Editorial Integrity

Making informed real estate decisions starts with having the right knowledge. At HomeAbroad, we offer US mortgage products for foreign nationals & investors and have a network of 500+ expert HomeAbroad real estate agents to provide the expertise you need. Our content is written by licensed mortgage experts and seasoned real estate agents who share insights from their experience, helping thousands like you. Our strict editorial process ensures you receive reliable and accurate information.

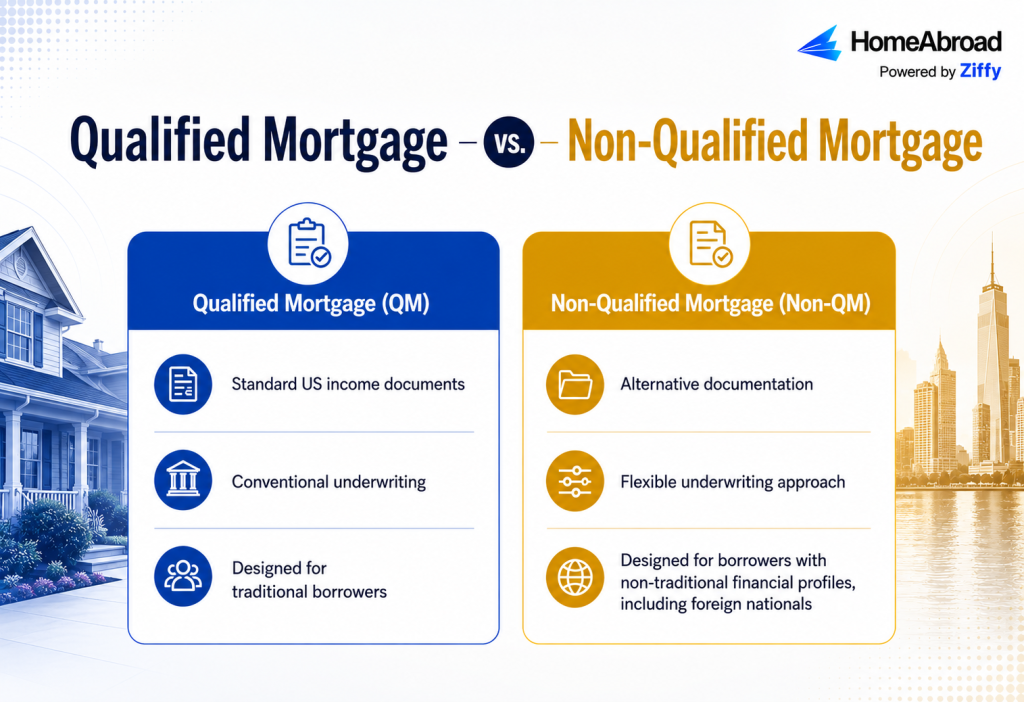

A Non-QM loan follows federal lending rules but uses alternative underwriting methods instead of conventional mortgage guidelines.

For many foreign national investors, Non-QM financing is the most practical path to buying US investment property.

At HomeAbroad, we offer four Non-QM loan programs: DSCR, Full Documentation, Fix and Flip, and Bridge Loans.

The right loan depends on your investment strategy, qualification method, and financing timeline.

Table of Contents

What “Non-QM” Actually Means

A Non-QM loan, short for Non-Qualified Mortgage, is a home loan that follows the federal Ability-to-Repay (ATR) rule but doesn’t meet every requirement to be classified as a Qualified Mortgage (QM) under the Consumer Financial Protection Bureau framework. For foreign national borrowers, Non-QM loans provide a practical financing path when traditional US income documents, credit history, or residency requirements don’t fit their financial profile.

Non-QM loans are underwritten differently from Qualified Mortgages, but they remain subject to federal Ability-to-Repay requirements. Their distinguishing feature is the use of alternative qualification methods that better accommodate borrowers with non-traditional financial profiles.

For international investors, that flexibility makes it possible to qualify using documentation that better reflects their financial situation. This interpretation is based on the CFPB’s Ability-to-Repay/Qualified Mortgage Rule.

