Editorial Integrity

Making informed real estate decisions starts with having the right knowledge. At HomeAbroad, we offer US mortgage products for foreign nationals & investors and have a network of 500+ expert HomeAbroad real estate agents to provide the expertise you need. Our content is written by licensed mortgage experts and seasoned real estate agents who share insights from their experience, helping thousands like you. Our strict editorial process ensures you receive reliable and accurate information.

The 1% rule is a quick screening tool, not a complete investment analysis or lending requirement.

A property that meets the 1% rule can still produce weak cash flow or fail to support financing.

Evaluate operating expenses, cash flow, cap rate, and DSCR before deciding whether a rental property is a good investment.

For foreign national investors, the 1% rule is most effective for remotely shortlisting properties before conducting deeper due diligence.

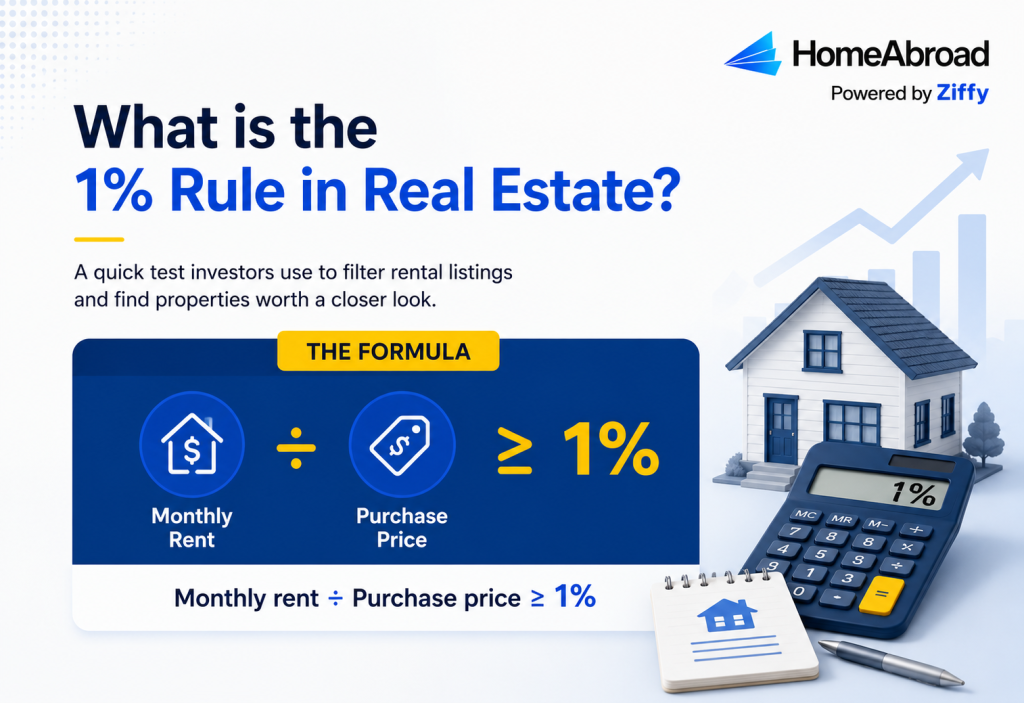

The 1% rule in real estate says a rental property should generate monthly rent equal to at least 1% of its purchase price. It remains a useful screening shortcut in 2026, but it shouldn’t be the only factor guiding an investment decision.

In many US markets, rising home prices, higher financing costs, and operating expenses mean a property can meet the 1% rule and still produce weak cash flow or fall short of underwriting requirements. This guide explains how the rule works, where it still applies, what it overlooks, and the metrics investors should use before making an offer.

Table of Contents

What Is the 1% Rule in Real Estate?

The 1% rule is a quick screening tool investors use to filter rental property opportunities before performing a detailed financial analysis. If the expected monthly rent equals at least 1% of the property’s purchase price, the investment may be worth investigating further. If it falls well below that threshold, many investors move on without spending additional time evaluating the property.

How to Calculate the 1% Rule

The calculation is straightforward:

Monthly Rent ÷ Purchase Price ≥ 1%

One of our recent foreign national clients was comparing two single-family rental properties before deciding which one to pursue. Both homes were located in the same market and had similar purchase prices, but their projected rental income told a different story.

