Editorial Integrity

Making informed real estate decisions starts with having the right knowledge. At HomeAbroad, we offer US mortgage products for foreign nationals & investors and have a network of 500+ expert HomeAbroad real estate agents to provide the expertise you need. Our content is written by licensed mortgage experts and seasoned real estate agents who share insights from their experience, helping thousands like you. Our strict editorial process ensures you receive reliable and accurate information.

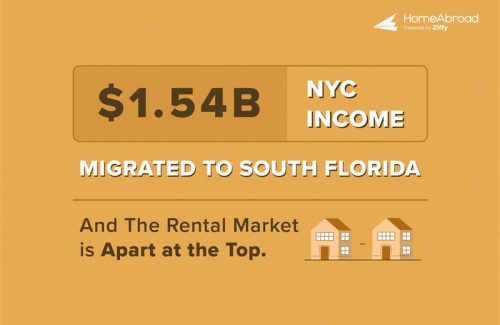

In one year, 8,036 New York City tax filers moved $1.54 billion in income to three South Florida counties. In the counties receiving that income, upper-tier rents are outpacing the rest of the market, while growth in mid- and lower-tier segments is more limited.

This analysis combines IRS migration records, a roughly 10-percentage-point effective tax gap, and Zillow rent data across 158 South Florida ZIP codes. The results reveal a consistent pattern: in counties receiving higher-income movers, rent growth is concentrated at the top end of the market.

Table of Contents

Key Highlights

-

$1.54 Billion in NYC Income Moved to Three South Florida Counties in a Single Year

$1.54 Billion in NYC Income Moved to Three South Florida Counties in a Single Year

In the 2022-2023 filing year, 8,036 NYC tax filers relocated to Miami-Dade, Broward, and Palm Beach counties, carrying $1.54 billion in adjusted gross income. Manhattan alone accounted for 66% of that total, over $1 billion, despite representing fewer filers than Brooklyn and Queens combined. - Manhattan Movers to Palm Beach Earn Nearly 7× the Local Median

Manhattan tax filers moving to Palm Beach County reported an average AGI of $578,149 per return, nearly seven times the county’s median household income ($83,581). Manhattan filers moving to Miami-Dade averaged $357,633. Across all three counties, Manhattan alone accounted for $1.02 billion, roughly two-thirds of total NYC income flowing to South Florida. - Upper-Tier Rents Are Outpacing the Rest of the Market in High-Income Inflow Counties

In Palm Beach County, upper-tier ZIP codes saw rents grow 3.84% year-over-year, compared to 1.33% in mid-tier and 1.10% in lower-tier segments. In Miami-Dade, upper-tier rents grew 2.58% while mid-tier (−0.30%) and lower-tier (−0.55%) rents declined. Counties receiving higher-income NYC movers show the strongest upper-tier divergence. The pattern holds across all three counties, but is most pronounced where average mover income is highest.

The NYC–Florida Tax Gap: A ~10 Percentage Point Difference

A household earning $1 million in New York City faces an effective income tax rate of 38.4%, compared to 28.2% for the same household in Florida. The gap, roughly 10 percentage points, or $101,853 per year is driven almost entirely by New York State and New York City income taxes, which together total $103,148 at this income level. Florida levies no state income tax.

This gap persists across income levels, though it narrows at $500,000 where the expanded SALT deduction (raised to $40,000 under the One Big Beautiful Bill) reduces the NYC tax burden. At $500,000, annual tax savings are $38,798; at $750,000, they reach $75,108 (where the SALT cap phases back to $10,000). The relative increase in after-tax income rises with income: 10.9% at $500,000, 15.5% at $750,000, and 16.5% at $1 million.

Note: These modeled tax comparisons assume married filing jointly status and compare income-tax burdens only. They exclude payroll, property, and sales taxes. Full assumptions are detailed in the methodology section.

This difference translates into a meaningful increase in potential housing budgets for relocating households.

