Editorial Integrity

Making informed real estate decisions starts with having the right knowledge. At HomeAbroad, we offer US mortgage products for foreign nationals & investors and have a network of 500+ expert HomeAbroad real estate agents to provide the expertise you need. Our content is written by licensed mortgage experts and seasoned real estate agents who share insights from their experience, helping thousands like you. Our strict editorial process ensures you receive reliable and accurate information.

A foreign national buyer can qualify financially but still face financing challenges if the condo project’s HOA, insurance, litigation, rental rules, or warrantability do not meet underwriting requirements.

While conventional lenders often decline non-warrantable condo projects, HomeAbroad offers DSCR Loan options that evaluate the property’s income potential and overall project stability.

Monthly HOA dues are included in PITIA, while HOA bylaws and insurance requirements can influence cash flow, loan eligibility, and the financing structure.

Requesting HOA documents, reviewing project eligibility, verifying insurance, and organizing foreign national documentation early can help identify issues before they delay underwriting or closing.

Table of Contents

You found a condo in the US that looks perfect as an investment property. The numbers work, the location is strong, and the rental income looks promising.

Then the financing starts falling apart. The building gets flagged for HOA issues. The condo is labeled non-warrantable. The insurance review fails. Or the DSCR calculation changes once the HOA dues are added to the payment. This is where foreign investors usually get stuck.

Condo loans are not approved on the buyer alone. The condo project itself goes through a separate review covering HOA finances, insurance, rental rules, litigation, occupancy, and warrantability. A financially strong buyer can still lose financing because of problems tied to the building itself.

At HomeAbroad, we finance foreign national condo purchases through our foreign national mortgages, including condo projects that conventional lenders may decline.

Some warrantable condos move through underwriting smoothly. Others require a DSCR structure because of investor concentration, short-term rental rules, or project-level issues. The outcome depends heavily on the specific building, HOA profile, insurance structure, and rental strategy tied to the property.

This guide breaks down how condo warrantability, HOA underwriting, insurance review, and DSCR condo analysis actually work for foreign national buyers. You’ll see why certain condo deals fail financing, how DSCR condo underwriting differs from agency rules, and what to review before making an offer so problems surface early instead of during closing.

Why Condo Financing Is Different for Foreign National Investors

A single-family purchase is underwritten around the borrower and the property.

A foreign national condo financing works differently because the financing process effectively reviews three separate layers at the same time:

- The condo project itself

- The foreign national borrower

- The operational logistics of closing the transaction from abroad

That is why condo financing carries more friction than a standalone single-family rental property.

The first layer is the condo project review. At HomeAbroad, we review the HOA’s financial condition, insurance coverage, litigation exposure, rental restrictions, reserve funding, owner-occupancy ratios, and overall warrantability profile before the loan moves toward final approval. A buyer may have strong liquidity and reserves, but the transaction can still run into problems if the condo project itself does not meet underwriting standards.

The second layer is foreign national underwriting. What we see often is that overseas buyers have fully workable financial profiles but incomplete documentation trails once underwriting begins. International wire transfers, reserve verification, overseas bank statements, LLC vesting structures, and alternative credit documentation all become part of the file because many foreign buyers do not have US credit scores or traditional US income history.

The third layer is operational execution. Earlier this year, a Miami condo transaction had strong reserves, clear source of funds, and an approvable DSCR profile, but the closing was pushed past the contract deadline because the HOA management company delayed the questionnaire package for almost six weeks. Timing issues like that are common in condo transactions involving foreign buyers, remote closings, and HOA-controlled documentation.

These three layers do not sit independently. HOA dues directly affect DSCR calculations. Insurance deficiencies can delay closings or increase reserve requirements. Rental restrictions inside the condo bylaws may change whether the property qualifies under a DSCR structure at all.

Steven Glick

Director of Mortgage Sales · HomeAbroad

When a foreign national investor purchases a condo, we begin reviewing the condominium project documentation alongside the borrower’s file from the start. Confirming items such as the HOA’s required documents, insurance information, and project eligibility early helps us identify any additional documentation that may be needed and keeps the financing process moving efficiently

At HomeAbroad, we manage all three layers as part of the same financing process. Based on our foreign national condo transactions across Florida, Texas, New York, and Nevada, the smoothest closings are usually the ones where the condo review, borrower documentation, and remote-closing logistics are coordinated from the beginning.

