Editorial Integrity

Making informed real estate decisions starts with having the right knowledge. At HomeAbroad, we offer US mortgage products for foreign nationals & investors and have a network of 500+ expert HomeAbroad real estate agents to provide the expertise you need. Our content is written by licensed mortgage experts and seasoned real estate agents who share insights from their experience, helping thousands like you. Our strict editorial process ensures you receive reliable and accurate information.

Quick answer:

A rate and term refinance replaces the existing mortgage on your US investment property with a new loan that lowers your interest rate, changes your loan term, or both, without taking cash out. For foreign national investors, HomeAbroad qualifies the refinance based on the property’s rental income rather than US personal income or an established US credit history.

If interest rates have fallen, your fixed or interest-only period is ending, or you want to improve monthly cash flow without using your property’s equity, a rate and term refinance may be the right solution. HomeAbroad also supports remote closings, allowing eligible foreign investors to refinance without traveling to the United States.

A rate and term refinance lowers your interest rate or adjusts your loan term. It does not increase your loan balance or hand you cash at closing.

HomeAbroad qualifies foreign national investors on the property’s rental income through a DSCR loan, an established US credit history is not required.

Because no equity leaves the property, rate and term financing generally prices below a cash-out refinance and often carries lighter seasoning requirements.

The refinance is judged on appraised market rent, which can differ from the rent on your current lease. That difference drives your qualifying ratio.

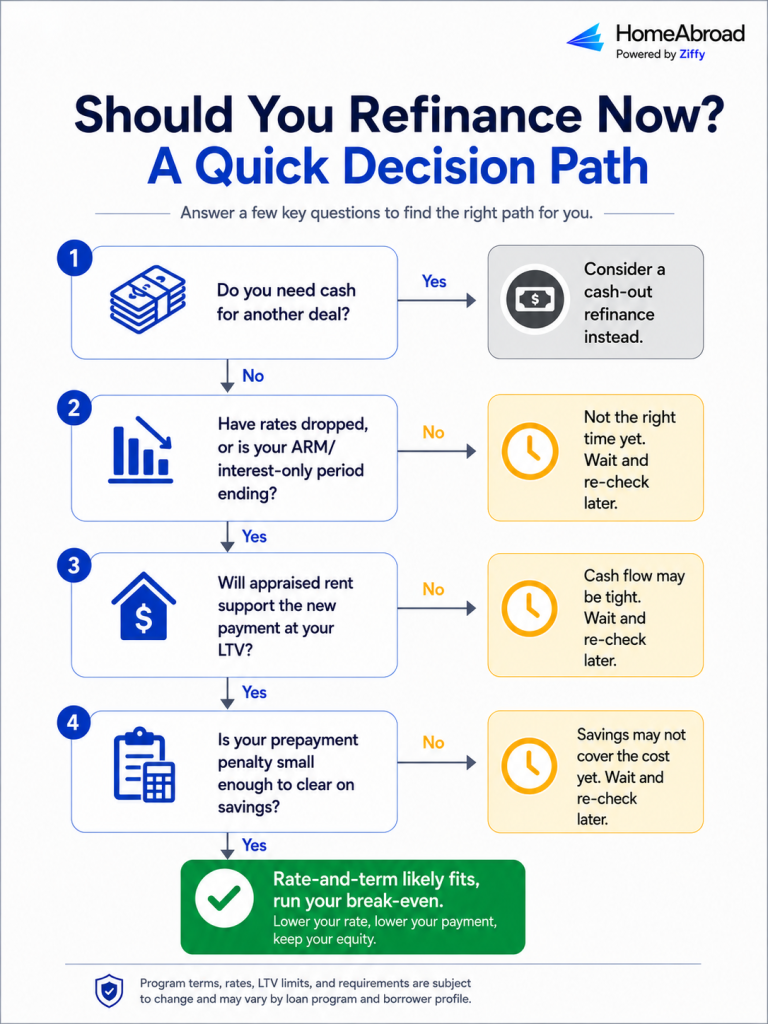

The decision comes down to break-even: weigh closing costs and any prepayment penalty on your existing loan against your monthly savings.

Table of Contents

A rate-and-term refinance replaces the existing loan on your US rental property with a new one at a lower interest rate or a different term, without increasing the balance and without taking cash out. For foreign national investors, HomeAbroad offers this through a DSCR (Debt Service Coverage Ratio) loan, which qualifies you on the property’s rental income rather than on US personal income or credit history.

For investors, the biggest advantage is the opportunity to reduce monthly payments and improve cash flow while keeping existing equity in the property. This guide explains how a rate-and-term refinance works, when it makes financial sense, how foreign national investors qualify, and the key factors to evaluate before deciding whether refinancing is the right move.

What a Rate-and-Term Refinance Is (and What It Is Not)

Refinancing means replacing your current mortgage with a new one. A rate-and-term refinance keeps the loan amount essentially the same and changes the economics of the loan: a lower interest rate, a longer or shorter term, or a switch from an adjustable rate to a fixed one. The point is a lower payment and steadier cash flow, not a lump sum of cash.