Household Income | Annual Tax Savings | Monthly Tax Savings | Housing Budget | Housing Budget |

|---|---|---|---|---|

$500,000 | $38,798 | $3,233 | $1,293 | $970 |

$750,000 | $75,108 | $6,259 | $2,504 | $1,878 |

$1,000,000 | $101,853 | $8,488 | $3,395 | $2,546 |

Even under a conservative assumption that households allocate 30% of tax savings to housing, the resulting budget increase ranges from $970 to $2,546 per month. At a 40% allocation, a $1 million household gains $3,395 per month.

These modeled increases fall within the range of observed upper-tier rents in the receiving counties, including approximately $3,662 per month in Miami-Dade and $3,737 in Palm Beach.

Note: Under the One Big Beautiful Bill (P.L. 119-21), the SALT deduction cap increased to $40,000 for 2025 (phasing out for MAGI above $500,000). At $500K, the NYC filer’s itemized deductions ($65,000) substantially exceed Florida’s $31,500 standard deduction, producing a federal tax difference of ~$10,720. At $750K and $1M, the SALT cap phases back to $10,000 and the federal difference narrows to ~$1,225- $1,295. All differences are netted into savings figures above.

Illustrative Policy Scenario

Under the Mamdani tax plan, a proposed increase of approximately 2 percentage points to New York City’s top income tax rate, annual tax savings would rise to $119,498 for a $1 million household. This scenario is illustrative and modeled separately in the methodology appendix.

Where the Money Went: $1.54 Billion Across Three Counties

In the 2022-2023 filing year, 8,036 tax filers from New York City’s five boroughs relocated to Miami-Dade, Broward, and Palm Beach counties, carrying $1.54 billion in adjusted gross income.

Manhattan’s 2,685 filers spread across Miami-Dade (1,445), Palm Beach (734), and Broward (506) moved more income than the remaining four boroughs combined. Over $1 billion of the $1.54 billion total originated from a single borough.

Destination County | Origin Borough | Number of Filers | Total AGI Moved | Average AGI per Filer |

|---|---|---|---|---|

Miami-Dade | Manhattan | 1,445 | $516.8M | $357,633 |

Miami-Dade | Brooklyn | 843 | $121.3M | $143,931 |

Miami-Dade | Queens | 590 | $65.6M | $111,200 |

Palm Beach | Manhattan | 734 | $424.4M | $578,149 |

Palm Beach | Brooklyn | 542 | $70.5M | $130,125 |

Palm Beach | Queens | 572 | $55.5M | $96,941 |

Broward | Brooklyn | 828 | $61.7M | $74,500 |

Broward | Queens | 745 | $51.5M | $69,192 |

Broward | Manhattan | 506 | $79.6M | $157,342 |

All Three Counties | Bronx, Staten Island | 1,231 | $92.5M | $75,167 |

Note: Bronx (836 filers) and Staten Island (395 filers) are combined across all three destination counties due to smaller filer volumes at the borough-county-pair level. Full breakdown available on request.

The income gradient across destinations is pronounced. Manhattan-to-Palm Beach filers reported an average AGI of $578,149 per return, the highest of any borough-to-county pair and nearly eight times the average for Broward-bound movers from Brooklyn ($74,500).

Palm Beach draws the highest-income movers overall (average AGI $263,466 across all NYC boroughs), followed by Miami-Dade ($223,580), while Broward attracts movers at a substantially lower average income ($88,849), consistent with the weaker rent divergence observed in that county. This distribution aligns closely with the rent patterns observed across the three counties and has direct implications for anyone evaluating rental property in Florida.

NYC’s share of each county’s out-of-state inflows reinforces this pattern. In Miami-Dade, NYC accounts for 14% of out-of-state tax returns but 17.5% of AGI, a disproportionately income-heavy flow.

In Broward, NYC accounts for 12% of returns but only 9.1% of AGI, consistent with lower-income inflows. Palm Beach falls in between at 9.8% of returns and 10.5% of AGI.

These single-year figures reflect a broader structural trend. From 2019 to 2023, Palm Beach County received $22.7 billion in net income inflow, the highest of any U.S. county, while Miami-Dade added $10.5 billion.