What Makes a Condo Financeable: Warrantability Explained

Warrantable vs. Non-Warrantable: The Core Distinction

A condo is considered warrantable when the project meets Fannie Mae or Freddie Mac condominium standards and qualifies for conventional financing.

A non-warrantable condo is a project where one or more of those standards fail. The most common triggers include low owner-occupancy ratios, high investor concentration, excessive commercial space, weak HOA reserves, pending litigation, or hotel-style operations tied to short-term rental activity.

Under current agency guidelines, conventional financing often becomes difficult when:

- Owner occupancy falls below roughly 50% in investor-heavy projects

- Commercial space exceeds around 35% of the building

- HOA reserve contributions are materially underfunded

- One investor or entity controls an outsized percentage of units

- The condo operates too similarly to a hotel or hospitality property

Some of these thresholds vary by loan program, occupancy type, and project review structure. Fannie Mae’s condo standards also evolve periodically, especially around reserve funding and project eligibility requirements. Fannie Mae project-review guidance under the Selling Guide remains the baseline reference point for most agency condo underwriting.

Resort and vacation markets run into these issues frequently because many otherwise profitable rental buildings operate more like hospitality assets than traditional residential condominiums.

Non-warrantable does not mean unfinanceable. It means the project falls outside conventional agency rules.

At HomeAbroad, we finance both warrantable and non-warrantable condos, but the pricing, down payment, reserve requirements, and loan structure can change depending on the condo project and underwriting path.

How DSCR Condo Project Review Differs from Agency Warrantability

A condo can fail agency warrantability and still qualify for HomeAbroad’s DSCR loan. The two reviews look at different things.

Agency financing follows standardized project rules tied to conventional secondary-market requirements. DSCR condo underwriting focuses more directly on whether the property functions as a stable income-producing asset with manageable project-level risk.

At HomeAbroad, our DSCR condo review typically evaluates the project’s physical condition, HOA financial stability, insurance adequacy, litigation severity, rental viability, and short-term rental restrictions.

That creates flexibility in areas where conventional financing often struggles, especially in:

- Investor-heavy condo projects

- Resort-market buildings

- Condos with elevated investor ownership concentration

- Non-warrantable projects with otherwise stable cash flow and operations

At the same time, DSCR underwriting may become stricter when the investor’s rental strategy depends heavily on Airbnb or vacation-rental income and the HOA bylaws create uncertainty around short-term rental usage.

We encourage buyers to request the HOA questionnaire as soon as a contract is accepted because underwriting cannot complete the condo review without it. Since every HOA follows its own document-request process, starting early helps avoid unnecessary delays, especially when coordinating with international buyers.

Review Criteria | Agency Warrantability | DSCR Condo Review |

|---|---|---|

Owner-Occupancy Ratio | Strict thresholds | More flexible |

Single-Entity Ownership | Heavily restricted | Reviewed case-by-case |

HOA Reserves |

| Overall financial stability reviewed |

Commercial Space | Tight percentage caps | More flexible depending on project |

Short-Term Rental Rules | Often restrictive | Rental viability evaluated directly |

Condo Litigation | Frequently disqualifying | Severity and nature reviewed |

Common Reasons Condos Fail Warrantability (and What Foreign Investors Can Do)

Low owner-occupancy ratios are one of the most common problems in resort-heavy markets like Miami and Orlando where a large percentage of units operate as rentals. Conventional financing may decline these buildings even when rental demand remains strong. In many cases, DSCR financing becomes the more practical path because the review focuses more heavily on income viability and project stability.

Single-entity concentration is another frequent issue in newer condo developments where a developer or institutional investor still controls a large percentage of units. What we see often is buyers discovering this only after the condo questionnaire comes back during underwriting. Pulling HOA and ownership information earlier in the process usually prevents that surprise.

Litigation creates a different category of risk. Structural-defect lawsuits and major construction claims create much bigger financing problems than smaller disputes between unit owners or vendors. Some DSCR structures remain workable depending on the severity of the litigation, insurance impact, and HOA financial condition, but the review becomes much more project-specific.

Commercial-space ratios also affect warrantability. Mixed-use buildings with large retail components may fail conventional condo rules even when the residential side of the project performs well operationally. Certain DSCR condo programs remain more flexible here depending on the overall building profile.

Short-term rental characterization is the final major category. Condo projects operating too similarly to hotels often fail agency financing entirely. In these situations, the HOA bylaws, rental restrictions, and documented rental history become critical in determining whether the property still works under a DSCR structure.

