Editorial Integrity

Making informed real estate decisions starts with having the right knowledge. At HomeAbroad, we offer US mortgage products for foreign nationals & investors and have a network of 500+ expert HomeAbroad real estate agents to provide the expertise you need. Our content is written by licensed mortgage experts and seasoned real estate agents who share insights from their experience, helping thousands like you. Our strict editorial process ensures you receive reliable and accurate information.

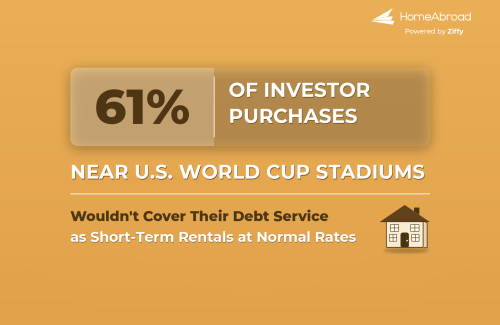

Most investors who bought a home near a U.S. World Cup stadium in the past three years would not cover principal-and-interest debt service if they ran it as a short-term rental at normal, non-tournament rates.

A HomeAbroad analysis of 4,178 financed investment-property purchases within three miles of the eleven U.S. host stadiums (2023-2025) finds that 61% would fall below a 1.0x debt-service coverage ratio, the standard test of whether rental income covers the loan, from 11% in Kansas City to 97% in Los Angeles.

Each property is priced on its market’s normalized booked short-term-rental revenue and the actual interest rate the borrower received. The analysis does not claim these owners are losing money, that any will default, or that anyone bought because of the tournament.

Note: This is a modeled cash-flow test, not a crash story or observed profit-and-loss statement. It asks whether HMDA-recorded, financed investment-property purchases within three miles of U.S. World Cup stadiums would cover principal-and-interest debt service if operated as short-term rentals at ordinary, non-tournament booked revenue. It does not claim these properties are currently short-term rentals, that owners are losing money or will default, or that the World Cup caused any purchase.

Table of Contents

61% of investor purchases near U.S. World Cup stadiums would miss STR break-even at normal rates.

Across 4,178 HMDA-recorded financed investment-property purchases within three miles of the eleven U.S. host stadiums, 2,566 would not cover principal-and-interest debt service as normalized short-term rentals. The median property covers about 82 cents of every debt-service dollar.

$1.32B in stadium-area investor lending is tied to below-coverage properties.

The below-coverage loans represent roughly 82% of all lending in the analysis, $1.32 billion out of $1.61 billion. The dollar exposure is larger than the loan-count share because weaker-coverage markets often carry larger loan balances.

Los Angeles and Kansas City show the clearest split.

Near SoFi Stadium, 97.2% of recent investor purchases fall below 1.0x DSCR. Near Arrowhead Stadium, only 10.7% do. The rental revenue is nearly identical in the model, but the average loan near SoFi is about $659K versus $155K near Arrowhead.

Miami saw the fastest investor buildup, and the highest borrowing cost.

Investor purchases near Hard Rock Stadium rose about 62% from 2023 to 2025, the fastest increase of any U.S. host market. Miami also has the highest average actual investor rate at 9.1% and the highest benchmark insurance cost, pushing 74.0% of purchases below coverage.

Atlanta had the most investor purchases; Philadelphia had the strongest coverage among high-volume markets.

Atlanta leads all U.S. host markets with 896 stadium-area investor purchases, but 61.2% fall below 1.0x DSCR. Philadelphia has the second-most purchases at 826, yet only 46.9% fall below coverage and its median DSCR clears at 1.07.

At Normal STR Rates, the Median Stadium-Area Investor Purchase Covers Only 82 Cents per Debt-Service Dollar

Debt-service coverage is the core test a lender applies to an income property: the ratio of the property’s net operating income to its debt payments. A DSCR of 1.0x means net income exactly covers debt service; below 1.0x, the income falls short and the owner must cover the gap from other sources.

The analysis applies that test to every stadium-adjacent investment purchase, using normalized booked short-term-rental income and each loan’s actual interest rate.