At the state level, Florida gained $137 billion in net income over this period, reinforcing its position as the top destination for foreign real estate investment in Florida and domestic relocation alike, while New York saw a net outflow of $76.7 billion. The NY-to-Florida corridor alone accounted for $37.4 billion and 1.35 million tax filers.

Based on IRS individual income tax data through tax year 2022, Florida reported 77,760 tax returns with AGI above $1 million, compared to 69,780 in New York.

The Tax Foundation’s 2026 State Tax Competitiveness Index ranks New York 50th out of 50 states, while Florida ranks 5th overall and 1st for individual income tax competitiveness.

Amresh Singh

Founder and CEOHomeAbroad

The Rent Signal: Upper-Tier Rents Are Outpacing Other Segments in High-Income Inflow Counties

Across 158 South Florida ZIP codes, a consistent pattern emerges: upper-tier rents are growing fastest in the counties receiving higher-income NYC movers, while growth in mid- and lower-tier segments is more limited.

The divergence is most pronounced in the counties with the highest average mover incomes and weakest in the county with the lowest.

In Palm Beach County, upper-tier ZIP codes saw rents grow 3.84% year-over-year, 2.51 percentage points faster than mid-tier and 2.74 points faster than lower-tier. Over 24 months, upper-tier rents grew 8.28%, more than double the mid-tier increase of 3.72%.

This represents the strongest upper-tier rent growth among the three counties and aligns with both the highest average mover income ($263,466) and the largest cumulative net income inflow.

In Miami-Dade, upper-tier rents grew 2.58%, while mid-tier rents declined 0.30% and lower-tier rents declined 0.55%, the only county where upper-tier growth coincided with outright rent declines in other tiers.

The average upper-tier rent reached $3,662 per month, requiring approximately $146,000 in annual household income at a 30% rent-to-income threshold.

Broward presents a more moderate pattern. Upper-tier rents grew 1.74%, and the gap over mid-tier (0.85%) stays under one percentage point, while lower-tier rents (1.02%) grew slightly faster than mid-tier.

Broward also receives NYC movers with the lowest average income of the three counties ($88,849 per filer), compared to $223,580 in Miami-Dade and $263,466 in Palm Beach. The smaller divergence is consistent with a lower-income inflow distributed more evenly across rent tiers.

County | Upper-Tier Rent Growth (YoY) | Mid-Tier Rent Growth (YoY) | Lower-Tier Rent Growth (YoY) | Upper–Mid Gap (pp) | Divergence Signal |

|---|---|---|---|---|---|

Palm Beach | +3.84% | +1.33% | +1.10% | 2.51pp | Clear Divergence |

Miami-Dade | +2.58% | -0.30% | -0.55% | 2.88pp | Clear Divergence |

Broward | +1.74% | +0.85% | +1.02% | 0.89pp | Mixed |

Note-Tiers constructed from 158 ZIP codes grouped by current rent level: top 25% = upper, middle 50% = mid, bottom 25% = lower.

The income gradient of NYC movers moves in the same direction as upper-tier rent growth. Palm Beach (average mover AGI: $263,466) shows the fastest upper-tier growth at 3.84% YoY, Miami-Dade ($223,580) shows 2.58%, and Broward ($88,849) shows 1.74%.

While this does not establish causation, it reflects a clear correlation between migration income levels and rent tier divergence.

The tax model provides additional context. A $1 million household gains approximately $3,395 per month in housing budget at a 40% allocation of tax savings, within the observed upper-tier rent range across all three counties ($3,662 in Miami-Dade, $3,737 in Palm Beach, $3,342 in Broward).

Even at a 30% allocation, the $2,546/month budget expansion is comparable to mid-tier rent levels across the three counties (ranging from $2,479 in Broward to $2,632 in Miami-Dade).

New Construction is Elevated – Upper-Tier Rents Continue to Outpace

The most immediate alternative explanation for the observed rent patterns is supply. The South Florida housing market is in the middle of a significant construction cycle, and nationally, 2024 saw the highest level of multifamily completions since 1986.

If upper-tier rents are rising, one possibility is that new luxury supply is influencing pricing at the top end of the market.

Recent data provides important context. In Miami-Dade, housing permits rose 19% year-over-year in the first half of 2025, with 85% of authorized units in multifamily buildings.

