Editorial Integrity

Making informed real estate decisions starts with having the right knowledge. At HomeAbroad, we offer US mortgage products for foreign nationals & investors and have a network of 500+ expert HomeAbroad real estate agents to provide the expertise you need. Our content is written by licensed mortgage experts and seasoned real estate agents who share insights from their experience, helping thousands like you. Our strict editorial process ensures you receive reliable and accurate information.

A no-doc mortgage means qualifying without traditional income documents such as W-2s, pay stubs, or US tax returns while still completing a full underwriting review.

For most foreign national investors, a DSCR loan is the primary no-income-verification financing option. Qualification is based primarily on the property’s rental income rather than personal employment income.

You’ll still need to provide documents such as proof of identity, property information, proof of funds, and required reserves.

A no-doc DSCR Loan is often the better fit for income-producing rental properties or when traditional income documentation is difficult to provide

A no-doc mortgage for investors lets borrowers qualify based primarily on a property’s rental income and the overall strength of the investment instead of personal income documents such as W-2s, pay stubs, or US tax returns. Rather than relying on traditional employment income, these loans evaluate whether the investment property meets the lender’s underwriting requirements.

That doesn’t mean a no-doc mortgage requires no paperwork. Modern no-income-verification loans still require documents such as proof of identity, proof of funds, property information, and, depending on the loan program, rental income documentation. The difference is that you don’t have to qualify through traditional US income verification.

For foreign national and international investors, this financing approach can make buying US rental property significantly more accessible. Instead of proving US employment history or providing US tax returns, eligible borrowers may qualify through programs such as Debt Service Coverage Ratio (DSCR) loans, which evaluate whether the property’s projected rental income can support the financing.

At HomeAbroad, we help foreign national investors and international buyers finance US investment properties through mortgage programs that align with their financial profile and investment strategy. In this guide, you’ll learn how no-doc mortgages work, who qualifies, what documents are still required, and when a no-income-verification loan makes more sense than a traditional Full Documentation Loan.

Table of Contents

What a No-Doc Mortgage Means for Investors

A no-doc mortgage is a business-purpose loan that allows real estate investors to qualify without providing traditional income documentation such as W-2s, pay stubs, or US tax returns. Instead of evaluating a borrower’s employment income, we assesses the strength of the investment, including the property’s rental income, available assets, and the overall transaction.

For foreign national investors, this financing approach can simplify the mortgage process because qualification is not tied to a US employment history or domestic tax filings. Depending on the loan program, borrowers may qualify based on the property’s ability to generate income rather than their personal earnings.

Although the term “no-doc mortgage” is still widely used, its meaning has changed over time. Today’s no-doc investor loans are legitimate mortgage products with clearly defined underwriting standards, not the loosely underwritten stated-income loans that became common before the 2008 financial crisis.

What “No-Doc” Actually Refers To Today

Modern no-doc mortgages are more accurately described as no-income-verification mortgages. They eliminate the requirement to verify personal income through documents such as:

- US tax returns

- W-2 forms

- Pay stubs

- Employment verification

- US income history

Instead, we evaluate factors that are more relevant to an investment property loan, including:

- The property’s projected or documented rental income

- Available funds for the purchase and required reserves

- The property’s appraisal

- The overall strength of the investment transaction

For many foreign national investors, this means qualifying for a US investment property without relying on traditional US employment or income documentation.

Myth vs. Reality

Myth: A no-doc mortgage means no paperwork.

Reality: A no-doc mortgage means no personal income documentation. Borrowers still provide documents such as proof of identity, property information, available funds, and other items required to complete the underwriting process.

How Investors Qualify Without Traditional Income Documentation

One of the biggest misconceptions about no-doc mortgages is that lenders simply choose not to verify a borrower’s financial profile. In reality, no-income-verification loans follow a different underwriting approach that focuses on the investment property rather than traditional personal income documentation.

For eligible investment property loans, qualification is based primarily on whether the property can support the requested financing. Instead of relying on documents such as W-2s, pay stubs, or US tax returns, lenders evaluate the property’s income potential and the overall strength of the transaction.

For foreign national investors, this approach can provide a practical financing path when traditional US income documentation is unavailable or difficult to provide.

