Editorial Integrity

Making informed real estate decisions starts with having the right knowledge. At HomeAbroad, we offer US mortgage products for foreign nationals & investors and have a network of 500+ expert HomeAbroad real estate agents to provide the expertise you need. Our content is written by licensed mortgage experts and seasoned real estate agents who share insights from their experience, helping thousands like you. Our strict editorial process ensures you receive reliable and accurate information.

Key Takeaways:

1. Interest-Only DSCR Loans lower monthly payments during the first 5 or 10 years, helping investors preserve cash flow for reserves, renovations, or future property purchases.

2. HomeAbroad qualifies Interest-Only DSCR Loans using the fully amortizing payment, ensuring borrowers benefit from improved cash flow without relaxed underwriting standards.

3. Eligible foreign national investors can access Interest-Only DSCR financing without US employment income or a US credit history, with qualification focused on the property's rental income.

4. The lower payment during the IO (Interest-Only) period comes with a future payment increase, so investors should understand how the property will support the higher payment once principal repayment begins.

Table of Contents

For many foreign national investors, the challenge isn’t finding a profitable US rental property. It’s balancing cash flow, reserves, and future investment opportunities without tying up too much capital in a single asset.

A pattern we’ve noticed among foreign national investors is that many are less concerned about paying down principal immediately and more focused on preserving flexibility during the early years of ownership.

That’s where an interest-only structure can make the numbers work more comfortably. By deferring principal payments for a defined period, investors reduce their monthly payment obligation during the early years of ownership.

Here’s what actually happens when you add an IO (Interest-Only) feature to a DSCR loan: during the interest-only period, typically 5 or 10 years, the monthly payment is lower because principal payments are deferred. The lower payment improves cash flow and reduces monthly carrying costs, giving investors more flexibility during the early years of ownership.

HomeAbroad offers Interest-Only DSCR Loans for foreign national investors purchasing US rental properties. Qualification focuses on the property’s rental income, eliminating the need for US employment verification and a US credit history. Interest-only pricing typically carries a rate premium of approximately 0.2% to 0.5% above standard DSCR loan pricing, depending on the property’s DSCR, loan-to-value ratio, reserve strength, and overall file profile.

How an Interest-Only DSCR Loan Works

The IO Period Explained

An IO (Interest-Only) DSCR Loan allows borrowers to make interest-only payments for a defined period before principal repayment begins. At HomeAbroad, eligible foreign national investors can typically choose an interest-only period of 5 or 10 years, depending on the loan program and property profile.

During the IO period, the monthly payment covers only the interest charged on the outstanding loan balance. Because no principal is paid down during this phase, the monthly payment is lower than it would be on a fully amortizing loan.

The basic interest-only payment calculation is:

Monthly Payment = Loan Balance × Annual Interest Rate ÷ 12

For example, a $400,000 loan at a 7.5% interest rate would generate an interest-only payment of approximately $2,500 per month.

One of the most common questions investors ask is whether a 40-year interest-only DSCR loan exists. The answer is yes. A typical 40-year structure combines a 10-year interest-only period followed by 30 years of amortizing payments. Some programs may also offer a 30-year term with a 5-year interest-only period followed by 25 years of amortization.

Scenario | Monthly Payment |

|---|---|

$400,000 Loan at 7.5% (Interest-Only) | ~$2,500 |

$400,000 Loan at 7.5% (Fully Amortizing) | ~$2,797 |

Monthly Cash Flow Difference | ~$297 |

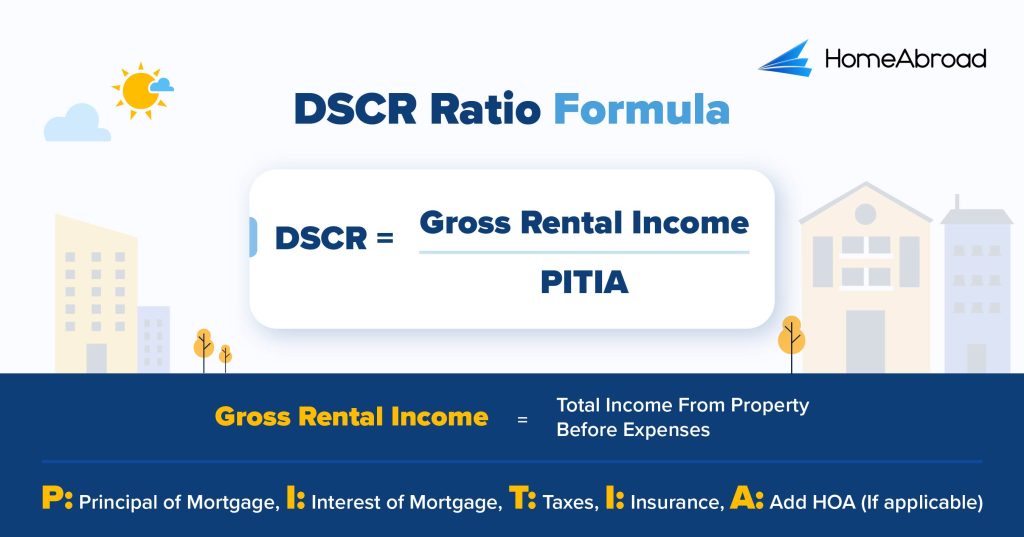

How IO Changes Your DSCR Calculation

DSCR measures whether a property’s rental income can support its housing expenses.

