Editorial Integrity

Making informed real estate decisions starts with having the right knowledge. At HomeAbroad, we offer US mortgage products for foreign nationals & investors and have a network of 500+ expert HomeAbroad real estate agents to provide the expertise you need. Our content is written by licensed mortgage experts and seasoned real estate agents who share insights from their experience, helping thousands like you. Our strict editorial process ensures you receive reliable and accurate information.

Key Takeaways

1. HomeAbroad offers DSCR Loans for Short-Term Rentals that allow eligible foreign national investors to qualify using property income instead of US employment income or tax returns.

2. We can help qualify Airbnb and VRBO properties using appraisal-supported income projections or documented operating history, depending on the property and loan program.

3. Property eligibility matters. HOA restrictions, local short-term rental regulations, and lender-specific STR guidelines can affect whether a property qualifies for financing.

4. Our team helps foreign investors navigate the entire process, including DSCR qualification, source-of-funds documentation, LLC ownership structures, reserves, underwriting, and remote closings.

Table of Contents

Many foreign investors discover the same problem when they start looking at US short-term rental properties. Airbnb and VRBO income may be generating strong cash flow, but traditional mortgage programs often struggle to use that income for qualification. The challenge becomes even more complicated for foreign nationals who may not have US credit history, US tax returns, or US employment income.

At HomeAbroad, we’ve helped investors from more than 40 countries close over 500 DSCR loans for US investment properties. One pattern we see consistently is that investors often understand how Airbnb income works operationally, but not how we evaluate that income during the underwriting process.

The good news is that qualifying for a DSCR loan for short-term rentals is possible even without US income documentation. The key is understanding how lenders measure rental income, what appraisal methods they use, which properties qualify, and where underwriting issues typically arise.

This guide focuses on the part most competitors skip: how Airbnb and VRBO income is actually qualified for DSCR loans. You’ll learn the two primary income-qualification methods, how appraisers evaluate short-term rental performance, what eligibility requirements apply, and the most common approval challenges that can delay or derail a transaction.

How STR Income Is Qualified: The Two Underwriting Paths

Purchase with No Operating History: Market-Rent Projection

When a foreign national purchases a short-term rental property that does not have an established operating history, we cannot rely on Airbnb or VRBO statements because no performance data exists yet.

Instead, we typically rely on a market-rent projection prepared during the appraisal process. Depending on the loan program, the appraiser may use AirDNA, Rabbu, or similar short-term rental data providers to estimate projected revenue based on comparable properties, occupancy patterns, nightly rates, and local market performance.

One distinction many investors miss is that projected Airbnb income and appraised rental income are not always the same thing. AirDNA and similar platforms provide market-based revenue estimates, while the appraiser determines the income figure that ultimately supports the valuation and underwriting decision.

If those figures differ, we generally rely on the income amount supported by the appraisal and program guidelines rather than the host’s personal revenue projections.

Refinance or Seasoned Property: Actual Operating Performance

For refinance transactions or properties with an established rental history, we often evaluate actual short-term rental performance instead of relying solely on market projections.

This typically requires 12 months of Airbnb or VRBO host statements, property-management-system (PMS) reports, or other documented rental-performance records. Underwriting reviews the property’s trailing income history to determine whether the rental operation generates enough cash flow to support the proposed loan.

What most guides don’t mention is that we often distinguish between gross booking revenue and the actual income received by the property owner after platform fees. Airbnb service charges, management fees, and other deductions can affect the final income figure used during underwriting.

Clean documentation and consistent reporting become critical because lenders must verify exactly how much income the property is producing.

How Seasonality and Vacancy Affect STR Qualification

Unlike long-term rentals with fixed lease payments, short-term rental income can fluctuate significantly throughout the year. A beach property may generate exceptional revenue during peak season but experience much lower occupancy during slower months.

Because of this variability, we do not simply annualize a property’s best-performing months when evaluating short-term rental income. Underwriting typically incorporates occupancy assumptions and vacancy adjustments designed to reflect year-round performance rather than peak-season results.

This is one reason many short-term rental DSCR programs target minimum DSCR ratios in the 1.10 to 1.25 range, compared with programs that may allow lower thresholds for long-term rental properties. The additional cushion helps account for revenue fluctuations, seasonal demand changes, and unexpected occupancy declines.