Many investors assume ‘no-doc’ means the lender isn’t evaluating risk. That’s not how these loans work. Instead of qualifying you based on W-2s or tax returns, we evaluate whether the investment itself supports the financing. For the right rental property, that often provides a more practical qualification path than a traditional income-based mortgage.

Why the Property, Not Your Paycheck, Carries the Loan

For many investment property loans, the property’s ability to generate income is a stronger indicator of repayment than traditional employment income.

For example, HomeAbroad’s DSCR Loan evaluates whether the property’s projected rental income can reasonably support the monthly housing expense. Instead of asking whether your salary can cover the mortgage payment, the underwriting process considers whether the investment property itself produces sufficient cash flow.

This approach is particularly beneficial for foreign national investors whose income may be difficult to document under conventional US mortgage guidelines. Rather than relying on traditional personal income documentation, we evaluates the property’s income potential together with the overall strength of the transaction.

If you’d like to learn more about how rental income is evaluated, explore our DSCR Loan Guide, which explains how Debt Service Coverage Ratio (DSCR) is calculated and used during the underwriting process.

HomeAbroad’s No-Doc Financing Options for Investment Property

Not every investment property qualifies the same way, but today’s no-doc financing options share one key characteristic: they don’t require borrowers to qualify through traditional personal income documentation such as W-2s, pay stubs, or US tax returns.

At HomeAbroad, these programs focus on the property’s income potential and the overall investment rather than the borrower’s employment history.

DSCR Loans (Qualify on Rental Income)

A Debt Service Coverage Ratio (DSCR) Loan is the most common no-income-verification financing option for investment properties. At HomeAbroad, we qualify eligible borrowers primarily based on whether the property’s projected rental income can support the monthly housing expense.

This makes DSCR loans a practical option for foreign national investors who may not have US employment income or US tax returns but are purchasing an income-producing rental property.

For eligible transactions where a property’s rental income doesn’t meet the standard DSCR requirement, HomeAbroad Loans also offers No-Ratio DSCR financing. This program provides additional flexibility for qualifying investment properties with lower initial rental income while still meeting applicable underwriting guidelines.

Best for:

- Long-term rental properties

- Cash-flowing investment properties

- Foreign national investors

- Eligible lower-DSCR properties through the No-Ratio DSCR program

Bridge and Fix and Flip Loans

Although Bridge Loans and Fix and Flip Loans are not traditionally classified as no-doc mortgages, they also do not rely on traditional personal income documentation as the primary qualification method.

These short-term financing solutions are intended for investors purchasing properties that require renovation, stabilization, or another value-add strategy before they can generate consistent rental income.

At HomeAbroad, we offer these loan programs to help investors acquire and improve properties before transitioning to long-term financing, such as a DSCR Loan, once the property is ready to generate rental income.

Best for:

- Distressed properties

- Renovation projects

- Short-term investment strategies

- BRRRR investors planning a later DSCR refinance

How Qualification Works Without Tax Returns or Pay Stubs

Qualifying for a no-doc mortgage doesn’t mean qualifying without underwriting. Instead of reviewing W-2s, pay stubs, or US tax returns, we evaluate whether the investment property and the overall transaction meet our lending requirements.

For most no-income-verification investment loans, qualification focuses on the property’s rental income, available funds, credit profile, and the borrower’s ability to complete the purchase rather than traditional employment income.

