regardless of who’s running it, comes down to the same five numbers: net operating income, cap rate, cash flow, cash-on-cash return, and DSCR. What changes for a foreign national investor is what feeds into those numbers and what happens after they’re calculated.

Three variables shift the math:

Financing structure. Most foreign national investors qualify through a DSCR loan, which evaluates the property’s income rather than the borrower’s US tax returns or credit history. That changes the down payment tier, the reserve requirement, and the loan-to-value ceiling that feed directly into your cash-on-cash calculation.

Currency exposure. Capital moving from a home-country account into a US down payment, and rental income moving the other direction, both cross a currency conversion. That conversion has a cost, and it isn’t a rounding error on a leveraged deal.

Exit tax treatment. A domestic investor’s deal analysis usually stops at annual cash flow. A foreign investor’s deal isn’t fully modeled until the withholding due at sale is accounted for, because that withholding is a tiered obligation, not a flat tax, and it can materially change what the investment actually returns.

This guide addresses each of these in sequence, alongside the standard metrics, so you can run one property through a single process instead of stitching together a domestic framework and a set of separate legal and tax notes.

Step 1: Confirm Your Financing Box Before You Analyze a Single Deal

Most rental property analysis frameworks put financing near the end, after the metrics are calculated. For a foreign national investor, that order should be reversed. Your down payment tier, reserve requirement, and DSCR minimum are set by your financing program before you ever run a number, and those figures directly determine what “cash invested” means in your cash-on-cash calculation later in this process.

Before running the numbers on any property, confirm these four financing requirements:

- HomeAbroad’s DSCR requirement is generally 1.0 or higher for the best terms. We also offer No-Ratio DSCR loans for eligible properties with a DSCR below 1.0.

- The minimum 25% down payment required for most foreign national DSCR loans.

- At least 6 months of post-closing cash reserves, based on the property’s monthly housing expenses.

- Whether you’re purchasing in your personal name or through a US LLC, since entity structure affects both financing terms and your later tax election

Steven Glick

Director of Mortgage Sales · HomeAbroad

Investors who get pre-qualified before they start evaluating properties move faster and waste less time on deals that were never going to close. The numbers on a property don’t mean much until you know what financing box you’re actually working inside.

Deal analysis checklist, before you run any property’s numbers:

- DSCR minimum confirmed for your program

- Down payment tier confirmed

- Reserve requirement confirmed

- Entity structure decided (personal name vs. LLC)

Once those four numbers are set, scope your property search to match them from the start. HomeAbroad’s AI-native investment property search platform lets you filter listings by price, projected cash flow, and target ROI, so you’re reviewing properties that already fit inside your financing box instead of running full analysis on ones that never had a chance to qualify.

We qualify DSCR loans using the appraiser’s market-rent analysis, not the online rent estimate the listing agent quoted or the number you calculated from a rental site. That distinction matters enough that it drives the entire next step.

Step 2: Verify Rental Income Like a Remote Investor

Most foreign national investors can’t drive by comparable rentals, knock on a neighbor’s door, or tour the unit in person before making an offer. That constraint changes how income verification has to work, and it’s the single most common place deal analysis breaks down.

Three sources give you a verified number instead of a guessed one:

The appraiser’s Form 1007 rent schedule. This is the same document we uses to qualify the loan, and it’s built from comparable rental properties the appraiser selects and adjusts, not from an automated online estimate.

A local property manager’s rent opinion. A property manager who leases units in that specific submarket can tell you what a unit actually rents for this month, not what an algorithm estimates it should rent for.

Two or three active comparable listings, pulled by your agent, matched for bedroom count, square footage, and condition within roughly half a mile of the subject property.

What we see often is investors underwriting a deal off a Zillow estimate that runs meaningfully higher than what the appraiser’s market-rent analysis eventually supports. That gap doesn’t just change your cash flow number on paper. It can change whether the loan qualifies at all.

where to verify market rent remotely

For initial screening:

- HomeAbroad’s AI-native investment property search platform shows a projected rent for every listing, which is useful for narrowing candidates quickly

For loan-qualifying verification:

- Appraiser Form 1007 rent schedule (the figure your loan is actually qualified against)

- Licensed local property manager’s rent opinion

- 2–3 active comparable listings from your agent

To be clear, a platform-projected rent is a screening estimate, not a substitute for the appraiser’s number. Use it to shortlist properties worth a full analysis, then verify the finalists against the sources above before you make an offer.

