Editorial Integrity

Making informed real estate decisions starts with having the right knowledge. At HomeAbroad, we offer US mortgage products for foreign nationals & investors and have a network of 500+ expert HomeAbroad real estate agents to provide the expertise you need. Our content is written by licensed mortgage experts and seasoned real estate agents who share insights from their experience, helping thousands like you. Our strict editorial process ensures you receive reliable and accurate information.

A proof of funds letter shows a seller that you have the money available to complete the purchase.

Proof of funds, source of funds, and pre-approval are different documents used at different stages of the transaction.

Foreign buyers can use funds held in overseas accounts, but the documentation may require translation or additional verification.

Financing through HomeAbroad may reduce the amount you need to show compared to an all-cash purchase, depending on your loan program and transaction.

Table of Contents

A proof of funds letter is a document from your bank or financial institution confirming that you have the money available to complete a US property purchase. Sellers, listing agents, and lenders ask for one before they take an offer seriously, especially on all-cash deals or in competitive markets.

For a foreign buyer, though, the process usually looks different from what a US bank customer experiences. Your funds may sit in a foreign currency, your bank may not use the letter format a US seller expects, and getting everything translated and ready can take longer than the day or two a domestic buyer typically needs.

According to the National Association of Realtors, international buyers purchased about $56 billion in existing US homes. Most of those transactions passed through the same offer-stage checkpoint every buyer faces: proving they can pay for the property before a seller will take their offer seriously.

This guide explains what a proof of funds letter should include, how it differs from the source of funds documentation required during underwriting, and how financing through HomeAbroad can reduce the amount you need to prove before submitting an offer.

What Is a Proof of Funds Letter, and Why Do Sellers Ask for One

A proof of funds letter, often shortened to POF, is a short statement, usually on the letterhead of a bank or financial institution, confirming that an account holder has enough liquid money to cover a specific purchase. For an all-cash buyer, that means the full purchase price plus closing costs. For a financed buyer, it typically covers the down payment, closing costs, and any reserves the loan program requires.

No law requires a proof of funds letter. Sellers and their agents ask for one because they have no other way to know whether an offer is real. A buyer can write any number into a purchase agreement. A proof of funds letter is the evidence behind that number. In a competitive market, an offer that arrives without one is often treated as less serious than an otherwise identical offer that includes it, regardless of the buyer’s actual financial position.

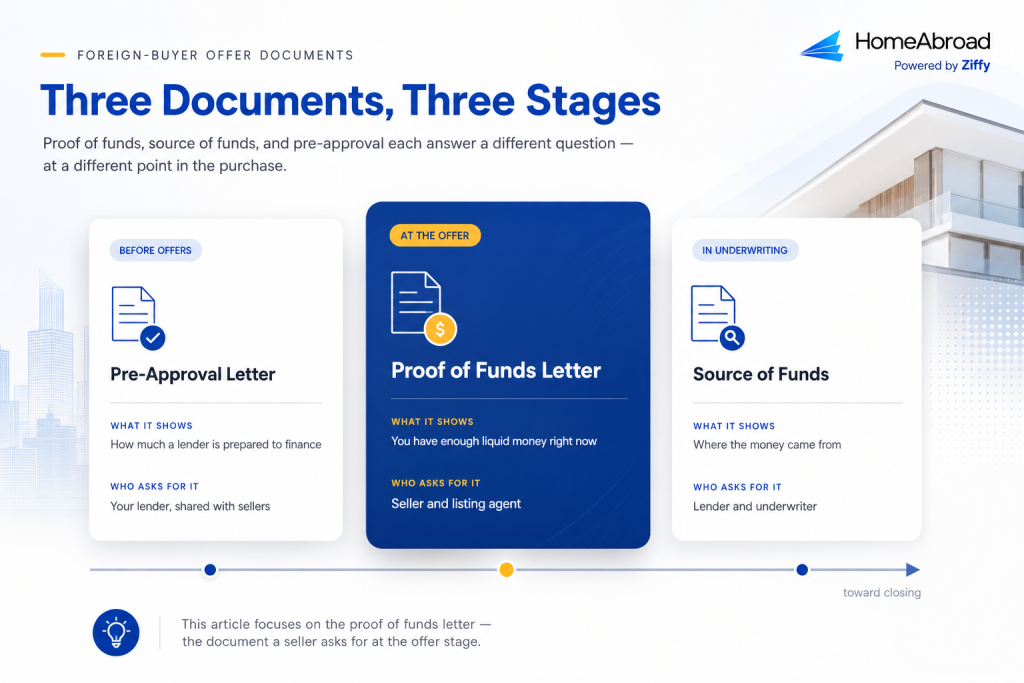

Proof of Funds vs. Source of Funds vs. Pre-Approval: Three Different Documents

Foreign buyers often assume these three documents are interchangeable, or that providing one satisfies the others. They serve different purposes at different points in the transaction, and a lender or seller asking for one does not mean the others are no longer needed.