A common approval issue occurs when investors build their projections around peak-season Airbnb data while the appraisal and underwriting process evaluate the property’s performance across an entire year. The stronger the year-round income profile, the easier it becomes for the property to meet DSCR requirements and support financing.

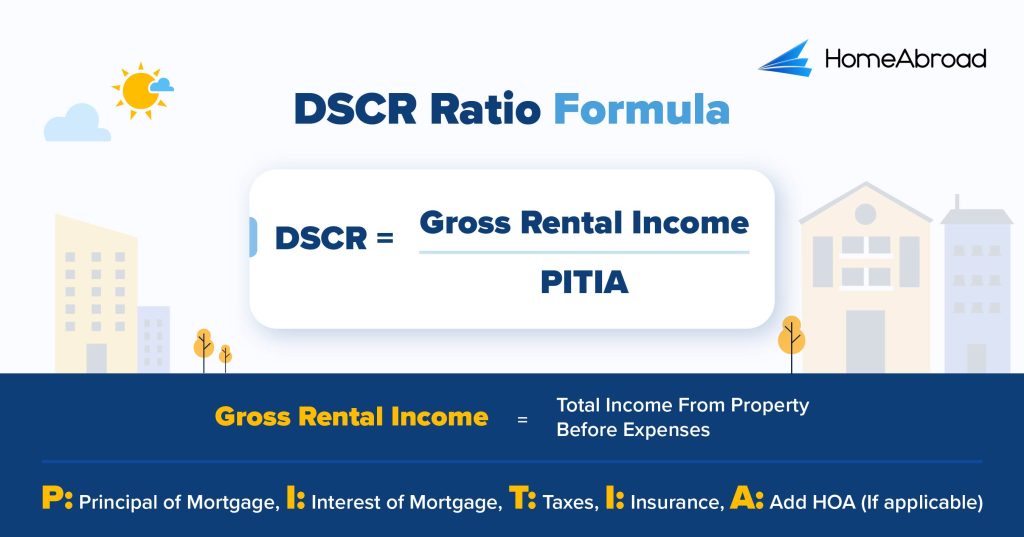

The STR DSCR Calculation: A Worked Example for a Foreign National Buyer

A DSCR loan evaluates whether a property’s rental income can support its housing expenses. The formula is straightforward:

PITIA stands for principal, interest, property taxes, insurance, and association dues.

For short-term rentals, the income figure typically comes from either the appraiser’s market-rent analysis or the property’s documented operating history, depending on the transaction type. The resulting ratio helps lenders determine whether the property generates enough income to support the proposed loan.

Consider a foreign national investor purchasing a vacation rental property in Florida.

Item | Monthly Amount |

|---|---|

Projected STR Income | $5,500 |

Principal & Interest | $2,700 |

Property Taxes | $500 |

Insurance |

|

HOA Dues | $250 |

Total PITIA | $3,800 |

DSCR = $5,500 ÷ $3,800 = 1.45

In this example, the property generates $1.45 of income for every $1.00 of housing expense, resulting in a DSCR of 1.45.

What makes short-term rental underwriting different is that several expenses can reduce the ratio more quickly than investors expect. HOA dues, for example, are included in PITIA and directly affect qualification. This is particularly important for condo investors because higher association fees can materially reduce DSCR even when rental income appears strong.

Insurance is another common factor. Short-term rental properties often carry higher insurance costs than traditional long-term rentals because of increased guest turnover and occupancy risk. In some markets, flood insurance may also be required, creating additional pressure on the ratio.

Property-management expenses deserve attention as well. While management fees are not typically part of PITIA, they still affect the property’s overall cash flow and should be considered when evaluating investment performance.

A pattern HomeAbroad sees frequently is foreign investors focusing primarily on projected Airbnb revenue while underestimating how taxes, insurance, HOA dues, and financing costs affect qualification. A property with strong nightly rates can still struggle to meet DSCR requirements if its expense structure is too heavy.

This is why successful foreign national investors evaluate both the income potential and the complete cost profile of a short-term rental before making an offer.