HOA Underwriting: What HomeAbroad Actually Reviews

The Condo Questionnaire (Form 1076 and Beyond)

One of the first operational hurdles in condo financing is the HOA questionnaire.

This is the document package HomeAbroad sends to the HOA or property management company to verify the condo project’s financial condition, insurance structure, occupancy profile, litigation exposure, reserve funding, and rental restrictions. In conventional lending, this is commonly tied to Form 1076, but DSCR condo reviews often require supplemental project information as well.

The important operational detail is that the questionnaire is not completed by the seller. It usually comes from the HOA management company, and that process moves slowly in many condo projects.

What we see often in foreign national condo transactions is buyers losing valuable underwriting time because nobody ordered the questionnaire immediately after contract acceptance. Many HOA management companies:

- Charge $250–$500 for document preparation

- Require upfront payment before processing

- Take 7–14 business days to return documents

- Delay responses when follow-up coordination happens across time zones

That delay can become a major issue because underwriting cannot fully review the condo project until the HOA package arrives.

At HomeAbroad, we usually recommend starting the HOA-document request process on day one of the contract period rather than waiting for appraisal or borrower-document collection to finish.

HOA Budget, Reserves, and Special Assessments

The HOA budget review is not just about whether the building has money in the bank. We review how the association is actually operating financially.

At HomeAbroad, condo underwriting typically reviews:

- Reserve allocation levels

- Operating deficits

- Delinquent HOA dues

- Upcoming structural projects

- Insurance costs

- Existing or pending special assessments

Agency-backed condo financing often expects reserve contributions around 10% of the HOA’s annual operating budget. DSCR condo underwriting is usually more flexible on the exact percentage, but we still need to see financial stability and documented reserve strength.

This became especially important in older condo buildings after the Surfside collapse in Florida, where reserve funding and deferred maintenance started receiving much heavier scrutiny across the market.

The distinction here is that HOA-funded structural work eventually flows through to unit owners. Large special assessments directly increase carrying costs, which can reduce property cash flow and impact DSCR qualification.

For foreign buyers, the practical takeaway is simple: request the HOA budget and reserve study before making an offer whenever possible, especially in older condo projects.

HOA Litigation and Pending Assessments

Litigation review is another area where condo financing becomes highly project-specific.

Agency financing often treats litigation as a near-binary issue. DSCR condo underwriting tends to evaluate the severity and nature of the lawsuit instead.

Structural-defect litigation, construction-defect claims, or lawsuits where the HOA itself is being sued create the biggest financing concerns because they can affect property value, insurance availability, and future assessments.

Smaller disputes usually carry less risk. For example:

- Unit-owner disputes

- Vendor disagreements

- Collection actions initiated by the HOA

May still remain financeable depending on the overall project profile.

Owner-Occupancy Ratios and Single-Entity Concentration

These are two of the most common reasons condo projects fail conventional warrantability review in investor-heavy markets.

Agency financing for condo investment properties often expects at least 50% owner occupancy within the building. Resort and vacation-rental markets regularly fall below that threshold because many units operate as rentals rather than primary residences.

Single-entity concentration creates another common issue. In newer projects, developers or institutional investors sometimes still control a large percentage of units, particularly in buildings with more than 20 units.

At HomeAbroad, DSCR condo programs are generally more flexible around both occupancy concentration and investor ownership levels than agency-backed financing. That flexibility is one reason DSCR financing remains a common path for foreign investors purchasing condos in high-rental-demand markets like Miami, Orlando, Las Vegas, and parts of Texas.

Condo Insurance Requirements for Foreign Investors

Master Policy vs. HO-6 Walls-In Coverage

Two insurance policies sit on every financed condo. The first is the HOA’s master insurance policy, which covers the building structure and common areas. The second is the unit owner’s HO-6 policy, often called walls-in coverage, which protects the interior of the unit along with personal property, liability exposure, and certain loss-assessment situations.

The master-policy review typically focuses on the building’s coverage limits, liability protection, deductible structure, flood coverage where applicable, and any named-storm or hurricane carve-outs. Coverage requirements can vary depending on the condo project, state, and financing structure.

In coastal markets, deductible exposure becomes especially important. In Florida, for example, hurricane deductibles commonly range from 2% to 5% of the insured building value, which can materially affect the HOA’s financial exposure after a storm event.