Document | What It Shows | When It’s Requested | Who Asks For It |

|---|---|---|---|

Proof of funds letter | You currently have enough liquid money available | At or shortly after you make an offer | Seller, listing agent |

Source of funds documentation | Where that money came from and how it moved into your account | During mortgage underwriting | Lender, underwriter |

Pre-approval letter | A lender has reviewed your file and is prepared to lend up to a certain amount | Before you start making offers | Buyer’s lender, shared with sellers |

A proof of funds letter answers “do you have the money right now?” Source of funds documentation, which HomeAbroad reviews as part of underwriting on every foreign national mortgage file, answers a different question: where the money originated, whether large deposits are explained, and whether the paper trail holds up. If you’re gathering source of funds documentation for underwriting, the foreign national mortgage documents checklist walks through exactly what that process requires and how it differs from what’s covered here.

A pre-approval letter answers a third question entirely: how much HomeAbroad is prepared to finance. It’s not proof that you personally have money on hand; it’s a conditional commitment based on the information reviewed during pre-approval.

Foreign buyers often include both a pre-approval letter and a proof of funds letter with their offer, giving sellers confidence that financing is in place and the buyer has sufficient funds to complete the transaction. For the sequence and expected timeline, see the foreign national mortgage pre-approval guide.

What Your Proof of Funds Letter Needs to Include

There’s no single required format, but sellers and agents consistently look for the same core elements. A letter missing any of these is more likely to be questioned or rejected:

- The bank or financial institution’s name and contact information, on official letterhead

- The account holder’s name, matching the name that will appear on the purchase agreement

- The current balance, or a statement that the account contains sufficient funds to cover the transaction

- The date the letter was issued

- A signature from a bank official, with contact information for verification

Most sellers want a letter dated within the last 30 to 60 days. Screenshots of a mobile banking app, printouts of an online balance page, or informal emails are usually not accepted as a substitute for an official letter, even when the underlying balance is accurate. Some buyers attach a redacted bank statement alongside the letter, with the account number blacked out, as additional support.

Foreign Bank Accounts: Currency, Format, and Translation

This is often where the experience for foreign buyers begins to differ from a typical domestic transaction, and it’s a step many general homebuying guides overlook.

Many foreign banks don’t issue a document called a proof of funds letter the way US banks do. Instead, you may need to request a bank reference letter or an account confirmation letter that serves the same purpose.

Before requesting the document, confirm that your bank can include the account holder’s name, the date the balance was verified, and the current available balance. If the bank’s standard template doesn’t contain these details, ask whether they can issue a customized letter that meets the seller’s requirements.

If the account holds funds in a foreign currency, the letter should show the balance in that currency. You can also include an approximate US dollar equivalent for the seller’s convenience, but because exchange rates fluctuate, it should be clearly identified as an estimate rather than a fixed amount.

If the statement or letter isn’t in English, submit a certified or professional translation alongside the original document. An informal translation prepared by a friend, relative, or the buyer is unlikely to meet transaction requirements and can delay the review process.

Steven Glick

Director of Mortgage Sales · HomeAbroad

We’ve seen buyers with more than enough funds experience delays simply because their bank letter was missing key details or the translation didn’t meet the transaction requirements. Spending a little extra time preparing those documents upfront usually prevents much bigger delays later.

Because certified translation and cross-border communication with a foreign bank both take time, this step is often the biggest timing risk in the process. A US buyer may receive a proof of funds letter from their bank the same day they request it. A foreign buyer coordinating with an overseas bank, arranging a certified translation, and, in some cases, obtaining additional verification or notarization should expect the process to take longer.

Currency conversion and translation questions can also arise later during underwriting. If additional documentation is requested, our guide to foreign national mortgage letters of explanation explains how these situations are typically addressed.

How Much You Actually Need to Prove, and How Financing Changes the Number

One of the most common points of confusion for foreign buyers is assuming they need to prove the entire purchase price, regardless of whether they’re financing the property. That’s true for an all-cash buyer. It’s not true for a buyer using a mortgage.