Once you have a verified rent figure, income is settled. The next step is making sure the expense side of the ledger is just as realistic.

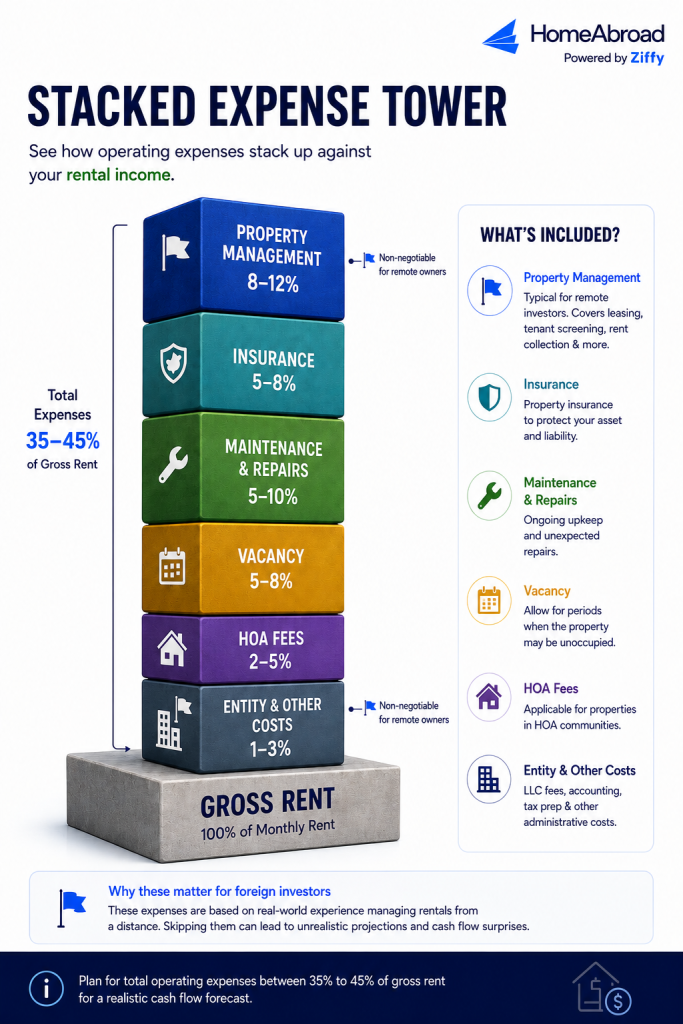

Step 3: Build the Real Expense Stack for a Remotely Managed Property

A rental property’s operating expenses look similar on paper whether the owner lives ten minutes away or ten time zones away. In practice, remote foreign ownership makes several line items larger or non-negotiable in ways that a generic expense worksheet won’t flag.

Expense category | Typical range | Why it’s different for a remote foreign owner |

|---|---|---|

Property management | 8–12% of gross rent | Most foreign investors rely on professional property management to handle leasing, rent collection, maintenance coordination, and tenant communication. |

Landlord Insurance | 5–8% of gross rent | Costs vary by property type, location, and coverage. Insurance is a recurring operating expense that should be included in every deal analysis. |

Maintenance & Repairs | 5–10% of gross rent | Budget for routine maintenance and unexpected repairs, since managing issues remotely usually requires local contractors. |

Vacancy Allowance | 5–8% of gross rent | Setting aside a vacancy reserve helps account for periods between tenants without overstating projected cash flow. |

HOA Fees | 2–5% of gross rent | HOA fees can affect both operating costs and rental restrictions, so review the governing documents before purchasing. |

Entity & Other Costs (If Using an LLC) | 1–3% of gross rent | Foreign investors purchasing through an LLC should also budget for registered agent fees, annual filings, accounting, and tax preparation. |

The most common underwriting mistake at this stage is treating property management as optional. It changes the entire expense stack if you assume you’ll handle leasing or maintenance calls yourself, and for an investor who isn’t in the country, that assumption rarely holds up past the first vacancy.

Step 4: Run the Deal Analysis: The Five Numbers That Decide the Deal

With verified income and a realistic expense stack in place, the deal analysis itself comes down to five calculations. This section shows the results using one running example property; for the full mechanics of each formula and how to sequence them, see our complete guide to cap rate, cash flow, and DSCR.

Example property: single-family rental, $340,000 purchase price, verified market rent of $2,650/month, financed with a DSCR loan at 25% down.

