Editorial Integrity

Making informed real estate decisions starts with having the right knowledge. At HomeAbroad, we offer US mortgage products for foreign nationals & investors and have a network of 500+ expert HomeAbroad real estate agents to provide the expertise you need. Our content is written by licensed mortgage experts and seasoned real estate agents who share insights from their experience, helping thousands like you. Our strict editorial process ensures you receive reliable and accurate information.

Transfer tax runs from 0% to over 4% depending on state, county, and city. There is no federal transfer tax.

Who pays is set by local custom and by contract, not by citizenship. Foreign buyers are charged the same rate as US citizens.

Some states, including Florida, New York, and Tennessee, impose additional mortgage-related taxes or recording charges. Confirm the requirements for the state where you’re buying and include those costs in your cash-to-close estimate.

Buying through a US LLC does not avoid transfer tax, and selling the LLC later can trigger it in some states.

Buyer-paid deed transfer taxes may become part of your property’s cost basis. Mortgage-related loan taxes are financing costs and generally receive different tax treatment.

Table of Contents

A real estate transfer tax is a one-time tax charged when property ownership moves from a seller to a buyer. It is calculated on the sale price, collected at closing, and has nothing to do with your citizenship. Rates range from zero in Texas and Wyoming to more than 4% of the purchase price in parts of New York City.

If you are financing your purchase, the tax on the deed is often not the largest number on your closing statement. Several states, including Florida, Georgia, Minnesota, New York, Tennessee, Virginia, Alabama, and the District of Columbia, impose mortgage-related taxes or recording charges in addition to the deed transfer tax. As a result, a cash buyer and a financed buyer can purchase the same property on the same day and walk away with different tax bills.

What a Real Estate Transfer Tax Is

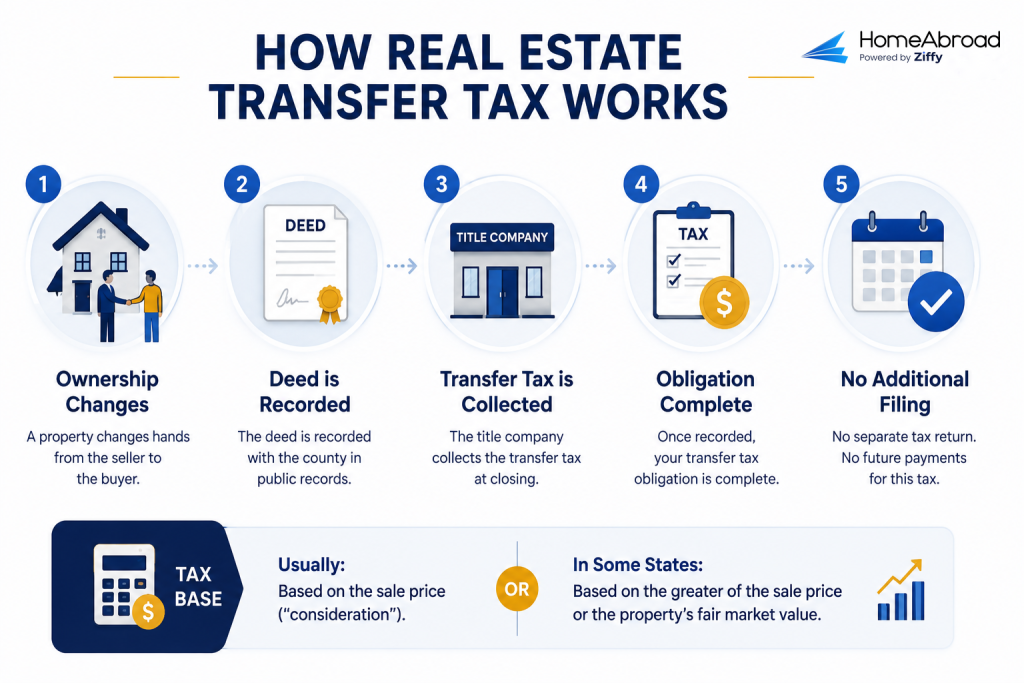

Every US state maintains public records showing who owns real property. In several states, a transfer tax is charged when ownership moves from one party to another and the deed is recorded. The tax is collected through the title company at closing. Once the deed is recorded, your transfer tax obligation is complete. You won’t file a separate tax return for it or pay it again.