1. Across 4,178 stadium-area investor purchases, 61.4% would fall below 1.0x DSCR if operated as short-term rentals at normalized rates, with a median coverage of 0.82.

Of the 4,178 financed, one-to-four-unit investment-property purchases recorded within three miles of a U.S. host stadium in 2023-2025, together representing $1.61 billion in mortgage lending, 2,566 would not cover their debt under the modeled scenario.

The median property reaches a DSCR of 0.82, meaning that after operating costs, its normalized short-term-rental income would cover about 82 cents of each dollar of its annual principal-and-interest debt service.

Several cost inputs are conservative, especially property tax and insurance, while the rental-income side still applies market-level STR revenue uniformly within each market.

Income is each market’s normalized, non-tournament booked short-term-rental revenue, what guests have actually paid in ordinary periods, not the elevated asking rates seen during the event window, and not a forward projection.

Debt is priced at the actual interest rate each borrower received, which the mortgage record reports directly for roughly 95% of these loans. The scenario does not assume any World Cup revenue at all; it asks whether these properties work as ordinary short-term rentals once the tournament passes, which is the question that determines whether an owner can hold the property for the long run.

2. The majority finding holds across every reasonable operating-cost assumption, from 56.6% below to 66.2%.

Operating costs are the largest discretionary input in any DSCR model, so the analysis tests a range rather than a single point.

Holding property tax and insurance fixed at their market-specific dollar levels and varying only the revenue-based operating costs, management, cleaning, utilities, supplies, and maintenance, the share below 1.0x moves only within a narrow band.

Variable operating cost (share of revenue) | Share below 1.0x DSCR | Median DSCR |

|---|---|---|

25% (most generous) | 56.6% | 0.89 |

30% (base case) | 61.4% | 0.82 |

35% (most conservative) | 66.2% | 0.74 |

Note: Operating costs in every scenario also include market-specific property tax (county effective rate applied to property value) and insurance (state benchmark premium), held constant across the three columns. Figures are calculated on unrounded values. The base case (30%) is used throughout the rest of this analysis.

Even under the most generous 25% variable-cost assumption, more than half of these purchases would still fall below 1.0x DSCR. The finding is therefore not an artifact of a single cost choice; it reflects the price, leverage, and rate levels at which these properties were bought.

3. $1.32B of Stadium-Area Investor Lending is Tied to Below-Coverage Properties

Because the weakest-coverage markets also carry the largest loans, the shortfall is even more concentrated in dollar terms than in loan-count terms.

Of the $1.61 billion in stadium-adjacent investment lending, about $1.32 billion, roughly 82% is attached to properties that would fall below 1.0x DSCR in the modeled scenario.

For those properties, the median monthly gap between modeled net income and principal-and-interest debt service is about $1,400.

This is a modeled shortfall, not an observed loss. It estimates the monthly cash-flow gap an owner would face if the property were operated as a short-term rental at ordinary booked revenue and produced the modeled net income.

The gap varies widely by market, from a few hundred dollars in Dallas to several thousand in the most expensive coastal markets.

Nearly the Same Rent, Four Times the Debt: Why Kansas City Clears and Los Angeles Falls Short

A single national average hides the most important pattern in the data. When the eleven markets are ranked by the share of purchases below 1.0x, the order is set almost entirely by local affordability, the relationship between what a property costs to buy and finance and what it earns as a rental, rather than by anything about the tournament.

Note: Markets are ranked by the share of HMDA-recorded stadium-adjacent investment-property purchases from 2023-2025 that fall below 1.0x DSCR in the base-case model. “Normalized annual booked STR revenue” is the market’s ordinary annual booked entire-home short-term-rental revenue input used in the model. “Median monthly shortfall” is the median among below-coverage loans only (DSCR below 1.0x); markets where most properties clear still show a positive figure here because it describes only the loans that fall below coverage, not the marketwide median. Boston’s figures rest on only 26 purchases because Gillette Stadium sits in a low-density area; they should be read as indicative only. Figures are rounded for readability; calculations use unrounded values.