Metric | Formula | Result on this property |

|---|---|---|

Net operating income (NOI) | Gross rent − operating expenses | $21,600/year |

Cap rate | NOI (Net operating income) ÷ Purchase price | 6.4% |

Monthly cash flow | (Annual NOI − Annual Debt Service) ÷ 12 | $115/month |

Cash-on-cash return | Annual cash flow ÷ Total cash invested | 1.6% |

DSCR | Gross rent ÷ PITIA | 1.20 |

Two of these numbers are already adjusted for something a domestic framework wouldn’t need to consider: total cash invested includes this borrower’s foreign-national down payment tier, not a standard 20–25% domestic investor figure, and the DSCR is calculated against the actual PITIA a foreign-national loan program produced, not a generic rate assumption.

Running these five numbers by hand is worth doing at least once so you understand what feeds into each one that’s the point of walking through the math above. In practice, HomeAbroad’s AI-native investment property search platform calculates cap rate, cash flow, cash-on-cash return, and 5-year equity and appreciation projections automatically for any listed property, which is the faster path once you’re screening multiple candidates.

Step 5: Adjust for Currency, Tax Withholding, and Entity Structure

This is the step a domestic deal analysis framework doesn’t include, and it’s where a deal that looks solid on an annual cash flow basis can still produce a disappointing actual return.

Currency conversion. Capital moving from your home country into the US, and rental income moving back out if you repatriate it, both cross a conversion. Build in a 5–15% buffer on both legs, sized to your home currency’s typical volatility against the dollar, rather than assuming today’s exchange rate holds for the life of the investment.

Rental income tax treatment. Under Section 871(d), a foreign investor can elect to be taxed on net rental income rather than the default flat withholding on gross rental income. This is a US tax election, not a treaty benefit, and it has to be affirmatively made it doesn’t happen automatically. For the full mechanics of eligible deductions and how to file the election, see our guide to the Section 871(d) net election.

Exit withholding. This is the piece most cash flow models skip entirely. Under FIRPTA (Foreign Investment in Real Property Tax Act), withholding at sale is tiered 0%, 10%, or 15% of the gross sales price depending on the transaction never a flat rate, and generally not reduced by a tax treaty for an individual nonresident alien seller.

A deal analysis that only projects annual cash flow and never models this withholding is an incomplete analysis, because it’s modeling the holding period and ignoring the exit.

Investors who only model their annual cash flow are running half the deal. The number that actually determines your return includes what happens at the sale, and that’s exactly the part most spreadsheets leave out.

Step 6: Run the Go/No-Go Decision

A deal that clears every individual metric can still be the wrong deal if it doesn’t clear your own thresholds with margin. This step turns the five numbers and the adjustments above into a straightforward pass/fail check against your buy box, not a universal “good number” that applies to every investor.

Run these checks against the property:

- Does DSCR clear your lender’s minimum with a margin, not just meet it exactly?

- Does cash-on-cash return still clear your target after the currency conversion buffer is applied?

- Does the deal still work if verified rent came in at the low end of the appraiser’s range rather than the high end?

- Have you modeled the FIRPTA withholding tier that applies to your eventual exit, not just annual cash flow?

If you’re weighing more than one property, running this checklist gets easier when you can see the candidates side by side. Saving properties on HomeAbroad’s investment platform and comparing them on one dashboard makes it straightforward to hold each one to the same four checks rather than judging them from memory.

Dorian Adams-Walker

Mortgage Loan Originator,

HomeAbroad

NMLS #2442830The number that kills more foreign-national deals at underwriting than any other isn’t cap rate or purchase price, it’s DSCR calculated against the actual reserve and down payment requirement for this borrower, not a generic assumption the investor started with

walk away if:

- Cash-on-cash return falls below your target once the currency buffer is applied

- The deal only works using the seller’s claimed rent, not the appraiser’s verified figure

- You haven’t confirmed whether your exit falls into the 0%, 10%, or 15% FIRPTA withholding tier

How HomeAbroad Helped a Foreign National Analyze and Finance a US Rental Property

The following case study is based on a completed HomeAbroad transaction. Certain borrower details have been removed for privacy, but the investment process and financing structure reflect how HomeAbroad helps foreign nationals evaluate, finance, and close on US rental properties.

The investor wanted to purchase a long-term rental property in Indianapolis, Indiana, but first wanted to determine whether the property’s projected cash flow would support a DSCR loan.