Across Southeast Florida, more than 27,000 units are currently under construction for delivery between 2025 and 2027, adding roughly 6.5% to existing rental stock in buildings with 50 or more units.

At the same time, occupancy in Miami-Dade remained high at 95.9% as of May 2025. Absorption exceeded new supply by approximately 1,200 units in the year ending Q1 2025, based on RealPage data, supported by population growth of an estimated 325,000 residents between 2020 and 2024.

Market | Vacancy Rate | YoY Rent Growth | 2026 Forecast |

|---|---|---|---|

Miami Metro | 6.3% | +1.2% | +3.8% |

Fort Lauderdale | – | −0.8% | +3.5% |

West Palm Beach | – | −0.7% | +3.0% |

National Average | 7.3% | −1.7% | +2.3% |

Note- 2026 forecasts sourced from RealPage (via CRE Daily). Vacancy rates from Apartment List (March 2026). Rent growth measurements vary by publisher and time period; Miami figure from RealPage May 2025, remaining figures from Apartment List February 2026.

Miami metro vacancy stands well below the national level and below Sunbelt peers such as Austin (9.9%), Dallas (8.7%), and Phoenix (8.3%). Miami is the only South Florida market with positive aggregate rent growth. Between 10% and 15% of units across South Florida markets are offering concessions, with the higher end in Fort Lauderdale and West Palm Beach.

This is where the tier-level analysis adds additional context. While aggregate rents in Fort Lauderdale and West Palm Beach are softening, upper-tier ZIP codes in Palm Beach County continue to show stronger growth (+3.84%) compared to mid- and lower-tier segments (under 1.5%).

The data indicates that broad market softening and upper-tier resilience can occur simultaneously, reflecting a market where new supply is being absorbed alongside concentrated demand at the higher end.

What Tax Migration Means for the Renters Already There

The upper-tier rent signal is unfolding in a market where affordability is already stretched. In Miami-Dade, roughly 48% of renter households are cost-burdened, and 90% of renters earning under $50,000 spend more than 30% of their income on housing.

At current rent levels, the gap is significant. The average Miami-Dade market rent of $2,678 per month (RealPage, May 2025) requires approximately $107,000 in annual household income, about 70% above the county’s median income of $63,000. At the upper tier ($3,662/month), the required income rises to roughly $146,000, more than double the median.

This pressure is compounded by a structural shortage of affordable housing. Miami-Dade faces a deficit of 90,181 rental units for households earning below 80% of area median income, projected to increase to 116,000 by 2030. The shortage is concentrated at the lower end of the market, where demand already exceeds supply.

Within this context, the distribution of demand across rent tiers becomes increasingly important. If higher-income in-migration contributes to demand at the top end of the market, one potential downstream effect is increased competition for mid-tier housing.

As higher-income households occupy upper-tier units, middle-income renters may face tighter availability, extending affordability pressure further down the income spectrum. Housing economists describe this dynamic as “filtering” the movement of demand and households across price tiers, though the specific South Florida pattern has not been directly modeled in this analysis.

Debjit Saha

Co-Founder and CTOHomeAbroad

Across all three counties, the income required to access upper-tier housing significantly exceeds local medians, while the income profile of incoming NYC households aligns more closely with these higher price points.

Methodology

Data Sources

Primary Sources

- IRS SOI County-to-County Migration Data (2022–2023): Returns, individuals, and AGI by origin-destination county pair (published March 2026).

- IRS Individual Income Tax Rate Schedules (TY 2025): Revenue Procedure 2024-40 (MFJ brackets)

- New York State Tax Law 601 (TY 2025): State income tax brackets

- NYC Administrative Code §11-1701 (TY 2025): City income tax brackets

- Florida Constitution, Art. VII §5: Prohibition of state income tax

- Zillow ZORI (ZIP-level): All homes plus multifamily, smoothed and seasonally adjusted

- One Big Beautiful Bill Act (P.L. 119-21), signed July 4, 2025: $40K SALT cap with MAGI phase-out; MFJ standard deduction raised to $31,500 for TY 2025