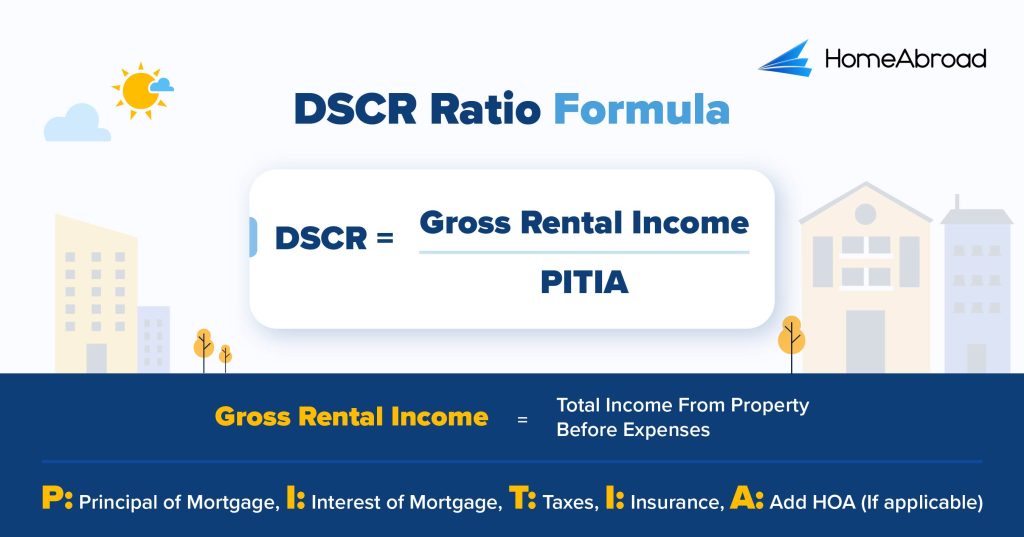

The DSCR Calculation, Step by Step

For investment properties, the primary qualification method is the Debt Service Coverage Ratio (DSCR). Rather than asking whether your salary can support the mortgage payment, we evaluates whether the property’s projected rental income can cover its monthly housing expense.

The standard calculation is:

Where:

- Gross Rental Income is the property’s market rent or documented lease income used for underwriting.

- PITIA includes the monthly Principal, Interest, Property Taxes, Insurance, and Association dues (if applicable).

In general:

- A higher DSCR indicates stronger rental income relative to the property’s monthly housing expense.

- At HomeAbroad, we generally require a DSCR of 1.0 or higher for the best financing terms.

- For eligible properties, we also offer No-Ratio DSCR Loans for investments with a DSCR below 1.0.

If you’d like to estimate a property’s DSCR before applying, use our DSCR Calculator to compare projected rental income with the property’s monthly housing expense.

Down Payment, Reserves, and LTV

In addition to evaluating the property’s income, HomeAbroad Loans also reviews several financial requirements before approving a no-doc investment loan.

These typically include:

- A minimum 25% down payment for eligible foreign national borrowers.

- At least six months of post-closing reserves to demonstrate the ability to support the investment after closing.

- The property’s Loan-to-Value (LTV) ratio, which determines the maximum financing available based on the property’s appraised value and purchase price.

Together with the property’s DSCR, these factors help determine whether the investment meets HomeAbroad’s underwriting guidelines.

What Documents You Still Need to Provide

A no-doc mortgage eliminates the need for traditional income documents such as W-2s, pay stubs, and US tax returns. It does not eliminate the documentation needed to verify your identity, the investment property, or your ability to complete the transaction.

At HomeAbroad, we review a defined set of documents to confirm the details of the borrower, the property, and the investment. Providing these documents early can help keep your loan on schedule and reduce delays during underwriting.

The Real Document Checklist

Although document requirements vary by loan program, HomeAbroad Loans generally requests:

Borrower Documents

- Valid passport or government-issued photo identification

- Visa or immigration documentation (when applicable)

- Entity formation documents if the property is being purchased through a US LLC

Property Documents

- Executed purchase agreement

- Property address and transaction details

- Property appraisal

- Market rent analysis or lease agreement, depending on the transaction

Financial Documents

- Proof of funds for the down payment and closing costs

- Documentation showing required post-closing reserves

- Source of funds, when required for underwriting or regulatory compliance

Submitting complete and accurate documentation at the beginning of the process helps our underwriting team review your file more efficiently.

Lucas Hernandez

Mortgage Loan Originator, HomeAbroad

One of the most common reasons a no-doc loan is delayed isn’t income documentation, it’s incomplete property information. Providing the purchase contract, rent documentation, proof of funds, and any required entity documents early helps our underwriting team keep the file moving toward closing.

No-Doc Financing for Foreign National Investors

Foreign national investors often assume they need US employment, a US credit history, or years of US tax returns to finance an investment property. For many investment loans, that isn’t the case.

HomeAbroad offers financing solutions specifically for foreign national investors purchasing US investment properties. For borrowers who don’t have traditional US income documentation, a Foreign National DSCR Loan allows qualification based primarily on the property’s rental income rather than personal employment income.