Property Eligibility: What Qualifies and What Gets Declined

Eligible Property Types and the Business-Purpose Rule

Most foreign national DSCR programs allow short-term rental financing on investment properties that are intended to generate rental income rather than serve as a primary residence.

Eligible property types commonly include:

- Single-family homes (SFRs)

- Townhomes

- Condominiums

- 2–4 unit residential properties

- Select small multifamily properties, depending on the loan program

The key requirement is that the property must be purchased and operated as an investment property. DSCR loans are designed for business-purpose lending, which means owner-occupied and primary-residence transactions generally do not qualify.

For foreign national investors, this distinction is important because a property that occasionally hosts family visits can still qualify as an investment property, but the primary purpose of ownership must remain rental income generation.

The HOA and Local-Ordinance Trap

One of the most common reasons a short-term rental deal falls apart has nothing to do with DSCR qualification.

Many investors identify a property with strong Airbnb revenue potential only to discover later that the homeowners association (HOA) prohibits short-term rentals altogether or imposes minimum lease requirements that make Airbnb and VRBO operations impossible.

Local regulations can create similar problems. Some cities require permits, registrations, occupancy taxes, inspection programs, or minimum-night stays before a property can legally operate as a short-term rental.

A property may appear to be an excellent STR investment based on location and projected income, but if HOA rules or local ordinances restrict short-term rentals, the income assumptions supporting the deal may no longer work.

This is especially important for condo investors, where association rules often change more frequently than investors expect.

Where STR Income Is Not Permitted

Not every DSCR loan program accepts short-term rental income. Some programs only allow traditional long-term rental income, while others restrict how STR income can be documented or require specific appraisal methods before the income can be used for qualification.

This means a property may function successfully as an Airbnb business but still fail to qualify under a particular lender’s DSCR guidelines.

A common misconception is that every lender automatically accepts AirDNA projections, Airbnb statements, or VRBO revenue reports. In reality, acceptable income sources vary by program.

If the investment strategy depends on short-term rental income, verify that the lender permits STR qualification before going under contract. Confirming this early can prevent costly appraisal expenses, underwriting delays, and failed transactions later in the process.

Foreign National Qualification Layer: What’s Different from a US Investor?

The DSCR calculation may be similar for all borrowers, but foreign national investors face several additional qualification requirements that most US-based investors never encounter.

One of the biggest advantages of foreign national DSCR loans is that US credit history is often not required. Instead of relying heavily on a US credit score or US employment income, we focus on the property’s cash flow, down payment strength, reserves, ownership structure, and overall risk profile.

Many foreign investors purchase short-term rentals through a US LLC, which can simplify property ownership and operations. Depending on the transaction structure, borrowers may also obtain an EIN for the LLC and, in some cases, an ITIN for tax reporting purposes. The exact requirements vary based on ownership structure, tax planning, and lender guidelines.

Source-of-funds verification is another area where foreign national files differ significantly from domestic transactions. Every dollar used for the down payment and closing costs must be documented and traceable. Underwriting and compliance teams review bank statements, transfer records, property-sale proceeds, business income documentation, gift funds, and other records to satisfy anti-money laundering (AML) requirements.

Foreign-currency reserves create an additional layer of complexity. At HomeAbroad, reserves may remain in foreign bank accounts provided the funds are verifiable, accessible, and properly documented. Currency fluctuations can also affect reserve calculations. A reserve account that comfortably meets requirements today may look different if exchange rates move significantly before closing.

Because of the additional documentation and cross-border risk profile, foreign national short-term rental borrowers often encounter larger down-payment and reserve requirements than domestic investors. The exact amount depends on the lender, property type, projected DSCR, and overall file strength.

Lucas Hernandez

Mortgage Loan Originator

HomeAbroad

NMLS #2171747One situation we see occasionally is a borrower with a strong Airbnb property and sufficient funds for closing, but the money has moved through multiple international accounts without a complete paper trail. The property qualifies, but the source-of-funds documentation becomes the issue that delays approval.

Foreign investors should also think about the exit strategy before purchasing the property. Tax considerations, ownership structure, and FIRPTA obligations can affect the eventual sale of a US investment property. While those topics are outside the scope of DSCR underwriting, they are important parts of the overall investment plan.