For many foreign nationals, conventional mortgage guidelines create obstacles because they are designed around US-based employment, credit histories, and tax documentation. At HomeAbroad, we address this by offering financing solutions that evaluate factors such as rental income, foreign-earned income, assets, or other qualifying financial documentation, depending on the loan program.

That is why many foreign national borrowers seek Non-QM financing long before they explore conventional mortgage options. If you’re new to financing US real estate, it’s also helpful to understand how Non-QM fits into the broader foreign national mortgage landscape before comparing individual loan programs.

Qualified Mortgage vs. Non-Qualified Mortgage

Feature | Qualified Mortgage (QM) | Non-Qualified Mortgage (Non-QM) |

|---|---|---|

Underwriting framework | Must satisfy Qualified Mortgage requirements established under the ATR rule | Must comply with the ATR rule but uses underwriting outside the QM framework |

Income verification | Primarily traditional US income documentation | May use alternative documentation appropriate for the borrower’s financial profile |

Typical borrower | US wage earners with conventional documentation | Self-employed borrowers, foreign nationals, real estate investors, and other borrowers with non-traditional financial profiles |

Flexibility | Limited by QM requirements | Greater flexibility while remaining subject to responsible underwriting |

Risk level | Not inherently safer | Not inherently riskier; loan quality depends on the borrower, property, and underwriting |

Why Non-QM Is the Standard Path for Foreign National Borrowers

Many foreign national investors are financially well qualified but don’t fit the documentation standards used in conventional US mortgage underwriting. They may earn income overseas, hold substantial assets, or have years of real estate investing experience, yet lack the US financial history that conventional mortgage programs typically rely on.

Traditional mortgage underwriting relies heavily on standardized US documentation. A foreign national, however, may earn income overseas, maintain assets in multiple countries, or have an established credit history outside the United States. These differences don’t necessarily reflect a borrower’s financial strength, but they do require a different underwriting approach.

That’s where Non-QM loans fill the gap. They allow lenders to evaluate a borrower’s ability to repay using documentation that better reflects an international financial profile while still following federal Ability-to-Repay requirements. Depending on the loan program, underwriting may focus on the property’s rental income, foreign-earned income, available assets, or other qualifying financial documentation.

We recently worked with a foreign national investor purchasing a rental property in Florida who had years of real estate investing experience overseas but no established US credit history. Instead of focusing solely on traditional US mortgage documentation, we evaluated the borrower’s financial profile using the qualification method required for the selected Non-QM program.

This is also why foreign national borrowers often see different Non-QM loan options depending on their investment strategy. An investor purchasing a cash-flowing rental property may qualify through a DSCR Loan, while another buyer with verifiable foreign income may find a Full Documentation Loan to be a better fit. The loan program changes, but the underlying Non-QM framework remains the same.

Our Non-QM loan programs provide a flexible financing framework for foreign national investors whose financial profiles don’t fit conventional mortgage guidelines.

Steven Glick

Director of Mortgage Sales · HomeAbroad

Many of our clients have substantial assets and years of investment experience overseas, even without a US credit history. Our role is to evaluate that financial strength using documentation that accurately reflects their profile.

The Non-QM Family: What Falls Under This Umbrella

Non-QM refers to a family of mortgage programs rather than a single loan type. Within that category, each program serves a different financing purpose and evaluates borrowers differently.

For foreign national investors, the right option depends on how you qualify, not simply on the type of property you’re buying.

DSCR Loans

A DSCR Loan qualifies borrowers primarily based on a property’s expected rental income rather than personal income. It’s designed for investors building or expanding a portfolio of income-producing properties and is often the preferred option for long-term buy-and-hold strategies.

A good fit if you:

- Own or are buying an income-producing rental property

- Prefer to qualify using property cash flow

- Plan to build a long-term rental portfolio

Full Documentation Loans

A Full Documentation Loan allows eligible foreign national borrowers to qualify using income and assets from their home country. This program is well suited for borrowers who want their personal financial strength considered, even if they don’t have an established US credit history.

