Editorial Integrity

Making informed real estate decisions starts with having the right knowledge. At HomeAbroad, we offer US mortgage products for foreign nationals & investors and have a network of 500+ expert HomeAbroad real estate agents to provide the expertise you need. Our content is written by licensed mortgage experts and seasoned real estate agents who share insights from their experience, helping thousands like you. Our strict editorial process ensures you receive reliable and accurate information.

Key Takeaways

1. Most DSCR loans include a prepayment penalty period that lasts 3 to 5 years.

2. Prepayment penalties are typically calculated as a percentage of the outstanding loan balance at the time of payoff.

3. Choosing a prepayment penalty structure often results in a lower interest rate, with rate reductions commonly ranging from 0.25% to 0.50% compared to comparable no-penalty options.

4. Foreign national investors should evaluate additional exit risks, including visa changes, capital repatriation needs, currency fluctuations, and entity restructuring considerations.

Table of Contents

Most DSCR loans include a prepayment penalty, which is a fee charged if you pay off the loan early through a property sale, refinance, or certain large principal paydowns before the penalty period expires. The most common structures are 3-year and 5-year step-down schedules, such as 3/2/1 or 5/4/3/2/1.

Having helped foreign national investors finance US rental properties across dozens of US markets, we’ve found that prepayment penalties are often misunderstood until an investor needs to sell or refinance earlier than expected. These penalties exist because DSCR loans are non-QM products that are often held in portfolio or securitized. When a loan is paid off earlier than expected, the anticipated interest income is reduced, so the prepayment penalty helps offset that loss.

For international investors, the original business plan is not always the final one. A refinancing opportunity may emerge, capital may need to be repatriated to an investor’s home country, or a change in residency or visa plans may accelerate an exit timeline. An investor who doesn’t account for the penalty structure can face a five-figure fee on a sale or refinance they expected to be straightforward.

What Is a DSCR Loan Prepayment Penalty?

A DSCR loan prepayment penalty is a fee charged when a borrower pays off the loan before the end of the agreed penalty period. This most commonly happens when an investor sells the property or refinances the loan, but it can also be triggered by certain large principal reductions. The fee compensates for interest income the lender expected to earn when the loan was originally priced.

For foreign national investors, this feature often comes as a surprise because it is significantly more common on DSCR loans than on conventional residential mortgages.

How the Penalty Is Triggered

A DSCR loan prepayment penalty is typically triggered by one of three events: selling the property, refinancing the loan through either a rate-and-term or cash-out refinance, or making principal payments that exceed the program’s annual allowance.

Regular monthly principal and interest payments do not trigger the penalty. Standard amortization is expected and already factored into the loan structure. The issue arises when a borrower pays down a substantial portion of the balance ahead of schedule.

At HomeAbroad, we encourage investors to review their loan documents carefully before making large principal reductions. Partial paydown provisions vary by program. Some loans allow additional principal payments up to a specified annual limit, while amounts above that threshold may trigger a prepayment fee on the excess portion.

Steven Glick

Director of Mortgage Sales · HomeAbroad

Partial principal paydowns above your loan’s annual threshold can trigger the prepayment penalty on the excess amount. Borrowers should review the prepayment penalty section of their loan documents before making large principal reductions. The amount that can be paid without triggering the penalty varies by loan program.

Why DSCR Loans Have Longer Penalty Windows Than Conventional Mortgages

The biggest reason DSCR loan prepayment penalties differ from conventional mortgage penalties is that DSCR loans are non-QM products. Qualified Mortgages (QM) are subject to consumer protection rules under Dodd-Frank that limit prepayment penalties to a maximum of three years. DSCR loans, as investment-property loans, are not governed by those same restrictions.

Many DSCR loans are either held in portfolio or packaged into private mortgage-backed securities (MBS). In both cases, investors and capital providers rely on projected interest payments over a defined period. When a DSCR loan is securitized, bondholders purchase expected cash flows. A borrower who sells in Year 1 collapses that cash flow, and the penalty compensates the pool.

This is why DSCR programs commonly include 3-year and 5-year penalty periods, and why the percentages can be higher than investors expect when comparing them to conventional financing.