The base is almost always the sale price, which US documents call the “consideration.” A few states use the greater of the price paid or the property’s fair market value, which matters if you are buying below market from a motivated seller.

The Different Names for the Same Tax

Searching for “transfer tax” in Florida and “transfer tax” in New Jersey returns two different words for the same event. This is the single biggest source of confusion for buyers comparing markets.

Term you will see | Where it is used |

|---|---|

Documentary stamp tax | Florida |

Real estate transfer tax (RETT) | New York, Michigan |

Realty transfer fee | New Jersey |

Recordation tax | Tennessee, Maryland, Washington DC |

Real estate excise tax | Washington |

Conveyance fee | Ohio, Connecticut |

Deed transfer tax | Pennsylvania, and common generic usage |

They all describe the same general concept: a tax imposed when ownership of real estate is transferred, although the calculation method and applicable rates vary by jurisdiction.

What Transfer Tax Is Not

Three costs get confused with transfer tax constantly, and the distinctions are worth fixing early because two of them are much larger.

- Property tax is annual and ongoing, assessed on the property’s assessed value by the local government. Transfer tax happens once.

- FIRPTA withholding is federal, and it applies to a foreign seller, not a buyer. It becomes relevant years later when you sell.

- Recording fees are flat administrative charges for physically filing the paperwork, usually somewhere between $50 and $250. They are a fee for a service, not a tax on the transaction value.

More on how these three separate out is in our guide to US taxes for foreign real estate buyers.

Who Pays the Transfer Tax, Buyer or Seller

There is no national rule. Who pays is decided by local custom, and custom is then written into the purchase contract, where it can be negotiated.

For example, in Florida and New York, the seller typically pays the deed transfer tax by convention. In Tennessee, state law places the realty transfer tax on the grantee, which is the buyer. In Michigan, transfer taxes are customarily paid by the seller, while in Pennsylvania, they are often split between the buyer and seller unless the purchase agreement specifies otherwise.

Two exceptions are worth knowing before you write an offer:

The first is New York’s mansion tax, which is buyer-paid by statute. A contract that shifts it to the seller does not release you if the seller fails to pay. The obligation follows the buyer.

The second is Miami-Dade County, where custom flips the deed tax onto the buyer even though the rest of Florida puts it on the seller.

Citizenship Does Not Change the Rate

This is worth stating plainly, because it is a question we get constantly and the answer is reassuring.

Transfer tax rates are set by where the property sits and what it sold for. Not by who is buying it. A nonresident alien buying a $500,000 house in Orlando pays exactly the same documentary stamp tax as a Florida resident buying the identical house. There is no foreign buyer surcharge, no different bracket, and no additional filing.

Some countries do charge non-residents extra to buy property. The United States does not do this at the state transfer tax level.

Steven Glick

Director of Mortgage Sales · HomeAbroad

Transfer tax is just one part of your cash to close, so I encourage investors to look at the entire offer rather than negotiating a single cost. If you decide to absorb the transfer tax to strengthen your offer, we factor that into your required funds during pre-qualification so there are no surprises later.

Transfer Tax Rates in Major Foreign Buyer Markets

State | Deed tax rate | Mortgage-Related Tax | Who Commonly Pays? |

|---|---|---|---|

Florida | $0.70 per $100 ($0.60 in Miami-Dade, plus applicable surtax) | Yes. Note documentary stamp tax and 0.2% nonrecurring intangible tax | Seller pays deed tax by custom (buyer in Miami-Dade). Buyer pays mortgage-related taxes. |

Georgia | Approximately 0.10% | Yes. Intangible recording tax of approximately 0.30% on qualifying loans | Deed tax typically seller; mortgage-related tax generally paid by the borrower. |

Minnesota | 0.33% | Yes. Mortgage Registry Tax of 0.23% (0.24% in Hennepin and Ramsey counties) | Seller generally pays deed tax; borrower pays the Mortgage Registry Tax. |