Commonly chosen by borrowers who:

- Earn income outside the United States

- Can document foreign income and assets

- Want personal financial strength considered during underwriting

Fix and Flip Loans

A Fix and Flip Loan provides short-term financing for investors purchasing properties to renovate and resell. The focus is on funding the acquisition and renovation so investors can execute their exit strategy efficiently before transitioning to their next project.

Ideal for investors who:

- Purchase properties that need renovation

- Plan to renovate before selling

- Need short-term project financing

Bridge Loans

A Bridge Loan provides temporary financing when the timing between transactions doesn’t align. Investors commonly use bridge financing to purchase a new property before another asset is sold or refinanced, helping them move quickly when opportunities arise.

Often used when you need to:

- Purchase before another property is sold

- Bridge a financing gap

- Move quickly on an investment opportunity

The first question we ask isn’t which loan a borrower wants. It’s how they plan to use the property. Someone buying a long-term rental has very different financing needs than an investor renovating a property for resale, and that usually points us toward the right program.

From Short-Term to Long-Term: How Our Loan Programs Can Work Together

The financing that works at one stage of an investment property may not be the best fit at the next. As the property and your investment strategy evolve, your financing needs may change as well.

At HomeAbroad, our loan programs are designed to support different stages of an investment strategy. Depending on your investment goals and qualification, you may be able to transition from one loan program to another as your property and financing needs evolve. Final approval for any new loan is always subject to underwriting and current program requirements.

Here’s a common example of how that journey may look:

Property Stage | Financing Solution | Purpose |

|---|---|---|

Property needs renovation | Fix and Flip Loan | Supports acquisition and renovation financing. |

Property is renovated and generating rental income | DSCR Loan | May provide long-term financing based on the property’s rental income, subject to underwriting. |

Another scenario may involve a Bridge Loan, which can help an investor purchase a property before another asset is sold or refinanced. Once that transaction is complete, the borrower may refinance into a longer-term financing solution that aligns with their investment strategy and qualification.

The right path depends on your property, timeline, and financial profile. Some investors use a single loan from purchase through ownership, while others benefit from different financing solutions as their investment objectives change.

We don’t start by recommending a loan product. We start by understanding where the property is today and where the investor wants it to be six or twelve months from now. That often determines which financing strategy makes the most sense.

What “Alternative Documentation” Actually Means for a Foreign National Borrower

Alternative documentation allows us to evaluate borrowers using financial records that reflect their qualification method, whether that’s property income, foreign income, or eligible assets.

For many foreign national investors, traditional US mortgage requirements, such as W-2s, US tax returns, or an established US credit history, don’t reflect how they earn income or manage their finances. At HomeAbroad, our loan programs are designed to evaluate borrowers using documentation that aligns with their qualification method.

DSCR Loans: Property Income Takes the Lead

Our DSCR Loan qualifies borrowers primarily based on a property’s rental income to support its mortgage payments. That means borrowers don’t need to qualify using their personal employment income.

This approach is especially helpful for foreign national investors purchasing income-producing properties, as it shifts the focus from personal income documentation to the property’s cash flow.

Full Documentation Loans: Foreign Income and Assets Matter

Some borrowers prefer to qualify using their personal financial strength. Our Full Documentation Loan allows eligible borrowers to verify income and assets earned outside the United States using acceptable financial documentation from their home country.

Depending on the borrower’s circumstances and program requirements, identification may be established using an eligible government-issued passport or an Individual Taxpayer Identification Number (ITIN) where applicable, rather than relying solely on a Social Security Number.

The documentation required varies by loan program and individual circumstances, and all information is reviewed as part of our underwriting process.

Good to Know

Alternative documentation doesn't eliminate the underwriting process. Every loan application is evaluated to verify a borrower's ability to repay using the documentation appropriate for the selected loan program. Program requirements and acceptable documentation may vary based on the transaction and current underwriting guidelines.

Which Non-QM Program Fits Your Investment Strategy?

Not all Non-QM loans are structured the same. The financing needed to purchase and hold a rental property is very different from the financing needed to renovate a property or bridge the gap between two transactions.

At HomeAbroad, each loan program is designed with a specific investment strategy in mind. As a result, down payment expectations, reserve requirements, loan terms, and repayment timelines vary by program.

