Editorial Integrity

Making informed real estate decisions starts with having the right knowledge. At HomeAbroad, we offer US mortgage products for foreign nationals & investors and have a network of 500+ expert HomeAbroad real estate agents to provide the expertise you need. Our content is written by licensed mortgage experts and seasoned real estate agents who share insights from their experience, helping thousands like you. Our strict editorial process ensures you receive reliable and accurate information.

Key Takeaways:

1. Foreign nationals, including US newcomers and investors, can get loans in the US without a US credit history.

2. Expats don’t need a green card, and investors don’t need a visa to qualify for a foreign national mortgage.

3. Foreign nationals can buy primary residences, second homes, vacation houses, or investment properties with foreign national mortgages.

4. HomeAbroad simplifies the US real estate process for international investors, from finding the right investment property through our AI-driven investment property search to tailored mortgage options that allow foreign nationals to qualify without a US credit history.

We’ve helped foreign nationals from 40+ countries buy property in the US without a US credit history. Most start with the same questions: Is it even possible? What documentation is required? Which loan programs actually work for international buyers?

According to the National Association of Realtors (NAR), international buyers purchased 78,100 US homes between April 2024 and March 2025, a 44% increase from the previous year. That growth reflects a clear shift. Foreign nationals aren’t sitting on the sidelines. They’re actively investing in US real estate using mortgage programs designed for global buyers.

What we see most often is that international buyers assume a US credit score is mandatory to qualify for a mortgage. It isn’t. At HomeAbroad, we structure foreign national mortgage programs specifically for buyers who don’t fit conventional lending models. Instead of relying on US credit history, underwriting focuses on verified assets, global documentation, and the fundamentals of the deal.

This guide explores our unique mortgage programs, how they work without a US credit history, and the steps to qualify.

Table of Contents

Can Foreign Nationals Get a Mortgage in the US?

Yes, foreign nationals can obtain a mortgage and purchase a house in the US with little to no credit history. Your citizenship, immigration, or residency status does not affect mortgage qualification.

As someone who has worked with international real estate investors, I’ve seen firsthand how a lack of US credit history creates a barrier for first-time homebuyers in the US, even if they have sufficient financial independence to secure a mortgage.

That’s where foreign national mortgages come in. HomeAbroad offers tailored global investor mortgage programs, which enable newcomers on H-1B, L-1, or other visas, as well as foreign investors, to qualify for a mortgage without an established US credit history, opening the door to new financing opportunities.

What is a Foreign National Mortgage?

A foreign national mortgage is a US mortgage program designed for US newcomers and foreign investors who want to secure a loan with no US income or credit history. These tailored mortgage programs don’t evaluate you based on your green card, visa requirements, or other traditional roadblocks.

When we work with clients who have international income or assets, the underwriting approach is different. Qualification focuses on the property’s rental income, how financial strength is documented, and how the deal is structured rather than where the income originates.

At HomeAbroad, we offer foreign national mortgage programs specifically for buyers without a US credit history. Our mortgage officers assess each application holistically, taking into account immigration status, credit situation, and the overall risk profile of the deal.

To be clear, foreign national mortgages aren’t shortcuts. They’re purpose-built solutions tailored for international buyers. When structured correctly, they provide a clear and reliable path to financing US real estate.

Now, let’s explore the different types of foreign national mortgages we offer and help you find the one that’s right for you.

Types of Foreign National Mortgage Loans

We offer four types of mortgages for foreign nationals to meet the diverse home-buying and investment needs of international real estate buyers in the US: Full Documentation Loans, DSCR (Debt Service Coverage Ratio) Loans, Fix-and-Flip Loans, and Bridge Loans.

Now, let’s examine these loan programs in detail.

1. Full documentation loan

A Full Documentation Loan is a loan option for US newcomers and foreign investors with no US credit history. It requires extensive documentation to verify income, assets, employment status, and debts.

As US credit history is not available, we will require an International Credit Report (ICR) from your country of origin to assess your creditworthiness and financial history.

We also accept a bank reference letter or a history of payment on two tradelines, such as a credit card or mortgage, in the applicant’s home country, as an alternative to a credit report from that country.

To be clear, this loan works best for buyers with stable, well-documented income and clean financial records, even if everything sits outside the US system.

Benefits:

- Qualification with no US credit history

- Foreign income and credit accepted

- Can qualify based on assets

- Get quick approval within 30 days

Full Documentation Loan Requirements:

- Debt-to-Income Ratio: Less than 43%

- Down Payment: 20%-25%

- Loan Term: Up to 30 Years

- Cash Reserves: 6 months

- Income Documents: Foreign income and asset documents. International Credit Report or alternative proof of creditworthiness from the home country

2. DSCR Loan

A Debt Service Coverage Ratio (DSCR) loan is a US mortgage program designed for international real estate investors who may not have a US credit history.