The HO-6 policy covers the unit itself from the walls inward. That usually includes interior finishes, appliances, personal property, liability coverage, water-damage exposure, and certain HOA loss assessments charged back to unit owners.

Both policies must clear before closing. The master policy is outside the buyer’s control. The HO-6 policy is not.

Hurricane, Flood, and Wind Coverage in Coastal Markets

Coastal condos pull foreign investors because they rent well and still feel like vacation property. The financing challenge is insurance.

Flood insurance becomes mandatory when the condo project sits inside a FEMA-designated Special Flood Hazard Area (SFHA). Wind coverage may also sit outside the primary master policy through separate state-backed systems such as Florida Citizens Property Insurance or the Texas Windstorm Insurance Association.

Insurance availability and pricing also vary significantly by market and building profile. Older coastal condo projects, investor-heavy towers, and short-term-rental-oriented buildings often face tighter underwriting and higher premiums than stabilized residential projects.

What we’ve seen across recent Florida condo transactions is that insurance-cost increases can materially change condo economics within a single renewal cycle. Higher premiums often push HOA dues upward, which then directly impacts DSCR qualification because those dues sit inside PITIA.

Insurance in LLC Name: The Foreign National Layer

Many foreign investors purchase US condos through a US LLC for liability separation and long-term ownership structuring.

That creates an additional insurance step that buyers often discover late in the transaction.

The HO-6 policy usually needs to be issued directly in the LLC’s name or with the LLC properly listed as an additional insured party. At the same time, the HOA master insurer and association records must recognize the LLC as the legal owner of the unit.

What we see often is buyers forming the LLC shortly before closing without coordinating the insurance structure early enough. Some older condo associations and insurance carriers push back on foreign-member LLC structures, incomplete operating agreements, or last-minute ownership changes.

The fix is operational rather than structural: start the insurance binder process the same time the LLC is formed, not the week closing documents are already being prepared.

DSCR Loans on Condos: How the Math and Review Differ

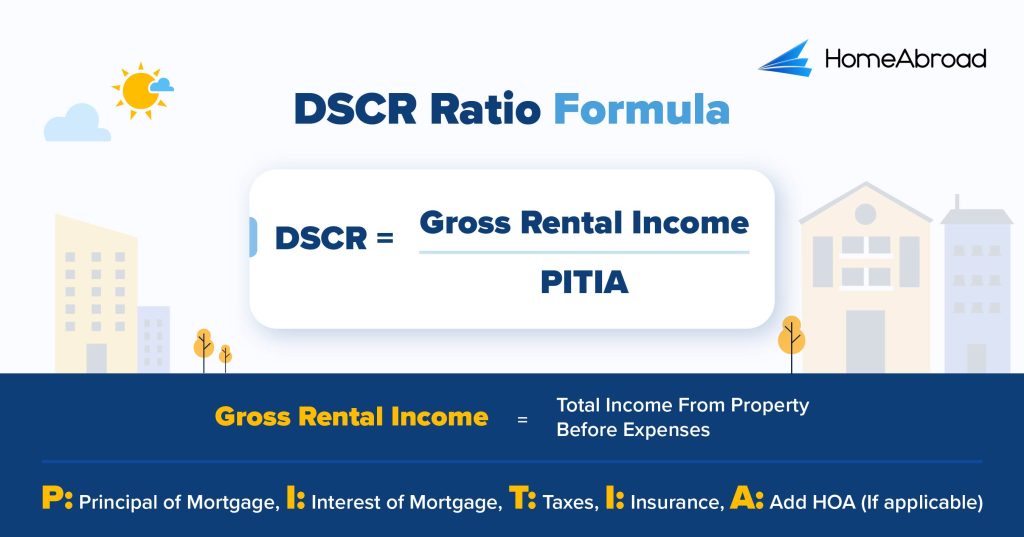

HOA Dues Inside the DSCR Calculation

One of the biggest misconceptions foreign investors have about condo DSCR loans is how HOA dues affect qualification.

In condo underwriting, HOA dues are not treated as a separate side expense. They are included directly inside PITIA, which means they reduce the property’s DSCR immediately.

The formula used is:

PITIA includes:

- Principal

- Interest

- Taxes

- Insurance

- HOA dues

In our experience, many investors calculate DSCR using only the mortgage payment and property taxes, then discover during underwriting that the HOA dues materially change the ratio.