New York | State 0.4%, with additional NYC taxes where applicable | Yes. Mortgage Recording Tax applies in New York and is higher in New York City | Seller pays deed transfer tax. Buyer pays the mansion tax and mortgage recording tax where applicable. |

Tennessee | $0.37 per $100 | Yes. Indebtedness tax of $0.115 per $100 (first $2,000 exempt) | Buyer (grantee) pays both by statute. |

Virginia | $0.25 per $100 (plus applicable local recordation taxes) | Yes. Deed of trust recordation tax | Buyer generally pays recordation taxes; seller pays the grantor’s tax. |

Alabama | Approximately 0.10% | Yes. Mortgage tax of 0.15% | Deed tax commonly paid by the seller; mortgage tax generally paid by the borrower. |

District of Columbia | 1.1% to 1.45% | Yes. Recordation tax on deeds of trust | Transfer tax generally seller; recordation costs commonly buyer. |

California | 0.11% county tax (cities may add additional taxes) | No | Varies by county; commonly seller in Southern California. |

Michigan | Approximately 0.86% combined state and county | No | Seller (grantor) by statute. |

Nevada | Approximately 0.39% statewide (county surcharges may apply) | No | Grantor and grantee are jointly liable under state law. |

Washington | Graduated rates starting at 1.10%, plus local taxes where applicable | No | Seller is generally responsible, with buyer liability if unpaid. |

Oklahoma | Approximately 0.15% | Yes. Mortgage registration tax | Seller commonly pays deed tax. |

States With No Transfer Tax

A meaningful number of states charge no state-level transfer tax. Texas is the headline for many of our clients because it is one of the largest markets we finance and carries no state transfer tax. Kansas also does not impose a state-level transfer tax.

Keep in mind that the absence of a state transfer tax does not always mean a lower cost of buying. Some states still charge recording fees or local taxes. For example, Colorado does not impose a traditional state real estate transfer tax but does charge a documentary fee, while Oregon has no state transfer tax but certain local jurisdictions, such as Washington County, impose their own transfer tax.

A state with no transfer tax is not automatically the least expensive place to own real estate. Texas has no state transfer tax, but it also has some of the highest annual property tax rates in the country. Looking at your total ownership costs over your expected holding period is often more important than focusing on transfer tax alone.

The Transfer Tax Most Foreign Buyers Miss: Taxes on the Mortgage

Several states treat your mortgage as a separate taxable document from your deed. The deed transfers the property. The mortgage creates a debt, and recording that debt is a separate taxable event with its own rate. For financed purchases, those mortgage-related taxes generally become the buyer’s responsibility.

Florida Taxes the Loan, Not Just the Deed

On a financed purchase, Florida can impose three separate taxes at closing:

- Deed documentary stamp: $0.70 per $100 of the price, rounded up to the next full $100. Seller pays by custom.

- Note documentary stamp: $0.35 per $100 of the loan amount, also rounded up. Buyer pays.

- Nonrecurring intangible tax: 0.2% of the loan, calculated on the exact amount with no rounding. Buyer pays.

Take a $500,000 purchase in Palm Beach County with a $375,000 loan, which is the 25% down structure many of our DSCR files use:

Line | Calculation | Amount | Paid by |

|---|---|---|---|

Deed doc stamp | 5,000 units × $0.70 | $3,500 | Seller |

Note doc stamp | 3,750 units × $0.35 | $1,312.50 | Buyer |

Intangible tax | $375,000 × 0.002 | $750 | Buyer |

Buyer’s total | $2,062.50 |

That $2,062.50 exists only because the purchase is financed. A cash buyer in the same county on the same house pays none of it.

Georgia Also Taxes Long-Term Mortgages

Georgia imposes an intangible recording tax on long-term mortgage notes, making it another important state for financed buyers to understand.

For qualifying loans, the tax is $1.50 per $500 of the loan amount (approximately 0.30%), subject to a maximum tax of $25,000. The tax generally applies to notes with a maturity longer than 62 months, which includes most investment property mortgages.

Unlike Florida, Georgia also provides a planning opportunity. A qualifying refinance with the same lender and borrower may be exempt up to the unpaid principal balance of the original loan, reducing the tax due on the refinance.