DSCR loans consider the income from the investment property, rather than the borrower’s personal income, making it easier for foreign investors with no financial footprint in the country to qualify. This means that no personal documentation, such as pay stubs, tax returns, or income verification, is required to qualify for these loans.

In our experience working with foreign investors, DSCR loans are often the most flexible option for buyers who want to scale portfolios or invest remotely. Because underwriting centers on the asset itself, investors can close from their home country and finance multiple properties at the same time.

Benefits:

- No US credit history needed

- Qualification based on the property’s income

- Multiple loans can be financed at the same time

- Can close from the home country.

- Fast approvals in less than 30 days

- Versatility in Property Use: Investment properties (residential and commercial)

DSCR Loan Requirements for Foreign Nationals:

- DSCR Ratio: >= 1 for best terms, <1 eligible with higher down payment. Properties with DSCR below 1.0 can still be eligible through our No-Ratio DSCR loan, which allows financing when rental income doesn’t fully cover the mortgage payment.

- Minimum down payment of 25%

- LTV Ratio: Purchase up to 75%, Rate/Term Refinance up to 75%, Cash-out Refinance up to 70%

- 6 Months of Cash Reserves

3. Fix and Flip Loan

Fix-and-Flip Loans are for global real estate investors with no US credit looking to purchase, renovate, and resell properties for profit.

These short-term loans finance property purchases and renovations, enabling investors to capitalize on rising property values.

Benefits:

- Quick approval and closing under 15 days

- Funds for purchase and renovation

- Flexible terms

- Potential for high returns on investment

Fix and Flip Loan Requirements for Foreign Investors:

- 6-24 months loan term

- Down Payment of 25% – 30%

- LTC (Loan-to-Cost) up to 85%

- Rehab Cost up to 100%

- ARV (After Repair Value) of up to 75%

- A detailed renovation plan, including cost estimates and proof of previous successful flip projects, may be required.

4. Bridge Loan

Bridge Loans are short-term financing solutions for international real estate investors needing immediate funds to bridge the gap between selling an existing property and purchasing a new one.

This won’t work if the repayment plan is unclear. Bridge loans require a realistic, time-bound exit.

They offer quick access to capital, even without a US credit history.

Benefits:

- Fast funding to secure a new property before selling the old one

- Flexible terms and repayment options

- Usable for various property types

- Get quick approvals within 15 days

Bridge Loan Requirements for Foreign Investors:

- 6-24 months loan term

- Down Payment of 30%

- Up to 70% LTV Ratio (Purchase)

- Up to 70% LTV Ratio (Rate term Refinance)

- Up to 65% LTV Ratio (Cash Out Refinance)

- Proof of existing property equity

- Exit strategy for loan repayment (e.g., sale of property)

- Property appraisal

HomeAbroad makes US real estate and mortgages easy and accessible for foreign nationals. We offer the best loan terms and experienced mortgage officers who specialize in working with foreign nationals, ensuring an effortless financing process.

Let’s see what our client, Sophie Tremblay (Canada), who successfully secured a foreign national mortgage with no US credit history, has to say:

HomeAbroad made the process of buying a vacation home in the US incredibly smooth. Their expertise in foreign national mortgages helped me secure a loan without the need for a US credit history. I couldn’t be happier with the outcome.

Sophie Tremblay – Snowbird – Purchased a Vacation home in Miami, FL

Did that motivate you to apply for a DSCR Loan? Let me show you how you can do it!

How to Apply for a Foreign National Loan

Applying for a foreign national loan can seem challenging, but with proper preparation and guidance from HomeAbroad, the process can be straightforward and efficient.

Here’s a step-by-step guide:

Step 1: Assess Your Financial Situation

Understand your financial health by creating a budget to determine your mortgage allocation.

Assess your income, expenses, and savings to get a clear picture of your financial standing. Use our foreign national loan calculator to estimate your potential loan amount and monthly payments.

This step ensures that you are financially prepared and sets realistic expectations for your home search.

Step 2 – Get Started with HomeAbroad

Finding trustworthy lenders who specialize in loans for foreign nationals is essential.

Consider HomeAbroad for competitive rates, flexible loan terms, and exceptional customer support.

We work with US newcomers and foreign investors to structure mortgage options that don’t rely on US credit history. The focus is on matching the right loan program to the property, the documentation available, and the buyer’s goals.