Earlier this year, we worked with a foreign investor evaluating a condo in Miami projected to generate about $3,000 per month in rental income. Before adding the HOA dues, the property’s monthly principal, interest, taxes, and insurance totaled roughly $1,800, producing a DSCR of:

Once the condo’s $400 monthly HOA dues were added into PITIA, the monthly obligation increased to $2,200 and the DSCR dropped to:

Nothing about the rental income changed. The HOA dues alone tightened the DSCR materially and changed the financing flexibility available on the deal.

That is why condo investors should calculate DSCR using the actual HOA dues before writing an offer, especially in luxury towers or coastal buildings where monthly association fees can become substantial.

STR Restrictions in HOA Bylaws (and Why DSCR Underwriting Checks)

If the investment strategy depends on Airbnb, VRBO, or other short-term rental income, the HOA bylaws become one of the most important documents in the transaction.

At HomeAbroad, DSCR condo underwriting reviews the project’s rental restrictions because the income strategy has to align with what the HOA legally permits.

Many resort-style condo projects allow short-term rentals, but many residential-oriented buildings do not. Common restrictions include:

- Minimum 30-day lease terms

- Seven-day minimum stays

- Annual rental caps

- Limits on the number of active STR units

- Restrictions on third-party booking platforms

What we see often in markets like Orlando and Las Vegas is foreign investors underwriting the property based on Airbnb income assumptions before anyone reviews the HOA bylaws carefully.

Local city and county STR regulations may also restrict short-term rentals independently of HOA rules. The HOA review is one layer, not the only one.

The key issue is that underwriting uses income the property can legally generate under both HOA rules and local regulations, not simply the investor’s projected strategy.

Condotel Financing: The Special Case

Condotels are not condos in the underwriting sense. They operate more like hotels, and the financing reflects that.

These properties commonly include:

- Front-desk check-in

- Daily housekeeping

- Centralized rental programs

- Hospitality-style operations

Agency-backed financing generally will not finance condotels because they fall outside standard residential condo guidelines.

DSCR financing is usually the most practical path for foreign investors purchasing these properties.

At HomeAbroad, certain DSCR condotel programs remain workable, but the underwriting structure changes significantly compared to standard condos. Investors should expect:

- Higher down payments, often around 30–35%

- Higher interest rates

- Additional review of the rental program structure

- Closer scrutiny of occupancy and income stability

The distinction here is that condotels are still financeable. They simply require a different risk framework than standard residential condos.

The Foreign National Documentation Layer for Condo Purchases

Source of Funds and Wire Transfer Trail

Condo purchases move quickly once a contract is signed. In many markets, earnest money deposits equal to roughly 5–10% of the purchase price must reach escrow within just a few days of contract acceptance. The remaining closing funds usually arrive 30–45 days later, which means the wire-transfer trail needs to be clean long before closing week begins.

For foreign national buyers, every incoming wire transfer must trace back to a documented source.

At HomeAbroad, we commonly review foreign bank statements, employer income documentation, foreign business income records, brokerage-account statements, and asset-sale documentation where applicable. Some files also require translated financial documents depending on the country, institution, and transfer structure involved.

The operational issue usually appears when funds move through multiple international accounts before reaching escrow. What we see often is buyers consolidating money between personal accounts, family accounts, or business entities shortly before closing, which then creates additional documentation requirements during underwriting.

Third-party wires create another layer entirely. If funds come from parents, relatives, or foreign business partners, the transaction may require gift documentation, ownership verification, or additional source-of-funds review.

The paper trail should be organized before the condo contract is signed, not while escrow deadlines are already running. Buyers using overseas funds should also understand how source-of-funds documentation works for foreign national mortgage underwriting before moving money internationally.

Reserves for Condo Purchases

Most foreign national DSCR condo programs require reserve funds remaining after closing.

At HomeAbroad, reserve requirements for condos commonly range between 6–12 months of PITIA.

The important detail is that condo reserves include HOA dues inside the calculation.

For example:

- Monthly PITIA including HOA: $2,800

- Six months reserves: $16,800

- Twelve months reserves: $33,600

Reserve assets can often remain in foreign or US financial accounts, although certain programs may apply adjustments or reduced weighting to overseas reserves depending on the institution and liquidity profile.

What catches many condo investors off guard is that higher HOA dues increase both the monthly PITIA obligation and the reserve requirement at the same time.

Remote Closings and Power of Attorney

Most foreign national condo purchases close remotely.