Because principal payments are not required during the interest-only period, the monthly payment obligation is lower. The reduced payment improves cash flow and increases the property’s operating cushion after closing.

Consider a property generating $3,200 per month in rental income with a $400,000 loan at 7.5%.

Scenario | Monthly Rent | Monthly Payment | DSCR |

|---|---|---|---|

Fully Amortizing | $3,200 | ~$2,797 | 1.14 |

Interest-Only | $3,200 | ~$2,500 | 1.28 |

The property’s rental income remains unchanged in both scenarios. The difference comes from the lower payment during the interest-only period, which improves cash flow and gives investors greater operating flexibility during the early years of ownership.

HomeAbroad qualifies Interest-Only DSCR Loans using the fully amortizing payment rather than the interest-only payment. The interest-only structure improves cash flow after closing, but qualification is still based on the property’s ability to support the fully amortizing payment.

IO Period Options: 30-Year and 40-Year Structures

Not all interest-only DSCR loans are structured the same way. The length of the interest-only period and the remaining amortization schedule directly affect monthly payments, future cash flow, and how sharply payments increase once principal repayment begins.

The 40-year structure is often the most misunderstood option. The interest-only period itself is typically the same as a comparable 30-year structure, usually 10 years. The difference is what happens afterward.

With a 30-year loan and a 10-year IO period, the remaining principal must be repaid over the final 20 years. With a 40-year structure, the same balance is repaid over 30 years instead. Spreading repayment across a longer period generally results in a smaller payment increase when the interest-only phase ends.

The choice between a 30-year and 40-year structure usually comes down to what happens after the interest-only period ends. Investors who expect to refinance, sell, or reposition the property within the next several years often prioritize the lower cost of a 30-year structure.

Investors planning a longer hold period may prefer a 40-year structure because the remaining balance is repaid over 30 years instead of 20, reducing the payment increase when the interest-only period expires.

When evaluating interest-only options, we look at the property’s cash-flow profile, the investor’s anticipated hold period, and whether a refinance or sale is part of the long-term strategy. For example, an investor planning to refinance within five to seven years may not benefit from extending amortization beyond that horizon, while an investor targeting a long-term hold may place greater value on reducing future payment shock through a 40-year structure.

When an Interest-Only DSCR Loan Makes Sense for Foreign Nationals

The pattern we see most often falls into three categories: investors expanding a portfolio, investors purchasing a property with a tight DSCR, and investors managing the seasonality of a short-term rental.

Scenario 1: The Scaling Investor

A foreign national investor with multiple US rental properties may prioritize preserving cash flow across the portfolio rather than accelerating principal reduction on a single asset.

For example, an investor planning to acquire a third or fourth property may use an interest-only structure to keep monthly obligations lower across existing rentals. For investors actively expanding a portfolio, preserving cash flow on existing properties can make the next acquisition easier to execute without increasing capital contributions.

Scenario 2: The Borderline DSCR Deal

Some properties generate strong rental income but fall just short of preferred DSCR thresholds when evaluated using a fully amortizing payment.

Consider a property producing $2,800 per month in rent. With a fully amortizing payment of $2,600, the property’s DSCR is approximately 1.08, creating a tighter qualification profile. An interest-only payment of $2,200 increases the property’s cash-flow cushion and operational flexibility after closing.

While HomeAbroad continues to underwrite using the fully amortizing payment, the lower interest-only payment can have a meaningful impact on day-to-day operations. In this example, the investor retains approximately $400 more per month during the interest-only period, improving the property’s operating cushion during the early years of ownership.

Scenario 3: The Short-Term Rental Investor

Short-term rental properties often experience seasonal fluctuations in occupancy and revenue. A property may perform exceptionally well during peak travel periods and then generate lower income during slower months.

An interest-only structure reduces the property’s fixed monthly payment obligation, creating additional breathing room during off-season periods without requiring changes to the investor’s long-term hold strategy.

The strongest interest-only transactions are usually the ones where the investor already knows what they want the property to look like five or ten years from now. By the time we discuss an IO structure, they’re often comparing today’s payment against a future refinance, rent-growth assumptions, or a planned portfolio expansion rather than looking only at the first year’s cash flow.

IO Makes Sense When…

- The property’s DSCR is tight on a fully amortizing payment

- The portfolio is in an active growth or acquisition phase

- The investor has a defined refinance, sale, or long-term hold strategy

- A short-term rental property experiences seasonal income fluctuations

IO May Not Make Sense When…

- Building equity as quickly as possible is the primary objective

- There is no plan for the payment increase after the IO period ends

- The anticipated hold period is shorter than the interest-only period itself

- The property’s cash flow remains weak even after the IO payment reduction

What an Interest-Only DSCR Loan Costs

The Rate Premium

Interest-only financing typically carries a rate premium compared to a standard DSCR loan because it creates additional risk for the lender. During the IO period, the loan balance does not decline through principal repayment, which means the investor builds equity more slowly and the lender’s collateral position improves at a slower pace.