Our expert loan officers guide borrowers through each stage of the process, from initial eligibility review to underwriting and closing, so expectations stay clear throughout.

Get started today!

Step 3 – Connect with a HomeAbroad Loan Officer

After receiving your details, our loan officer will contact you to discuss your needs and answer any questions you may have.

Step 4 – Get Preapproval

Obtain a preapproval letter to indicate your borrowing capacity and serious intent to buy the property.

This letter strengthens your position with sellers, making your offers more competitive.

Our loan officer will request a few basic financial details for your specific foreign national mortgage program preapproval.

Step 5 – Gather Your Documents

Collect your documents for your specific loan program. Our mortgage officer will provide a detailed list of documents and guide you through the process for swift approval.

Step 6 – Make an Offer on Your Dream Home

Once you find the perfect home, make an offer. Partner with our Certified International Property Specialist (CIPS) agent, who has international expertise, to simplify the homebuying process.

They will also assist you in researching and preparing a competitive offer.

Our expertise in negotiating and understanding market trends can give you an edge in securing your desired property.

Get a HomeAbroad agent in your area today!

Find the best real estate agent with international expertise

Connect with a HomeAbroad real estate agent in your area.

Step 7 – Lock in Your Interest Rate

Interest rates can fluctuate, so it’s crucial to lock in your rate to secure favorable terms. Your mortgage officer will guide you through this process to get you the best possible rate available at that time.

This step protects you from potential rate increases before closing and provides financial stability.

Step 8 – Underwriting & Appraisal

After processing your loan application, we will send it to an underwriter for review. The underwriter will review your application to ensure you meet all loan requirements.

The underwriter will also order an appraisal to determine the property’s current market value. If the underwriter has any questions or needs additional information, they’ll reach out.

After complete analysis, the underwriter can approve, reject, or approve with conditions.