Supporting Sources

- MIAMI Association of Realtors (March 2026 migration analysis)

- Apartment List (National Rent Report, March 2026; metro vacancy estimates for Austin, Dallas, Phoenix)

Contextual Sources

- U.S. Census Building Permits Survey (via MIAMI Realtors, H1 2025)

- American Community Survey (2020-2024): Income, rent, cost burden

- UF Shimberg Center: Affordable housing gap estimates

- Tax Foundation (2026 State Tax Competitiveness Index)

- RealPage (via CRE Daily): 2026 rent forecasts, occupancy, and absorption data

- IRS Statistics of Income, Historical Data Table 2 (TY 2022): Millionaire filer counts by state

Key Definitions

| Term | Definition |

| Tax migration advantage | Difference in total tax burden (federal + state + city) between a NYC resident and a FL resident at the same gross income. |

| Effective tax rate | Total tax burden divided by gross household income. Includes federal, state, and city income taxes. Excludes payroll, property, and sales taxes. |

| Housing budget expansion | Modeled estimate of additional monthly spending power for housing, calculated as 30%, 40%, or 50% of monthly tax savings. |

| Rent tiers | ZIP codes sorted by most recent ZORI value (descending), grouped into percentile brackets. Top 25% = upper. Middle 50% = mid. Bottom 25% = lower. |

| Upper-to-mid gap | Difference in YoY rent growth between upper and mid-tier within a county, in percentage points. |

| Clean ZIP | A ZIP with valid ZORI observations at all three time points (Feb 2024, Feb 2025, Feb 2026). ZIPs with missing values were excluded, as was one extreme outlier ($28,500/month in Miami-Dade ZIP, likely reflecting small-sample luxury listings). |

| AGI | Adjusted gross income per IRS tax returns. Includes wages, business income, capital gains, and other taxable income before deductions. |

Modeling Assumptions

| Parameter | Value | Rationale |

| Filing status | Married Filing Jointly | Most representative for $500K+ households |

| NYC deductions | Itemized: $40K SALT (OBBB, phases out >$500K MAGI) + $25K other | Exceeds standard deduction at these income levels |

| FL deductions | Standard: $31.5K | Exceeds itemized ($25K, no state tax to deduct) |

| SALT cap | $40,000 | (OBBB,P.L.119−21).Phasesoutat30¢/ for MAGI >$500K, floor $10K |

| Mortgage interest | Excluded | Renter model, no mortgage interest deduction |

| Housing allocation | 30% / 40% / 50% of monthly savings | Conservative / base / aggressive scenarios |

| Income bands | $500K / $750K / $1M | Upper-tier renter households most likely to relocate |

| Rent tier method | ZIP-level ZORI, sorted, grouped by percentile | Top 25% = upper, middle 50% = mid, bottom 25% = lower |

| Clean ZIP count | 65 Miami-Dade, 51 Broward, 42 Palm Beach (158 total) | Per “Clean ZIP” definition above |

| IRS limitation | County data: total AGI, not by bracket | $200K+ breakdown in state-to-state files only |

| Mamdani scenario | NYC top rate +2pp (3.876% – 5.876%) | Illustrative; based on proposal, not enacted law |

| Model type | Comparative tax model | Aggregate scenarios, not individual tax advice |

Tax Model Construction

The tax migration model compares total tax burden for households at three income levels ($500,000, $750,000, and $1,000,000) under two location scenarios: New York City and Florida.

For the NYC scenario, minus itemized deductions ($65,000 at $500K income; $35,000 at $750K and $1M, where the SALT cap phases to $10,000). Federal tax is computed using TY 2025 MFJ brackets. New York State and New York City taxes are computed separately using their respective published bracket schedules and summed.

For the Florida scenario, federal taxable income is calculated as gross income minus the standard deduction ($31,500), which exceeds the available itemized deductions. Federal tax is computed using the same brackets. State and local income tax is zero.

Annual tax savings equal the difference in after-tax income between the two scenarios. Monthly savings are annualized savings divided by 12. Housing budget expansion is monthly savings multiplied by the allocation percentage.

