Editorial Integrity

Making informed real estate decisions starts with having the right knowledge. At HomeAbroad, we offer US mortgage products for foreign nationals & investors and have a network of 500+ expert HomeAbroad real estate agents to provide the expertise you need. Our content is written by licensed mortgage experts and seasoned real estate agents who share insights from their experience, helping thousands like you. Our strict editorial process ensures you receive reliable and accurate information.

UK citizens and residents can buy, finance, own, and sell US real estate without a visa, green card, Social Security Number, or US residency status.

Many UK investors qualify for foreign national mortgages and DSCR loans without a US credit history, allowing them to finance US rental properties instead of purchasing entirely with cash.

Cross-border tax planning matters. US rental income, FIRPTA withholding at sale, and potential US estate-tax exposure should be understood before investing.

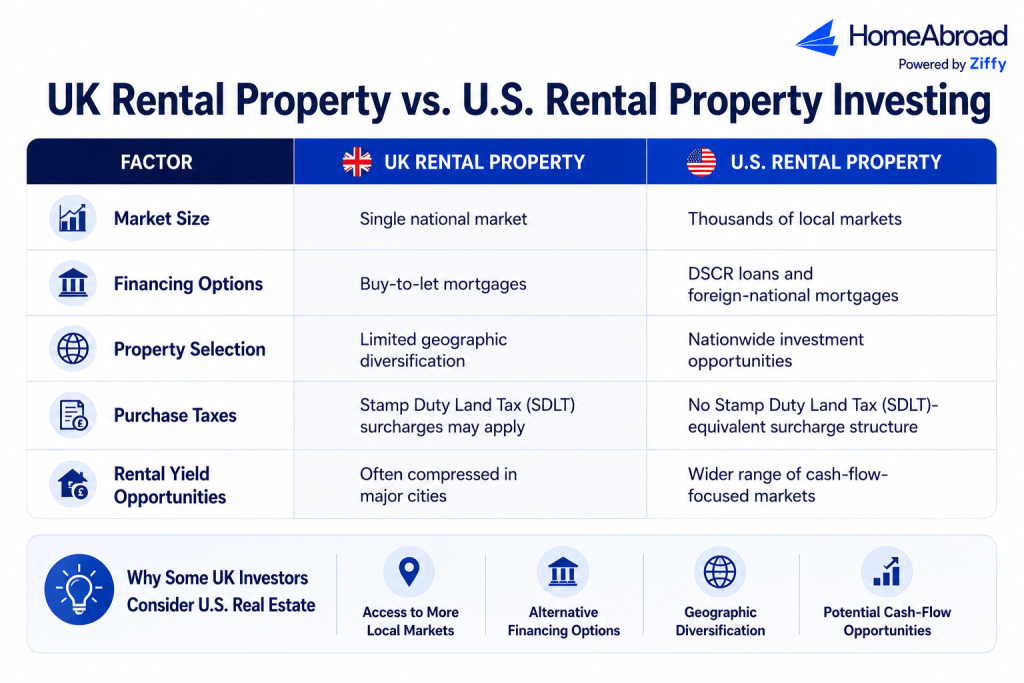

The US offers access to thousands of local real estate markets, flexible financing options, and rental-property opportunities that can complement a UK property portfolio.

The United States continues to attract real estate investors from around the world, and buyers from the United Kingdom remain an important part of that market. National Association of REALTORS data shows that UK buyers acquired approximately 3,100 US homes worth about $2 billion, reflecting continued interest in American real estate among British investors.

For many UK investors, the attraction comes down to access, scale, and flexibility. The US offers access to one of the world’s largest residential real estate markets, a wide range of investment opportunities, and financing structures that differ from those available in the UK. Investors can purchase rental properties in major metropolitan areas, growing Sun Belt markets, college towns, and vacation destinations, all within a single legal and financing framework.