The two most common structures are:

- Power of Attorney (POA) allowing a US-based attorney or representative to sign on the buyer’s behalf

- Remote online notarization where state law permits fully digital closings

For POA structures, foreign buyers often execute documents through the nearest US consulate or approved international notarization process.

What we see often is buyers underestimating how long consulate appointments and authentication steps can take. In many cases, POA preparation should begin at least 4–6 weeks before closing rather than waiting until final loan approval.

Common Mistakes Foreign Investors Make on Condo Deals

One pattern we’ve noticed across foreign national condo transactions is that most financing problems start long before underwriting officially begins. The issue is usually not the loan itself. It is the timing of when key condo-project and operational questions get addressed.

Signing the Contract Before Reviewing Warrantability

What we see often is buyers falling in love with a condo unit, signing the contract quickly, and only later discovering the building has warrantability issues.

Sometimes the HOA has active litigation. Sometimes the building is investor-heavy. Sometimes the project operates too similarly to a hotel for conventional financing to work.

The problem is not always that the deal becomes unfinanceable. The issue is that the financing structure changes after the contract is already signed, which can compress timelines and create avoidable underwriting pressure.

At HomeAbroad, our pre-qualification review helps identify warrantability and condo-project risks before buyers move fully into escrow.

Underwriting the Deal Using Airbnb Income Without Checking HOA Rules

What we see often in Orlando, Miami, and Las Vegas condo markets is foreign investors underwriting a deal using projected Airbnb income before anyone checks whether the HOA actually allows short-term rentals.

Later in the process, underwriting reviews the condo bylaws and finds:

- Minimum lease restrictions

- Rental caps

- Waiting periods

- Prohibitions on Airbnb-style activity

Once the file shifts from projected STR income to long-term market rent, the DSCR can change materially.

Confirm HOA rental rules before you underwrite the deal as a short-term rental investment.

Assuming the HOA Master Policy Covers Everything

Another common misunderstanding involves condo insurance. Many international buyers assume the HOA’s master insurance policy fully protects the individual unit. In reality, the master policy usually covers only the structure and common areas.

The buyer still typically needs an HO-6 walls-in policy covering interior finishes, personal property, liability exposure, and certain loss assessments.

This becomes especially important in coastal condo markets where wind deductibles, flood exposure, and named-storm exclusions can materially affect carrying costs and reserve planning.

At HomeAbroad, insurance review is built into the condo underwriting process so coverage issues surface before closing documents are finalized.

Waiting Too Long to Start the HOA Questionnaire Process

The HOA questionnaire is one of the biggest timing bottlenecks in condo financing.

What we see often is buyers focusing heavily on borrower documents while nobody orders the HOA package until halfway through escrow. Then underwriting stalls for another 7–14 business days waiting for the management company to respond.

Many HOA management companies also charge document-processing fees and will not begin preparing the package until payment is received.

Starting the HOA questionnaire process immediately after contract acceptance usually prevents the biggest condo-underwriting delays later in the transaction.

At HomeAbroad, we typically coordinate HOA-document requests early in the process because condo underwriting cannot move efficiently without the project documentation.

Delaying LLC Formation Until the Final Week Before Closing

Foreign investors commonly purchase condos through US LLC structures for liability and estate-planning purposes.

The issue is that LLC vesting affects multiple parts of the transaction simultaneously:

- Insurance binders

- HOA ownership records

- Title preparation

- Closing documents

- Entity verification during underwriting

A pattern we’ve noticed is buyers forming the LLC too late in the process, which then creates last-minute insurance and title delays before funding.

The cleaner approach is to form the LLC early and coordinate the entity structure, insurance setup, and ownership documentation in parallel rather than sequentially.

How We Finance Foreign National Condo Purchases at HomeAbroad

At HomeAbroad, we finance foreign national condo purchases through three primary structures depending on the property type, rental strategy, and borrower profile.

Our DSCR loans are most commonly used for investment-focused purchases where the property’s rental income supports qualification. This structure is often the best fit for:

- Long-term rental condos

- Short-term rental condos where HOA bylaws allow STR activity

- Non-warrantable condo projects

- Investor-heavy resort markets

Because DSCR qualification focuses primarily on property cash flow rather than personal income, the process is usually faster and more operationally flexible for buyers living abroad. Most DSCR condo transactions close in roughly 30–45 days depending on HOA response times and appraisal complexity.