The rate premium helps compensate for that additional risk while giving investors greater cash-flow flexibility during the early years of ownership.

The final rate depends on the complete loan structure. Your DSCR ratio, loan-to-value (LTV), reserve position, property type, and foreign national profile all influence pricing. For the most current baseline rates, investors should review HomeAbroad’s DSCR rates page or speak with a loan officer directly.

As an example, if a standard foreign national DSCR loan rate is at 7.00%, an interest-only structure may be priced between approximately 7.1% and 7.4%, depending on the specifics of the transaction.

On a $400,000 loan, a 0.3% rate premium may add roughly $100 per month in interest expense, while principal deferral can reduce the monthly payment by $300 to $600 per month.

At HomeAbroad, we price Interest-Only DSCR Loans based on the overall strength of the transaction rather than the IO feature alone. A stronger DSCR, lower LTV, and larger reserve position can all contribute to a more competitive pricing profile.

Payment Shock at IO End: Plan for It

The most important risk to understand is what happens when the interest-only period ends.

During the IO period, a $400,000 loan at 7.5% produces a monthly payment of approximately $2,500. Once the interest-only phase expires, the loan begins amortizing and the payment is recalculated over the remaining term. On a 30-year loan with a 10-year IO period, the remaining balance must be repaid over the final 20 years, increasing the monthly payment to approximately $3,200 or more.

Warning: A payment increase of $700 or more per month is not unusual when a 10-year interest-only period ends. Investors should model the post-IO payment before closing, not when the adjustment arrives years later.

The most common ways investors prepare for this transition include:

- Refinancing before the interest-only period expires.

- Allowing rent growth over time to absorb some or all of the payment increase.

- Selling the property as part of a planned exit strategy.

Steven Glick

Director of Mortgage Sales

HomeAbroad

NMLS #1231769One mistake we occasionally see is investors underwriting the deal using only the interest-only payment. Before selecting an IO structure, we encourage borrowers to stress-test the property using the future amortizing payment as well. If the numbers only work during the IO period, the investor should understand that before closing, not when the payment changes years later.

How to Get an Interest-Only DSCR Loan Through HomeAbroad

One of the first things we do when discussing an Interest-Only DSCR Loan is model both payment structures side by side. This allows investors to compare the fully amortizing payment against the interest-only payment before deciding which structure best supports the property’s cash flow and long-term investment plan.

When you speak with a HomeAbroad loan specialist, we’ll typically review the property’s expected rental income, purchase price, down payment, reserve position, and long-term investment strategy. From there, we can model both fully amortizing and interest-only scenarios so you can compare monthly cash flow, total financing costs, and the future payment after the IO period ends.

The documentation requirements remain the same as a standard DSCR loan. Source-of-funds documentation is often the most important part of the file because funds moving across multiple accounts, currencies, or countries may require additional verification before closing.

The overall timeline is also similar to a traditional DSCR transaction, with most loans closing within approximately 30 to 45 days, depending on the property, appraisal, and documentation readiness.

HomeAbroad has helped foreign national investors from more than 40 countries finance US investment properties through DSCR programs. If you’re considering an Interest-Only DSCR Loan, bring us the property’s estimated rent, purchase price, and expected down payment. We can model the monthly payment under standard, interest-only, and 40-year structures so you can see the cash-flow differences before submitting an application.

Frequently Asked Questions

Can Foreign Nationals Get an Interest-Only DSCR Loan?

Yes. HomeAbroad offers Interest-Only DSCR Loans specifically for foreign national investors purchasing US rental properties. Eligible borrowers can access interest-only options without US employment income or a US credit history, subject to standard DSCR qualification requirements.

How Is DSCR Calculated on an Interest-Only Loan?

HomeAbroad qualifies Interest-Only DSCR Loans using the fully amortizing payment rather than the interest-only payment. The interest-only period improves monthly cash flow after closing, but it does not reduce underwriting standards or change the qualification threshold.

What Is a 40-Year Interest-Only DSCR Loan?

A 40-year Interest-Only DSCR Loan typically combines a 10-year interest-only period with 30 years of amortizing payments. The longer repayment period helps reduce payment shock when the interest-only phase ends, making it a popular option for long-term rental investors.

What Is the Rate Premium for an Interest-Only DSCR Loan?

Interest-Only DSCR Loans generally carry a rate premium of approximately 0.2% to 0.5% above standard DSCR pricing. The exact premium depends on factors such as the property’s DSCR, loan-to-value ratio, reserve strength, and overall file profile.

Does an Interest-Only DSCR Loan Require a Higher DSCR?

No. HomeAbroad underwrites interest-only loans using the same qualifying standards applied to fully amortizing DSCR loans. The interest-only election is designed to improve cash flow and liquidity, not to lower qualification requirements.