At the same time, buying property in the United States from the UK involves questions that domestic investors never face. How do UK residents qualify for US mortgages? Can you buy through a company or LLC? How does FIRPTA affect foreign sellers? What role does the US-UK tax treaty play? And what should investors know about US estate-tax exposure before purchasing property?

This guide answers those questions and more. Whether you’re a UK citizen purchasing your first US rental property or an experienced investor looking to expand your portfolio, you’ll learn how financing works, how cross-border tax rules affect ownership, and what steps are involved in acquiring and managing US investment property from abroad.

Table of Contents

Can a UK Citizen or Resident Buy Property in the US?

Yes. UK citizens and UK residents can legally buy, own, rent, and sell property in the United States. You do not need a visa, green card, Social Security Number (SSN), or US residency status to purchase US real estate.

Whether you’re buying a single-family rental, vacation rental, condominium, or multifamily investment property, foreign ownership is generally permitted throughout the United States. UK investors can purchase property in their own name, through a limited company, or through a US LLC, depending on their investment goals and tax-planning considerations.

Buying US property does not require relocating to the United States or establishing a lengthy US financial history. Foreign nationals regularly purchase and finance US real estate while continuing to live and work abroad.

What You Legally Need

Although citizenship and residency are not barriers, investors should be prepared to provide documentation that supports the transaction.

In most cases, UK buyers will need:

- A valid passport or government-issued identification

- Proof of available funds for the down payment and closing costs

- A mortgage pre-qualification or proof of funds for cash purchases

- A US Individual Taxpayer Identification Number (ITIN) for certain tax filings and reporting requirements

An ITIN is not required before you begin searching for property, but many foreign investors obtain one during the purchase process because it may be needed for tax reporting and rental-property ownership.

Cash vs. Financing: Why Many UK Investors Start with Cash

According to the National Association of REALTORS, approximately 61% of UK buyers purchased US property with all cash. While cash purchases can simplify transactions, they are not the only option available to foreign investors.

Many UK investors initially assume financing will be difficult without a US credit history or Social Security Number. As a result, they often focus exclusively on cash purchases and overlook financing solutions designed specifically for international buyers.

Foreign-national mortgage programs and DSCR loans allow eligible investors to finance US rental property without following the traditional US borrower path. For investors purchasing income-producing real estate, the question is often not whether financing is available. The more important consideration is how financing fits into the broader investment strategy.

Why UK Investors Are Buying US Rental Property

For many British investors, buying property in the United States is not simply about owning real estate abroad. It is about accessing a different investment environment with a larger market, broader financing options, and, in some cases, stronger rental-income potential than traditional UK buy-to-let investments.

The US housing market contains thousands of local markets with different price points, rental-demand drivers, and investment profiles. Investors can choose between cash-flow-focused markets in the Midwest, population-growth markets across the Sun Belt, student-housing markets, and vacation-rental destinations.

Scale is another advantage. The United States remains one of the largest residential real estate markets in the world, providing investors with extensive transaction data, established financing options, and professional property-management infrastructure.

Currency diversification also plays a role. Rental income, property appreciation, and eventual sale proceeds are tied to the US economy and the US dollar, giving UK investors exposure beyond pound-denominated assets.

US Rental Yields vs. UK Buy-to-Let After the SDLT and Section 24 Squeeze

Many UK landlords have faced increasing pressure from higher acquisition costs and tax changes over the past decade.

Additional Stamp Duty Land Tax (SDLT) surcharges increase upfront acquisition costs, while Section 24 restrictions have reduced the value of mortgage-interest tax relief for many leveraged investors. Combined with rising financing costs, these changes have compressed returns in many UK buy-to-let markets.

By comparison, some US markets continue to offer higher rental income relative to property value.

For many UK investors, the decision is not about replacing UK property ownership. Instead, it is about adding exposure to a market that offers different financing options, rental-income dynamics, and long-term investment opportunities.

How UK Buyers Finance US Property

Many UK investors assume obtaining a US mortgage requires a Social Security Number, a US credit score, or years of financial history in the United States.