If you’re financing an investment property in Georgia, confirm whether the intangible recording tax applies to your transaction and include it in your cash-to-close estimate.

New York City Can Produce the Largest Closing Tax

New York’s mortgage recording tax runs 1.8% on loans under $500,000 and 1.925% at $500,000 and above, calculated on the loan rather than the price.

On a $720,000 mortgage, that is $13,860, wired the day the mortgage is recorded. For most financed NYC buyers it is the single largest line on the closing statement, larger than title insurance and larger than the attorney fees.

It also stacks. If the property is residential and the price is $1 million or more, the mansion tax applies on top, and the buyer pays both.

One structural quirk: co-op purchases are transfers of shares in a corporation rather than transfers of real property, so the mortgage recording tax does not apply to them. This is one of the few facts that genuinely changes the number.

Tennessee Charges It Too, and the Buyer Pays Both

Tennessee is the market most people miss on this, and it is one we lend in heavily.

Tennessee’s recordation tax is actually two taxes. The realty transfer tax is $0.37 per $100 of the greater of the price or the property’s value, and state law places it on the grantee, which means the buyer. The indebtedness tax is $0.115 per $100 of the loan, with the first $2,000 exempt, and it falls on the debtor, which also means the buyer.

On a $350,000 Nashville purchase with a $262,500 loan:

- Realty transfer tax: $350,000 × 0.0037 = $1,295

- Indebtedness tax: ($262,500 − $2,000) × 0.00115 = $299.58

- Buyer’s total: roughly $1,595

The rates are modest. The point is that both land on the buyer, unlike Florida where the seller absorbs the larger of the two by custom. A Tennessee buyer carries the whole thing.

Why This Matters When You Are Comparing Markets

None of this argues for paying cash. A one-time cost of roughly 0.55% of the loan in Florida is small next to what leverage does for a portfolio. The same capital that buys one property outright can control three financed ones, and our clients recycle capital through cash-out refinancing precisely because that math works.

The point is narrower. This cost belongs in your model, and it usually is not there. Foreign buyers comparing an Orlando purchase against a Dallas purchase often compare price, rent, and property tax, then discover the loan taxes on the Closing Disclosure three days before funding.

At HomeAbroad, we finance foreign national purchases in all of these markets, and our pre-qualification builds state-specific loan taxes into the cash-to-close figure from the start. That is why our Florida and New York estimates read higher than a generic national closing cost calculator. The calculator is not wrong about the deed. It just does not know your loan is taxable.

If you are weighing which loan structure fits, our DSCR loan program qualifies you on the property’s rental income rather than your personal income, which is the structure most of our international investors use.

The biggest issue isn’t the tax itself. It’s finding out about it when the Closing Disclosure is issued. If the note stamps and intangible tax weren’t included in the original cash-to-close estimate, buyers may need to wire additional funds at the last minute, which can delay closing if they’re moving money internationally.

Cash Buyer vs Financed Buyer: Same House, Different Tax Bill

The example below compares the transfer-tax-related costs for the same $500,000 Orlando property under two financing scenarios. Calculation using stated assumptions. Illustration only. Not a client transaction.

Line item | All-cash buyer | Financed buyer ($375,000 loan) |

|---|---|---|

Deed doc stamp | $3,500 (seller pays by custom) | $3,500 (seller pays by custom) |

Note doc stamp | $0 | $1,312.50 |

Intangible tax | $0 | $750.00 |

Buyer’s out-of-pocket | $0 | $2,062.50 |

Worth holding both facts at once. The National Association of Realtors reported that foreign buyers purchased roughly $56 billion in US residential real estate between April 2024 and March 2025, and nearly half of those purchases were all-cash. Many international buyers therefore never incur mortgage-related taxes.

For financed buyers, however, the additional $2,062.50 equals about 0.4% of the purchase price while preserving $375,000 of capital that can be deployed elsewhere. That is a line item to budget, not a reason to change your investment strategy.

Mansion Taxes and High-Price Surcharges

New York’s mansion tax applies to residential transfers of $1 million or more, runs from 1% to 3.9% depending on the purchase price, and is paid by the buyer.