4. The share below 1.0x ranges from 97.2% in Los Angeles to 10.7% in Kansas City- a spread the national average completely hides.

The full ranking places the expensive coastal markets at the top and the affordable interior markets at the bottom. In Los Angeles, Santa Clara, and the New York/New Jersey market, more than nine in ten purchases would fall short. In Kansas City, fewer than one in nine would.

The clearest way to see the pattern is to set the two ends of the table side by side. The decisive difference is not revenue, Kansas City’s normalized booked revenue ($41,713) is actually higher than Los Angeles’s ($41,066). It is price and the debt that comes with it.

Metric | Los Angeles | Kansas City |

|---|---|---|

Stadium | SoFi | Arrowhead |

Investor purchases | 457 | 318 |

Average loan | $659K | $155K |

Normalized annual booked STR revenue | $41,066 | $41,713 |

Average actual rate | 8.4% | 8.5% |

Median DSCR | 0.36 | 2.15 |

Share below 1.0x | 97.2% | 10.7% |

Note: Nearly identical rental revenue and interest rates; the coverage outcome is driven almost entirely by the four-fold difference in loan size.

A property earning roughly the same rent covers more than two dollars of debt for every dollar owed in Kansas City and about 36 cents in Los Angeles, because the Los Angeles property carries more than four times the loan.

That is the core of the analysis: a short-term rental near a stadium is not inherently a strong or weak investment, its coverage depends on the price paid and the leverage taken on, which vary enormously by market.

One caveat applies to that comparison: rental revenue is applied at the market level, so within-market differences in coverage reflect price, leverage, and rate rather than property-specific rental income. Actual revenue likely scales with property value, which would temper the most extreme coastal readings

Amresh Singh

Founder and CEO | HomeAbroad

Hold the rent and the rate roughly constant, and the result still flips from comfortably covered to deeply short. The driver is price and leverage, not the rent, and not the World Cup. We modeled on normalized booked revenue so the tournament spike couldn’t flatter the math.

Insurance in Miami and Property Taxes Near MetLife Push More Loans Below Coverage

Price and leverage explain the coastal extremes, but they do not fully explain why Miami sits so high in the ranking despite mid-range home prices, or why the New York/New Jersey market joins California at the top. There, the pressure comes from the second half of the operating-cost equation: property tax and insurance.

5. Annual property tax and insurance run about $11,600 per property in the New York/New Jersey market and $9,700 in Miami, versus roughly $4,300 in Philadelphia, and that gap reshapes the ranking.

The analysis prices carrying costs with market-specific inputs rather than a single national assumption: each county’s effective property-tax rate applied to the property’s value, plus a state benchmark insurance premium. Those inputs vary sharply, and the variation maps onto the coverage ranking.

Market | Effective Property-tax rate | Benchmark Annual insurance | Median Annual tax + insurance | Effective Operating-cost ratio | Share below 1.0x |

|---|---|---|---|---|---|

New York/New Jersey | 1.592% | $1,214 | $11,642 | 60% | 91.5% |

Santa Clara | 0.624% | $1,641 | $10,689 | 47% | 92.4% |

Miami | 0.765% | $5,838 | $9,701 | 48% | 74.0% |

Boston | 0.994% | $1,733 | $7,846 | 38% | 30.8% |

Los Angeles | 0.725% | $1,641 | $7,840 | 49% | 97.2% |

Seattle | 0.875% | $1,539 | $7,795 | 45% | 68.9% |

Dallas | 1.185% | $3,899 | $7,276 | 50% | 53.4% |

Houston | 0.877% | $3,899 | $7,188 | 50% | 62.9% |

Atlanta | 0.982% | $2,041 | $5,822 | 45% | 61.2% |

Philadelphia | 0.973% | $1,278 | $4,294 | 42% | 46.9% |

Kansas City | 1.114% | $2,191 | $4,140 | 40% | 10.7% |

Note: Effective property-tax rate is the ATTOM 2025 county effective rate applied to property value; insurance is a Bankrate 2026 state benchmark annual premium for $300,000 in dwelling coverage. “Effective operating-cost ratio” is the median of all operating costs (variable costs plus tax and insurance) as a share of revenue. These are all-homes and owner-occupied benchmarks; see the methodology note on why they make the coverage shortfall a conservative floor.