In reality, foreign-national mortgage programs are designed specifically for international buyers and regularly finance UK investors purchasing US rental property.

For many investors, financing is not simply a way to purchase property. It is a strategy for preserving capital, improving portfolio diversification, and maintaining liquidity for future investments.

DSCR Loans for UK Investors: How Qualification Works

For rental-property investors, DSCR loans are often the most straightforward financing option.

DSCR stands for Debt Service Coverage Ratio. Rather than focusing primarily on a borrower’s personal income, the loan is evaluated based on the property’s ability to generate rental income.

The calculation is simple:

DSCR = Monthly Rental Income ÷ Monthly PITIA

PITIA includes:

- Principal

- Interest

- Property Taxes

- Insurance

- Association dues (when applicable)

For example, one HomeAbroad-financed investment property generated $1,800 in monthly rent with monthly PITIA expenses of approximately $1,525.

DSCR = $1,800 ÷ $1,525 = 1.18

Because the property’s rental income exceeded its monthly housing expenses, it met the lender’s DSCR requirements and qualified for financing.

The advantage for UK investors is that DSCR loans do not require a US credit score, Social Security Number, W-2 income, or US tax returns. Qualification is centered on the property’s income potential and the overall strength of the transaction.

Steven Glick

Director of Mortgage Sales · HomeAbroad

Many UK investors are surprised by how different foreign-national underwriting is from a traditional domestic mortgage. For rental-property purchases, we’re evaluating the property’s income profile, the investor’s reserves, source of funds, and overall transaction strength rather than looking for years of US credit history.

Down Payment, Rates, and Documentation

Most UK investors purchasing US rental property through a foreign-national mortgage program should expect a minimum down payment of approximately 25%, although requirements vary based on property type, loan size, and borrower profile.

Foreign-national mortgage rates are generally higher than conventional owner-occupied mortgage rates available to US residents. Rates vary with leverage, property type, reserves, and overall file strength.

For investors who do not qualify through a DSCR loan, a full-documentation mortgage program may also be available. These programs typically review income earned outside the United States and may consider international credit reports and other alternative documentation.

Common documentation requirements include:

- Passport and identification documents

- Proof of funds for down payment and reserves

- Recent bank statements

- Property purchase contract

- International credit report (when applicable)

- Documentation supporting foreign income for full-documentation programs

Remote Closing and Typical Timelines

Many UK investors never need to travel to the United States during the financing process.

Mortgage applications, underwriting reviews, document collection, and closing coordination can often be completed remotely. Depending on the state, investors may also be able to use remote notarization, power of attorney arrangements, or other closing options that reduce travel requirements.

While every transaction is different, a well-prepared foreign-national mortgage file can often move from application to closing in approximately 30 days.

The most common delays are not related to underwriting. In our experience, they usually involve source-of-funds documentation, international transfers, incomplete paperwork, or last-minute changes to ownership structures.

Get Pre-Qualified as a UK Investor

Before searching for properties, it is helpful to understand how much financing may be available and which mortgage program best fits your investment strategy.

HomeAbroad helps UK investors evaluate foreign-national mortgage options, and financing structures for US rental properties. A pre-qualification review can identify expected down-payment requirements, documentation needs, reserve requirements, and potential loan options before you make an offer.

For many investors, understanding financing early makes it easier to evaluate opportunities, compare markets, and move quickly when the right property becomes available.

The Cross-Border Tax Picture for UK Investors

For UK investors, tax planning is one of the most important parts of a successful US real estate investment. Rental income, property sales, and estate planning all involve rules that operate across two countries.

The key is understanding how US taxation, UK taxation, and cross-border reporting interact before purchasing a property.

Every UK investor should understand three areas:

- How US rental income is taxed

- How FIRPTA applies when selling US property

- How US estate-tax rules may affect long-term ownership

US Rental Income and the Section 871(d) Election

Rental income generated from US property is generally considered US-source income and is subject to US taxation.