The structure has a trap in it. The brackets are cliffs, not marginal rates. The entire purchase price is taxed at the applicable bracket rate, so a purchase at $2,000,001 is taxed at 1.25% on the full purchase price, not just on the dollar above the threshold.

Watch the thresholds carefully. A purchase at $999,999 owes no mansion tax. At $1,000,000, the buyer owes $10,000. Negotiating a purchase price below a threshold can produce meaningful savings.

New York also imposes a 0.25% supplemental transfer tax on residential sales of $3 million or more.

High-value transfer taxes aren’t unique to New York. Los Angeles City’s Measure ULA imposes additional transfer taxes of 4% on sales from $5.4 million to $10.9 million and 5.5% on sales above $10.9 million. Other jurisdictions, including New Jersey, also impose high-price transfer tax surcharges.

Because these thresholds and rates change more frequently than standard transfer taxes, always confirm the current enacted rules for the city and state where you’re buying before relying on published figures.

Buying Through a US LLC Does Not Avoid Transfer Tax

Most of the foreign national investors we finance hold property through a US limited liability company. It is a sensible structure for liability separation and for keeping investment and personal finances clean.

It does not avoid transfer tax. Buying property into an LLC is still a conveyance. The deed still moves from the seller to your entity, and the tax applies at purchase exactly as it would if you bought in your own name.

The assumption that causes problems comes later. Some investors plan to sell the LLC rather than the property, assuming that if the deed never changes hands, transfer tax does not apply. In New York, that approach generally doesn’t work.

Tax Law §1401 treats the transfer or acquisition of a controlling interest in an entity that owns real property as a taxable conveyance, with the tax measured on the fair market value of the underlying real estate. New York isn’t alone. States including Washington, Michigan, and Maryland also have controlling-interest provisions, although the ownership thresholds, look-back periods, and filing requirements differ by jurisdiction.

Whether a specific entity transfer triggers tax in a specific state is a question for a US tax attorney or a CPA licensed there. The reason to raise it here is timing: this is a question worth asking before you buy, when the ownership structure is still a choice, rather than after, when unwinding it creates its own taxable event.

There is a financing dimension too, and this one is ours. Your vesting has to match your loan documents exactly. Restructuring ownership after closing to chase a tax outcome creates a mismatch between the title record and the loan file, and that mismatch causes real problems on the next refinance. How ownership is structured also affects loan eligibility in the first place, which our guide to how title and vesting work for foreign buyers covers in detail.

Changing the vesting from your personal name to an LLC after the loan process has started usually means updating the loan application, entity documents, disclosures, and sometimes parts of underwriting. It’s much easier to decide on the ownership structure before applying, because mid-process changes can add several days to the timeline.

Exemptions, and Why They Rarely Help Buyers

Most states exempt certain transfers, including transfers between spouses, gifts with nominal consideration, transfers to government bodies, certain trust transfers, and some intra-family transfers.

Here’s the precise framing, because this gets stated inaccurately in many places. These exemptions depend on the nature of the transfer, not on the citizenship of the parties. A nonresident alien transferring property to a spouse in Broward County is treated under the same statute as a US citizen making the same transfer. There is no exemption you lose by being foreign, and none you gain by becoming a US resident.

For most foreign national investors, these exemptions won’t apply. An arm’s-length purchase from an unrelated seller, which describes nearly every transaction we finance, is generally subject to the applicable transfer taxes. Budget the full amount.

Transfer Tax, FIRPTA, and Property Tax Are Three Different Things

Transfer tax | FIRPTA withholding | Property tax | |

|---|---|---|---|

When | Once, at closing | Once, at sale | Every year |

Who it hits | Buyer, seller, or both by custom | The foreign seller | The owner |

Calculated on | Sale price | Gross sale price | Assessed value |

Rate | 0% to 4%+ by location | Tiered: 0% / 10% / 15% | Local, roughly 0.3% to 2.5% |

Level | State, county, city | Federal | Local |

FIRPTA withholding follows a tiered structure of 0%, 10%, or 15%, depending on the sale price and the buyer’s intended use of the property. Many sources mention only the 15% rate, but that applies only to the highest withholding tier.