Two distinct mechanisms are visible. In the New York/New Jersey market, the driver is property tax: Bergen County’s 1.592% effective rate is the highest in the field and, on a mid-priced home, produces a tax-and-insurance load above $11,600 a year, enough to lift the market to a 60% effective operating-cost ratio, the highest here.

In Florida, the driver is insurance: Miami’s state benchmark premium ($5,838) is far above any other market’s, which on its own pushes Miami to 74.0% below 1.0x even though its homes cost less than Seattle’s or Los Angeles’s.

The Texas markets are more moderate on this measure than a casual reader might expect. On ATTOM’s all-homes effective rates, 0.877% in Harris County (Houston) and 1.185% in Tarrant County (Dallas), Houston lands at 62.9% below and Dallas at 53.4%, with Dallas’s median property essentially at break-even (0.98x).

One caveat matters here and is disclosed in full in the methodology: these effective rates are averages across all single-family homes, most of which are owner-occupied and may benefit from homestead exemptions, assessment caps, or other owner-occupant protections that investment-property owners do not receive.

That makes the Texas and Florida estimates especially conservative because investor-owned properties may face higher property-tax or insurance costs than the model assumes. In Texas in particular, the coverage shown here is best read as a conservative floor rather than a worst case.

Investor Purchases Rose Even as Stadium-Area Borrowers Paid Rates Near 8%

The debt side of the coverage equation carries its own findings. Investment-property loans price above owner-occupied mortgages, and the actual rates recorded for these purchases show how much more these borrowers are paying to carry the debt the coverage test measures against.

6. Stadium-area investors borrowed at an average actual rate of 8.16%, about 1.7 percentage points above the owner-occupied benchmark.

The Freddie Mac headline 30-year rate, which describes owner-occupied, prime, conforming loans, stood at 6.47% on June 18, 2026 and 6.49% on June 25, 2026.

The investment-property purchases in this analysis carry an average actual originated rate of 8.16%, roughly 1.7 percentage points higher, the premium lenders attach to non-owner-occupied loans.

Because the analysis prices each property’s debt at its own recorded rate rather than the headline figure, the coverage test reflects what these borrowers actually pay, not a more flattering benchmark.

The rate also varies by market in ways that compound the coverage picture. Investors near Hard Rock Stadium in Miami carried the highest average rate at 9.1%, while those in Houston carried the lowest at 7.6%. Miami’s combination of the field’s most expensive debt and its highest insurance load is why it sits high in the ranking despite mid-range home prices.

7. Stadium-adjacent investor purchases rose 22% from 2023 to 2025, led by Miami and Seattle, while Kansas City was the only market where activity fell.

Even as rates stayed elevated, the pace of stadium-area investment buying increased every year across the period.

Year | Investor Purchases | Lending Volume |

|---|---|---|

2023 | 1,255 | $438M |

2024 | 1,396 | $550M |

2025 | 1,527 | $619M |

Note: Stadium-adjacent (three-mile), originated, one-to-four-unit investment-property purchases across all eleven U.S. host markets. 2025 figures draw from the early-release federal dataset and are preliminary.

The national rise was uneven, and the spread is itself a local story. Miami led with a 62% increase in stadium-adjacent investment purchases from 2023 to 2025, followed by Seattle (+55%), New York/New Jersey (+41%), and Los Angeles (+35%).

At the other end, Kansas City, the one market where the large majority of these purchases would comfortably cover their debt, was the only market where investor buying declined, falling 21% over the same period. The markets where investors leaned in hardest were, for the most part, the markets where the modeled coverage is weakest.

Debjit Saha

Co-Founder and CTO | HomeAbroad

Investors kept buying here even with financing near 8%, yet most of these purchases wouldn’t cover their debt on normal, year-round income. A few weeks of tournament demand don’t change the arithmetic of a thirty-year loan, and that’s what disciplined underwriting should weigh.