A cash-out refinance does the opposite. It replaces your loan with a larger one and pays you the difference from the equity you have built. Both start from the same property, but they solve different problems. One lowers your carrying cost. The other frees up capital.

For an investor, the label matters because it changes your pricing, your loan-to-value ceiling, and sometimes how long you have to wait before you qualify. Loan-to-value, or LTV, is the loan amount divided by the property’s appraised value, expressed as a percentage.

Rate-and-Term vs Cash-Out at a Glance

Feature | Rate and Term Refinance | Cash Out Refinance |

|---|---|---|

Main purpose | Lower rate or change term | Access equity as cash |

Effect on loan balance | Stays about the same | Increases |

Cash to you at closing | None (beyond minor adjustments) | Yes, the equity drawn |

Typical LTV ceiling | Up to 75% | Up to 70% |

Relative pricing | Lower rate premium | Higher rate premium |

Seasoning | Often lighter | Usually a set ownership period |

Best fit | Improving monthly cash flow | Funding the next deal |

For the equity-access side of this decision, see HomeAbroad’s guide to the foreign national cash-out refinance.

Why “No Cash Out” Changes Your Terms

The reason rate-and-term and cash-out price differently is risk. When you take cash out, the lender extends more credit against the same property, which raises its exposure. When you only reset the rate or term, the loan balance holds steady and the lender’s position stays roughly where it was.

Lower risk generally means a lower rate premium on rate-and-term financing, and it can mean fewer restrictions on when you are allowed to refinance. That pricing gap is not academic. On a loan you plan to hold for years, even a fraction of a percentage point compounds into real money.

Lucas Hernandez

Mortgage Loan Originator, HomeAbroad

One of the first questions I ask is whether the investor needs access to equity or simply wants a lower payment. If improving cash flow is the priority, a rate and term refinance is often the more efficient option because you’re replacing the existing loan rather than increasing it. That difference can affect both pricing and eligibility.

How Rate-and-Term Refinancing Works for Foreign National Investors

The mechanics that set HomeAbroad apart from a domestic lender are in how you qualify and how the property is measured. This is where a foreign national investor needs the detail, because most refinance guides assume a US borrower with a US credit score and US tax returns.

Qualifying on Property Income, Not Personal Income

A DSCR loan asks a single underwriting question: does the property’s rent cover its own mortgage payment? The ratio is the property’s gross rent divided by its PITIA, which stands for principal, interest, taxes, insurance, and association dues where a homeowners association applies. A DSCR of 1.0 means rent exactly covers the payment. Above 1.0 means the property produces surplus cash flow.

Because the property carries the qualification, you do not need an established US credit history to refinance. That point is easy to misread, so it is worth stating plainly: no US credit history required does not mean no documentation, or automatic approval.

HomeAbroad still verifies identity, assets, reserves, and the property’s income. It means your qualification does not hinge on a US credit score you may never have had the chance to build. For the full mechanics of how these loans are underwritten, see HomeAbroad’s DSCR loans guide.

The Appraisal and Market-Rent Reality

One detail surprises foreign national investors more than almost any other. When HomeAbroad orders the appraisal, underwriting uses the appraiser’s estimate of market rent, not necessarily the rent written into your current lease. An appraisal is an independent professional estimate of the property’s value and, for investment properties, its market rent.

In markets where rents have softened, appraised market rent can come in below your signed lease. When it does, your qualifying DSCR at underwriting is lower than you expected, which can affect the rate and the maximum loan you qualify for. Knowing this before you apply lets you check recent rent comparables in your area and set realistic expectations.

Before ordering the appraisal, I encourage investors to review comparable rentals in the neighborhood. That gives them a more realistic expectation and helps avoid surprises if the appraiser’s opinion differs from the current lease.

How HomeAbroad Helped a Canadian Investor Refinance a Mississippi Rental

One of our Canadian clients owned a single-family rental property in Laurel, Mississippi, and wanted to refinance the property into a long-term financing solution that aligned with its rental income. The investor had purchased the property for $420,000 and, like many foreign national investors, didn’t have US credit history or US income documentation to qualify for a conventional refinance.

HomeAbroad structured a DSCR refinance for the property with a $263,000 loan amount and a 30-year fixed interest rate of 6.625%. Instead of evaluating the borrower’s personal income or US tax returns, qualification was based on the property’s ability to support the mortgage payment through its rental income.

The refinance moved from application to closing in 26 days, providing the investor with long-term financing built around the property’s income profile rather than traditional US borrower qualifications.

This transaction demonstrates how a DSCR refinance can help foreign national investors replace existing financing with a long-term loan structure without relying on US credit history or personal income documentation. Every refinance is subject to current underwriting guidelines, property performance, and program requirements.

Want to see the complete transaction? Read our full Canadian investor DSCR refinance case study to learn how HomeAbroad structured the loan and guided the refinance from application to closing.