By default, foreign investors can be subject to a 30% tax on gross rental income. That means tax may apply before accounting for mortgage interest, property taxes, insurance, repairs, depreciation, and other ownership expenses.

Many experienced foreign investors instead elect to treat rental income as Effectively Connected Income (ECI) under Section 871(d) of the Internal Revenue Code.

This election allows rental income to be taxed on a net basis rather than a gross basis. Eligible investors can generally deduct expenses such as:

- Mortgage interest

- Property taxes

- Insurance

- Property management fees

- Maintenance expenses

- Depreciation

For leveraged investors, this creates an important connection between financing and tax planning. Mortgage interest and other ownership expenses may reduce taxable rental income, which is one reason many investors evaluate financing and tax strategy together rather than as separate decisions.

For a detailed explanation of how the election works, see our complete guide to the Section 871(d) election for foreign real estate investors.

FIRPTA and Selling US Property

When a foreign owner sells US real estate, the transaction may be subject to the Foreign Investment in Real Property Tax Act (FIRPTA).

FIRPTA withholding is often misunderstood, particularly because the applicable withholding rate depends on the transaction and available exemptions. Because FIRPTA affects proceeds at the time of sale, investors should understand the rules before planning an exit.

For a complete breakdown of FIRPTA withholding rates, exemptions, and filing requirements, see our dedicated FIRPTA guide.

What the US-UK Tax Treaty Does and Doesn’t Do

US rental income remains taxable in the United States, and the treaty does not eliminate FIRPTA withholding requirements when US real estate is sold.

Where the treaty can provide value is in helping reduce double taxation. UK taxpayers may be able to claim foreign-tax credits for certain US taxes paid, subject to UK tax rules and individual circumstances.

UK investors should also be aware of US estate-tax exposure. Non-US persons can face different estate-tax rules than US citizens, making ownership structure and long-term planning important considerations for larger portfolios.

Because tax outcomes depend on residency, ownership structure, financing arrangements, and individual circumstances, investors should consult qualified cross-border tax professionals before making decisions based on tax treatment alone.

FIRPTA: What UK Sellers Withhold When They Sell

Many UK investors spend considerable time planning how to buy US property but give far less attention to what happens when they eventually sell it.

When a UK investor sells US real estate, the transaction may be subject to the Foreign Investment in Real Property Tax Act (FIRPTA), which can require withholding at closing.

FIRPTA withholding is not always 15%. Depending on the transaction, withholding may be:

- 0% in certain exempt transactions

- 10% for some qualifying purchases

- 15% under the standard withholding rules

The applicable withholding rate depends on factors such as the property’s intended use, transaction value, and eligibility for specific exemptions.

FIRPTA withholding is separate from the seller’s final US tax liability. The amount withheld at closing acts as a prepayment, and the actual tax owed is determined when the appropriate US tax returns are filed.

What FIRPTA Doesn’t Change

Two areas frequently create confusion for UK investors.

First, the US-UK tax treaty does not eliminate FIRPTA withholding requirements. While treaty provisions may help address double taxation through foreign-tax-credit mechanisms, they do not exempt UK investors from FIRPTA at the time of sale.

Second, a 1031 exchange does not automatically eliminate FIRPTA obligations. Investors considering an exchange strategy should evaluate FIRPTA implications separately from the exchange itself.

FIRPTA Withholding Certificates

In some situations, foreign sellers may apply for a FIRPTA withholding certificate from the IRS.

A withholding certificate can potentially reduce or adjust the amount withheld at closing when the standard withholding amount significantly exceeds the seller’s expected tax liability.

Because processing times and eligibility requirements vary, investors should evaluate this option well before listing a property for sale.

Many foreign investors focus on acquisition financing and rental income but don’t start planning for FIRPTA until they’re already under contract to sell. The investors who experience the fewest surprises usually begin reviewing their exit strategy months before the property reaches the market.

FIRPTA planning becomes significantly easier when ownership structure, tax reporting, and sale objectives are considered early in the investment lifecycle rather than at the closing table.