Coastal Markets Would Need Far More Than a Small Rent Bump to Break Even

The coverage ratio also describes the size of the gap, not just its presence, and the gap is far wider in some markets than others.

8. The median stadium-area investor purchase earns about 82 cents per debt-service dollar; in the most expensive markets it earns less than 40.

Across all 4,178 purchases, the median DSCR of 0.82 means the typical property’s net operating income would cover about four-fifths of its debt service. But that single figure spans an enormous range.

In Philadelphia, the median property already clears at 1.07x; in Kansas City it clears at 2.15x, generating more than twice its debt payment. In Los Angeles, Santa Clara, and New York/New Jersey, the median sits between 0.36x and 0.40x, under 40 cents on the debt dollar.

Grouping the markets makes the distance to break-even concrete. The three expensive coastal markets (Los Angeles, Santa Clara, and New York/New Jersey) together show 95.3% below 1.0x and a median DSCR of 0.37 across 717 purchases.

The three Texas and Florida markets (Miami, Houston, and Dallas) show 63.3% below and a median of 0.85 across 984 purchases. The two most affordable markets (Kansas City and Philadelphia) show 36.8% below and a median of 1.33 across 1,144 purchases.

That difference defines how far each group is from break-even. A market clustered near 0.85x would need a meaningful but conceivable combination of lower leverage, higher rents, or lower rates to reach 1.0x.

A market at 0.37x would need its net operating income to roughly triple, or its debt service to fall by about two-thirds, to reach 1.0x, a gap that ordinary rate or rent movement does not close.

This analysis does not forecast whether any of those inputs will change; it measures the distance between current cash flow and break-even as it stands. The distance is modest in the affordable interior markets and very large on the expensive coasts.

Methodology

This analysis combines four data layers: HMDA loan-level mortgage records, Census tract geography, short-term-rental revenue data, and market-specific operating-cost benchmarks.

The analysis covers the eleven U.S. host stadiums for the 2026 FIFA World Cup and does not include the Canadian or Mexican host venues.

Loan records come from the federal Home Mortgage Disclosure Act dataset available through the FFIEC/CFPB HMDA platform.

The analysis uses HMDA-recorded, originated home-purchase loans from 2023, 2024, and 2025, filtered to investment-property occupancy and one-to-four-unit dwellings. These records are used to identify financed investor purchases near the eleven U.S. World Cup host stadiums only.

Stadium-area geography is defined using Census tract centroids. Each HMDA loan record carries a census tract, and the analysis keeps loans in tracts whose 2020 centroid lies within three miles of a U.S. host stadium. This creates a consistent stadium-adjacent loan universe across all markets.

Short-term-rental income comes from AirROI market data. The model uses normalized annual booked entire-home STR revenue for each host market, rather than event-window pricing or asking rates for unbooked inventory. This keeps the cash-flow test focused on ordinary, non-tournament rental income.

Debt service is calculated from each loan’s amount, actual originated interest rate, and loan term. Annual debt service is twelve times the monthly principal-and-interest payment.

Where a usable actual rate is unavailable, the market median rate is used.

Because public HMDA loan amounts and property values are privacy-modified and approximate, and because property tax and insurance are estimated from market-level benchmarks rather than actual property bills, the model is best read as a standardized market comparison, not a property-level underwriting file.

Operating costs combine three inputs: variable operating costs, property tax, and insurance. The base case uses variable costs equal to 30% of normalized annual booked STR revenue. Property tax is modeled using county-level effective property-tax rates from ATTOM’s 2025 Property Tax Analysis, applied to property value.

Insurance is modeled using state-level average annual homeowners premiums for $300,000 in dwelling coverage from Bankrate, as published in 2026. Both are market-level benchmarks applied uniformly within each market, not property-specific bills.

These benchmarks are deliberately conservative. ATTOM’s effective tax rates are averages across all single-family homes, most of which are owner-occupied and receive homestead exemptions and assessment caps that an investment-property owner does not, so in states with large homestead benefits (notably Texas and Florida) the rate an investor actually pays is higher than the benchmark used here.