Appraisal Methodology for Short-Term Rental Properties

The appraisal process plays a much larger role in short-term rental financing than many foreign investors realize. Even if an Airbnb property has strong booking history, the we still relies on the appraisal to determine whether the projected income supports the loan.

For DSCR programs, the appraiser prepares a standard rental analysis using Form 1007 and may also complete a short-term rental market-rent addendum when the lender permits STR income qualification. The goal is to determine what a comparable short-term rental property could realistically generate in the local market.

To do this, the appraiser typically analyzes nearby Airbnb and VRBO properties with similar size, location, amenities, occupancy patterns, and nightly rates. Data providers such as AirDNA, Rabbu, and local market sources may also be used to support the analysis.

Here’s what actually happens during appraisal: the appraiser does not simply accept the revenue figure shown on an Airbnb listing or the investor’s spreadsheet. Instead, they build an independent market-supported income estimate based on comparable properties and underwriting guidelines.

One of the most common surprises for investors is discovering that an appraiser’s projected rental income can differ from what they saw on AirDNA or from what a seller claimed the property was earning. Underwriting always relies on the appraisal-supported figure.

This distinction becomes important when AirDNA projections and appraisal conclusions do not match. If AirDNA estimates $7,000 per month but the appraiser supports only $6,000 based on comparable properties, we generally underwrite the loan using the appraisal-supported income.

A common misconception is that the appraisal exists only to confirm property value. For short-term rental DSCR loans, the appraisal also serves as one of the primary tools used to validate projected income. In many cases, the appraiser’s conclusion becomes the number that ultimately determines whether the property qualifies for financing.

Common Approval Challenges: How Foreign National STR Deals Fall Apart

Most foreign national short-term rental transactions do not fail because the borrower is foreign. They fail because a detail that looked minor early in the process becomes a major underwriting issue later.

DSCR Falls Below the Minimum Requirement

One of the most common surprises occurs when the property’s projected income looks strong, but the expense structure is heavier than expected. Higher short-term rental insurance premiums, HOA dues, taxes, and financing costs all increase PITIA and reduce the DSCR ratio.

A property that appeared to qualify at 1.25 DSCR during initial analysis can fall below the lender’s minimum requirement once the appraisal, insurance quote, and final loan terms are completed.

HOA Restrictions Are Discovered Too Late

A property may have excellent Airbnb performance and a strong appraisal, but none of that matters if the HOA prohibits short-term rentals.

Many investors assume that existing Airbnb listings prove short-term rentals are allowed. In reality, association rules may have changed, enforcement may have increased, or previous owners may have operated outside the rules. Discovering a rental restriction after going under contract can derail the entire transaction.

The Lender Does Not Accept the Income Source

Not every lender evaluates short-term rental income the same way. Some programs accept AirDNA-supported projections. Others require specific appraisal methodologies, operating history, or documented platform income. Investors sometimes build their acquisition strategy around revenue estimates from a platform that the lender ultimately does not use for qualification.

When that happens, the property’s expected DSCR may look very different during underwriting.

Source of Funds Documentation Is Incomplete

Foreign national borrowers must document the source of funds. The challenge is not usually the amount of money. The challenge is proving where it came from. Funds that move through multiple international accounts, undocumented transfers, missing statements, or unexplained deposits often trigger additional underwriting conditions and can delay approval even when the property itself qualifies.

Peak-Season Revenue Creates Unrealistic Expectations

Another common issue is relying too heavily on peak-season Airbnb performance. A vacation property may generate exceptional revenue during holiday periods or high-tourism months, but underwriting evaluates the property’s ability to perform throughout the year. Appraisers and lenders typically apply market-based occupancy assumptions rather than assuming peak-season performance will continue indefinitely.

Jason Saylor

Sr. Customer Loan Specialist, HomeAbroad

The strongest STR files are usually the ones built around realistic year-round performance. The deals that struggle most often are the ones where projected income, HOA rules, or source-of-funds documentation were never fully vetted before the offer was submitted.

Most of these challenges are preventable. Investors who verify short-term rental eligibility, confirm lender income requirements, and organize source-of-funds documentation before going under contract typically experience a much smoother approval process.