DSCR Prepayment Penalty Structures: Step-Down, Flat, and No-Penalty

The penalty option you select affects both your future flexibility and the interest rate you receive at closing. The right structure depends largely on how long you expect to keep the loan. An investor planning to hold a property for ten years evaluates prepayment penalties very differently from someone expecting to refinance within two or three years.

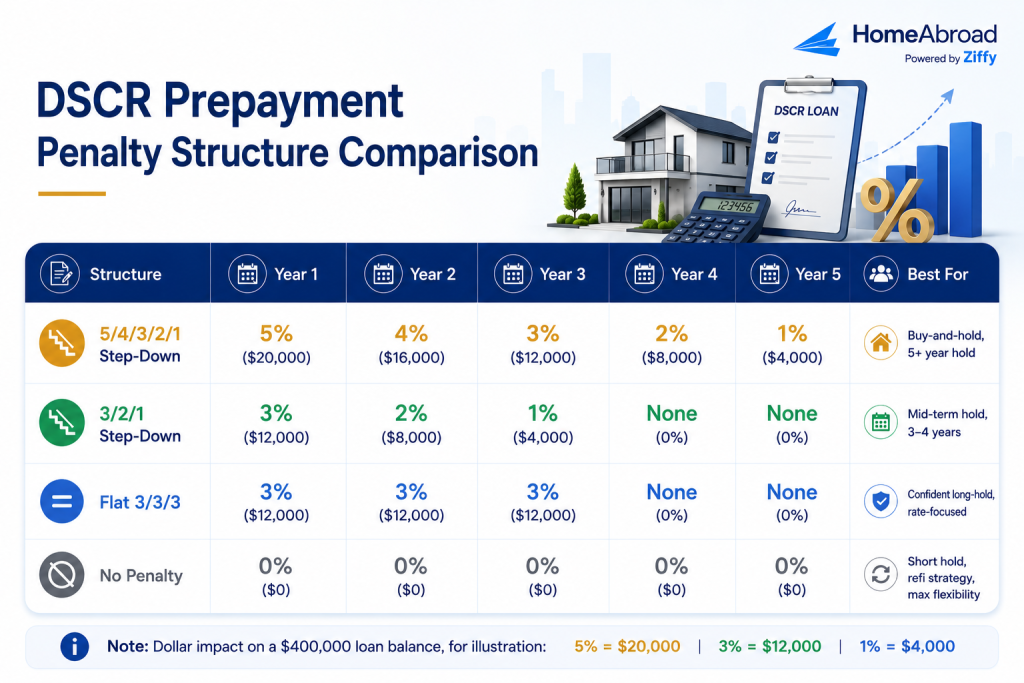

The Step-Down Structure (5/4/3/2/1 and 3/2/1)

The step-down structure is the most common prepayment penalty format in the DSCR market. Under this approach, the penalty percentage decreases each year until it eventually expires.

A 5/4/3/2/1 structure means the penalty is 5% of the outstanding loan balance if the loan is paid off in Year 1, 4% in Year 2, 3% in Year 3, 2% in Year 4, and 1% in Year 5. After Year 5, the penalty no longer applies.

A shorter 3/2/1 structure follows the same concept but expires after three years. Because the lender has a shorter period to recover expected interest income, this option may carry slightly different pricing than a longer step-down structure.

On a $400,000 loan balance, paying off the loan during Year 1 under a 5/4/3/2/1 schedule would result in a $20,000 penalty. A payoff in Year 3 would cost $12,000. A payoff in Year 6 would incur no penalty.

Across the 500+ DSCR loans we’ve helped investors finance, the 5/4/3/2/1 step-down has consistently been the most commonly selected structure among buy-and-hold investors, particularly those targeting a 7- to 10-year investment horizon.

The Flat-Fee Structure (3/3/3 or 5/5/5)

A flat-fee structure works differently because the penalty percentage remains unchanged throughout the entire penalty period.

For example, a 3/3/3 structure applies a 3% penalty whether the loan is paid off in Year 1, Year 2, or Year 3. A 5/5/5 structure follows the same concept for a longer period. Unlike a step-down schedule, there is no gradual reduction as the loan ages.