Loan Program | Typical Financing Purpose | What to Expect |

|---|---|---|

DSCR Loan | Long-term investment financing | Generally structured with longer loan terms and reserve requirements designed for rental property ownership. |

Full Documentation Loan | Long-term financing using foreign income and assets | Similar long-term financing structure, with qualification based on documented personal finances. |

Fix and Flip Loan | Purchase and renovate a property for resale | Short-term financing focused on acquisition, renovation costs, and the planned exit strategy. |

Bridge Loan | Bridge the gap between two transactions | Short-term financing intended to provide liquidity until another property is sold or refinanced. |

Rather than comparing programs by interest rate alone, it’s more useful to consider how long you’ll need the financing and what you’re trying to accomplish. An investor purchasing a rental property to generate long-term cash flow has different financing needs than someone renovating a property for resale or purchasing a new investment before another transaction closes.

Choosing a loan that aligns with your investment timeline can make the financing process more efficient and help ensure the loan supports your overall strategy instead of working against it.

Steven Glick

Director of Mortgage Sales · HomeAbroad

Many borrowers begin by asking about rates or down payments. My first question is how they plan to use the property, because that usually narrows the right financing option much faster than comparing loan features.

Choosing the Right Non-QM Program: A Simple Decision Framework

The best Non-QM loan depends on how you plan to use the property and how you want to qualify. Use the questions below to identify which HomeAbroad financing solution may be the best fit for your investment strategy.

If this sounds like you… | Consider… |

|---|---|

I’m buying a rental property and want to qualify based on the property’s rental income, not my personal income. | DSCR Loan |

I have foreign income and assets that I’d like to use for qualification instead of relying solely on rental income. | Full Documentation Loan |

I’m buying a property to renovate and resell within a short timeframe. | Fix and Flip Loan |

I need short-term financing to bridge the gap between buying one property and selling or refinancing another. | Bridge Loan |

While these scenarios provide a helpful starting point, the right loan ultimately depends on your financial profile, investment objectives, and property details. During the financing process, we’ll review your goals and recommend the program that best aligns with your investment strategy.

Next Steps

The right financing solution depends on your investment goals, qualification method, and timeline. If you’re ready to explore your options, we’ll help you compare our loan programs and identify the one that best fits your investment strategy.

At HomeAbroad, we help foreign national investors compare loan options based on how they plan to use the property, how they want to qualify, and their long-term investment strategy. Whether you’re purchasing your first US rental property, renovating a home for resale, or expanding an existing portfolio, we’ll help you identify the financing solution that fits your needs.

If you’re ready to move forward, you can:

- Speak with our mortgage specialist to discuss your investment goals and qualification options.

- Start your mortgage pre-approval to understand which financing solutions you may qualify for.

Every investment strategy is different, and so is every financing solution. Our team will help you evaluate your options and guide you through the next steps based on your specific transaction and financial profile.

Ready to Finance Your US Investment Property? Start your pre-approval with HomeAbroad to find the financing solution that aligns with your investment strategy.

Frequently Asked Questions

Can I get a Non-QM loan without a US credit history?

Yes. HomeAbroad’s Non-QM loan programs are designed for borrowers who don’t have an established US credit history. Depending on the program, we may evaluate alternative documentation, international financial information, or the property’s rental income as part of the underwriting process.

Can foreign nationals buy investment property in the US with a Non-QM loan?

Yes. Foreign nationals can finance eligible US investment properties with a Non-QM loan if they meet the program’s underwriting requirements. The available loan options depend on factors such as the property type, qualification method, and investment strategy.

Is a DSCR Loan considered a Non-QM loan?

Yes. A DSCR Loan is a type of Non-QM loan that qualifies borrowers primarily based on a property’s rental income rather than personal income.

Can I refinance into a different Non-QM loan later?

Yes. As your investment strategy or property changes, refinancing into another loan program may be an option if you meet the applicable underwriting and program requirements at that time.

Are Non-QM loans only for investment properties?

No. While many Non-QM loans are used to finance investment properties, some programs can also support other property types, depending on the loan product and current underwriting guidelines.