STR vs. Long-Term Rental DSCR for Foreign Nationals: Which Should You Choose?

Both short-term rental (STR) and long-term rental (LTR) properties can qualify for foreign national DSCR financing, but they serve different investment goals.

Short-term rentals typically offer higher income potential. In the right market, an Airbnb or VRBO property can generate significantly more revenue than a traditional long-term lease. That additional income can create stronger cash flow and potentially higher returns.

The tradeoff is that underwriting is usually more complex. Appraisers must support projected STR income, occupancy assumptions matter, local regulations can affect operations, and lenders may apply stricter DSCR requirements because revenue fluctuates throughout the year.

Long-term rentals generally offer a simpler qualification path. Income is more predictable, underwriting guidelines are often more straightforward, and investors face fewer operational variables after closing. For many first-time foreign investors, long-term rentals provide a cleaner entry point into the US real estate market.

A pattern we often see is experienced operators gravitating toward short-term rentals because they understand occupancy management, pricing strategy, and guest operations. Investors seeking stability, simpler underwriting, and more predictable cash flow frequently prefer long-term rentals.

The decision usually comes down to your investment strategy. Choose a short-term rental if your priority is maximizing revenue potential and you’re comfortable managing a more operationally intensive asset. Choose a long-term rental if you value consistency, simpler qualification, and a more predictable income stream.

For a deeper look at how long-term rental DSCR loans work, including qualification requirements and property eligibility, see our guide on DSCR Loans for Long-Term Rentals.

How HomeAbroad Helps Foreign Nationals Finance Short-Term Rentals

Successfully financing a short-term rental involves much more than meeting a DSCR requirement. Income qualification, appraisal methodology, source-of-funds documentation, reserve verification, insurance requirements, ownership structure, and closing logistics all play a role in whether a transaction reaches the finish line.

At HomeAbroad, we’ve helped investors from more than 40 countries close over 500 DSCR loans for US investment properties. Our team guides foreign national investors through the entire process, from evaluating rental income and selecting the right loan program to preparing documentation, coordinating appraisals, and navigating underwriting requirements.

We also provide support beyond financing, including LLC formation assistance, US bank account setup guidance, insurance coordination, and remote-closing solutions for investors purchasing property from overseas.

Whether you’re evaluating your first Airbnb investment or expanding an existing portfolio, understanding how to qualify short-term rental income before making an offer can save significant time and frustration later.

Get pre-qualified with HomeAbroad to review your financing options, property eligibility, and investment goals before you go under contract.

Frequently Asked Questions About DSCR Loans for Short-Term Rentals

Can You Use a DSCR Loan for an Airbnb Property?

Yes. Many DSCR lenders allow Airbnb and VRBO properties, provided the property meets program guidelines and the rental income can be properly documented through an appraisal-supported projection or operating history.

What’s the Downside of a DSCR Loan for a Short-Term Rental?

The biggest challenge is income variability. Short-term rental revenue fluctuates based on occupancy, seasonality, local regulations, and market conditions. As a result, lenders may require higher DSCR ratios, larger down payments, or additional reserves compared to some long-term rental properties.

What Is the 75-55 Rule for Airbnb?

The 75-55 rule is an Airbnb hosting guideline, not a mortgage underwriting rule. It generally refers to occupancy and availability benchmarks used by some hosts to evaluate property performance. DSCR lenders do not qualify loans based on the 75-55 rule.

Do Foreign Nationals Need US Credit History for an STR DSCR Loan?

No. Most foreign national DSCR programs do not require US credit history. Instead, lenders focus on the property’s cash flow, down payment, reserves, source-of-funds documentation, and overall loan structure.

Can I Use AirDNA Projections to Qualify for a DSCR Loan?

Sometimes. Many lenders use AirDNA-supported data during the appraisal process, but qualification is typically based on the appraisal-supported income figure rather than a standalone AirDNA report provided by the borrower.

Is Short-Term Rental Income Allowed on Every DSCR Program?

No. Some DSCR programs specifically allow short-term rental income, while others only permit long-term rental income. Investors should confirm a lender’s STR guidelines before going under contract because qualification rules vary by program.