Qualifying Without US Income Documentation

A Foreign National DSCR Loan allows eligible borrowers to qualify without providing documents such as:

- US tax returns

- W-2 forms

- Pay stubs

- US employment verification

Instead, HomeAbroad Loans evaluates whether the property’s projected rental income can support the monthly housing expense while also reviewing the overall transaction against our underwriting requirements.

For many foreign national investors, this provides a more practical financing path because qualification isn’t tied to a US employment history.

ITIN and No-SSN Borrowers

Many foreign national investors purchase US real estate before obtaining a Social Security Number (SSN). Depending on the transaction, an Individual Taxpayer Identification Number (ITIN) may be required for tax reporting purposes, but mortgage qualification and tax obligations are separate matters.

Because ITIN requirements vary based on your ownership structure and tax circumstances, HomeAbroad Loans recommends working with a qualified tax professional to determine whether an ITIN is needed for your investment.

Buying Through a US LLC

Many foreign national investors choose to purchase US investment properties through a US Limited Liability Company (LLC) for business, liability, or tax-planning reasons.

At HomeAbroad, we finance eligible investment properties purchased through an LLC, provided the transaction meets our underwriting guidelines. If you’re considering this ownership structure, it’s important to establish the entity before closing and consult qualified legal and tax professionals to determine whether purchasing through an LLC aligns with your investment objectives.

For borrowers who prefer to qualify based on verified income documentation from their home country, we also offer Full Documentation Loans. Comparing both options can help you determine which financing approach best fits your financial profile and investment goals.

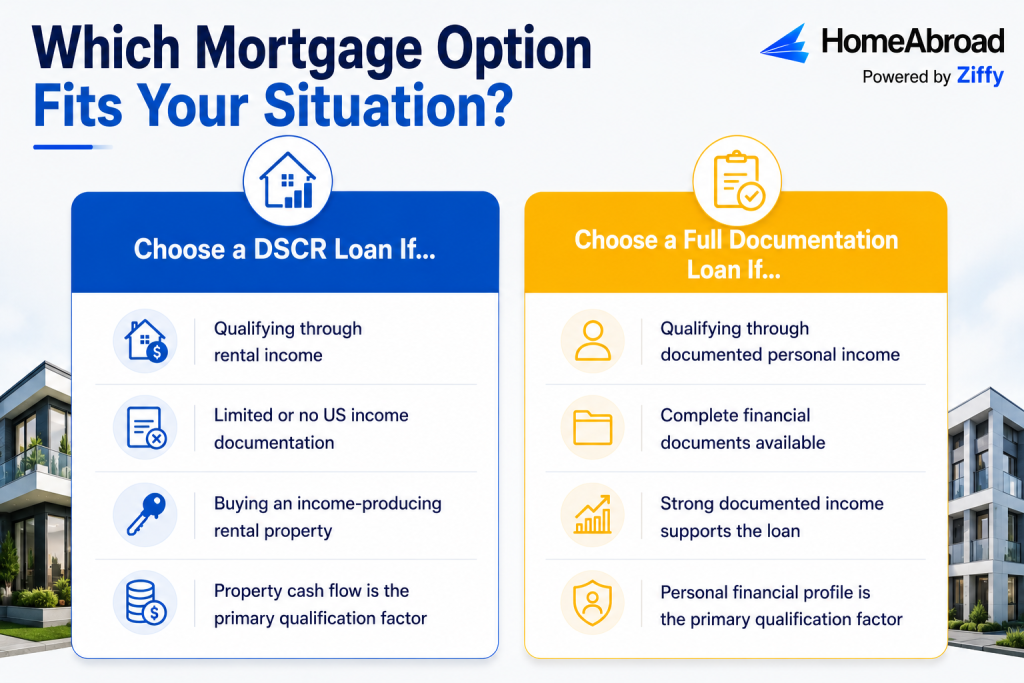

When a No-Doc Loan Fits and When Full Documentation Is Better

No-doc financing isn’t the right solution for every investor. While a DSCR Loan can simplify qualification for borrowers without traditional US income documentation, a Full Documentation Loan may provide better financing terms for borrowers who can verify their income and financial profile.

The best choice depends on how you qualify, the property you’re purchasing, and your long-term investment strategy.