Property Details | Property A | Property B |

|---|---|---|

Purchase Price | $246,000 | $323,000 |

Estimated Monthly Rent | $2,620 | $2,860 |

Rent-to-Price Ratio | 1.07% | 0.89% |

Using the 1% rule as an initial screening tool, Property A met the benchmark:

$2,620 ÷ $246,000 = 1.07%

Property B fell well below it:

$2,860 ÷ $323,000 = 0.89%

The client chose to continue evaluating Property A while eliminating Property B from further consideration. From there, we moved beyond the 1% rule and reviewed projected cash flow, operating expenses, financing costs, and the property’s expected DSCR (Debt Service Coverage Ratio) before discussing financing options.

This shows why the 1% rule works best as a first-pass filter. Passing the rule doesn’t guarantee a property is a good investment or that it will qualify for financing. It simply identifies properties that deserve a deeper financial analysis.

You can also reverse the calculation to estimate your target rent. For example, a property priced at $350,000 would need approximately $3,500 in monthly rent to satisfy the 1% rule.

What the Rule Is Actually For

The 1% rule is designed to answer one question:

“Is this property worth analyzing further?”

Its purpose is to eliminate unsuitable properties quickly, not determine whether a deal is profitable.

This becomes especially useful when comparing dozens of listings across multiple cities or states, particularly for international investors evaluating properties remotely.

It’s equally important to understand what the rule doesn’t do.

The 1% rule is not a lending requirement. We do not approve or decline a mortgage based on whether a property meets this benchmark. Financing decisions rely on a broader review of the property’s income, the borrower’s financial profile, and the loan program’s underwriting requirements.

The 2% Rule and the Rent-to-Price Ratio

The 1% rule is one version of a broader rent-to-price measurement used by real estate investors.

The rent-to-price ratio measures a property’s monthly rent as a percentage of its purchase price. The 1% and 2% rules simply establish different benchmarks within that ratio.

The 2% rule sets a much higher threshold, requiring monthly rent equal to 2% of the purchase price. While this benchmark was achievable in certain lower-cost markets following the 2008 housing downturn, qualifying properties have become increasingly uncommon in today’s market. When they do exist, they often involve higher renovation costs, weaker tenant demand, or elevated investment risk.

Across many US markets today, rent-to-price ratios are generally lower than they were a decade ago, making the 1% rule a more realistic screening benchmark than the 2% rule for most investors.

1% vs. 2% at a Glance

1% Rule | 2% Rule | |

|---|---|---|

Monthly rent on a $200,000 property | $2,000 | $4,000 |

Common in 2026? | Select markets | Rare |

Best used for | Initial screening | Historical comparison |

Does the 1% Rule Still Work in 2026?

The 1% rule is still a useful way to screen rental properties, but it shouldn’t be the deciding factor when evaluating an investment. The market has changed in two important ways since the rule became popular.

Why the rule is harder to hit now

US home prices have risen faster than rents across most major metros over the past several years, which pushes rent-to-price ratios down. At the same time, mortgage rates remain well above the levels many investors locked in before 2022, so the debt payment on a given purchase price is larger.

A property can pass the 1% screen and still produce thin or negative cash flow once you account for today’s financing costs, insurance premiums, and property taxes.

What HomeAbroad’s own lending data shows

HomeAbroad’s research team recently ran a debt-coverage test on 4,178 financed investment-property purchases near US World Cup host stadiums between 2023 and 2025. The median property reached a modeled debt service coverage ratio of 0.82, meaning its normalized rental income would cover about 82 cents of every dollar of annual principal-and-interest debt service.

That figure is a modeled cash-flow test, not an observed profit-and-loss result, and it does not claim those owners are losing money. What it does show is how compressed the gap between purchase prices and achievable rents has become in high-demand markets: even properties that look close to the 1% threshold on paper frequently fail the coverage test a lender actually applies.

You can read the full methodology in the World Cup stadium real estate analysis.