For buyers purchasing second homes, vacation condos, or higher-value residential units, we also offer full-documentation loans. These files involve a deeper review of foreign income, assets, source of funds, and international financial documentation, so timelines are typically closer to 35–50 days.

Bridge financing is generally used in shorter-term scenarios such as condo renovations, transitional acquisitions, or properties that may not yet qualify for long-term DSCR financing.

To be clear, DSCR rates typically run higher than conventional financing. The tradeoff is property-based qualification, operational flexibility for foreign buyers, and access to condo projects that conventional agency lenders may not finance at all.

If you are evaluating a US condo purchase as a foreign investor, the best starting point is usually a pre-qualification review before making an offer. That allows us to identify warrantability, HOA, insurance, DSCR, and documentation issues early rather than discovering them during underwriting.

Next Steps If You Are Buying a US Condo from Abroad

Before signing a condo contract, make sure the financing structure actually fits the project, the HOA rules, and your investment strategy. The best starting point is usually getting pre-qualified early, pulling the HOA documents before escrow timelines tighten, and running the DSCR calculation using the real HOA dues, insurance costs, and rental restrictions tied to the building.

At HomeAbroad, we offer foreign national condo financing through DSCR loans and full-documentation loans, depending on the property and borrower profile. Our DSCR loans are designed for foreign investors who may not have a US credit history, Social Security numbers, or personal income documentation in the United States. We also help international buyers with:

- LLC setup for US property ownership

- US bank account setup guidance

- Remote closing coordination

- Reserve requirement planning

- DSCR viability review before application

Talk to our foreign national mortgage team to review your condo scenario, confirm the right financing structure, and get pre-qualified before making an offer on the property.

FAQS

Can foreign nationals finance a non-warrantable condo in the US?

Yes. At HomeAbroad, we finance many non-warrantable condo projects through DSCR and foreign national loan programs. A condo failing conventional agency guidelines does not automatically mean the project is unfinanceable. The condo project, HOA structure, insurance profile, and rental strategy still need to pass underwriting review.

What is the minimum down payment for a foreign national condo loan?

Most foreign national condo loans require around 20–25% down for standard DSCR structures. Certain condo projects, condotels, short-term rental properties, or higher-risk non-warrantable projects may require larger down payments, sometimes closer to 30–35%.

Are condotels eligible for DSCR financing?

Yes, certain condotels can qualify through HomeAbroad’s DSCR programs. These properties usually require higher down payments, higher reserves, and more specialized underwriting because the project operates more like a hospitality asset than a traditional residential condo.

How long does the HOA questionnaire process take?

In most condo transactions, the HOA questionnaire process takes roughly 7–14 business days after the request is submitted. Some HOA management companies move faster, while others require additional processing fees and extended review times. Starting the HOA-document request immediately after contract acceptance usually prevents underwriting delays later.

Can I hold the condo in an LLC as a foreign national?

Yes. Many foreign investors purchase US condos through a US LLC for liability separation and long-term ownership structuring. At HomeAbroad, we regularly finance LLC-held condo purchases for foreign nationals, although the LLC documentation, insurance setup, and title structure must align correctly before closing.

Does the HOA fee count against my DSCR ratio?

Yes. HOA dues are included inside PITIA for DSCR calculations. That means higher HOA fees directly reduce the property’s DSCR ratio and can materially affect qualification, reserve requirements, and maximum loan sizing.

What insurance do I need on a US condo if I live abroad?

A financed condo purchase typically involves two insurance layers: the HOA master policy covering the building structure and a separate HO-6 walls-in policy covering the interior of the unit, liability exposure, personal property, and loss assessments. Coastal condo markets may also involve separate windstorm or flood coverage requirements.

Can I close on a US condo without flying to the US?

Yes. Most foreign national condo purchases close remotely. At HomeAbroad, we regularly coordinate remote closings using Power of Attorney structures, approved online notarization systems, and international signing procedures depending on the property state and transaction setup.

Why did my agency lender decline this condo when DSCR financing may still work?

Agency-backed condo financing follows strict Fannie Mae and Freddie Mac warrantability rules tied to occupancy ratios, litigation exposure, reserve funding, commercial space percentages, and ownership concentration. DSCR condo underwriting uses a different review framework because it is non-QM financing. In some cases, a condo project that fails agency rules may still qualify through DSCR underwriting based on rental viability, HOA stability, insurance structure, and overall project performance.