For a detailed breakdown of FIRPTA withholding rates, exemptions, withholding certificates, and filing requirements, see our complete FIRPTA guide for foreign property sellers.

US Estate Tax and the US-UK Estate Tax Treaty

For many UK investors, estate tax receives far less attention than financing, rental income, or FIRPTA. Yet for larger portfolios, it can become one of the most significant long-term planning considerations.

Under current US rules, non-resident non-citizens generally receive a US estate-tax exemption of only $60,000 for US-situs assets. This is substantially lower than the multi-million-dollar estate-tax exemption available to US citizens and residents.

For a UK investor who owns US real estate directly, this distinction matters. If the value of US-situs assets exceeds the available exemption, part of the estate may be subject to US estate tax upon death.

How the US-UK Estate Tax Treaty Can Help

Fortunately, UK investors may have access to planning opportunities that are unavailable to many other foreign investors.

The United States and the United Kingdom maintain an estate and gift tax treaty that can, in certain circumstances, provide UK-domiciled individuals with a prorated share of the US unified credit. This can result in significantly greater estate-tax protection than the standard $60,000 exemption available under domestic US law alone.

The exact benefit depends on several factors, including:

- UK domicile status

- Worldwide asset values

- The proportion of assets located in the United States

- Estate structure and ownership arrangements

Because these calculations are highly individualized, investors should avoid assuming they are automatically limited to the $60,000 exemption or automatically entitled to treaty benefits.

The relief available under the US-UK Estate and Gift Tax Treaty depends on an investor’s domicile status, worldwide estate value, and the proportion of assets located in the United States.

Ownership Structure Matters

Estate-tax planning is one reason many international investors evaluate ownership structures before purchasing property.

Depending on an investor’s goals, property may be held directly, through a US LLC, through a foreign entity, or through another ownership structure. Each approach involves different legal, tax, financing, and administrative considerations.

An LLC can serve important business and liability purposes, but estate-tax treatment depends on the overall ownership structure and underlying facts rather than the existence of an LLC alone.

Planning Before You Buy

Estate-tax planning is often easiest before a property is acquired rather than after a portfolio has grown.

Investors considering larger acquisitions, multiple-property portfolios, or long-term US real estate holdings should discuss estate-tax implications with qualified cross-border tax and legal professionals. A structure that works well for financing, asset protection, and tax reporting today may create different estate-planning considerations years later.

For investors building larger US portfolios, estate-tax planning deserves the same attention as financing, cash flow, and property selection. A conversation with a qualified cross-border tax advisor can help determine whether treaty benefits, ownership structures, or other planning strategies are appropriate for your circumstances.

Step-by-Step: How a UK Investor Buys a US Rental Property

Buying US real estate from the UK is often more straightforward than many investors expect. While every transaction is different, most successful purchases follow the same general path from market selection to closing.

HomeAbroad helps UK investors navigate each stage of the process, from financing and property acquisition to ownership setup and post-closing support.

Step 1: Choose Your Target Market and Investment Budget

The first step is determining where you want to invest and what type of property fits your goals.

Some investors prioritize cash flow, while others focus on appreciation, diversification, or a combination of both. Markets in Florida, Texas, Arizona, Georgia, Tennessee, and other investor-friendly states often attract UK buyers because of their rental demand, population growth, and property-price-to-rent ratios.

Many investors begin this process using HomeAbroad’s AI-native investment property search platform, which helps identify US properties based on rental income potential, projected cash flow, financing scenarios, and investment objectives. Rather than manually screening hundreds of listings, investors can evaluate opportunities using investment-focused metrics from the start.

Before searching for properties, establish a realistic budget that includes:

- Down payment requirements

- Closing costs

- Cash reserves

- Property taxes

- Insurance

- Property-management costs

The goal is to identify markets that align with your investment objectives before evaluating individual properties.

Step 2: Get Pre-Qualified for Financing

Many investors begin looking at properties before understanding how much financing is available to them.