This structure is generally less attractive for investors who may sell or refinance midway through the penalty window because the cost remains the same regardless of timing. The trade-off is that flat-fee structures are often paired with the most favorable rate pricing. They are typically best suited for investors who are highly confident they will hold the property for at least five years and want to prioritize rate reduction.

No-Penalty Option

Some DSCR programs offer a no-prepayment-penalty option, allowing investors to sell, refinance, or pay off the loan without incurring an early payoff fee.

The flexibility comes at a cost. No-penalty programs typically carry an interest rate that is approximately 0.25% to 0.50% higher than a comparable step-down structure. For investors planning to hold a property long term, that higher rate can outweigh the benefit of avoiding a penalty that may never be triggered.

A no-penalty structure is often a strong fit for investors with a planned hold period of less than three years, borrowers pursuing a refinance strategy, or foreign national investors who anticipate potential changes that could require an earlier-than-expected exit. Availability depends on the loan program, LTV, property type, and overall borrower profile.

With foreign national investors, the hold period is only the starting point. We’ve had investors focus heavily on rate during the application process, then realize later that flexibility was more important because they planned to refinance sooner than expected.

How Prepayment Penalty Affects Your DSCR Loan Interest Rate

A DSCR loan’s prepayment penalty structure directly affects the interest rate you receive at closing. When an investor accepts a longer or more restrictive prepayment penalty, the loan becomes more predictable from a pricing perspective.

The lender and secondary market investors have greater confidence that the expected interest income will be realized over a longer period. That reduced risk is typically reflected in a lower interest rate.

In most DSCR scenarios, the difference between a no-penalty option and a 5-year step-down structure is approximately 0.25% to 0.50%, although pricing varies by DSCR ratio, LTV, property type, loan amount, and market conditions.

Consider a $400,000 DSCR loan. A 0.375% rate reduction translates to roughly $1,500 less interest expense per year. Over a five-year hold period, that’s approximately $7,500 in savings. For an investor who plans to own the property for at least five years, those savings are realized every month through a lower borrowing cost.

This is where many investors evaluate the decision incorrectly. The conversation often starts with avoiding a future penalty rather than calculating the cost of carrying a higher rate. If the property is expected to remain in the portfolio for the full penalty period, the prepayment penalty may never be triggered. The interest savings, however, begin immediately and continue throughout the hold.

At HomeAbroad, we review both sides of the equation before structuring a loan. Instead of focusing solely on the penalty percentage, we compare the projected interest savings against the potential cost of an early exit.

DSCR rates change frequently and vary based on factors such as DSCR ratio, LTV, property type, loan amount, borrower profile, and market conditions. Any rate examples are for illustration only and do not constitute a rate lock or lending commitment.

As of August 2026, HomeAbroad’s foreign national DSCR baseline rate is approximately 7.00% for well-qualified scenarios. Rate adjustments for different prepayment penalty structures vary by program and market conditions, so investors should confirm current pricing with a HomeAbroad loan specialist before locking a loan.

Jason Saylor

Sr. Customer Loan Specialist

HomeAbroad

NMLS #2594493We’ve worked with investors who initially wanted a no-penalty option, but after comparing five years of additional interest costs against their actual exit plans, they realized a lower-rate step-down structure could save more than $7,000 on a $400,000 loan.

Rate-vs-Penalty Trade-Off Illustration

Penalty Option | Estimated Rate Adjustment | Monthly Payment on $400K | 5-Year Interest Savings vs. No-Penalty |

|---|---|---|---|

No Penalty | +0.375–0.50% | Higher | Baseline |

3/2/1 Step-Down | +0.125–0.25% | Moderate | ~$3,500–$5,000 |

5/4/3/2/1 Step-Down | Par / Baseline | Lower | ~$7,000–$10,000 |

Flat 3/3/3 | Below Par | Lowest | ~$10,000+ |

Rates and pricing adjustments vary by DSCR ratio, LTV, property type, occupancy strategy, and overall loan structure. Confirm current pricing with a HomeAbroad loan specialist for a scenario-specific comparison.

What Foreign National Investors Must Evaluate Before Selecting a Penalty Structure

The standard question when selecting a prepayment structure is how long you plan to hold the property. For foreign national investors, that answer is only part of the equation because events outside the property itself can alter the timeline.