Similarly, US tax treaties generally do not reduce FIRPTA withholding for an individual nonresident alien seller. When a reduced withholding amount is appropriate, the mechanism is IRS Form 8288-B, not the applicable tax treaty.

Both topics are covered properly in our FIRPTA withholding rules guide.

How Transfer Tax Affects Your Numbers at Exit

Transfer tax isn’t deductible against your rental income, but certain purchase costs can still affect your tax position when you eventually sell.

Buyer-paid deed transfer taxes may become part of your property’s cost basis, while mortgage-related loan taxes are financing costs and generally receive different tax treatment.

For foreign investors, cost basis directly affects the taxable gain on a sale. A higher basis generally means a lower taxable gain, which can reduce your overall US capital gains exposure. It may also support a stronger Form 8288-B application when requesting a reduction in FIRPTA withholding, depending on your specific tax situation.

One trap worth naming: a foreign seller still needs Form 8288-B to reduce FIRPTA withholding even inside a 1031 exchange. The exchange defers the gain. It does not eliminate the withholding requirement by itself. Our 1031 exchange rules for foreign investors guide explains how the two rules interact.

Tracking your basis and preparing a Form 8288-B application are tasks for a qualified CPA. Keep your Closing Disclosure and settlement documents, as they help substantiate purchase costs when calculating your property’s adjusted basis and preparing future tax filings.

Where Transfer Tax Fits in Your Cash to Close

Four steps, in order:

- Confirm the state and county rate, and who pays by local custom. County add-ons often exceed the state rate itself.

- Add mortgage-related taxes separately. Check whether your state or local jurisdiction imposes additional mortgage-related taxes or recording charges, and include those costs in your cash-to-close estimate.

- Add mansion tax if the price crosses a threshold. In New York this is buyer-paid and cannot be contracted away.

- Add the total to your down payment, closing costs, and program reserves. Use that figure when planning your wire transfer rather than relying on an estimate prepared before you selected a market.

That total feeds one more document. A financed buyer’s proof of funds letter needs to cover down payment, closing costs, and reserves. Underestimating transfer tax by $10,000 in New York produces a letter that under-documents what the transaction actually requires, and sellers notice. Our guide to proof of funds letter requirements covers how much you actually need to show.

Getting the Number Right Before You Wire

Transfer tax is one of the few closing costs you can estimate with a high degree of confidence before closing. The applicable rates are published, but the final amount depends on the property’s location, purchase price, financing structure, loan amount, and any applicable state or local mortgage-related taxes.

The part that goes wrong is scope. Buyers account for the deed transfer tax but overlook mortgage-related taxes, only discovering the difference when the Closing Disclosure arrives a few days before closing.

At HomeAbroad, we specialize in helping foreign nationals finance US real estate without requiring US credit history for eligible loan programs. As part of the pre-qualification process, we estimate your down payment, closing costs, reserves, and applicable transfer taxes so you know how much you’ll need before you wire funds.

Get pre-qualified and see the full cash-to-close for the market you are actually considering.

Frequently Asked Questions

Do foreign buyers pay a higher transfer tax than US citizens?

No. The rate is set by the property’s location and its sale price. Citizenship, residency, and visa status do not change it. There is no foreign buyer surcharge at the state transfer tax level in the United States.

Is transfer tax due when I refinance?

No. Ownership does not change in a refinance, so no transfer tax applies. But the mortgage taxes do. A cash-out refinance in New York triggers the mortgage recording tax again on the new loan, and a Florida refinance triggers note stamps and intangible tax again. In states with higher transfer taxes this can meaningfully change whether a refinance pencils.

Can transfer tax be added to my loan?

No. It is a cash cost due at closing and cannot be financed into the mortgage.

Which states have no transfer tax?

Texas and Kansas do not impose a state-level real estate transfer tax. However, local recording fees or other closing costs may still apply, and some jurisdictions can impose their own charges. Always confirm the requirements for the specific state, county, and city where you’re buying.

Do I need an ITIN to pay transfer tax?

No. An Individual Taxpayer Identification Number, which is the tax ID issued to people who are not eligible for a Social Security Number, is not required for this. Transfer tax is collected by the county through your title company at closing and is not reported on a personal tax return.