At $750K and $1M, the deduction gap ($35,000 NYC itemized vs. $31,500 FL standard) produces a small federal tax difference of $1,225-$1,295. At $500K, the $40,000 SALT cap widens the NYC deduction to $65,000, creating a larger federal tax difference of ~$10,720. All differences are netted into savings figures

Rent Tier Construction

ZORI data was downloaded at the ZIP code level from Zillow Research for all available Florida ZIP codes and filtered to Miami-Dade, Broward, and Palm Beach counties.

ZIPs missing ZORI values at any of the three required time points (February 2024, February 2025, February 2026) were excluded. One extreme outlier was also excluded: a Miami-Dade ZIP reporting $28,500/month, substantially above the next-highest ZIP ($7,636/month), likely reflecting a small sample of ultra-luxury listings rather than a representative market rate. After cleaning, 158 ZIPs remained: 65 in Miami-Dade, 51 in Broward, and 42 in Palm Beach.

Within each county, ZIPs were sorted by latest ZORI value in descending order and assigned to tiers based on position. Tier boundaries were determined by count, not by rent thresholds, so the cutoff values differ by county.

Year-over-year and 24-month growth were calculated at the tier level using the average ZORI value for all ZIPs in each bracket at each time point.

NYC-to-Florida Migration Data Processing

The IRS SOI county-to-county inflow CSV was filtered for three Florida destination counties and five New York City origin counties (Manhattan, Brooklyn, Queens, Bronx, Staten Island), producing 15 borough-to-county pairs.

For each pair, number of returns, number of individuals, and adjusted gross income (reported in thousands in the source file, converted to dollars) were extracted.

Average AGI per return was calculated as total AGI divided by number of returns. Cells suppressed by IRS disclosure rules (fewer than 20 matched returns, appearing as −1) were excluded.

Cumulative 2019-2023 county-level flows and state-level totals were sourced from the MIAMI Association of Realtors analysis of the same IRS dataset, published March 2026.

Limitations

IRS SOI county-to-county data does not break AGI by income bracket at the county level. Average AGI per return includes all income levels and is therefore lower than the average for the $500K+ cohort modeled in the tax analysis.

The mover income figures cited are conservative estimates of the high-income segment.

IRS data is lagged by approximately one year. The 2022-2023 filing year reflects address changes between tax years 2022 and 2023. Migration patterns may have shifted since the data was collected.

ZORI tracks the 40th to 60th percentile of rents and does not capture the full distribution, particularly at the extreme upper end.

Tier construction using percentile-based ZIP groupings is a proxy for price segmentation, not a direct measurement of luxury vs. affordable units.

This analysis documents a correlation between migration income levels and rent tier divergence. It does not establish causation. Other factors, including new luxury construction, remote work migration, international capital flows, and local zoning policy, may contribute to observed rent patterns.

AGI per tax return approximates household income for married-filing-jointly households, the predominant filing status at the income levels modeled.

Replicability

The core migration, rent-tier, and tax-model findings are fully replicable using publicly available data at no cost. IRS SOI migration files are downloadable from irs.gov.

Zillow ZORI data is downloadable from zillow.com/research/data. Tax rate schedules are published by the IRS, New York State, and New York City.

ACS data is available at data.census.gov. The tier construction method and tax model use published inputs with no proprietary data.

Notes

- All dollar figures are nominal and not adjusted for inflation.

- The 158-ZIP dataset excludes ZIPs with missing historical ZORI values and one extreme outlier. Including those ZIPs would not materially change tier-level averages but would reduce the reliability of growth rate calculations.

- The Mamdani tax increase scenario is modeled as illustrative and does not reflect enacted law.

- The takeaway is not that taxes alone drive rents, but that high-income migration and upper-tier rent resilience are moving together in the same places, and the data now exists to measure it at the ZIP level.

- Full underlying data tables are included with the report, and calculations and source files are available upon request at [email protected]

![Can Foreign Nationals Buy Property in Florida? [A Comprehensive Guide]](https://homeabroadinc.com/wp-content/uploads/2024/12/CanForeignersBuyinFlorida.jpg)