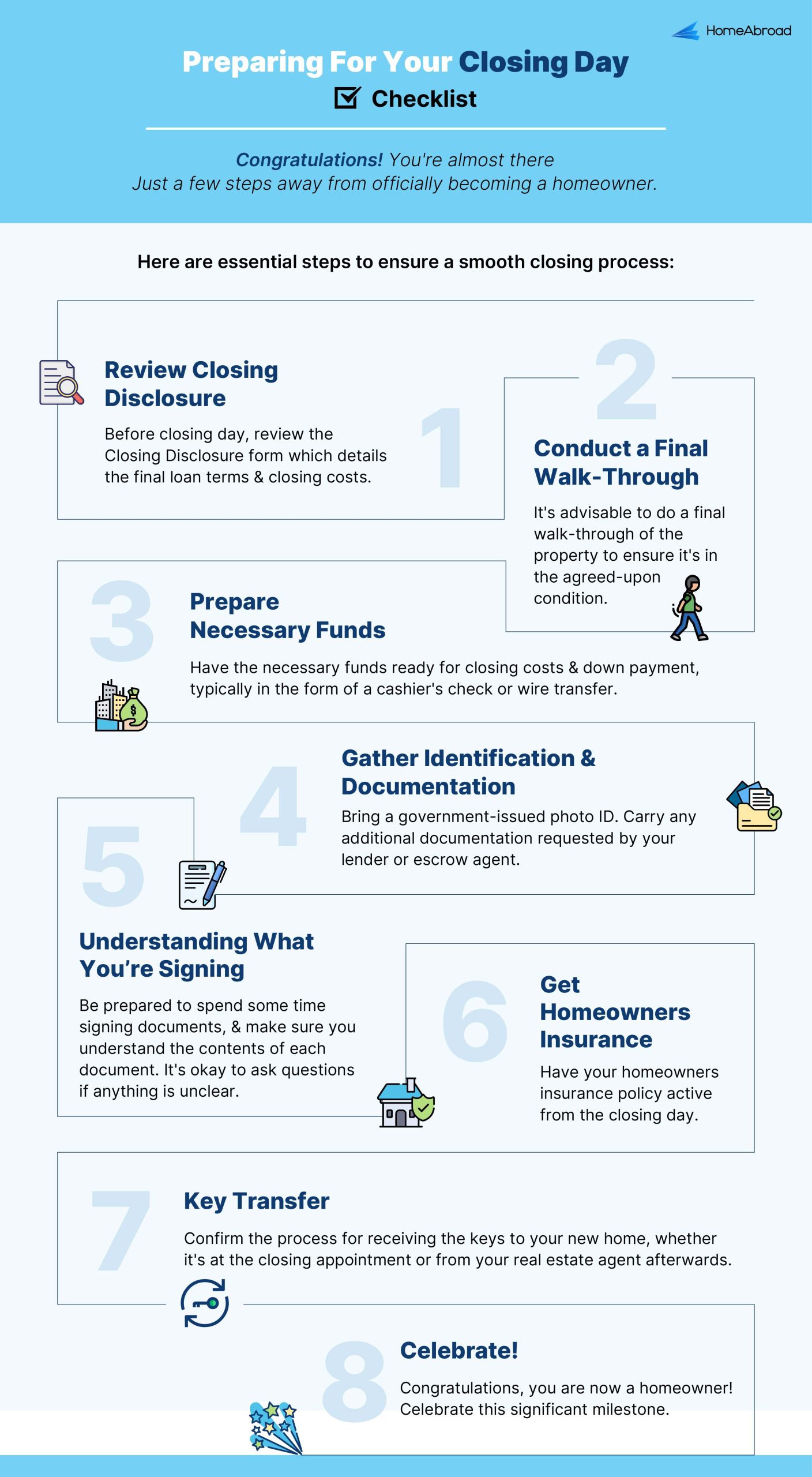

Step 9 – Closing

Once your loan has been approved and all the conditions have been met, including the completion of the title report and home inspection, you’ll attend a closing meeting.

At the closing, you’ll review and sign all the final paperwork, including the loan documents and any other closing documents.

You will also pay closing costs, which may include fees for title searches, appraisals, and other services.

Once everything is signed and you have paid the closing costs, you will receive the keys to your new home!

Here is a closing day checklist to be well-prepared for the big day.

Our foreign national mortgage officers at HomeAbroad specialize in working with international buyers and US newcomers. We understand the documentation gaps, cross-border considerations, and structural challenges that often come up when foreign nationals apply for US mortgages.

What we see most often is that clarity early in the process is what makes deals move smoothly. That’s why we use a streamlined, AI-enabled platform to pre-qualify borrowers based on verified assets, deal fundamentals, and property details, without requiring a US credit history.

We also support remote closings for foreign national investors. Buyers can complete the entire mortgage process from abroad while staying closely connected to the transaction, timelines, and required documentation.

The focus isn’t just approval. It’s a financing process that’s predictable, transparent, and aligned with how international buyers actually buy US real estate.

Congratulations! You Got a US Mortgage.

HomeAbroad plays a critical role in helping foreign investors and US newcomers secure mortgages even without a US credit history. We understand the complexities international buyers face, and our lending approach is built specifically to address those challenges rather than forcing borrowers into traditional credit frameworks that don’t apply to them.

We are a one-stop PropTech and FinTech platform dedicated to simplifying US real estate for international buyers and newcomers. We understand the unique challenges that global investors face, and that’s why we’ve built a platform that brings everything together in one place.

With tailored foreign national mortgages, an AI-driven investment property search platform, and a network of over 500 expert real estate agents, we make it easier to find the right property that fits your goals.

Beyond property search and financing, our concierge services guide you through every step from setting up an LLC and opening a US bank account to securing insurance and coordinating property management.

Our mission is straightforward: to empower international real estate investors with the tools, expertise, and support they need to invest in US real estate with confidence and success, ensuring you receive the best terms and guidance to achieve your dream of owning US real estate.

Apply now and get started with your US real estate journey today!

Foreign National Loans: FAQs

Can foreign nationals close on a US mortgage from overseas?

Yes, it is possible. At HomeAbroad, we offer remote closing options so you can complete the process from anywhere in the world.

Do I need a US credit history to buy a house?

Foreign national loans are tailored for foreign buyers without a US credit history. We use credit reports from your home country and other assessment methods to bypass the traditional credit check.

What types of properties can I purchase with a mortgage if I am a non-US citizen?

Foreign nationals can buy various types of properties, including single-family homes, condos, townhouses, and investment properties. The type of property you can purchase may depend on the specific loan program and lender requirements.

How do I improve my chances of getting approved for a foreign national mortgage?

To improve your chances of approval, ensure you have all the required documentation and maintain a strong financial profile. We can help you organize all your documents so you can obtain your loan quickly and smoothly.

At HomeAbroad, we ensure the reliability of our content by relying on primary sources such as government data, industry reports, firsthand accounts from our network of experts, and interviews with specialists. We also incorporate original research from respected publishers when relevant. Discover more about our commitment to delivering precise and impartial information in our editorial policy.

National Association of Realtors: 2025 International Transactions in U.S. Residential Real Estate