Documents You’ll Need

Requirements vary by borrower and by the current program, but a foreign national DSCR refinance file generally includes:

- Passport or government identification

- Proof of funds and reserves

- Details and a payoff statement for your existing loan

- Lease agreement and proof of rent collection

- Entity documents, if the property is held in a limited liability company (LLC)

- Property insurance information

- The appraisal, ordered through HomeAbroad during underwriting

Treat this as a starting checklist. Your loan officer will confirm the exact current list for your situation.

When a Rate-and-Term Refinance Makes Sense

The strategy fits a handful of clear situations. You bought in a higher-rate stretch, such as 2022 or 2023, and rates have since come down. Your loan is adjusting off a fixed introductory period, or an interest-only period is ending and the payment is about to rise.

You used a bridge or hard money loan to acquire the property and now want long-term, stable financing. Or your DSCR is thin, and a lower payment would lift your coverage and give you more room before a future cash-out.

Break-Even and the Cost of Refinancing

A refinance is worth doing when the savings outrun the costs within a reasonable window. On the cost side, count closing costs, any points, reserve requirements, and one line item investors routinely forget: the prepayment penalty on your existing loan.

Many DSCR loans carry a prepayment penalty that a refinance can trigger, often on a step-down schedule that shrinks each year. If you are still early in that schedule, the penalty can outweigh the savings from a lower rate. HomeAbroad’s guide to the DSCR loan prepayment penalty walks through how those structures work.

The math is straightforward once you have the numbers. Add up the total cost to refinance, divide by your expected monthly savings, and you have the number of months to break even. If you plan to hold well past that point, the refinance usually earns its keep.

A prepayment penalty doesn’t automatically mean you should postpone refinancing. We compare the penalty, closing costs, and projected monthly savings to see how quickly the refinance pays for itself. Once investors understand that timeline, they can decide whether refinancing now or waiting a little longer better supports their investment goals.

When It Does Not Make Sense

Rate-and-term is the wrong tool in a few cases. If you need capital for your next acquisition, a cash-out refinance is the vehicle that actually delivers it. If a steep prepayment penalty is still active on your current loan, the savings may not clear the cost yet, and waiting may serve you better. And if appraised market rent will not support the new payment at your target LTV, the numbers may not work until rents or your equity position improve.

The Refinance Process and Timeline With HomeAbroad

The process is built to run remotely, which matters when you live outside the US.

- Pre-qualification. A conversation about the property and your goal, with a first read on realistic LTV and DSCR before any formal application.

- Documentation. You provide the file described above.

- Appraisal. HomeAbroad orders the appraisal, which sets the market value and the market-rent figure underwriting will use.

- Underwriting. The property’s DSCR, the LTV, your reserves, and your documentation are reviewed against current program guidelines.

- Closing. Once conditions are cleared, you close, often remotely, without needing to travel to the US.

Timelines vary with the property, the documentation, and market conditions, so treat any single figure as an estimate rather than a promise. A well-prepared file with a leased, stabilized property tends to move faster than one with open questions.

You can start by getting pre-qualified with HomeAbroad.

Rate-and-Term Refinance and Your US Tax Exposure

Because a rate-and-term refinance takes no cash out, it is not itself a taxable event, and it does not change your underlying US tax obligations on the property. It also does not reduce US estate-tax exposure. Under current rules, non-resident aliens generally receive only a $60,000 exemption on US-sited assets, which is far smaller than the exemption available to US citizens, and how you hold the property affects that exposure.

This is general information, not personalized tax advice. For anything involving your specific facts, or for how foreign-owner taxes such as FIRPTA apply when you eventually sell, work with a qualified US international tax professional and see HomeAbroad’s FIRPTA and foreign-owner tax rules guide.

Next Steps

If rates have moved since you bought, or your loan is shifting off a fixed or interest-only period, a rate and term refinance may lower your payment and strengthen your cash flow without touching your equity. The way to know is to run your property’s numbers against current pricing.

Get pre-qualified with HomeAbroad or request a personalized rate quote to see whether a rate-and-term refinance supports your investment goals. We’ll walk you through your property’s DSCR, estimated savings, and break-even timeline before you decide to refinance.

Frequently Asked Questions

Can I refinance if I bought the property in cash?

Often yes. Investors who purchased with cash may be able to refinance without the usual wait through a delayed-financing approach. Terms depend on the property and the current program, so confirm eligibility with a HomeAbroad loan officer.

Do I need US credit to qualify?

No established US credit history is required for HomeAbroad’s foreign national DSCR programs. Qualification is based on the property’s rental income. This is not the same as skipping a creditworthiness review or documentation.

Is there a waiting period for a rate-and-term refinance?

Rate-and-term refinances often carry lighter seasoning requirements than cash-out refinances, since no equity is being extracted. The exact requirement depends on your current loan and the program, so verify it before you apply.

Can I refinance a property held in an LLC?

Yes, LLC ownership is supported on most DSCR programs. You will provide your entity documents as part of the file.

What rate can I expect?

DSCR refinance rates move with the market and with your specific property, leverage, and reserves. Rather than quote a number that dates quickly, check HomeAbroad’s current DSCR loan rates for the latest ranges.