Where it still works

The rule remains a realistic screen in parts of the Midwest and South, where purchase prices stayed moderate relative to rents. Cities like Cleveland, Memphis, Birmingham, and parts of Cincinnati and Indianapolis still produce listings at or near the 1% threshold. For market-by-market detail, see the guide to the best places to buy rental property in the USA.

Steven Glick

Director of Mortgage Sales · HomeAbroad

The 1% rule is useful for narrowing a long list of properties, but it’s not the point where financing decisions are made. Before moving forward, we want to see how the property’s rental income holds up after market-rent analysis and debt service are factored into the equation.

What the 1% Rule Leaves Out

The rule compares two numbers and nothing else. Everything that determines whether a rental actually makes money sits outside it.

Operating costs. Property taxes, insurance, HOA dues (homeowners association fees, a monthly charge common in US condos and planned communities), vacancy, repairs, capital expenditures, and property management. Two properties can both pass the 1% screen and land in opposite places once these are counted. A $200,000 home in a high-insurance coastal market and a $200,000 home in a low-tax Midwestern suburb are entirely different investments at the same rent.

Financing. The rule says nothing about interest rates, loan structure, down payment, or whether a lender will approve the deal at all.

Rent accuracy. The rule is only as good as the rent figure you feed it. Listing-site estimates often run higher than the market-rent figure a licensed appraiser will support during underwriting, and the appraiser’s number is the one that counts.

Appreciation and taxes. A property in a high-growth market can fail the 1% screen and still outperform over a full holding period. The rule measures none of that, and it says nothing about US tax treatment of rental income for foreign owners either.

The 1% rule does not tell you... → Whether the property cash flows after taxes, insurance, and management → Whether a lender will finance it → Whether the rent estimate will survive an appraisal → Anything about appreciation, tax treatment, or exit

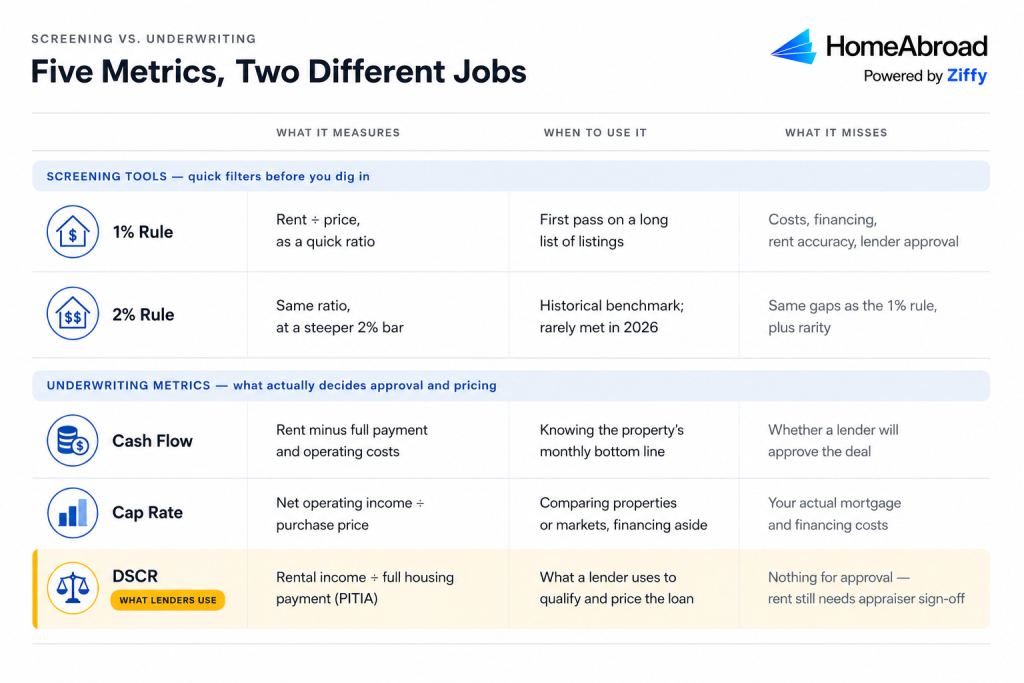

From Screening to Underwriting: DSCR, Cash Flow, and Cap Rate

Once a property passes your first screen, three metrics do the real work.