An all-cash buyer generally needs a proof of funds letter covering the full purchase price plus estimated closing costs, since there’s no lender contributing to the transaction. A buyer financing the purchase through HomeAbroad typically only needs to show the down payment, closing costs, and any reserves the specific loan program requires, since HomeAbroad is providing the remaining balance.

Many international buyers assume they need to show the full purchase price to make a competitive offer. If you’re financing the property, that’s often not the case. Understanding your loan structure before requesting a proof of funds letter helps you present an offer that accurately reflects how the transaction will be funded.

Suppose a foreign buyer is purchasing a $500,000 US investment property with cash. In most cases, they would need to show proof of funds covering nearly the full purchase price, plus enough money to cover estimated closing costs.

Now consider the same property being financed through a DSCR loan. Because qualification is based primarily on the property’s rental income rather than the buyer’s personal income, the buyer would generally only need to show enough funds for the down payment, required reserves, and closing costs, which is often significantly less than the full purchase price.

The exact amount depends on the loan program, property type, and borrower profile. Before requesting your proof of funds letter, speak with a HomeAbroad mortgage specialist to confirm the documentation and funds required for your specific transaction.

For buyers deciding between programs, the DSCR loan guide and the Full Documentation Loan guide outline how each program qualifies borrowers and what documentation each one requires.

Getting Your Letter Ready Fast Enough to Compete

The biggest mistake foreign buyers make with proof of funds isn’t the letter itself; it’s timing. Waiting until an offer is accepted, or even until you’ve found a property, to start requesting a letter from a foreign bank often means the letter arrives after a seller has already moved on to another buyer.

I recommend requesting your proof of funds letter around the same time you begin the pre-approval process. When both are ready before you start making offers, you can move quickly on the right property instead of waiting on paperwork while other buyers are competing for the same deal.

Having both documents ready before you begin submitting offers allows you to respond quickly when the right property becomes available. It also gives you time to resolve any issues with your bank documentation before you’re working against a seller’s deadline.

Once you have a letter, keep an eye on how long it stays useful. If your property search runs past the 30- to 60-day window most sellers expect, request an updated letter rather than submitting an outdated one and hoping it isn’t questioned.

Protecting Your Financial Information When You Share It

A proof of funds letter contains sensitive information, including your bank’s name, your account holder name, and often your account balance. Before sending it, black out your account number if it’s visible on any attached statement. Share the letter only with parties who are actually part of the transaction: your real estate agent, your HomeAbroad loan officer, the seller’s agent, and the seller.

Avoid sending it over unsecured channels, and if a request for your financial documents seems unusual or comes from someone you can’t verify, confirm with your agent or loan officer before responding.

Start With Pre-Approval, Not Guesswork

Knowing how much proof of funds you’ll need starts with understanding your financing options. At HomeAbroad, we help foreign buyers determine the right loan program, estimate their down payment and reserve requirements, and identify the documentation needed before they begin making offers. That means you can request the right proof of funds letter the first time and move forward with confidence when the right property becomes available.

Ready to take the next step? Connect with a HomeAbroad mortgage specialist to explore your financing options and start your pre-approval with confidence.

Frequently Asked Questions

Do I need a proof of funds letter to make an offer on a US property?

It’s not legally required, but most sellers and listing agents expect one, especially for all-cash offers or in competitive markets. An offer submitted without a proof of funds letter is often treated as less serious than one that includes it.

Is a proof of funds letter the same as a pre-approval letter?

No. A proof of funds letter shows the money you already have available right now. A pre-approval letter shows how much a lender, such as HomeAbroad Loans, is prepared to lend you. Foreign buyers often submit both together, since the two documents cover different parts of the purchase.

Can I use a bank statement instead of an official letter?

Some sellers accept a recent bank or brokerage statement with the account number redacted, but most prefer a signed letter on official letterhead because it’s harder to alter and easier to verify. If you’re unsure which your seller expects, ask your agent before submitting your offer.

What if my funds are held in a foreign currency?

The letter should state the balance in the currency where the funds are held. You can note an approximate US dollar equivalent for the seller’s convenience, but label it as an estimate, since exchange rates change daily.

How long is a proof of funds letter valid?

Most sellers want a letter dated within the last 30 to 60 days. If your property search takes longer than expected, request an updated letter rather than submitting an outdated one.