A pre-qualification review helps determine:

- Available loan programs

- Estimated purchasing power

- Expected down payment requirements

- Reserve requirements

- Documentation needs

For rental-property investors, this stage often includes evaluating whether a DSCR loan or a full-documentation foreign-national mortgage is the better fit.

HomeAbroad reviews financing options early so investors can evaluate opportunities with a clear understanding of budget and loan eligibility before making an offer.

The investors who move most efficiently are usually the ones who address financing first. Once financing parameters are clear, it’s much easier to evaluate properties, submit competitive offers, and avoid delays later in the process.

Pro Tip: Investors who obtain financing guidance before beginning their property search often identify opportunities more quickly because they already understand their purchasing range and documentation requirements.

Step 3: Work with an Investor-Focused Real Estate Agent

Once financing parameters are established, the next step is identifying properties that meet your investment criteria.

Through HomeAbroad’s team of investor-focused real estate professionals and Certified International Property Specialists (CIPS), UK investors can access local market expertise across the United States.

At this stage, investors typically evaluate:

- Rental demand

- Comparable rents

- Vacancy trends

- Neighborhood fundamentals

- Property condition

- Exit potential

Rather than focusing solely on purchase price, successful investors evaluate whether a property’s income profile supports their long-term strategy.

Step 4: Submit an Offer and Complete Due Diligence

After identifying a property, the purchase process moves into negotiation and due diligence.

During this period, investors review:

- Property inspections

- Title reports

- Insurance requirements

- Existing leases (if applicable)

- Property condition

- Financial assumptions

This stage is designed to verify that the property performs as expected before the transaction moves toward closing.

Step 5: Set Up Your ITIN and US Banking Relationships

Many foreign investors establish an Individual Taxpayer Identification Number (ITIN) and US banking relationships during the transaction process.

These items often support:

- Tax reporting

- Rental-income collection

- Property-related expenses

- Ongoing portfolio management

HomeAbroad can help coordinate these steps through our concierge and investor-support services, reducing friction for overseas buyers managing a transaction from abroad.

Step 6: Underwriting, Appraisal, and Final Loan Approval

Once the mortgage application is submitted, the loan file moves through underwriting.

For DSCR loans, the property itself becomes a major part of the review process. Rental-income analysis, appraisal results, reserves, and source-of-funds documentation are all evaluated before final approval.

For UK investors, documentation is often the determining factor in how quickly a loan moves through underwriting. Bank statements, source-of-funds records, and international financial documents that are organized before submission typically result in a smoother review process.

Well-organized documentation at this stage can significantly reduce closing timelines.

Step 7: Close Remotely

Many UK investors complete most or all of the closing process without traveling to the United States.

Depending on the state and transaction structure, investors may use remote notarization, power-of-attorney arrangements, or other remote-closing options.

Closing documents are executed, funds are transferred, ownership is recorded, and the property officially becomes part of the investor’s portfolio.

Pro Tip: International wire transfers and source-of-funds verification often take longer than investors expect. Organizing these items early can help avoid last-minute closing delays.

Step 8: Complete Your Post-Close Tax Setup

The transaction does not end when the property closes.

After acquisition, investors should work with qualified tax professionals to establish the appropriate reporting structure for rental income and ongoing ownership.

For many UK investors, this includes evaluating the Section 871(d) election, which can allow rental income to be taxed on a net basis rather than being subject to withholding on gross rental income.

It is also a good time to review bookkeeping, property-management procedures, banking arrangements, and long-term ownership planning.

Post-closing decisions can influence both cash flow and tax efficiency. Establishing the right reporting structure, banking setup, and property-management processes from the beginning can make ongoing ownership significantly easier.

Common Mistakes UK Investors Make

Buying US property from the UK is relatively straightforward, but certain mistakes appear repeatedly in cross-border transactions. Most are avoidable with proper planning.

Mistake #1: Assuming FIRPTA Is Always a Flat 15%

Some investors only begin researching FIRPTA after accepting an offer on their property.