The insurance benchmark likewise reflects owner-occupied policies, while landlord and short-term-rental policies typically cost more. Both choices push modeled operating costs downward, making the reported coverage shortfall a conservative floor rather than an overstatement.

Percentages, medians, and totals are calculated on unrounded values, so rounded figures shown in tables may not reproduce the exact results if recalculated from the displayed numbers.

Data Sources

1. HMDA loan-level data

The analysis uses loan-level records from the FFIEC/CFPB HMDA platform to identify financed, originated, one-to-four-unit investment-property purchases in the eleven U.S. World Cup host markets from 2023 to 2025.

2. Census tract geography

2020 Census tract geography is used to define the three-mile stadium-adjacent area around each U.S. host stadium. Loans are included when their Census tract centroid falls within that three-mile radius.

3. Short-term-rental revenue

Normalized annual booked entire-home short-term-rental revenue for each market comes from AirROI. These are booked revenue figures, realized transaction revenue, not asking rates or unbooked list-window pricing, and are used to reflect ordinary, non-tournament income.

4. Property-tax benchmarks

County-level effective property-tax rates come from ATTOM’s 2025 Property Tax Analysis and are applied to each property’s value.

5. Insurance benchmarks

State-level average annual homeowners premiums for $300,000 in dwelling coverage come from Bankrate, as published in 2026.

6. Mortgage-rate reference

The Freddie Mac Primary Mortgage Market Survey 30-year rate (6.47% on June 18, 2026) is used only as a macro reference for the owner-occupied benchmark; it is not used to price any individual loan.

The market-level tax and insurance benchmarks applied in the model are:

| Market | County (effective tax rate, ATTOM 2025) | State (annual insurance, Bankrate 2026) |

| Los Angeles | Los Angeles, CA – 0.725% | California – $1,641 |

| Santa Clara | Santa Clara, CA – 0.624% | California – $1,641 |

| Seattle | King, WA – 0.875% | Washington -$1,539 |

| Kansas City | Jackson, MO -1.114% | Missouri – $2,191 |

| Dallas | Tarrant, TX – 1.185% | Texas – $3,899 |

| Houston | Harris, TX – 0.877% | Texas – $3,899 |

| Atlanta | Fulton, GA – 0.982% | Georgia -$2,041 |

| Miami | Miami-Dade, FL – 0.765% | Florida – $5,838 |

| Boston | Norfolk, MA – 0.994% | Massachusetts – $1,733 |

| New York/New Jersey | Bergen, NJ – 1.592% | New Jersey – $1,214 |

| Philadelphia | Philadelphia, PA – 0.973% | Pennsylvania – $1,278 |

Definitions

Term | Definition |

| 1. Stadium-adjacent investor purchase | A HMDA-recorded, financed, originated home-purchase loan for a one-to-four-unit investment property in a Census tract whose centroid lies within three miles of a U.S. World Cup host stadium. |

| 2. Debt-service coverage ratio | Modeled net operating income divided by annual principal-and-interest debt service. |

| 3. Below coverage | A modeled DSCR below 1.0x, meaning modeled net income does not fully cover annual principal-and-interest debt service. |

| 4. Normalized annual booked STR revenue | Market-level annual booked entire-home short-term-rental revenue intended to reflect ordinary, non-tournament income. |

| 5. Principal-and-interest debt service | The annualized loan payment for principal and interest only, calculated from loan amount, interest rate, and loan term. |

| 6. Variable operating costs | Revenue-based operating costs such as management, cleaning, supplies, maintenance, utilities, and other recurring operating expenses. |

| 7. Carrying costs | Property tax and insurance in this model. |

| 8. Effective operating-cost ratio | Total modeled operating costs as a share of normalized annual booked STR revenue. |

| 9. Economic DSCR model | A standardized cash-flow test used for comparison across markets. It is not a lender-specific underwriting decision. |

Calculation Method

The main calculation tests whether each property’s modeled net operating income covers annual principal-and-interest debt service.

Annual DSCR equals modeled net operating income divided by annual principal-and-interest debt service. Modeled net operating income equals normalized annual booked STR revenue minus operating costs. Operating costs equal variable operating costs plus benchmark property tax plus benchmark insurance.