Using HomeAbroad’s AI-native investment property search platform, the investor shortlisted properties based on projected rental income, cash flow, and estimated return rather than browsing listings based only on price. After comparing several opportunities, one single-family rental matched both the investor’s budget and financing goals.

Property snapshot

Property details | Property details |

|---|---|

Purchase price: $355,000 | Loan program: DSCR Loan |

Monthly rent: $2,980 | Down payment: 25% |

Property type: Single-family rental | Loan term: 30-year fixed |

Location: Indianapolis, Indiana | Closing: Completed remotely |

Deal analysis

- Monthly Market Rent: $2,980

- Monthly PITIA: $2,420

- DSCR: 1.23

- Projected Monthly Cash Flow: Approximately $260

With a DSCR of 1.23, the property’s rental income comfortably covered the monthly housing expense and qualified under HomeAbroad’s DSCR Loan Program. The investor completed the purchase with a 25% down payment while maintaining the required six months of post-closing cash reserves.

By analyzing the property’s rental income, operating costs, financing structure, and expected cash flow before making an offer, the investor moved into underwriting with a property that already aligned with HomeAbroad’s lending requirements. The transaction closed remotely, allowing the investor to add a US rental property without relying on US employment income or a US credit history.

Common Mistakes Foreign Investors Make When Analyzing US Deals

Most investment mistakes aren’t caused by choosing the wrong market. They happen because investors rely on assumptions instead of verified numbers. These are four issues HomeAbroad sees most often when reviewing foreign national investment property purchases.

Trusting the seller’s projected rent

The rent quoted in a listing or by the seller isn’t the figure HomeAbroad uses during underwriting. We qualify DSCR loans using the appraiser’s Form 1007 market-rent analysis, which can differ from online estimates or the seller’s projections.

Underestimating the cost of remote ownership

Foreign investors should budget for professional property management, maintenance reserves, and other recurring operating costs from the beginning. Treating these expenses as optional can make a property appear more profitable than it actually is.

Ignoring FIRPTA when planning the exit

Many investors focus only on annual rental income. A complete deal analysis should also consider FIRPTA withholding, which applies when foreign owners sell US real estate and can affect the investment’s overall return.

Underestimating currency exchange costs

Exchange-rate movements can affect both your initial investment and the income you repatriate over time. Building a reasonable currency buffer into your analysis provides a more realistic view of expected returns instead of relying on today’s exchange rate remaining unchanged.

Next Steps

Deal analysis for a foreign national investor starts with financing, not the property listing. If you haven’t confirmed your DSCR minimum, down payment tier, and reserve requirement yet, that’s the place to begin everything in this framework builds from those numbers. For a broader introduction to building a US rental portfolio as a foreign investor, see our complete guide to rental property investing.

Get pre-qualified for a DSCR loan to confirm your financing box before you run your next deal.

Frequently Asked Questions

How do foreign nationals analyze a US real estate investment deal?

Foreign nationals analyze US investment properties using the same core metrics as domestic investors, including net operating income (NOI), cap rate, cash flow, cash-on-cash return, and DSCR. They should also account for currency conversion, US tax obligations, financing requirements, and FIRPTA withholding when evaluating a property’s overall return.

What is the most important metric when analyzing a rental property?

No single metric tells the whole story. A good deal should be evaluated using several measures, including cash flow, cap rate, cash-on-cash return, and DSCR. For foreign national investors using a DSCR loan, the property’s Debt Service Coverage Ratio (DSCR) is particularly important because it affects financing eligibility.

Can I qualify for a DSCR loan if my property’s DSCR is below 1.0?

Yes. HomeAbroad generally offers its best terms on properties with a DSCR of 1.0 or higher, but eligible foreign national investors may also qualify through our No-Ratio DSCR Loan Program for properties with a DSCR below 1.0. These loans typically require a higher down payment.

How do I verify a property’s rental income before making an offer?

The most reliable way is to review the appraiser’s Form 1007 market rent schedule, which HomeAbroad uses during underwriting. You can also compare local rental listings and obtain a rent opinion from an experienced property manager before purchasing the property.

Should foreign investors include currency exchange in their deal analysis?

Yes. Exchange rate fluctuations can affect both the cost of transferring your down payment into the United States and the value of rental income when converting it back into your home currency. Including a currency buffer provides a more realistic estimate of your investment returns.