The result can be inaccurate net-proceeds estimates, unnecessary closing stress, and missed opportunities to explore withholding-certificate options before the transaction reaches the closing table.

Better approach: Understand the likely FIRPTA impact when you buy the property, not when you decide to sell it.

Mistake #2: Ignoring US Estate-Tax Exposure

A single rental property may not create a significant estate-planning concern. A growing portfolio can.

We’ve seen investors spend years optimizing financing and cash flow while never evaluating how US estate-tax rules apply to their holdings. Restructuring ownership after multiple acquisitions is often more complex and expensive than planning before the portfolio expands.

Better approach: Discuss ownership and estate-planning considerations before purchasing additional properties.

Mistake #3: Skipping the Section 871(d) Election

Some foreign investors collect rental income for years before learning that they could have elected net-income treatment under Section 871(d).

The cost is not usually a penalty. It’s the potential loss of tax efficiency from failing to deduct expenses such as mortgage interest, depreciation, property taxes, and property-management costs.

Better approach: Discuss tax elections with a qualified cross-border tax professional shortly after acquiring the property.

Mistake #4: Assuming All-Cash Is Always the Best Option

Many UK investors can qualify for foreign-national financing but never explore the option.

As a result, they commit substantially more capital to a single property than necessary and limit future purchasing flexibility.

Better approach: Compare both financing and all-cash scenarios before deciding how to structure an acquisition.

Mistake #5: Choosing the Wrong Ownership Structure

Ownership structures that work for domestic US investors are not always appropriate for foreign investors.

We’ve encountered buyers who created entities before speaking with lenders, only to discover later that financing requirements, tax considerations, or long-term ownership goals pointed them toward a different structure.

Better approach: Evaluate financing, tax, and ownership considerations together before forming entities.

Mistake #6: Treating Currency Conversion as an Afterthought

A property purchase can take weeks or months to complete. Exchange-rate movements during that period can materially affect acquisition costs, down-payment amounts, and projected returns.

The strongest cross-border investment plans account for more than the property itself. Financing, ownership structure, tax planning, and currency movement all influence the outcome

Small decisions made before an offer is submitted can have a larger impact than many investors expect.

Case Study: How a UK Buyer Financed a Florida Property Without US Credit

A recent HomeAbroad transaction illustrates how UK buyers can finance US property even without a US credit history, Social Security Number, or US-based income.

The borrower, a UK resident, purchased a single-family property in Edgewater, Florida, for $292,000 using HomeAbroad’s foreign national mortgage program. The buyer made a 30% down payment and secured a $204,400 loan through a 30-year fixed-rate Non-QM full-documentation mortgage designed for international borrowers.

The financing structure behind this purchase illustrates how foreign-national mortgage programs can help UK buyers qualify for US property without traditional US credit requirements. Like many UK buyers, the borrower had no US credit score, no US tax returns, and no US employment income. Instead, the loan was underwritten using verified UK financial documentation, including income records and bank statements from the United Kingdom.

Deal Snapshot

Property | Financing |

|---|---|

Location: Edgewater, Florida | Loan Type: Foreign National Full-Doc Mortgage |

Property Type: Single-Family Residence | Loan Amount: $204,400 |

Purchase Price: $292,000 | Down Payment: 30% |

Borrower Location: United Kingdom | Loan Term: 30-Year Fixed |

Closing Timeline: About 30 Days | No US Credit History Required |

Because documentation was organized early and aligned with underwriting requirements before submission, the loan moved efficiently through review and closed within approximately one month.

This transaction highlights a reality many UK investors discover during the financing process: a lack of US credit history does not automatically prevent property ownership. The more important factors are documenting income, assets, reserves, and source of funds in a format that satisfies foreign-national underwriting guidelines.

This transaction closed in approximately 30 days using UK income documentation and a foreign-national mortgage program. It also demonstrates that a lack of US credit history does not automatically prevent financing when the borrower can document income, assets, and source of funds in a format that satisfies underwriting requirements.