DSCR: the number lenders actually use

The debt service coverage ratio (DSCR) divides the property’s monthly rental income by its full monthly housing payment, known in US lending as PITIA (principal, interest, taxes, insurance, and association dues).

Take Property A from earlier, a $246,000 property purchased with 25% down. The PITIA comes to $2,150 per month against $2,620 in appraiser-supported rent:

$2,620 ÷ $2,150 = 1.21 DSCR

The property that “passed the 1% rule” now has a precise meaning for a lender: its income covers debt service with a 21% cushion. That is the conversation that determines approval and pricing. A DSCR loan qualifies on this ratio rather than on the borrower’s personal income, which is why it has become the standard financing route for international investors.

At HomeAbroad, we offer DSCR financing that foreign nationals can qualify for using the property’s rental income, without US credit history or US tax returns. Exact thresholds, down payment, and terms depend on the current program and the specific transaction.

Cash flow is the monthly bottom line: rent minus PITIA minus operating costs and reserves for vacancy and repairs. It is the number that tells you what the property pays you.

Cap rate (capitalization rate) divides annual net operating income by purchase price, ignoring financing. It is most useful for comparing properties and markets on equal footing.

A simple three-step screening sequence

- Screen with the 1% rule. Sort a long list of candidates down to a short one. Under 0.7%, be skeptical; near or above 1%, keep looking.

- Build a full cash-flow estimate. Add real figures for taxes, insurance, HOA, management, vacancy, and maintenance for that specific property and county.

- Run the DSCR before you offer. Use a conservative, comp-supported rent figure, not a listing-site estimate. A DSCR calculator gives you the ratio in a minute and tells you whether the deal is financeable on income-based terms.

Online rent estimates are a helpful starting point, but they aren’t what determines a property’s financing outcome. During underwriting, the appraiser’s market-rent analysis carries much more weight, and even a small difference in rental income can affect DSCR and the financing options available.

How International Investors Should Use the 1% Rule

For investors evaluating US properties from London, Dubai, Sydney, Mumbai, or anywhere outside the United States, the 1% rule is most valuable as a remote screening tool. Instead of analyzing every listing in detail, you can quickly compare opportunities across different cities and narrow your search to properties that deserve a closer look.

At HomeAbroad, our real estate agents use a similar approach when helping international investors search for properties remotely. We help clients identify markets that align with their investment goals, screen potential rental properties, and narrow a long list of opportunities before moving to detailed financial analysis and financing discussions.

Two adjustments matter when screening remotely. First, treat online rent estimates as a starting point only. We evaluate a property’s market rent using the appraiser’s analysis during underwriting, which may differ from the rental estimates shown on listing websites. Validating rental income early can help you avoid spending time and money on properties that may not perform as expected.

Second, don’t rely on the 1% rule alone when comparing properties from overseas. Once you’ve created a shortlist, review each property’s projected cash flow, operating expenses, and DSCR using realistic financing assumptions before deciding which opportunities are worth pursuing.

Investors planning to grow beyond a first property can see how these screens fit a longer plan in the guide to buying multiple rental properties as a foreign national.

Ready to invest in your first US rental property? At HomeAbroad, we help international investors every step of the way, from identifying high-potential markets and screening investment properties to evaluating cash flow and securing financing. Whether you’re purchasing your first rental property or expanding your portfolio, our team is here to help you make informed investment decisions with confidence.

FAQs

Do lenders require the 1% rule?

No. Lenders test debt coverage, credit factors, and reserves. For investment properties financed on rental income, the DSCR is the metric that decides approval and pricing, and programs exist for ratios both above and below 1.0.

What is a good rent-to-price ratio in 2026?

It depends on the market and your goal. Cash-flow-focused investors typically want to see 0.8% or better before digging in, while investors targeting high-appreciation metros often accept lower ratios and underwrite the deal on total return instead

Does the 1% rule apply to short-term rentals?

Not cleanly. Short-term rental income is seasonal and expense-heavy, so a monthly rent multiple built for long-term leases misreads it. STR deals are better screened on projected annual revenue against total annual costs, then tested with a DSCR based on the income figure the lender’s appraisal process will accept.