International real estate investors should evaluate more than projected appreciation and interest rate trends when selecting a prepayment structure. The right option depends on how likely you are to encounter an event that could require a sale, refinance, ownership transfer, or capital withdrawal before the penalty period expires.

Note: Standard DSCR prepayment penalty guidance assumes the exit decision is voluntary and market-driven. International investors may face timeline changes driven by capital movement requirements, ownership restructuring, or cross-border financial considerations that have little to do with property performance.

Exit Scenarios Unique to International Investors

1. Visa status and residency changes

A change in immigration status can affect how an investor manages US real estate holdings. In some situations, an investor may decide to sell, transfer ownership, or refinance a property after a visa expires, a residency plan changes, or travel restrictions make active management more difficult. These decisions are not typically part of the original investment plan, but they can occur during the prepayment penalty period.

2. Repatriation of capital

Some countries periodically adjust foreign investment rules, reporting requirements, or capital transfer regulations. When those changes occur, investors may need to liquidate US assets on a timeline driven by regulatory requirements rather than market conditions.

3. Currency risk can magnify the real cost

Prepayment penalties are calculated and paid in US dollars. If an investor’s home currency weakens significantly against the dollar after the loan closes, the effective cost of a $15,000 or $20,000 penalty becomes much higher when converted back into local currency. This additional layer of risk should be considered when comparing a lower-rate loan with a penalty against a higher-rate no-penalty option.

4. LLC ownership changes

Many foreign nationals purchase US investment properties through LLC structures for liability protection and ownership planning purposes. However, transferring LLC membership interests, restructuring ownership, or dissolving the entity may be treated as a transfer event under loan documents.

Depending on the circumstances, a transfer may trigger provisions contained in the loan documents, making it important to review ownership changes before they are completed.

5. Estate and inheritance considerations

Non-resident investors may also face estate planning considerations that domestic borrowers do not. The death of a co-owner, partner, or beneficiary can create situations where assets must be transferred, refinanced, or sold unexpectedly. A prepayment penalty does not automatically disappear because an ownership change is tied to an estate matter.

Steven Glick

Director of Mortgage Sales · HomeAbroad

We’ve worked with investors who originally planned a long-term hold but later needed to move capital for reasons unrelated to the property. In those situations, the prepayment structure became far more important than the original investment projections.

See our guide to DSCR loans for long-term rentals as a foreign national for additional considerations when structuring a long-term US investment strategy.

How to Choose the Right Prepayment Structure for Your Investment Strategy

The decision comes down to two numbers: how long you expect to keep the loan and how much interest savings you’re receiving in exchange for the prepayment penalty.

For investors with a confirmed buy-and-hold strategy of five years or longer, a 5/4/3/2/1 step-down or flat-fee structure often makes the most financial sense. The lower interest rate creates savings throughout the hold period, while the risk of triggering the penalty remains low because the planned exit occurs after the penalty window expires.

Investors targeting a three- to four-year hold period typically benefit from a 3/2/1 step-down structure. It provides some rate advantage while allowing the penalty period to expire before the anticipated sale or refinance.

A no-penalty option is often the better fit when the timeline is uncertain or a refinance is part of the strategy. Paying a slightly higher rate can be worthwhile if interest rates decline, market conditions shift, or personal circumstances create a need for flexibility during the first few years of ownership.

Match Your Hold Period to Your Penalty Structure

Planned Hold Period | Recommended Structure | Rationale |

|---|---|---|

1–2 years | No Penalty | Penalty cost often exceeds potential rate savings |

3–4 years | 3/2/1 Step-Down | Penalty period aligns with expected exit timeline |

5+ years | 5/4/3/2/1 Step-Down | Rate savings are fully realized while penalty risk remains minimal |

Uncertain / Refinance Likely | No Penalty | Flexibility has greater value than rate optimization |

Buy-and-Hold / No Planned Sale | Flat Structure (3/3/3 or 5/5/5) | Lowest rate potential; penalty is unlikely to be relevant |

Jason Saylor

Sr. Customer Loan Specialist

HomeAbroad

NMLS #2594493Before we discuss rate options, I ask foreign national investors three questions: Could your residency or visa plans change in the next few years? Is there any reason you might need to move capital out of the US sooner than expected? And would ownership of the property or LLC likely change during the hold period? By the third question, I usually have a good sense of whether they need the flexibility of a no-penalty option or whether a step-down structure is the better fit.