Next Steps: Financing Your US Investment Property from the UK

By now, you should have a clear understanding of how UK investors finance, own, and manage US real estate, along with the key tax and ownership considerations that come with cross-border investing.

The next step is applying those concepts to your own investment goals.

That starts with determining how much capital you want to deploy, which financing strategy best fits your situation, and which markets align with your investment objectives. Financing, ownership structure, tax planning, and long-term portfolio strategy are closely connected, making it helpful to evaluate them together rather than in isolation.

Get Pre-Qualified as a UK Investor

HomeAbroad helps UK investors finance US real estate through foreign national mortgage programs, DSCR loans, and other investment-property financing solutions.

A pre-qualification review can help you:

- Understand available loan options

- Estimate down-payment requirements

- Review documentation requirements

- Evaluate financing scenarios before making an offer

- Identify potential issues early in the process

Every successful investment starts with a plan. Connect with HomeAbroad today to review your financing options, understand your purchasing power, and move forward with confidence.

Frequently Asked Questions:

Can a UK citizen get a US mortgage?

Yes. UK citizens can qualify for US mortgages through foreign national loan programs designed for international buyers. Depending on the property and borrower profile, financing options may include DSCR loans and full-documentation foreign national mortgages.

Do I need a US credit score to buy property in the United States?

No. Many foreign national mortgage programs do not require a US credit score. Lenders may review international credit reports, foreign income documentation, bank statements, reserves, and source-of-funds documentation instead.

How is my US rental income taxed in the UK?

US rental income is generally taxable in the United States because the property is located there. UK taxpayers may also have UK reporting obligations. In many cases, the US-UK tax treaty helps prevent double taxation through foreign-tax-credit mechanisms, but investors should consult a qualified cross-border tax professional regarding their specific situation.

Does buying property in the US give you residency?

Unfortunately, buying property in the US does not qualify an individual for residency. However, the EB-5 visa program offers a pathway to a green card through real estate investment, provided certain criteria are met.

How long can I stay in the United States if I buy property there?

Buying property does not grant US residency or immigration benefits. The amount of time you can spend in the United States depends on your visa status, citizenship, and applicable immigration rules, not on property ownership.

Can I buy US property through a UK company?

Potentially, yes. Some investors purchase property through a company or other ownership structure for tax, liability, or estate-planning reasons. However, financing availability, tax treatment, reporting requirements, and long-term planning considerations can vary significantly. Professional legal and tax advice is recommended before choosing an ownership structure.

Is it cheaper to buy property in the US than in the UK?

That depends on the market. Some US cities offer lower purchase prices relative to rental income than many UK markets, while others are comparable to major UK metropolitan areas. Investors should evaluate property taxes, insurance costs, financing terms, management expenses, and expected rental income rather than comparing purchase prices alone.

Can I complete a US property purchase without traveling to the United States?

In many cases, yes. Mortgage applications, document collection, underwriting, and portions of the closing process can often be completed remotely. Depending on the state and transaction structure, remote notarization or power-of-attorney arrangements may also be available.

At HomeAbroad, we ensure the reliability of our content by relying on primary sources such as government data, industry reports, firsthand accounts from our network of experts, and interviews with specialists. We also incorporate original research from respected publishers when relevant. Discover more about our commitment to delivering precise and impartial information in our editorial policy.

National Association of Realtors: 2024 International Transactions in U.S. Residential Real Estate

IRS: FIRPTA Withholding

IRS: US-UK Tax Treaty

Govt.UK : UK Stamp Duty

Investopedia: 1031 Exchange

![Can Foreigners Buy Property in the USA? [2026]](https://homeabroadinc.com/wp-content/uploads/2021/07/CanForeignersBuyinUS.jpg)

![A Guide to US Mortgages for UK Citizens [2026]](https://homeabroadinc.com/wp-content/uploads/2022/06/USMorgagesGuideForUKInvestor.png)