When a No-Doc Loan Is the Right Path

A no-income-verification loan may be the better option if:

- You’re purchasing an income-producing investment property.

- The property’s rental income is strong enough to support DSCR qualification.

- You don’t have US tax returns, W-2s, or pay stubs.

- Your income is earned outside the United States and isn’t easily documented under conventional US mortgage guidelines.

- You’re looking for a financing process built around the investment property rather than your employment history.

For many foreign national investors, a DSCR Loan provides the most practical qualification path because the property’s rental income becomes the primary factor in the underwriting process.

When a Full Documentation Loan Serves You Better

A Full Documentation Loan may be the better choice if:

- You can provide complete financial documentation from your home country.

- Your income is stable, well documented, and supports conventional underwriting.

- You’re looking to qualify based on your personal financial strength rather than the property’s rental income.

- The investment property may not meet DSCR qualification, but your documented income supports the requested financing.

For eligible foreign national investors, we accepts qualifying financial documentation from the borrower’s home country as part of the Full Documentation Loan underwriting process.

Need Help Deciding?

Some investors qualify for more than one mortgage program, while others may benefit from discussing their financing options before choosing a loan.

Our mortgage specialist can review your investment strategy, documentation, and property details to help determine whether a DSCR Loan or a Full Documentation Loan is the better fit for your financing goals.

How to Get a No-Doc Investor Mortgage With HomeAbroad

If you’ve determined that a no-income-verification loan is the right fit for your investment strategy, the next step is understanding how the mortgage process works. While every transaction is different, the overall process is straightforward and focuses on the investment property rather than traditional income documentation.

Step 1: Discuss Your Financing Goals

Start by speaking with a HomeAbroad Loans mortgage specialist about your investment strategy, the type of property you’re planning to purchase, and the loan program that best fits your situation. If you’re still evaluating properties, obtaining a pre-approval can help you understand your financing options before you begin your property search.

Step 2: Submit Your Loan Application

Once you’ve identified a property and your offer has been accepted, you’ll complete the loan application and provide the documents required for your chosen loan program. For a DSCR Loan, the focus is on the property’s income potential and the overall transaction rather than traditional US income documentation.

Step 3: Property Review and Underwriting

At HomeAbroad, we coordinate the appraisal and underwriting review to verify that the property and transaction meet program requirements. During this stage, our team may request additional information or documentation to complete the review.

Step 4: Close on Your Investment Property

After all underwriting conditions have been satisfied, you’ll review your final loan documents and complete the closing process. From there, you’ll be ready to take ownership of your US investment property.

Whether you’re purchasing your first US rental property or expanding an existing investment portfolio, we offers mortgage solutions tailored to foreign national investors.

Connect with HomeAbroad today to discuss your goals, explore your mortgage options, and take the next step toward owning US investment property.

Frequently Asked Questions

Is a no-doc mortgage the same as a no credit check mortgage?

No. A no-doc mortgage means you don’t qualify using traditional income documents such as W-2s, pay stubs, or US tax returns. HomeAbroad Loans still evaluates the investment property and the overall transaction as part of the underwriting process. Qualification requirements vary by loan program.

Can I get a no-doc mortgage without a Social Security Number (SSN)?

Yes, depending on the loan program. Many foreign national investors purchase US investment property without a Social Security Number. In some cases, an Individual Taxpayer Identification Number (ITIN) may be required for tax reporting purposes. Your mortgage specialist can explain the documentation requirements for your situation.

Does getting a no-doc mortgage affect my visa or immigration status?

No. Purchasing US real estate or obtaining a mortgage does not provide a visa, permanent residency, or any other immigration benefit. Mortgage financing and US immigration status are governed by separate rules.

Can I qualify for a no-doc mortgage if I don’t have US income?

Yes. Eligible foreign national borrowers may qualify through a Foreign National DSCR Loan, which evaluates the property’s rental income instead of requiring US employment income or tax returns.

How do I know whether a no-doc loan or a Full Documentation Loan is right for me?

The right option depends on how you qualify. If you want to qualify based primarily on a property’s rental income, a Foreign National DSCR Loan may be the better fit. If you can provide complete financial documentation from your home country, a Full Documentation Loan may offer another financing option. A HomeAbroad Loans mortgage specialist can help you compare both programs based on your investment goals.