Common Mistakes Investors Make With Prepayment Penalties

Prepayment penalties rarely surprise investors because they were hidden in the loan documents. The bigger issue is how often borrowers underestimate the impact a penalty structure can have on the total cost of financing.

1. Choosing a No-Penalty Option Without Running the Numbers

Some investors assume a no-penalty loan is automatically the safer choice. In practice, that higher rate can become an expensive form of flexibility. On a $400,000 loan, approximately $7,500 in interest savings over five years can outweigh a prepayment penalty that never comes into play because the property is held beyond the penalty period.

2. Confusing the Penalty Period With the Loan Term

A 30-year DSCR loan with a 5/4/3/2/1 prepayment penalty does not have a 30-year penalty. The penalty applies only during the first five years and then expires. We’ve seen investors reject a lower-rate option because they assumed the penalty remained in place for the entire loan term when it actually ended long before their planned exit.

3. Making Large Principal Payments Without Reviewing the Loan Terms

Some investors use excess cash flow to pay down principal aggressively, expecting to reduce interest costs faster. Many DSCR loans limit how much extra principal can be paid each year. Exceeding that allowance can trigger a prepayment fee on the excess amount. Before making a large lump-sum payment, review your promissory note and confirm the annual allowance to avoid an unexpected charge.

Ready to Evaluate Your DSCR Loan Options?

The most important question is How long are you likely to keep the loan? Investors with a defined long-term hold often benefit from lower-rate step-down structures. Investors with uncertain timelines are usually better served by paying a higher rate in exchange for flexibility.

Before locking a DSCR loan, we review both the expected hold period and the events that could force an earlier exit. The wrong penalty structure often doesn’t become a problem until circumstances change, which is why it deserves the same attention as the interest rate itself.

Want to learn more? See our complete DSCR Loan Guide for a deeper look at qualification requirements, rates, and investment property financing strategies.

Get pre-qualified today to explore your DSCR loan options and compare available prepayment structures.

FAQ: DSCR Loan Prepayment Penalty

Do DSCR loans always have prepayment penalties?

No, but most do. Many DSCR loan programs include a prepayment penalty period of three to five years because lenders and investors expect to earn interest over a certain timeframe. No-penalty options are available, but they typically come with a higher interest rate.

What is the 5/4/3/2/1 prepayment penalty on a DSCR loan?

A 5/4/3/2/1 prepayment penalty decreases each year over a five-year period. The fee is 5% of the outstanding balance in Year 1, 4% in Year 2, 3% in Year 3, 2% in Year 4, and 1% in Year 5. After Year 5, the penalty no longer applies.

Can a DSCR loan be paid off early?

Yes. A DSCR loan can be paid off at any time, but doing so during the penalty period usually triggers a fee. Most programs also allow limited extra principal payments each year without penalty. Once the penalty window expires, the loan can be paid off without additional charges.

How do prepayment penalties work differently for foreign national investors?

The penalty calculation is the same, but foreign national investors often face exit scenarios that domestic investors do not. For example, a borrower may plan to hold a property for seven years but later need to sell because of visa changes, capital repatriation requirements, or ownership restructuring within an LLC. Because these events can occur during the penalty period, investors should review the loan’s prepayment provisions and ownership transfer terms before locking a program.

Can I negotiate or buy out a DSCR loan prepayment penalty?

Sometimes. Certain DSCR programs allow borrowers to reduce or eliminate the penalty by accepting a higher interest rate or paying an upfront fee at closing. Available options vary by loan program, property type, LTV, and borrower profile.

Are DSCR loan prepayment penalties enforceable in all states?

Not always. State laws determine whether prepayment penalties can be enforced and what disclosures lenders must provide. Because DSCR loans are investment property loans, many restrictions that apply to owner-occupied mortgages do not apply. Some states have additional disclosure or compliance requirements even when the penalty itself is permitted. This guide does not cover state-by-state requirements. Your loan officer and legal counsel can confirm how prepayment penalty rules apply in your state before closing.