Variable operating costs are set at 30% of revenue in the base case. Property tax is calculated by applying the market’s ATTOM effective property-tax rate to property value. Insurance is assigned using the relevant Bankrate state benchmark annual premium. A property is counted as below coverage when its modeled DSCR is below 1.0x.

| DSCR = (normalized annual booked STR revenue − operating costs) ÷ annual principal-and-interest debt service |

Operating costs = 30% of revenue + property tax + insurance

Sensitivity Testing

To test whether the finding depends too heavily on one operating-cost assumption, the model uses three variable-cost scenarios:

- 25% of revenue

- 30% of revenue

- 35% of revenue

In all three scenarios, property tax and insurance remain fixed at their market-specific benchmark levels. Only the revenue-based operating-cost assumption changes.

Replicability

To replicate the calculation:

- Pull HMDA loan-level records for the relevant U.S. World Cup host markets for 2023, 2024, and 2025.

- Filter to originated home-purchase loans with investment-property occupancy and one-to-four-unit dwellings.

- Use 2020 Census tract geography to identify tracts whose centroid lies within three miles of each U.S. host stadium.

- Keep the loans located in those tracts.

- Attach each market’s normalized annual booked entire-home STR revenue from AirROI.

- Calculate each loan’s annual principal-and-interest debt service using loan amount, actual originated interest rate, and loan term.

- Apply the base-case operating-cost model: 30% of revenue plus the ATTOM county property-tax benchmark and the Bankrate state insurance benchmark.

- Calculate annual DSCR for each loan.

- Count the share of loans below 1.0x overall and by market.

- Repeat the calculation using 25% and 35% variable operating-cost assumptions for the sensitivity test.

Limitations

- HMDA captures financed mortgage activity reported by covered institutions. It does not capture all-cash purchases or every entity, commercial, or non-HMDA-covered financing structure.

- The investment-property flag does not show whether a property is actually operated as a short-term rental.

- The analysis does not claim the World Cup caused any purchase, operating strategy, or cash-flow shortfall.

- Loan amounts and property values in public HMDA data are modified for privacy and should be interpreted as approximate for per-property modeling.

- Where HMDA property value is exempt or missing (about 5% of records), value is estimated by dividing the loan amount by an assumed 75% loan-to-value ratio.

- Rental revenue is modeled at the market level, while loan exposure is measured at the Census-tract level. Actual near-stadium revenue may differ from the broader market input.

- Normalized booked STR revenue is not a forecast and may change over time. The same normalized market revenue is applied to 2023-2025 purchases and is not adjusted by purchase year.

- Property-tax and insurance inputs are benchmarks, not actual property-specific bills.

- The model focuses on principal-and-interest debt service. Property tax and insurance are treated as operating and carrying costs rather than as part of a lender-specific PITIA denominator.

- The model does not include HOA dues, furnishing costs, income taxes, depreciation, reserves, capital expenditures, special assessments, or local STR regulatory compliance costs unless captured indirectly in the variable operating-cost assumption.

- The analysis is descriptive and conditional. It does not claim that borrowers are distressed, that properties are unprofitable under other strategies, or that any loan will default.

- 2025 HMDA figures use the available public HMDA release and may be updated in later dynamic datasets if late submissions or resubmissions are incorporated.

Notes

- Rounded table values may not exactly reproduce percentages, medians, or totals because calculations use unrounded data.

- The model uses normalized annual booked STR revenue, not World Cup event-window revenue or asking prices for unbooked short-term-rental inventory.

- The coverage test is designed for consistent market comparison, not property-level underwriting.

- Additional analysis, including broader market-area cuts and non-U.S. host-venue comparisons, is available upon request at [email protected].

![DSCR Loan Rates Today [July, 2026]](https://homeabroadinc.com/wp-content/uploads/2022/09/dscr-loan-interest-rates.png)

![DSCR Loan Refinance: How to Qualify & Maximize Benefits [2026]](https://homeabroadinc.com/wp-content/uploads/2024/11/DSCRLoanRefinance.jpg)